Thailand Agricultural Equipment & Machinery Competition Benchmarking 2025: Product Portfolio, Dealer Network, Customer Segments & Company Performance

Published on: December 2025

Report Overview

Thailand Agricultural Equipment Market Overview

Market Highlights

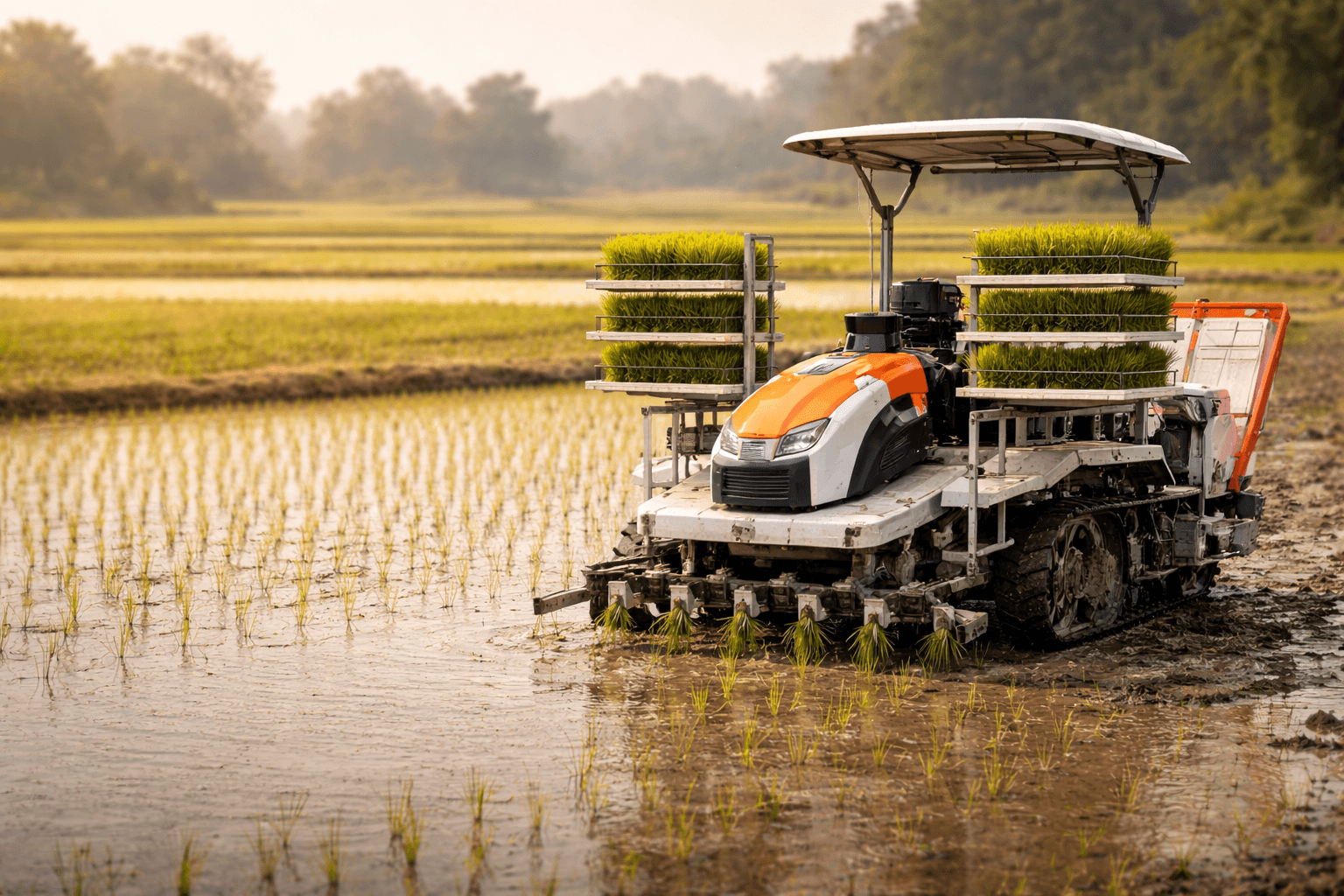

The Thailand Agricultural Equipment Market showcases a diverse competitive structure, where multinational corporations, regional manufacturers, and local firms engage in a dynamic interplay. Multinationals leverage their extensive resources for efficiency, while regional players focus on tailored solutions that resonate with local agricultural practices, and local firms capitalize on agility and niche expertise to carve out market segments.

Innovation from global leaders is seamlessly integrated with localized adaptations, as companies customize agricultural technologies to meet Thailand's unique environmental and operational challenges. Collaborations between technology providers and local distributors ensure that advanced solutions are effectively tailored to the specific needs of Thai farmers, enhancing productivity and sustainability.

The distribution and aftersales ecosystem is critical in fostering customer loyalty and operational efficiency. Strategic partnerships among manufacturers, distributors, and service providers enhance the accessibility of agricultural equipment, while robust aftersales support, including maintenance and training, ensures that users derive maximum value from their investments.

Forward-looking strategies emphasize agility, sustainability, and technological integration as key competitive differentiators. Companies are increasingly adopting data-driven approaches to optimize operations, while commitments to sustainable practices and innovative product designs are shaping the future landscape of the agricultural equipment market in Thailand, driving both growth and resilience.

Ecosystem Matrix

The Thailand agricultural equipment ecosystem is dominated by established large players like Kubota and Yanmar, supported by international brands with strong local presence. Their dominance is reinforced by wide distribution networks and dealer partnerships across provinces.

Medium and small players cater to specialized needs, niche farming communities, and aftermarket supply, collectively shaping a balanced market structure with competitive pricing, local customization, and broader adoption of mechanization in rice and sugarcane farming.

Leading Player Profiles

Company Profile Overview

Thailand’s agricultural equipment players exhibit a diverse mix of multinationals, conglomerates, and local enterprises, with Kubota and Yanmar leading in tractors and rice mechanization.

Domestic firms like CP Machinery and Mitr Phol Machinery thrive by addressing sugarcane mechanization, while smaller players capture aftermarket opportunities through local spare part distribution and repair services.

Key Operational Performance Metrics

Company Performance Overview

Unlock Market Insights

Dive deeper into production, distribution, and pricing intelligence.

Get Customized ReportOperational metrics such as dealer networks, pricing, and after-sales service coverage directly define revenue scalability for agricultural equipment manufacturers in Thailand, especially in rural rice and sugarcane belts.

Large international firms benefit from structured dealer networks and after-sales coverage, while smaller local players face scalability constraints but sustain business through niche regional distribution and competitive pricing.

Core Financial Performance Metrics

Financial parameters such as revenue, COGS, and EBITDA margins highlight competitive pressures from rising input costs, localized demand cycles, and high competition among international and domestic brands.

Large players sustain stronger financial margins due to scale, whereas small and medium players operate on thinner margins, relying on niche equipment demand and spare parts to remain profitable.

Table of Contents

1. Ecosystem Matrix

1.1 Large Players

1.1.1

Kubota Thailand

1.1.2

Yanmar S.P.

1.1.3

Siam Agro Industry Supply (SAIS)

1.1.4

John Deere Thailand

1.1.5

CLAAS Thailand

1.1.6

CNH Industrial Thailand

1.2 Medium Players

1.2.1

Charoen Pokphand Machinery

1.2.2

Mitr Phol Machinery Division

1.2.3

E-Trade Agro Machinery

1.2.4

Agri Solutions Asia

1.2.5

Thai Agri Parts

1.2.6

Rangsit Tractor

1.3 Small Players

1.3.1

Thai Farm Machinery

1.3.2

Who

1.3.3

Buriram Agro By

1.3.4

Agrow Thai Machinery

1.3.5

Eastern Tractor

1.3.6

Thai Agro Tools

2. Leading Player Profiles

2.1 Company Name

2.2 Group Name

2.3 Headquarters

2.4 Established Year

2.5 Core Offerings

2.6 Mode of Functioning

3. Key Operational Performance Metrics

3.1 Production Capacity (Units/Year)

3.2 Dealer Network (Units)

3.3 Service Centers (Units)

3.4 Distribution Coverage (% of Domestic Market)

3.5 Product Range (Number of Models)

3.6 Pricing (USD Mn)

3.7 Export Share (%)

3.8 After-Sales Service (% Coverage)

4. Core Financial Performance Metrics

4.1 Parameters

4.1.1 Revenue (USD Mn)

4.1.2 Revenue Growth (%)

4.1.3 COGS (USD Mn)

4.1.4 COGS Growth (%)

4.1.5 EBITDA (USD Mn)

4.1.6 EBITDA Growth (%)

4.1.7 EBITDA Margin (%)

4.1.8 PAT (USD Mn)

4.1.9 PAT Margin (%)

5. Methodology

5.1 Approach

5.1.1 Desk Sources

5.1.2 Primary Interviews

5.1.3 Sanity Checking & Validation

5.2 Benchmarking Process

5.2.1 Data Collection

5.2.2 Primary Validation

5.2.3 Proxy KPI Modelling

5.2.4 Normalization & Indexing

5.2.5 Gap Analysis

5.2.6 Peer Review

5.3 Sample Composition

5.3.1 Scope Items

5.3.2 Sample Size

5.3.3 Target Respondents

Methodology

Ken Research will deploy its proprietary, multi-layered research framework—combining robust secondary research, targeted primary outreach, and rigorous data validation—to deliver an authoritative competitive landscape analysis of the Thailand Agricultural Equipment Market. The methodology ensures comprehensive coverage of leading manufacturers, regional distributors, and service providers, using both reported financials and carefully calibrated proxy KPIs to benchmark performance.

Desk Sources

- Industry reports from proprietary databases and Ken Research archives

- Company annual reports and investor presentations

- Government and trade association publications, including the Office of Agricultural Economics and Thai Tractor Manufacturers Association

- Trade magazines, journals, and industry e-articles

- Financial databases such as Bloomberg, Capital IQ, and Orbis

- Web traffic and app usage dashboards, including SimilarWeb and App Annie

Primary Interviews

- Category managers and R&D heads of agricultural equipment manufacturers

- Senior sales and marketing leaders at OEMs

- Distributors and regional dealers

- Farmers’ cooperatives and large fleet buyers

- Service providers and technology partners offering IoT and precision agriculture solutions

Sanity Checking and Validation

- Triangulation through cross-verification of secondary data, primary inputs, and proxy model outputs

- Proxy KPI synthesis using dealership count, machine sales volume, after-sales service reach, financing tie-ups, web traffic, and patent filings

- Outlier analysis to identify and reconcile anomalous data points via follow-up discussions

- Assumption tracking with a structured log documenting limitations and proxy KPI sources

- Peer review through internal expert evaluation of methodology, models, and key outputs before finalization