Saudi Arabia Digital Payments Market to Reach 17 billion Transactions by 2030 as the Kingdom Targets an 80% Cashless Economy

Ken Research

March 9, 2026 - 6 min read

March 9, 2026

by Ken ResearchSaudi Arabia’s digital payments ecosystem has shifted from infrastructure development to scaled adoption, supported by regulatory alignment and measurable transaction growth. The Kingdom’s non-cash transaction share has expanded from 32% in 2019 to 63% in 2023, with a 70% milestone expected by 2025 and an 80% target by 2030.

This transition is not incremental, as it is backed by transaction volumes rising from 2.9 billion in 2019 to 10.8 billion in 2023 and projected to reach 17.0 billion by 2030. The structural drivers include government digitisation, instant payment rails, expanding POS infrastructure, and fintech licensing acceleration.

Additionally, the Saudi Arabia digital payments market is moving into a monetisation phase where ecosystem depth, cost efficiency, and regulatory compliance define competitive positioning. The following sections unpack the infrastructure evolution, adoption metrics, competitive dynamics, and forward opportunity layers shaping this transformation.

National Payment Rails Scale from SPAN Foundations to SARIE Instant Transfers

Saudi Arabia’s payment modernisation began with SPAN in 1990, which connected bank ATMs nationwide and established real-time interoperability. This foundational layer enabled the growth of electronic transactions and laid the groundwork for centralised bill processing via SADAD in 2004.

SADAD currently connects more than 100 major billers nationwide and processes millions of recurring payments monthly. By 2024, it had connected over 300 billers and processed 364 million payments, reinforcing its role in public and utility payments infrastructure.

The transformation accelerated after SPAN’s rebranding to MADA in 2015, integrating global schemes such as Visa and Mastercard. By 2023, MADA processed 7.7 billion transactions across 1.5 million POS terminals, while SARIE launched in 2021, surpassed 400 million instant bank transfers and processed SAR 13.26 trillion in Q3 alone, confirming systemic scale.

99% Internet Penetration and 85.3% Urbanization Strengthen Digital Payment Scalability

Saudi Arabia’s macro-digital indicators outperform regional averages, creating structural support for payment digitisation. With 35.6 million internet subscribers and approximately 99% penetration, digital access barriers are minimal across consumer segments.

Urbanisation stands at 85.3%, compared to 77.3% across the Middle East, enabling concentrated infrastructure deployment and higher POS density. The Kingdom’s population of 36.01 million, combined with 70% under the age of 35, supports rapid adoption of wallets, BNPL, and app-based financial services.

Economically, Saudi Arabia accounts for USD 1.08 trillion in nominal GDP in 2024, representing 31% of the Middle East’s USD 3.5 trillion economy. The financial sector contributes USD 4.8 billion in market value and 4.4% to GDP, indicating further room for financial deepening relative to regional benchmarks.

Non-Cash Transactions Expand at 17.4% CAGR as Government Digitizes 100% of Payments

The Kingdom’s non-cash transaction share increased from 32% in 2019 to 55% in 2021 and 63% in 2023, reflecting a 17.4% CAGR between 2019 and 2025. Transaction volumes rose from 2.9 billion in 2019 to 6.2 billion in 2021 and 10.8 billion in 2023, with projections of 12.9 billion in 2025 and 17.0 billion by 2030.

Government digitisation has been a decisive catalyst, with 100% of public sector payments and collections now processed digitally. Integration across SADAD and SARIE, alongside 261+ licensed fintech players connected to instant rails, has expanded ecosystem liquidity.

As a result, transaction growth is no longer driven solely by consumer behaviour but by structural digitisation across public and private sectors. This shift reduces cash dependency while expanding addressable volumes for gateways, wallets, and alternative credit models.

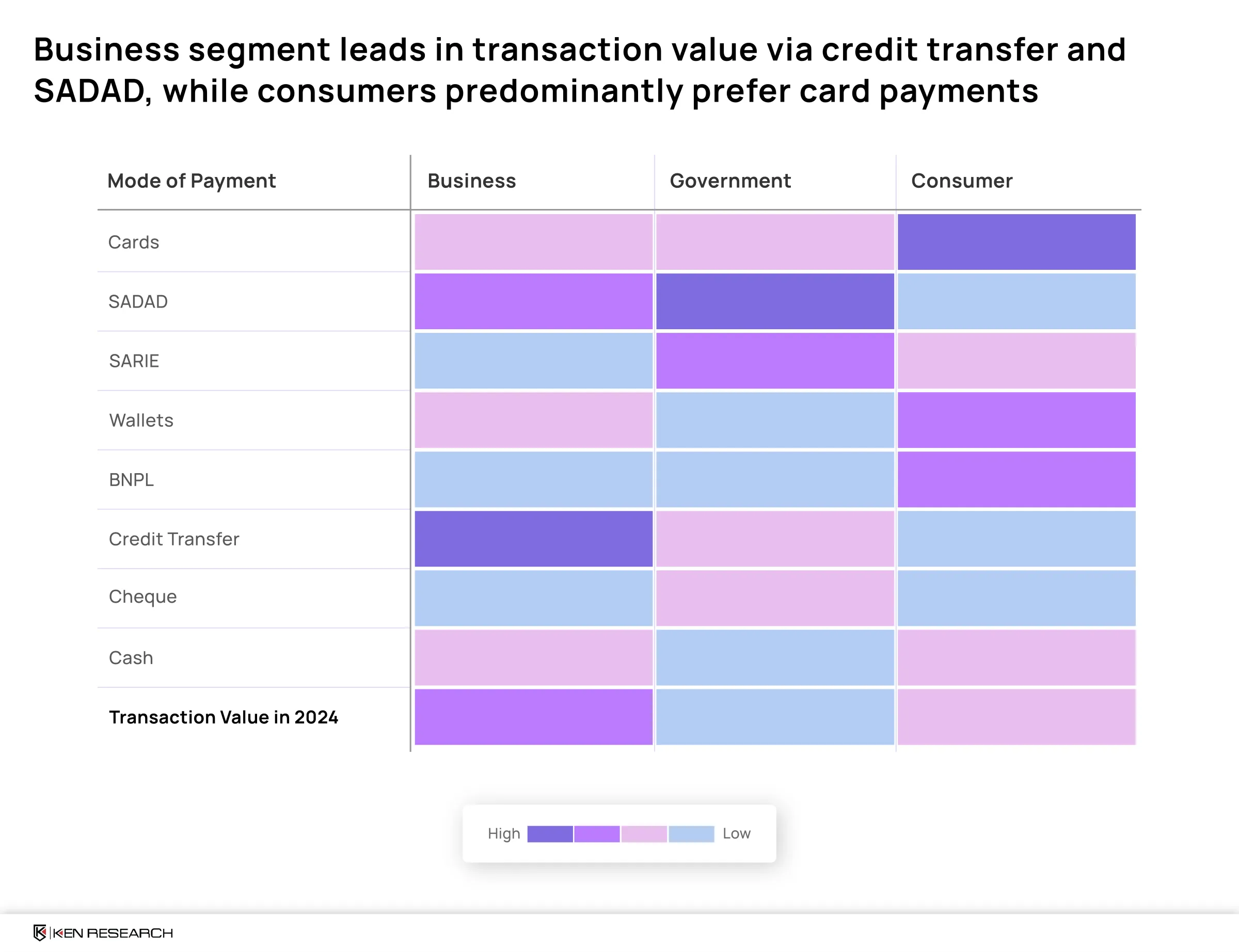

Segment-Level Payment Behaviour: Business Drives Credit Transfers, Consumers Propel Cards and Wallets

In 2024, the business segment leads transaction value through credit transfers and SADAD, reflecting high-value B2B settlement patterns. Government entities rely heavily on SADAD and SARIE, consistent with full public payment digitisation.

Consumers, by contrast, predominantly use card payments, supported by MADA’s 1.5 million POS terminals and broad acceptance across retail and e-commerce. Wallet and BNPL adoption is rising within this segment, while cash and cheque usage continues to decline, particularly among younger demographics.

This segmentation indicates that infrastructure rails ensure volume stability, while consumer-facing innovations drive growth in interaction layers. Consequently, monetisation opportunities differ materially across enterprise, public, and retail channels.

E-Wallets and BNPL Positioned as High-Growth, Low-Cost Scalers in Cost-Efficiency Matrix

Growth-cost mapping places E-wallets, BNPL, and SADAD in the high-growth, low-cost quadrant, reflecting operational efficiency and rapid adoption. Cards remain high-growth but operate at higher infrastructure and acceptance costs due to POS hardware and network fees.

Credit transfers represent steady performers with lower growth potential due to operational complexity, while cash and cheques fall into the low-growth, high-cost category. The bubble analysis indicates that cards still command the largest transaction value, but scalability economics favour digital wallets and BNPL models.

This cost differential is driving SME migration toward wallet-based and gateway-enabled solutions, particularly as high card MDR fees influence merchant margins. Capital allocation strategies increasingly prioritise models with lower transaction costs and stronger digital integration.

Gateway Leaders, 12M-User Wallets, and 11M-User BNPL Platforms Intensify Market Competition

Among payment gateways, HyperPay and PayTabs each serve approximately 2,000 merchants, while Geidea supports an estimated 100,000+ merchants through omni-retail and SME integration. Their monetisation models span MDR, SaaS tools, device bundling, and lending add-ons.

In the wallet segment, STC Pay serves approximately 12 million users, positioning itself as an everyday wallet transitioning toward banking capabilities. Urpay serves approximately 6.5 million users with a focus on remittances and simple wallet services, monetising via interchange and FX fees.

BNPL players such as Tabby, with approximately 11 million users, and Tamara focus on checkout financing and merchant co-marketing strategies. Differentiation lies in risk models, cross-market scalability, and merchant uplift performance in fashion and e-commerce verticals.

77% Expat Workforce, SME Digitisation, and Wallet-Led Processing Drive the Next Growth Wave

Cross-border remittances remain structurally significant, supported by an expatriate workforce representing approximately 77% of the labour base. This creates sustained demand for low-cost digital remittance solutions integrated into wallet ecosystems.

SME onboarding through gateways such as Geidea, PayTabs, and HyperPay is expanding merchant digitisation, particularly in long-tail retail segments. Concurrently, cybersecurity and fraud monitoring mandates by regulators reinforce trust and compliance standards.

High card transaction fees are accelerating SME interest in alternative digital channels, strengthening wallet adoption and gateway diversification. As a result, the next growth wave will likely emerge at the consumer interaction and processing layers rather than core government rails.

Conclusion

Saudi Arabia’s digital payments market is transitioning from infrastructure expansion to ecosystem monetisation at scale. With non-cash transactions increasing from 32% in 2019 to 63% in 2023 and projected to reach 80% by 2030, alongside transaction volumes expected to grow to 17.0 billion, the Kingdom is firmly advancing toward a digitally dominant financial system. Government-backed platforms such as SADAD, MADA, and SARIE have institutionalised trust, liquidity, and interoperability, while wallets, BNPL, and payment gateways are unlocking higher-margin growth across consumer and SME segments. Supported by 99% internet penetration, 85.3% urbanisation, and over 261 licensed fintech players, Saudi Arabia’s digital payments ecosystem is evolving into a structurally scalable, regulation-backed, high-growth market aligned with Vision 2030 objectives.

Ken Research Insight

KSA’s digital payments ecosystem is entering a decisive value-creation phase where infrastructure maturity is translating into competitive differentiation and revenue optimisation. While transaction growth metrics signal strong momentum, strategic clarity requires a deeper assessment of forward-looking forecasts, segment-level monetisation models, competitive market shares, regulatory trajectory, and cost-structure evolution through 2030.

The next wave of opportunity will be shaped by wallet penetration economics, BNPL credit dynamics, SME gateway expansion, and cross-border remittance corridors. Ken Research’s comprehensive market intelligence provides detailed forecasts, competitive benchmarking, and scenario-based strategic insights to support investors, payment service providers, financial institutions, and fintech leaders in capitalising on Saudi Arabia’s rapidly expanding digital payments marke

Related tags

Payments

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.