3 Growth Corridors Poised to Command 50% of Malaysia’s LED Market by 2030

Ken Research

August 20, 2025 - 4 min read

August 20, 2025

by Khushi RastogiBy 2030, three growth corridors are expected to command nearly half of Malaysia’s LED market value, reshaping how policy, investment, and industry strategy converge in the lighting sector.

rollout of LED streetlights, regulations catalysed Efficiency Regulations to the 2012 announcement to phase out GLS bulbs by 2014, and the 2019 nationwide LED streetlight rollout, regulation catalysed adoption and pushed urban penetration above 80%. With prices now at parity with conventional lighting, the era of blanket market expansion is over.

The next cycle of growth will be defined not by adoption rates, but by the concentration of value in targeted segments where policy alignment, compliance capability, and export readiness will determine who captures the upside.

Grounded in the Green Technology Master Plan (2017–2030) and the National Energy Transition Roadmap (2023), this analysis identifies the three corridors most likely to deliver disproportionate market value and long-term competitiveness.

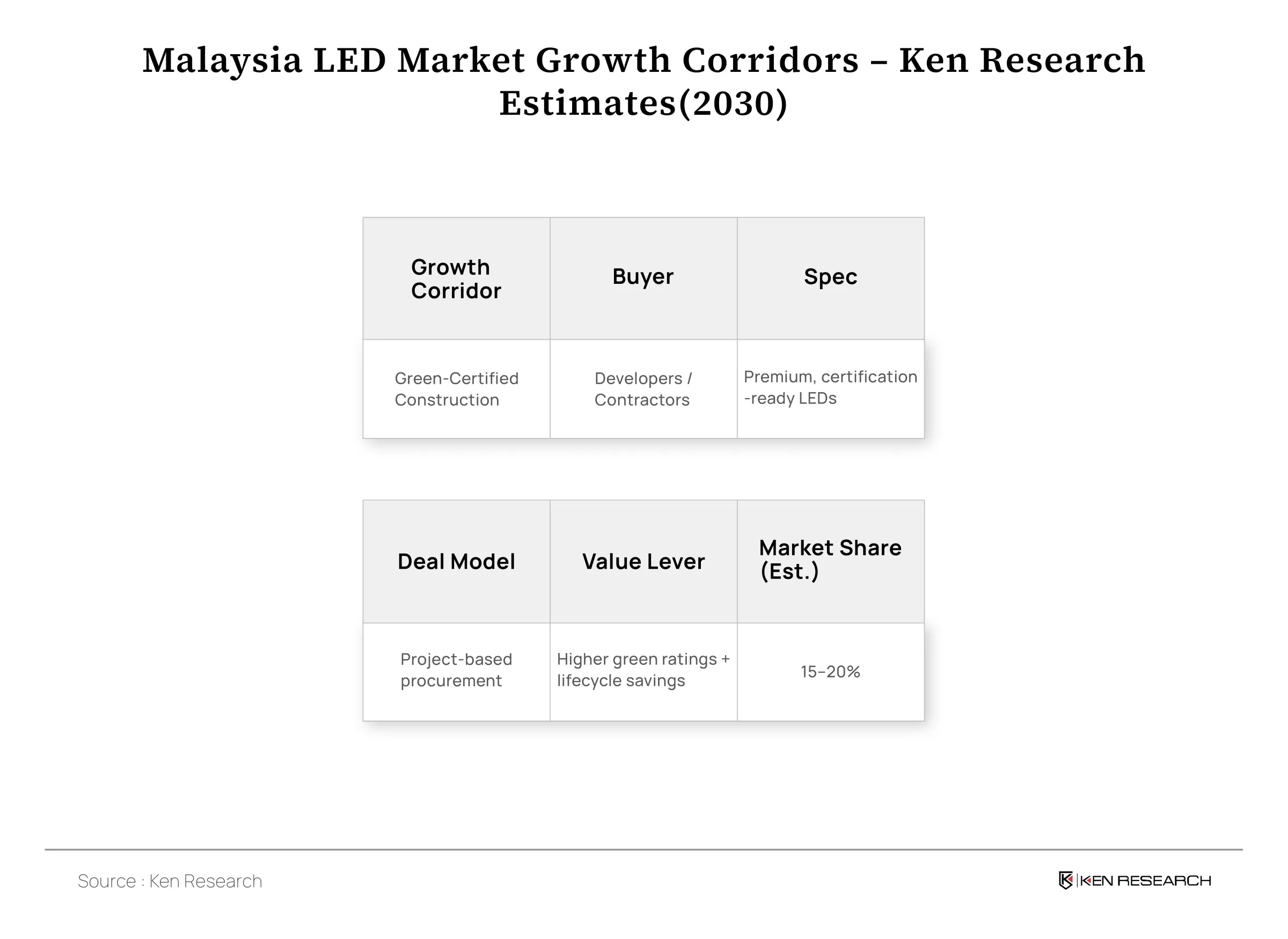

Green-Certified Construction

Malaysia’s green building movement, underpinned by frameworks such as GreenRE and the Green Building Index (GBI), has transitioned LEDs from a compliance necessity into a strategic asset for developers.

Policies such as the National Green Technology Policy of 2009 and the National Energy Efficiency Action Plan of 2015 have embedded energy performance criteria into the design and certification of commercial, institutional, and premium residential projects.

Developers view high-performance LEDs as boosting certification scores, marketability, financing, and lifecycle savings. Valuing total ownership cost, this segment rewards premium, certification-ready suppliers. Notably, retrofitting 54 government buildings cut 14,758 MWh electricity and 10.94 ktCO₂ emissions, showcasing LEDs’ measurable impact.

While private-sector demand in green-certified construction is creating a premium segment, a parallel wave of opportunity is emerging in the public sector where infrastructure retrofits are becoming a central pillar of Malaysia’s urban transformation. Ken Research estimates that by 2030, green-certified construction could represent 15–20% of total LED market value, reflecting the demand for premium specifications and the industry’s growing emphasis on total cost of ownership

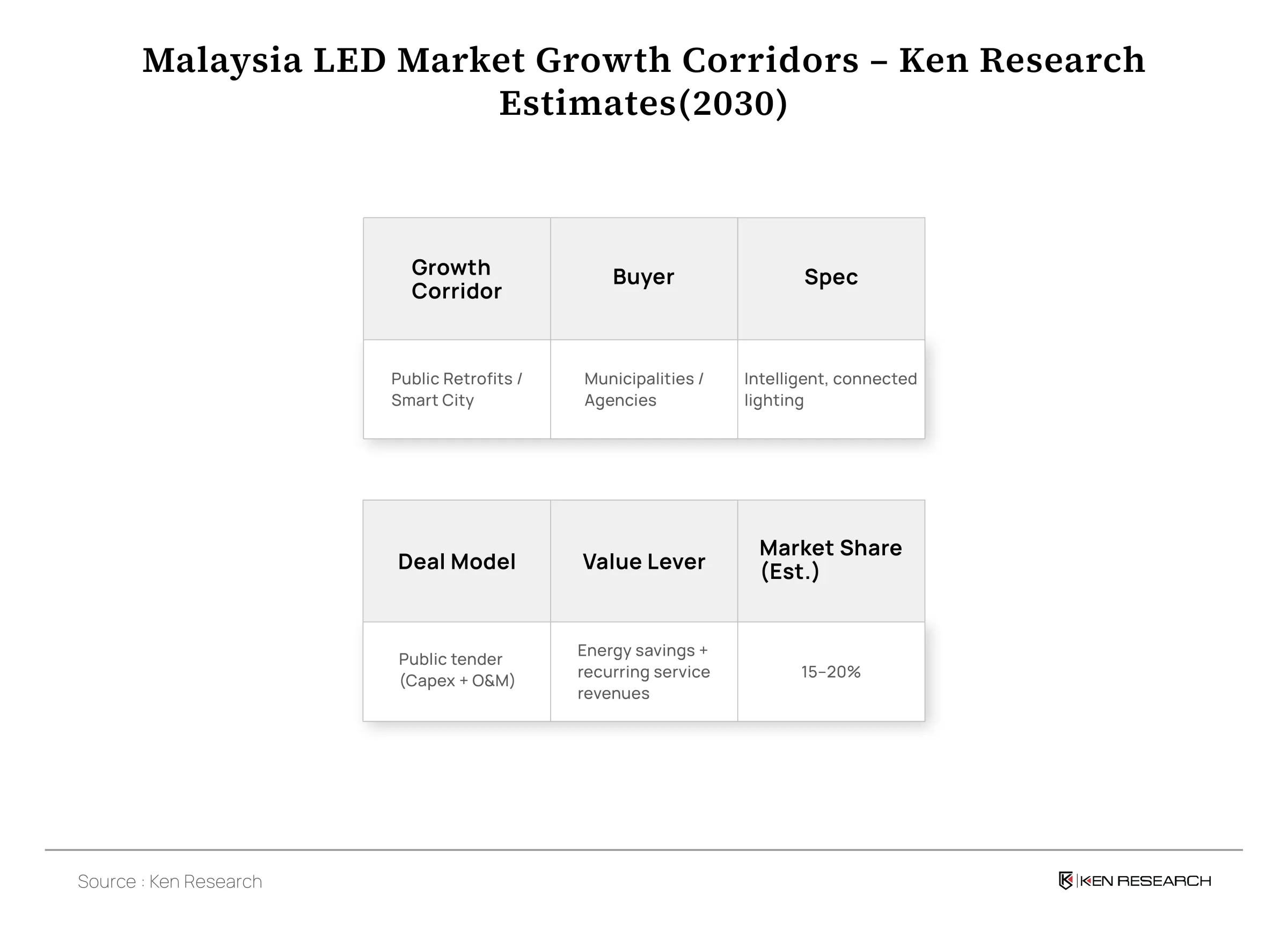

Public Infrastructure Retrofits

Malaysia’s urban development strategy is accelerating the modernisation of public lighting systems across municipalities, transport hubs, and public facilities. The Melaka “Interact City” initiative, which deployed more than 1,000 cloud-connected streetlights, demonstrated energy savings of up to 60% while improving both operational efficiency and public safety. Similar projects are no longer confined to major urban centres mid-sized cities are beginning to replicate these models, opening opportunities for suppliers capable of delivering turnkey solutions that integrate hardware, software, and long-term maintenance.

As tenders increasingly mandate integrated monitoring systems, the economics of these projects are shifting. Recurring revenues from operations and maintenance (O&M) are becoming just as significant as upfront capex, favouring firms with expertise in both setup and lifecycle management. Reflecting these dynamics, Ken Research estimates that public infrastructure retrofits and smart city projects could account for 15–20% of Malaysia’s LED market by 2030.

Beyond Malaysia, this capability also creates a springboard into early-stage LED adoption markets across ASEAN, offering local manufacturers additional export opportunities.

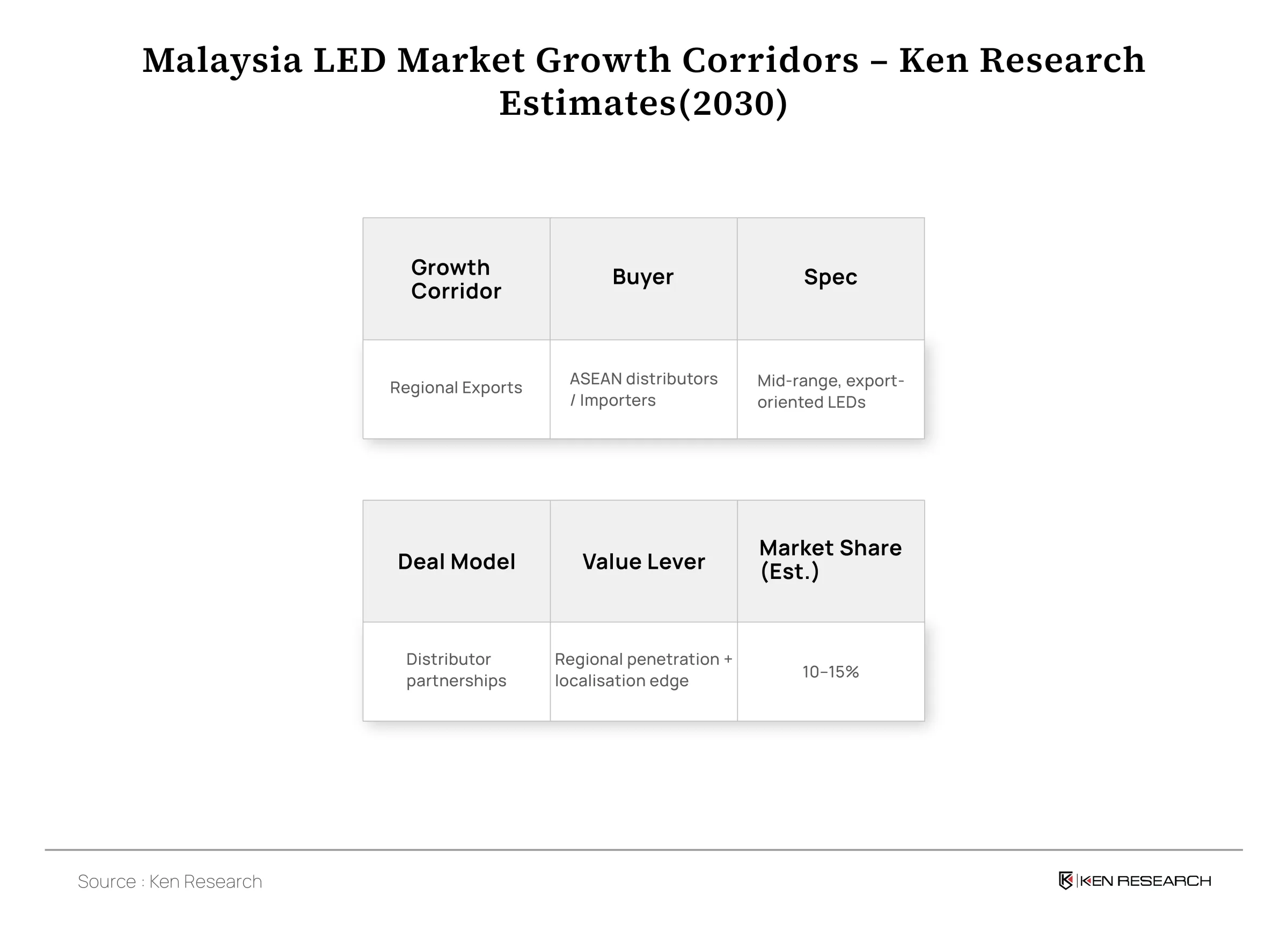

Regional Export Expansion

Malaysia’s manufacturing base is steadily reinforcing its role as a regional LED hub, supported by policy measures such as the National Investment Aspirations (NIA) Plan of 2021, which incentivises local production and aims to reduce import dependency.

Major investments have strengthened this position. OSRAM’s Penang facility, one of its largest in Asia, has expanded Malaysia’s high-performance component manufacturing capabilities, while Dialight’s operations have introduced advanced industrial and specialty lighting solutions. At the same time, local manufacturers such as Red Sky Lighting are driving product localisation and cost-efficient innovation, enabling Malaysia to balance global expertise with homegrown adaptability.

These developments extend beyond capacity expansion. They have accelerated technology transfer, lifted production standards, and positioned Malaysia to serve high-growth ASEAN markets including Vietnam, Indonesia, and the Philippines where LED adoption remains in its early stages.

At the same time, diversifying into regional exports helps buffer against the intense price competition within Malaysia’s basic LED segment, where Chinese suppliers dominate with products priced as low as USD 1.5–3.5.

According to Ken Research model assumptions, regional exports are projected to represent 10–15% of Malaysia’s LED market by 2030, supported by early-stage ASEAN penetration and Malaysia’s competitive edge in localised manufacturing.

Conclusion

Malaysia’s LED industry has entered a new competitive phase in which value is no longer evenly distributed across the market. Growth will increasingly be captured in green-certified construction, public infrastructure retrofits, and regional export expansion each requiring a unique combination of compliance expertise, technical innovation, and delivery capability.

These corridors not only offer higher margins and longer-term contracts but also provide defensible positions against commodity competition. The companies that can align their capabilities with these emerging opportunities, while anticipating shifts in policy and technology, will not only secure a disproportionate share of the market but also shape the trajectory of Malaysia’s lighting industry in the next cycle of growth.

Related tags

Consumer Electronics

Consumer Products and Retail

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.