₱6,350 Per Session Coverage, 22% Patient Growth and ₱990,600 Annual Protection Are Structurally Transforming the Philippines Dialysis Market

Ken Research

February 23, 2026 - 4 min read

February 23, 2026

by Ken ResearchIn 2024, PhilHealth increased the haemodialysis benefit to ₱6,350 per session, enabling financial protection of up to ₱990,600 per patient annually. This policy shift materially reduced affordability constraints and reinforced long-term treatment adherence across chronic kidney disease patients.

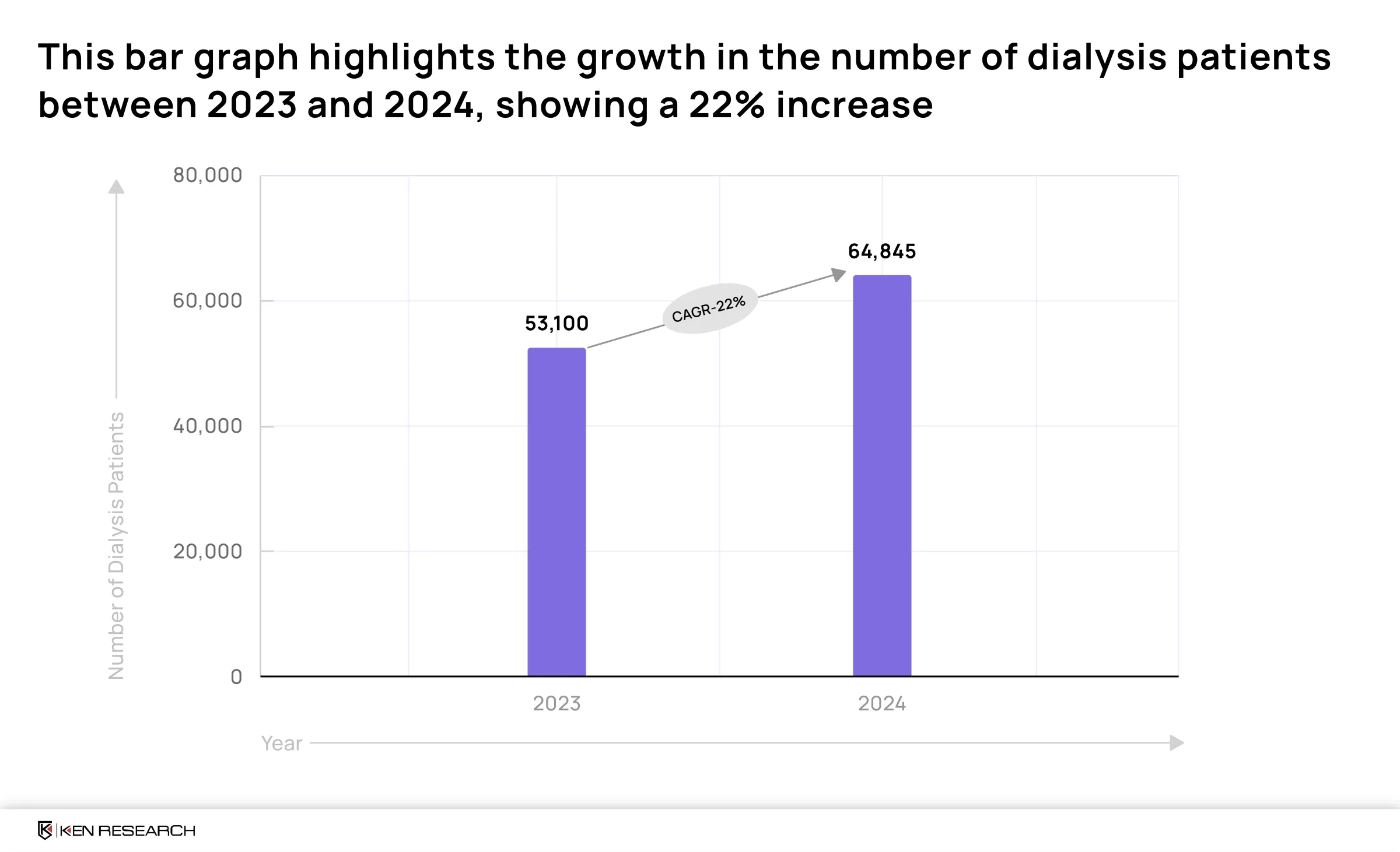

Dialysis patients reached 64,845 in 2024, with a 22% increase during the year, confirming accelerated utilisation under improved reimbursement access. The growth reflects structural access expansion rather than temporary patient inflows.

The market is projected to expand at approximately 4.20% compound annual growth, establishing a stable baseline demand. As volume visibility improves, the strategic focus shifts decisively toward converting predictable treatments into sustainable operating margin expansion.

Fresenius SE’s CO. (FMC’s) Strategic Positioning in the Philippines Dialysis Market: How Demand Dynamics Shape Competitive Edge

Against this strengthening demand backdrop, Fresenius SE & Co. KGaA participates in dialysis through its stake in Fresenius Medical Care (FMC). Because FMC is no longer consolidated line-by-line, group-level reporting does not directly reflect dialysis operating performance.

In the Philippines, FMC operates 24 dialysis centres, establishing a defined care-delivery presence within a reimbursement-supported environment. However, evaluating earnings quality requires examination of FMC’s segment disclosures.

Accordingly, competitive positioning must be assessed by linking local demand dynamics to FMC’s Care Delivery and Care Enablement performance before benchmarking against B. Braun SE.

FMC Leveraged 4.0% Growth in Care Enablement to Achieve €267 Million Profit in FY2024

In FY2024, Care Delivery revenue declined from €15,578 million to €15,275 million, a 1.9 % year-on-year decrease. Despite revenue contraction, operating margin improved from approximately 9.7 % to 10.3 %, demonstrating effective cost control under volume moderation.

Conversely, Care Enablement revenue increased from €5,345 million to €5,557 million, reflecting 4.0 % growth, while operating income improved from a €67 million loss to €267 million profit. This lifted margins from roughly 2.3 % to 6.1 %, confirming material operating leverage recovery.

Operating cash flow totalled €2,386 million, compared with €2,629 million in the prior year, while net leverage improved to approximately 2.9 times from around 3.2 times, materially strengthening balance-sheet flexibility and capital allocation capacity.

FMC’s 2024 Performance Gives It the Competitive Edge Over B. Braun in the Philippines Dialysis Market

B. Braun SE reported Avitum division sales of €1,884.480 million, compared with €1,849.489 million, reflecting 1.9 % growth.

At the group level, total sales reached €9,136.9 million, representing 4.4 % year-on-year growth, with an EBITDA margin of 12.1 % and EBIT of €379.5 million. Divisional margin for Avitum was not separately disclosed.

The stronger growth and margin expansion within FMC’s enablement segment demonstrate superior operating leverage recovery. In procurement-sensitive markets such as the Philippines, this differential materially enhances competitive positioning in tender-driven environments.

FMC’s €1 Billion Buyback and Margin Expansion Will Power Its Future Dialysis Market Dominance

FMC increased savings targets under its transformation program and announced a €1 billion share buyback, signalling confidence in the durability of free cash flow. Management has articulated an ambition to achieve mid-teens operating income margins by 2030, reinforcing a margin-led growth thesis.

Guidance indicates expectations of low single-digit revenue growth alongside high-teens to high-twenties operating income growth, excluding special items. When viewed against current segment profitability, this reflects a substantial structural margin expansion objective.

Fresenius SE’s ownership recalibration reinforces portfolio discipline, underscoring a strategic pivot toward efficiency and capital-deployment rigour rather than expansion driven by scale alone.

Staffing, Pricing, and Utilisation Affect Dialysis Profit Margins in a Competitive Market

Although reimbursement stabilises demand, dialysis economics remain sensitive to staffing intensity. Wage progression, nurse availability, and training requirements directly influence per-session cost structures, particularly in urban treatment hubs.

Procurement-driven pricing pressure affects dialysis machines and consumables under competitive tenders. While consumables generate recurring revenue, pricing compression can influence the overall profitability path.

Because dialysis revenue is session-based, missed treatments directly reduce realised income. Seasonal illness cycles therefore create short-term utilisation volatility, reinforcing the importance of operational resilience and throughput optimisation.

Conclusion

Fresenius SE’s dialysis exposure in the Philippines remains structurally indirect and must be evaluated through FMC’s segment-level disclosures. FY2024 performance highlights delivery stabilisation and enablement-driven margin recovery as the primary profitability drivers.

Reimbursement reform enhances treatment continuity and demand visibility; however, sustained differentiation will depend on operational precision, procurement leverage, and disciplined capital deployment.

As per Ken Research, the Philippine dialysis sector has transitioned into a reimbursement-secured growth phase where demand volatility has materially moderated. Structural volume support is firmly established under expanded coverage. The decisive differentiator will be the ability to scale operating margins while defending per-session economics under staffing and procurement pressure.

Operators embedding margin architecture into expansion strategies will outperform within a mid-single-digit growth baseline, while those prioritising footprint without operational discipline risk margin compression despite favourable demand fundamentals.

Related tags

Healthcare

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.