India’s Kiwi Market Is Racing Toward ₹95 Billion, But 70% Still Comes from Imports: Can India Ever Compete with New Zealand and Chile?

Ken Research

January 22, 2026 - 5 min read

January 22, 2026

by Khushi RastogiIndia’s kiwi fruit market has evolved from a niche premium segment into a steadily expanding category within the urban fresh fruit ecosystem. By 2024, rising health awareness, increased exposure to global diets, and improved cold-chain infrastructure had already strengthened consumption momentum across metropolitan and tier-1 cities. In 2025, the market reached a value of INR 54.4 billion, entering a high-growth phase supported by premiumisation and widening consumer adoption, with the industry projected to grow at a CAGR of 14.9%.

Looking ahead, the market is forecast to reach INR 95.4 billion by 2029, underscoring strong long-term demand fundamentals. However, supply-side constraints persist. In FY 2023–24, India imported over 43,000 tonnes of kiwi, significantly exceeding domestic output and highlighting a structural demand–supply imbalance.

This reflects a deeper issue of supply-chain competitiveness, particularly when India’s domestic kiwi ecosystem is benchmarked against global export leaders such as New Zealand and Chile, which operate at scale with integrated production-to-export systems.

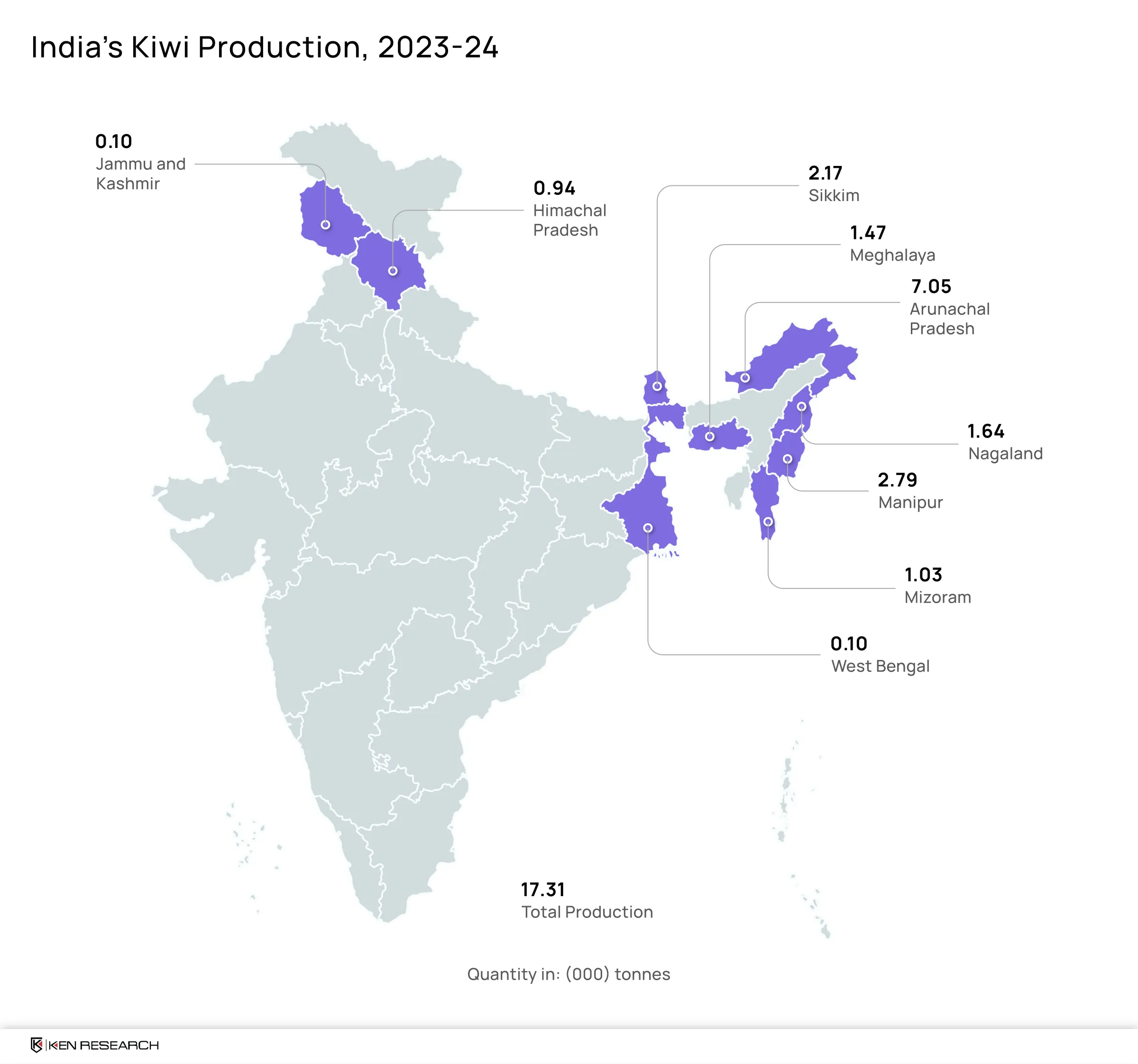

India’s Kiwi Boom vs Domestic Limits

India’s domestic kiwi production remains small in aggregate and fragmented across multiple hill states, limiting its ability to support national demand at scale. In 2023-24, total domestic kiwi output across all producing states was approximately 18,160 tonnes, less than half of recent annual import volumes.

Production is geographically concentrated in temperate and sub-temperate regions, primarily in the Northeast and select Himalayan belts. Arunachal Pradesh is the dominant producer, accounting for approximately 7,430 tonnes in 2023-24, or about 45-50% of national output. While this makes Arunachal the clear anchor of domestic supply, the absolute volume remains modest relative to market demand.

Beyond Arunachal Pradesh, production is distributed across smaller clusters. Manipur produced approximately 4,020 tonnes, followed by Sikkim (2,170 tonnes) and Meghalaya (2,080 tonnes). These states benefit from favourable agro-climatic conditions but operate largely through smallholder-driven orchards, constraining economies of scale and post-harvest standardisation.

Further down the production curve, Nagaland (1,650 tonnes), Himachal Pradesh (1,100 tonnes), Mizoram (1,030 tonnes), and West Bengal (100 tonnes) contribute incremental volumes. Uttarakhand, an emerging production geography, reported 381.8 tonnes in 2022-23 from 682.66 hectares, supported by a state-level kiwi development policy. Despite policy momentum, current output remains commercially marginal.

Taken together, India’s kiwi production exhibits breadth without depth-multiple producing states, but no second large-scale hub capable of materially shifting national supply dynamics. This fragmentation results in seasonal, region-specific supply, limiting year-round availability and quality consistency, particularly for organised retail and institutional channels.

How New Zealand and Chile Built Export Power?

The global kiwi export landscape is dominated by New Zealand and Chile, whose horticulture systems are explicitly structured for international trade rather than domestic consumption. In 2024–25, New Zealand led global fresh kiwifruit exports with approximately USD 2.09 billion in export value, a customs-based measure reflecting the value of physical fruit shipments. During the same period, Chile ranked among the leading exporters, recording export values of around USD 267.5 million, underscoring its importance in global trade flows.

New Zealand’s export leadership has strengthened over time, with fresh kiwifruit export value rising by over 20% between 2020 and 2024. Separately, in the 2024–25 season, the industry sold a record 220.9 million trays globally, generating approximately USD 3.1 billion in total industry revenue, which includes fruit sales as well as service income from licensing, branding, and post-harvest coordination. This model is supported by large-scale commercial orchards, advanced cold-chain infrastructure, and coordinated global marketing.

Chile’s competitiveness is driven by its extended March-November harvest window, enabling counter-seasonal supply to northern hemisphere markets. In 2025, Chile exported approximately 146,603 tonnes of kiwifruit, up from 143,156 tonnes in 2024, supplying the United States and Europe through strong phytosanitary compliance and efficient logistics. Together, these systems show that kiwi competitiveness is driven by supply-chain integration, seasonality management, and logistics depth rather than production volume alone.

Why Can’t India’s System Scale?

India’s competitiveness gap is visible across four structural dimensions.

First, production economies export-orientated orchards overseas.

Second, post-harvest infrastructure is underdeveloped near production zones. Limited access to controlled-atmosphere storage and fragmented cold-chain handling increase spoilage risk and reduce shelf life, undermining buyer confidence.

Third, supply reliability is constrained by seasonality and geography. Domestic production is concentrated in narrow harvest windows, whereas global exporters maintain year-round availability through multi-origin sourcing.

Finally, trade readiness is limited. Unlike New Zealand or Chile, India’s kiwi sector lacks large-scale aggregation, varietal standardisation, and export-grade compliance frameworks, positioning the country primarily as a consumption market rather than a competitive supply base.

What Would It Take to Compete?

Building competitiveness is possible, but only through structural transformation rather than incremental expansion. Achieving parity with global exporters would require cluster-based commercial orchards, high-yield varietals, farmer aggregation models, and significant cold-chain investment near production hubs, supported by assured off-take from organised buyers.

However, current market signals indicate that import optimisation will outpace domestic substitution in the near to medium term. Recent stabilisation in global kiwi supply, coupled with trade facilitation measures such as India–New Zealand tariff liberalisation, continues to improve the economics of imports relative to domestic production.

Domestic kiwi cultivation is therefore more likely to evolve as a long-term complementary supply rather than a near-term replacement for imports.

Imports vs Self-Reliance: The Real Choice

India’s kiwi market contrasts sharply with export leaders such as New Zealand and Chile, which operate large-scale, integrated supply chains, while India’s production remains fragmented and seasonal. This explains continued import dependence despite strong domestic demand and agronomic potential. Stress-testing a self-reliance approach shows that expanding cultivation alone cannot deliver scale, consistency, or year-round availability without parallel investments in aggregation, cold-chain infrastructure, and assured market access. Until these system-level capabilities are built, imports will remain the most efficient way to meet premium demand. The rational choice is therefore a dual strategy: optimise imports for near-term supply security while developing domestic production as a long-term, complementary source rather than a substitute.

Related tags

Fruits and Vegetables

Farming

Agriculture and Animal Care

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.