US Medical Robots Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2773

December 2024

85

About the Report

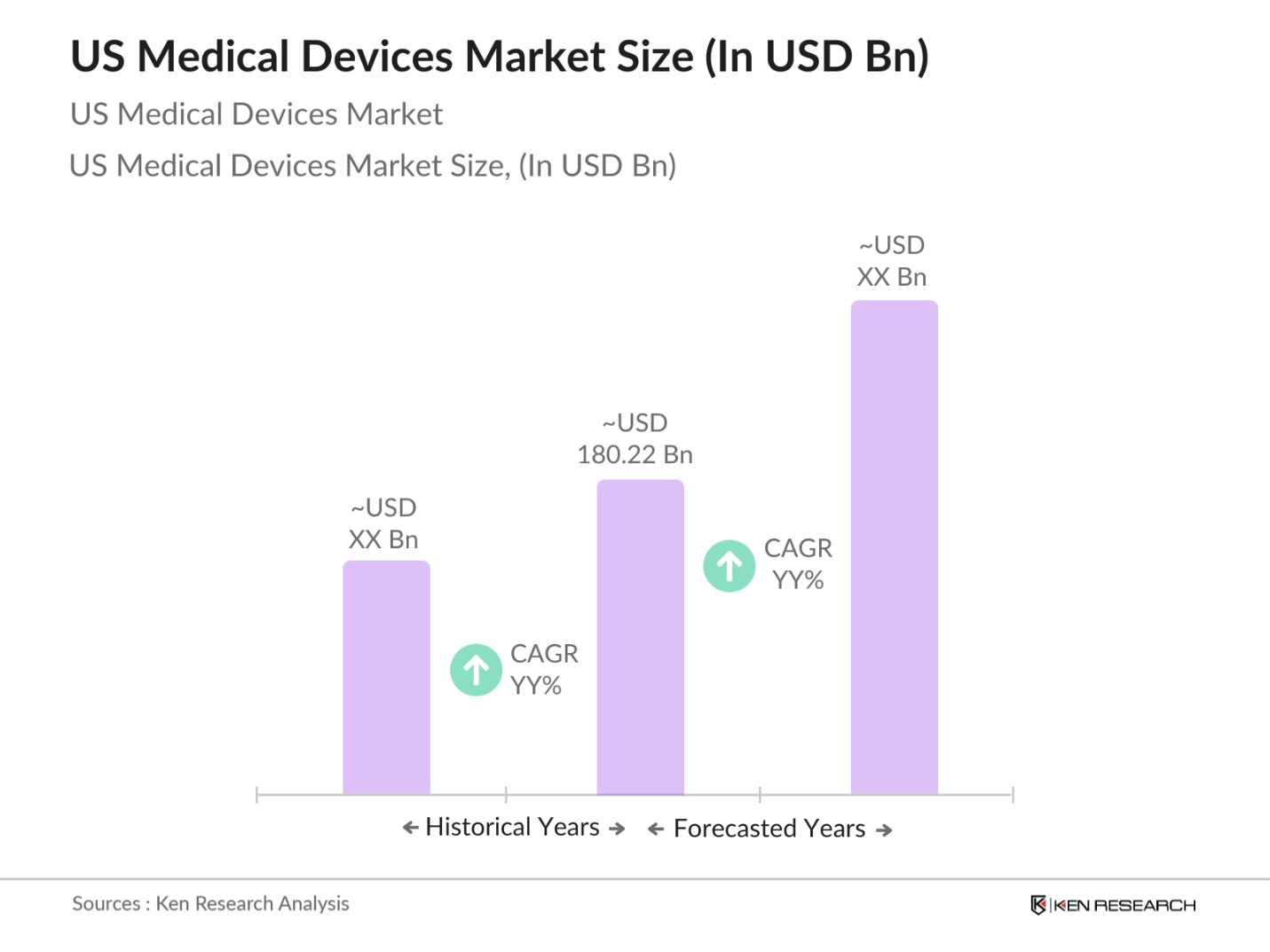

US Medical Devices Market Overview

- The US Medical Devices Market is valued at USD 180.22 billion, reflecting a robust growth trajectory driven by an aging population, increasing prevalence of chronic diseases, and continuous advancements in technology. The market dynamics are underpinned by a strong focus on innovation, resulting in the introduction of advanced medical devices that cater to the evolving healthcare needs.

- Key cities such as New York, San Francisco, and Boston play a pivotal role in the US Medical Devices Market due to their concentration of leading healthcare institutions, research facilities, and innovative startups. These cities are home to significant healthcare expenditures and a robust ecosystem that fosters collaboration between medical device manufacturers, healthcare providers, and research organizations. This concentration of resources and talent positions them as dominant players in the market, driving growth through innovation and high-quality healthcare services.

- The U.S. Food and Drug Administration (FDA) has launched several initiatives aimed at fostering innovation in medical devices. The FDA's Breakthrough Devices Program is designed to expedite the review process for devices that provide more effective treatment or diagnosis of life-threatening or irreversibly debilitating diseases. As of 2023, this program has seen a significant increase in applications, indicating a robust commitment to supporting innovative technologies that improve patient care and outcomes.

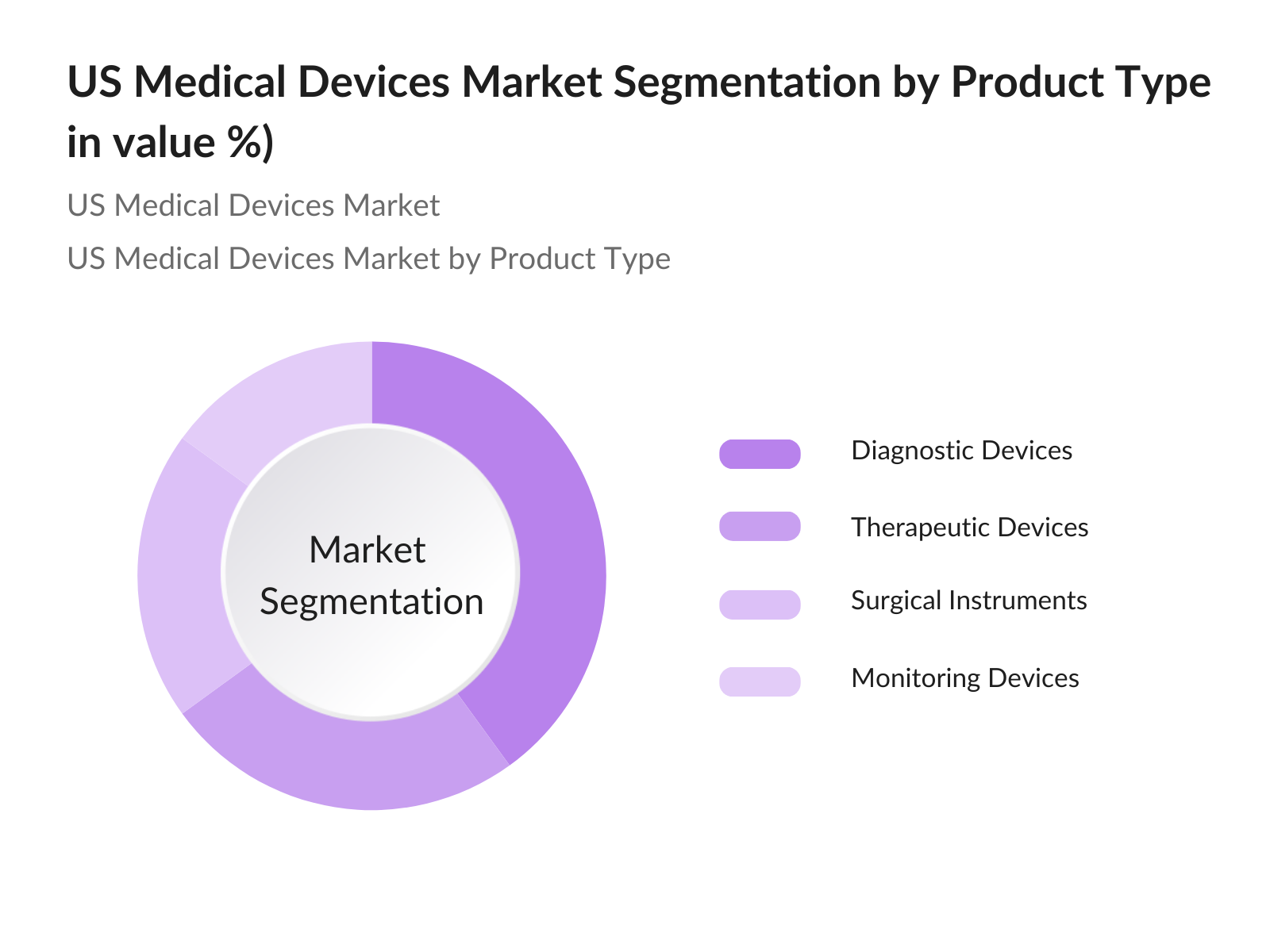

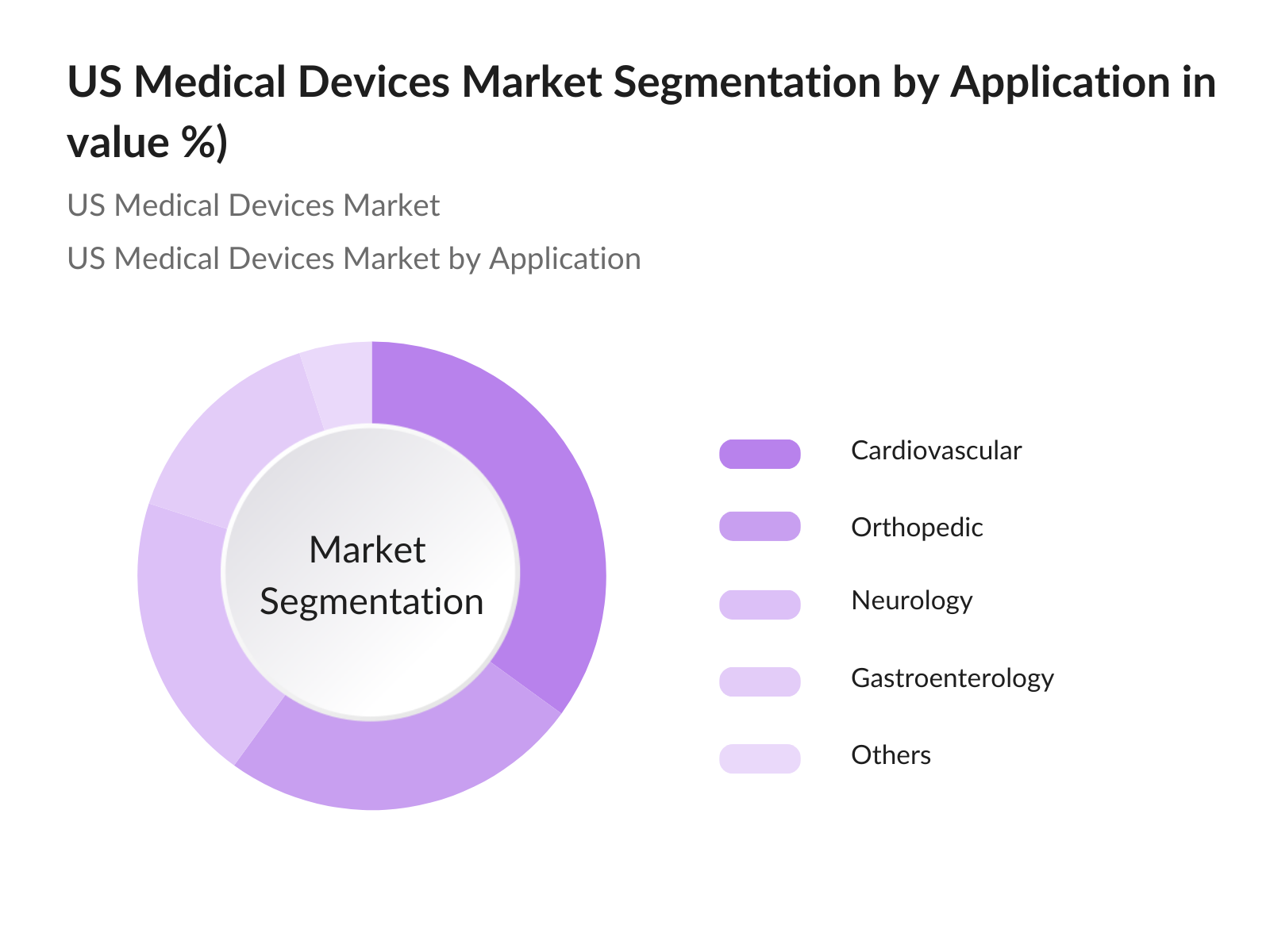

US Medical Devices Market Segmentation

By Product Type: The US Medical Devices Market is segmented by product type into diagnostic devices, therapeutic devices, surgical instruments, and monitoring devices. Diagnostic devices currently hold a dominant market share, primarily due to the increasing demand for early disease detection and ongoing innovations in imaging technologies. The continuous advancement in diagnostic imaging modalities, such as MRI and CT scans, has significantly improved the accuracy and speed of diagnoses, making them essential in modern healthcare settings.

By Application: Market segmentation by application includes cardiovascular, orthopedic, neurology, and gastroenterology. Cardiovascular devices dominate the market, driven by the increasing incidence of heart diseases and related conditions. With the rise in lifestyle-related risk factors, there is a growing demand for devices such as stents, pacemakers, and defibrillators. This segment benefits from extensive research and development, leading to enhanced device efficacy and safety, thereby boosting its market presence.

US Medical Devices Market Competitive Landscape

The US Medical Devices Market is characterized by a competitive landscape with several major players. The market is dominated by key companies, including Medtronic, Johnson & Johnson, and Siemens Healthineers. This consolidation highlights the significant influence of these key companies, which drive innovation and maintain market leadership through extensive R&D and robust distribution networks.

|

Company |

Establishment Year |

Headquarters |

Product Portfolio |

Revenue (USD Bn) |

Market Presence |

R&D Expenditure |

Number of Employees |

Major Partnerships |

|

Medtronic |

1949 |

Minneapolis, MN |

Cardiovascular, Neurology |

- |

- |

- |

- |

- |

|

Johnson & Johnson |

1886 |

New Brunswick, NJ |

Orthopedic, Surgical |

- |

- |

- |

- |

- |

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

Diagnostic Imaging |

- |

- |

- |

- |

- |

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

Monitoring Devices |

- |

- |

- |

- |

- |

|

Abbott Laboratories |

1888 |

Abbott Park, IL |

Diagnostic Devices |

- |

- |

- |

- |

- |

US Medical Devices Market Analysis

Market Growth Drivers

- Aging Population: The U.S. population aged 65 and older is projected to reach 78 million. This demographic shift significantly increases the demand for medical devices, particularly those catering to age-related health issues. In 2022, many adults aged 65 or older reported having two or more chronic conditions, underscoring the need for innovative medical solutions. The elderly population is expected to reach 54 million, further intensifying the market demand for devices such as monitoring systems and mobility aids. This growing segment of the population necessitates advancements in medical technology to address their specific health needs.

- Rise in Chronic Diseases: Chronic diseases are a leading cause of mortality in the U.S., with 6 in 10 adults living with at least one chronic disease as of 2023. The prevalence of conditions such as diabetes and heart disease is on the rise, necessitating advanced medical devices for management and treatment. For example, diabetes prevalence is projected to increase to 54.4 million individuals by 2025, creating a significant demand for monitoring and therapeutic devices. Moreover, healthcare costs related to chronic diseases are expected to exceed $1 trillion annually by 2024, which reflects the urgent need for effective medical interventions.

- Technological Advancements: Technological advancements are pivotal in transforming the medical devices landscape. As of 2023, a significant number of hospitals in the U.S. have implemented advanced technologies such as telehealth and remote monitoring systems. Innovations in artificial intelligence and machine learning are enhancing diagnostic accuracy and patient outcomes. For instance, the integration of AI in imaging devices has led to substantial improvements in early detection rates for certain cancers, thereby improving treatment timelines. The continued adoption of AI technologies among U.S. healthcare providers is expected to further propel the market growth of sophisticated medical devices.

Market Challenges:

- Stringent Regulatory Requirements: The regulatory environment for medical devices in the U.S. is rigorous, with the Food and Drug Administration (FDA) overseeing the approval of new technologies. In 2022, the FDA received over 4,000 premarket notifications, indicating the high barrier to entry for manufacturers. The process can take up to 510 days for review, delaying product launches and increasing costs. These stringent regulations, while essential for ensuring safety and efficacy, create challenges for companies attempting to innovate swiftly.

- High Costs of Research and Development: The average cost of developing a new medical device can exceed $2.3 billion, with significant investments required for research and clinical trials. As of 2023, many medical device companies report that high R&D costs significantly impede their ability to innovate and bring new products to market. Additionally, it typically takes several years to move from concept to market, which poses financial risks for companies, particularly small and mid-sized enterprises. These high costs are a substantial barrier to entry and can stifle competition within the industry.

US Medical Devices Market Future Outlook

Over the next five years, the US Medical Devices Market is expected to show significant growth driven by continuous government support, advancements in medical technology, and increasing consumer demand for high-quality healthcare solutions. As the population ages and healthcare needs evolve, there will be a surge in demand for innovative medical devices that enhance patient outcomes and improve quality of life. Furthermore, the trend towards personalized medicine and minimally invasive procedures will further fuel market expansion, as healthcare providers seek to offer tailored solutions to patients.

Market Opportunities:

- Adoption of Wearable Devices: Wearable medical devices have seen a surge in adoption, with estimates indicating that the number of connected wearable devices will reach 1 billion units by 2024. This trend is driven by increasing consumer demand for personal health monitoring solutions, particularly in managing chronic conditions. As of 2023, many patients with chronic diseases are using wearable devices to track their health metrics, showcasing a shift towards proactive health management. This growing market segment provides immense opportunities for manufacturers focusing on innovation in wearables.

- Shift Towards Minimally Invasive Procedures: Minimally invasive procedures are becoming more prevalent, with 1.5 million minimally invasive surgeries performed in the U.S. in 2022. This trend is largely driven by advancements in surgical technology and an increased focus on patient recovery times. Many surgeons have reported an increase in patient demand for such procedures, emphasizing the need for innovative medical devices designed for minimally invasive interventions. As these procedures continue to gain traction, the market for related medical devices is expected to expand significantly.

Scope of the Report

|

By Product Type |

Diagnostic Devices Therapeutic Devices Surgical Instruments Monitoring Devices Others |

|

By Application |

Cardiovascular Orthopedic Neurology Gastroenterology Others |

|

By Technology |

Electronic Devices Bioelectric Devices Software-based Devices |

|

By End-User |

Hospitals Clinics Home Healthcare |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Medical Device Manufacturers

Healthcare Providers

Hospitals and Clinics

Investment and Venture Capitalist Firms

Government and Regulatory Bodies (FDA, CDC)

Research Institutions

Insurance Companies

Distributors and Suppliers

Companies

Players Mention in the Report

Medtronic

Johnson & Johnson

Siemens Healthineers

Philips Healthcare

Abbott Laboratories

GE Healthcare

Stryker Corporation

Boston Scientific

Becton, Dickinson and Company

Thermo Fisher Scientific

3M Company

Zimmer Biomet

Terumo Corporation

Hologic Inc.

Intuitive Surgical

Table of Contents

01. US Medical Devices Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Growth Rate

02. US Medical Devices Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03. US Medical Devices Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population

3.1.2. Rise in Chronic Diseases

3.1.3. Technological Advancements

3.1.4. Increased Healthcare Expenditure

3.2. Market Challenges

3.2.1. Stringent Regulatory Requirements

3.2.2. High Costs of Research and Development

3.3. Opportunities

3.3.1. Emerging Markets

3.3.2. Digital Health Innovations

3.3.3. Strategic Collaborations

3.4. Trends

3.4.1. Adoption of Wearable Devices

3.4.2. Shift Towards Minimally Invasive Procedures

3.5. Government Regulation

3.5.1. FDA Regulatory Framework

3.5.2. Health Insurance Portability and Accountability Act (HIPAA)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

04. US Medical Devices Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Diagnostic Devices

4.1.2. Therapeutic Devices

4.1.3. Surgical Instruments

4.1.4. Monitoring Devices

4.1.5. Others

4.2. By Application (In Value %)

4.2.1. Cardiovascular

4.2.2. Orthopedic

4.2.3. Neurology

4.2.4. Gastroenterology

4.2.5. Others

4.3. By Technology (In Value %)

4.3.1. Electronic Devices

4.3.2. Bioelectric Devices

4.3.3. Software-based Devices

4.4. By End-User (In Value %)

4.4.1. Hospitals

4.4.2. Clinics

4.4.3. Home Healthcare

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

05. US Medical Devices Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Medtronic

5.1.2. Johnson & Johnson

5.1.3. Siemens Healthineers

5.1.4. Philips Healthcare

5.1.5. Abbott Laboratories

5.1.6. GE Healthcare

5.1.7. Stryker Corporation

5.1.8. Boston Scientific

5.1.9. Becton, Dickinson and Company

5.1.10. Zimmer Biomet

5.1.11. Thermo Fisher Scientific

5.1.12. 3M Company

5.1.13. Baxter International

5.1.14. Terumo Corporation

5.1.15. Hologic Inc.

5.2. Cross Comparison Parameters (Revenue, R&D Expenditure, Number of Employees, Geographic Presence, Product Portfolio, Market Share, Partnerships, Customer Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

06. US Medical Devices Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

07. US Medical Devices Market Future Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08. US Medical Devices Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

09. US Medical Devices Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the US Medical Devices Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the US Medical Devices Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATI) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple medical device manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the US Medical Devices Market.

Frequently Asked Questions

01. How big is the US Medical Devices Market?

The US Medical Devices Market is valued at USD 180.22 billion, driven by advancements in technology, an aging population, and increasing healthcare expenditures.

02. What are the challenges in the US Medical Devices Market?

Challenges in the US Medical Devices Market include stringent regulatory requirements, high costs of research and development, and competition from emerging market players that may disrupt established business models.

03. Who are the major players in the US Medical Devices Market?

Key players in the US Medical Devices Market include Medtronic, Johnson & Johnson, Siemens Healthineers, and Abbott Laboratories, known for their extensive product portfolios and significant market presence.

04. What are the growth drivers of the US Medical Devices Market?

The US Medical Devices Market is propelled by factors such as an aging population, rising chronic diseases, and technological advancements that enhance the efficacy and safety of medical devices.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.