Used Cars Dominate With 55% Market Share and EV Adoption Accelerates: How Iraq’s Vehicle Market Is Approaching Over 30 billion by 2030?

Ken Research

February 4, 2026 - 7 min read

February 4, 2026

by Khushi GuptaThe most defining change in Iraq’s vehicle market is the growing dominance of used passenger vehicles. In 2024, used passenger vehicles accounted for over half of the total market volume, translating to over 320,000 units. This is not a temporary response to price volatility; it reflects a durable shift in how Iraqi consumers evaluate vehicle ownership. New passenger vehicles, by contrast, represented around 19% of market volume in 2024.

The underlying driver is demographic. With approximately 60% of Iraq’s population under the age of 25, a large portion of buyers are first-time vehicle owners with limited purchasing power. For this cohort, used passenger vehicles offer the optimal balance of affordability, functionality and urban suitability. As a result, the secondary market has become the primary entry point into vehicle ownership.

From an ecosystem perspective, this elevates the importance of used-vehicle sourcing, refurbishment quality, dealer credibility, financing access, and aftersales support. Competitive advantage increasingly lies not in selling more vehicles, but in managing the lifecycle of used inventory efficiently.

Fuel Mix Is Stable Today, but Electrification Is Defining the Growth Curve

Fuel mix dynamics add another layer to Iraq’s evolving vehicle market. In 2024, gasoline vehicles form the backbone of demand, accounting for around 65% of total sales. Diesel vehicles follow with around 31 % share, reflecting continued relevance for commercial and utility-oriented usage.

Electric and hybrid vehicles remain a small portion of the market at around 4% in 2024. However, their importance lies not in current scale, but in growth momentum. Between 2024 and 2030, electric and hybrid vehicles are expected to expand at approximately 26% CAGR, making them the fastest-growing fuel category in the market.

Infrastructure planning plays a central role in this shift. Iraq’s plan to deploy 500 public charging stations by 2029, along with pilot charging initiatives in Baghdad developed in collaboration with Zain Iraq, reduces adoption friction for electric and hybrid vehicles. While the market is not yet infrastructure-ready for mass electrification, these steps materially improve the feasibility for early adopters.

Will Online Marketplaces Double the Reach as Iraq’s Digital Adoption Accelerates Through 2030?

Sales channel evolution represents another structural shift in Iraq’s vehicle market. In 2024, independent dealers account for the largest share of vehicle sales, over 300,000 units. Their strength lies in flexible pricing, broad inventory access, and deep local relationships, particularly in the used vehicle segment.

OEM dealerships account for around 170,000 units in 2024. While smaller than independent dealers, their role remains significant due to growing consumer preference for verified vehicles, warranties, and structured aftersales support, especially among middle-income buyers upgrading from older vehicles.

The most notable change, however, is occurring in online marketplaces. From a base of over 90,000 units in 2024, online platforms are expected to expand to over 210,000 units by 2030, supported by the highest channel-level growth rate. Rising smartphone penetration and increasing trust among younger, urban buyers are accelerating this shift.

Auction channels remain niche, accounting for only around 10,000 units, growing modestly to around 30,000 units by 2030. Their relevance lies primarily in fleet disposals, bulk imports, and price-sensitive transactions rather than mainstream retail demand.

Taken together, these trends indicate a gradual move away from fragmented, informal sales toward more structured, discoverable, and trust-based channels. Competitive advantage increasingly depends on omnichannel presence, transparency, and customer experience; capabilities that are unevenly distributed across the market today.

How Is Vehicle Age Emerging as a Key Decision Factor in Iraq’s Vehicle Market?

Vehicle age segmentation further illustrates how buyer priorities are changing. In 2024, 0-5-year-old vehicles account for over 210,000 units, making them the largest single age segment. These vehicles offer a balance between modern features, fuel efficiency, and manageable ownership costs.

5-10-year-old vehicles account for over 170,000 units, while vehicles older than 10 years represent around 90,000 units. New vehicles account for about 125,000 units, reflecting selective but sustained demand for brand-new ownership.

By 2030, 0-5-year-old vehicles are expected to rise to around 375,000 units, the highest among age segments. New vehicles grow at a similar pace, indicating parallel demand for modernisation and affordability.

Vehicles older than 10 years are expected to grow slowly, signalling gradual fleet renewal rather than volume expansion. This shift has important implications for imports, refurbishment standards, spare parts demand, and financing models, all of which increasingly revolve around younger used inventory.

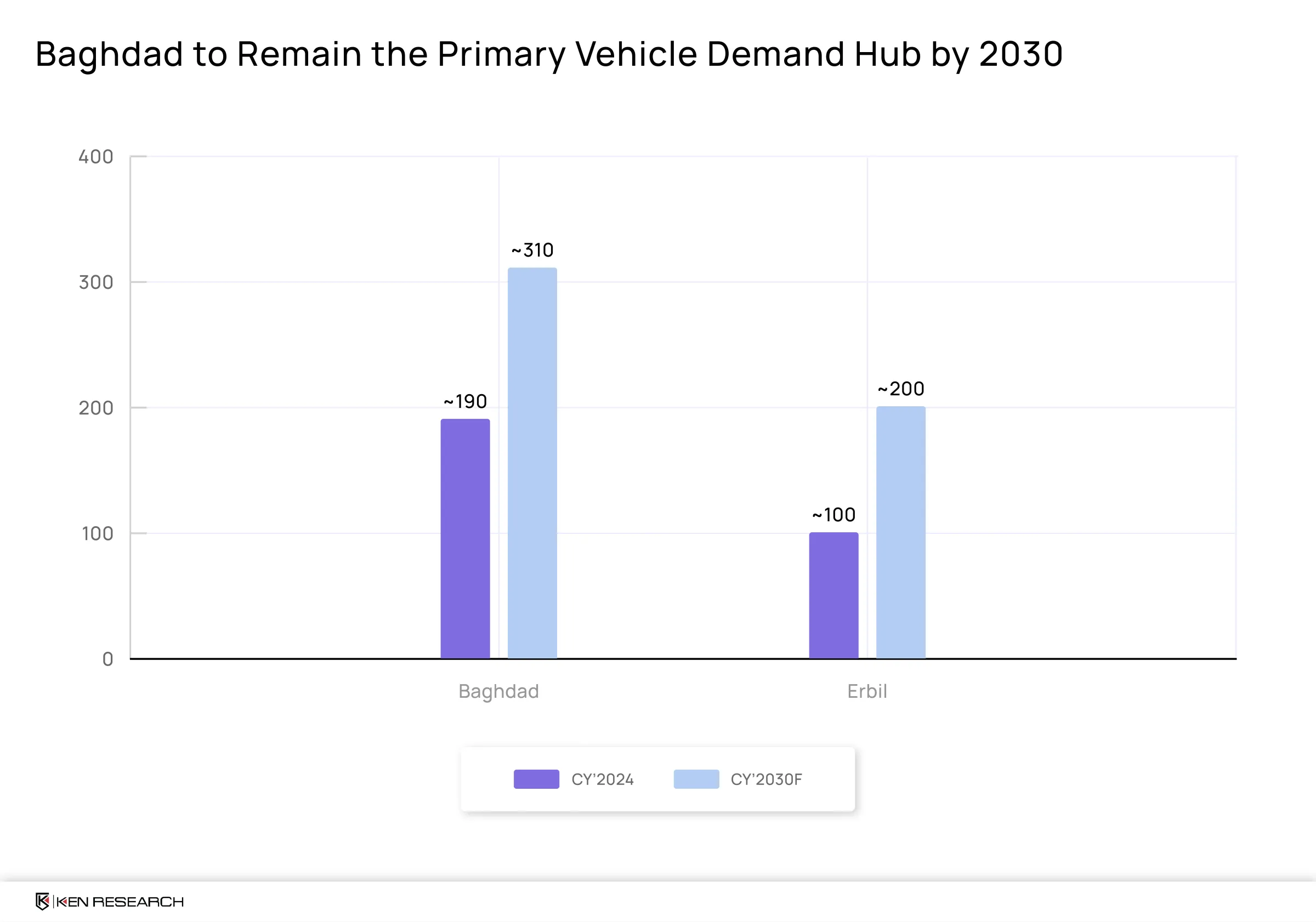

Are Baghdad and Erbil Set to Remain the Core Demand Hubs Through 2030?

Regionally, Iraq’s vehicle market remains concentrated in a few key urban centres. Baghdad is the single largest demand hub, accounting for around 190,000-unit sales in 2024. Population density, income concentration, and the country’s most developed dealer ecosystem underpin this dominance.

Erbil follows with around 100,000-unit sales in 2024, supported by higher purchasing power and a relatively structured retail environment. Together, Baghdad and Erbil already generate more than half of the national vehicle demand, shaping pricing benchmarks and inventory flows across the country.

By 2030, this concentration remains intact. Baghdad volumes are expected to rise to around 310,000 units, while Erbil over 200,000 units. These cities will continue to dictate market direction, making them essential anchors for OEMs, distributors, and financiers.

Are Tier-2 Cities Becoming the Next Growth Engine of Iraq’s Vehicle Market?

Beyond the primary hubs, demand is steadily spreading into Basra, Mosul, and Sulaymaniyah, signalling a more balanced regional market. In 2024, Basra and Sulaymaniyah each account for around 85,000 and 80,000 units, respectively, while Mosul contributes around 60,000 units.

By 2030, these markets show meaningful expansion. Basra is expected to reach around 142,000 units, Sulaymaniyah around 140,000 units, and Mosul around 110,000 units. Basra’s port access strengthens its role as an entry point for imports, while Sulaymaniyah and Mosul are supported by dealership expansion, ongoing urbanisation and rising vehicle replacement demand.

While Baghdad and Erbil remain indispensable, long-term volume scalability increasingly depends on disciplined execution across these Tier-2 cities.

Conclusion

Used passenger vehicles have become the dominant entry point to ownership, gasoline remains the demand anchor, and sales are steadily migrating toward formal dealers and digital platforms. At the same time, buyer preferences are clearly shifting toward newer used vehicles, supported by gradual fleet renewal and expanding demand beyond Baghdad and Erbil into Tier-2 cities. Together, these dynamics indicate a market that is becoming more organised, quality-focused, and regionally diversified, with growth driven by affordability, trust, and urbanisation rather than new-vehicle penetration alone.

Ken Research highlights that the clearest strategic opportunity lies in prioritising 0-5-year-old used passenger vehicles in Baghdad, Erbil, and high-growth Tier-2 cities such as Basra and Sulaymaniyah. The investments in structured sourcing, refurbishment standards, transparent pricing, and digital-first sales models will deliver superior returns compared to pure new-vehicle expansion. Players that align inventory, financing, and aftersales capabilities around younger used vehicles, and build omnichannel visibility, are best positioned to capture both volume growth and customer lifetime value as Iraq’s vehicle market continues to formalise.

Related tags

Electric Vehicle

Automotive and Automotive Components

Automotive, Transportation and Warehousing

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.