APAC Agricultural Drone Market Outlook to 2030

Region:Asia

Author(s):Shambhavi

Product Code:KROD4958

Region:Asia

Author(s):Shambhavi

Product Code:KROD4958

November 2024

98

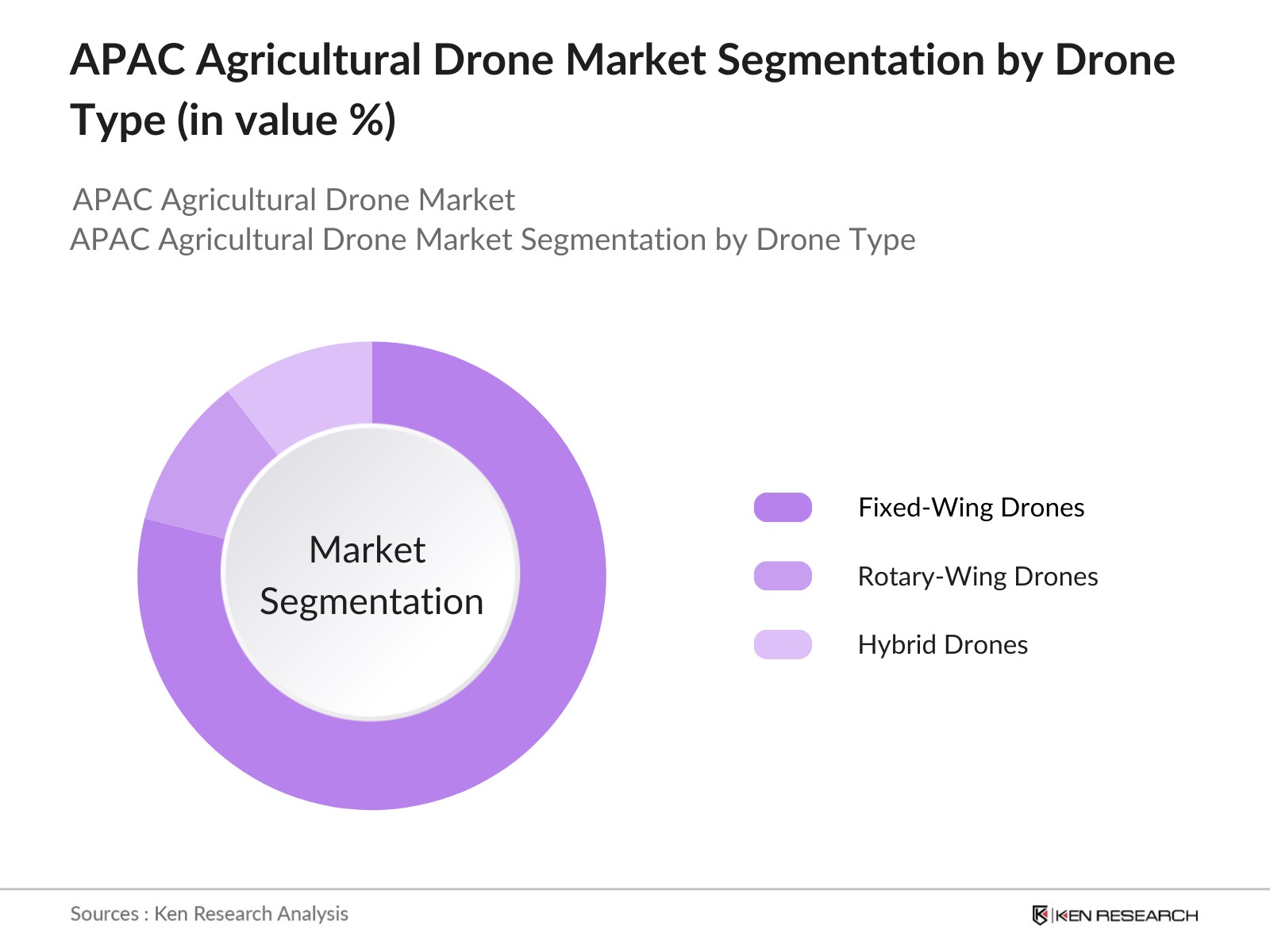

By Drone Type: The APAC agricultural drone market is segmented by drone type into Fixed-Wing Drones, Rotary-Wing Drones, and Hybrid Drones. Rotary-wing drones, specifically multirotors, have the dominant market share, as they offer superior maneuverability and precision when surveying small fields and challenging terrain. Their ability to hover makes them ideal for monitoring crops, soil conditions, and spraying pesticides in confined areas.

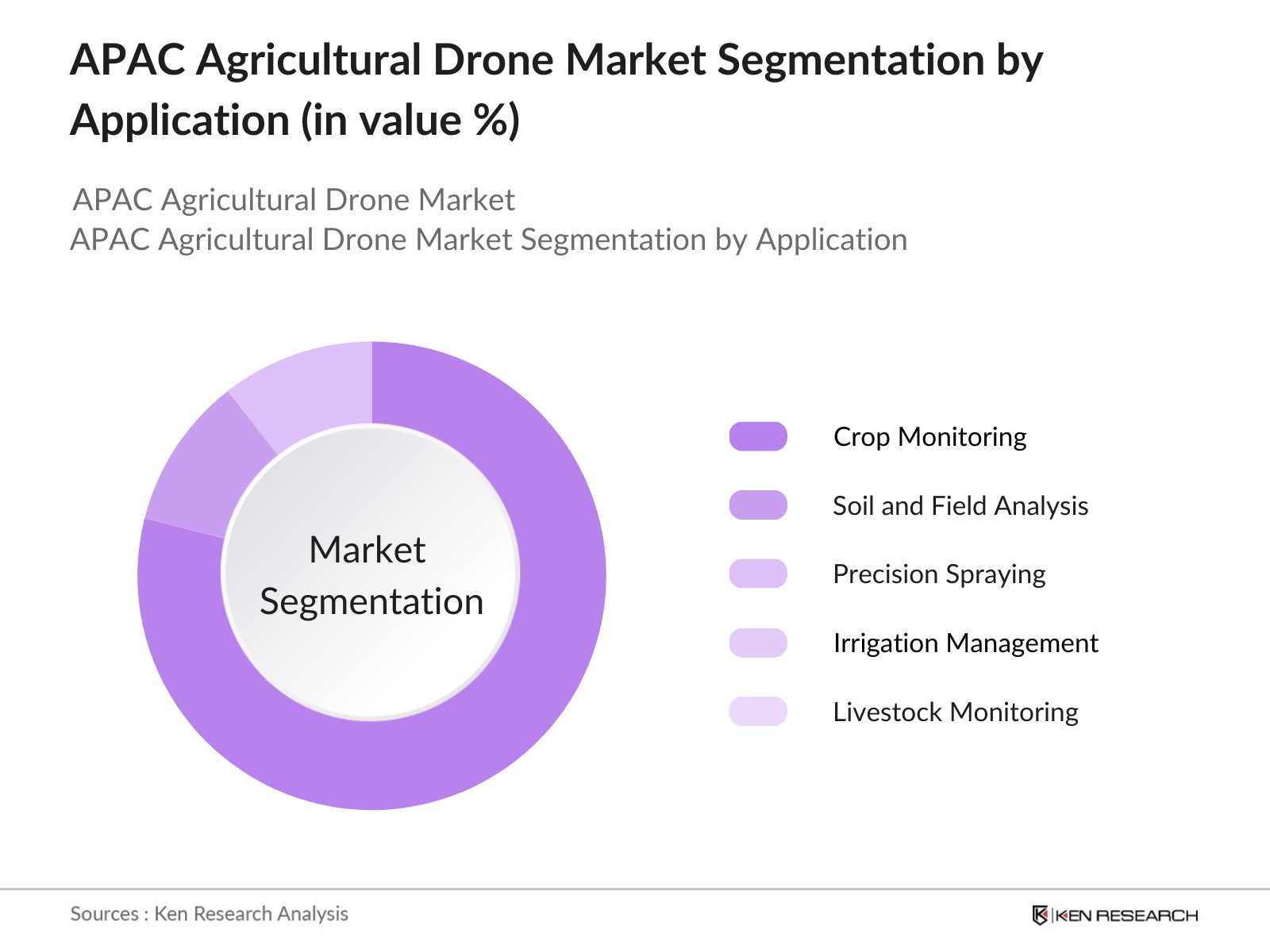

By Application: The market is segmented by application into Crop Monitoring, Soil and Field Analysis, Precision Spraying, Irrigation Management, and Livestock Monitoring. Precision Spraying holds a dominant market share, driven by the growing need to optimize pesticide and fertilizer usage. Drones equipped with advanced spraying mechanisms can cover large fields quickly and precisely, significantly reducing chemical use and ensuring that crops are uniformly treated.

The APAC agricultural drone market is dominated by a few key players, including DJI, Parrot SA, and Trimble Inc., who lead the market through innovation, strategic partnerships, and expansion into new geographical areas. These companies have established strong distribution networks and continue to invest in R&D to maintain their competitive edge.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD) |

Employees |

R&D Expenditure |

Product Portfolio |

Global Presence |

Partnerships |

Certification |

|

DJI |

2006 |

Shenzhen, China |

~ |

~ |

~ |

~ |

~ |

~ |

~ |

|

Parrot SA |

1994 |

Paris, France |

~ |

~ |

~ |

~ |

~ |

~ |

~ |

|

Trimble Inc. |

1978 |

Sunnyvale, US |

~ |

~ |

~ |

~ |

~ |

~ |

~ |

|

Yamaha Motor Co., Ltd. |

1955 |

Iwata, Japan |

~ |

~ |

~ |

~ |

~ |

~ |

~ |

|

AgEagle Aerial Systems |

2010 |

Wichita, USA |

~ |

~ |

~ |

~ |

~ |

~ |

~ |

Over the next five years, the APAC agricultural drone market is expected to witness substantial growth, driven by advancements in AI, IoT, and machine learning integration. Governments across the region continue to support the adoption of smart farming technologies, which will further drive drone utilization in agriculture. The introduction of more affordable drones and the expansion of drone-as-a-service business models will make these technologies accessible to smaller farms, thus broadening the market.

|

Segment |

Sub-segments |

|

Drone Type |

Fixed-Wing Drones, Rotary-Wing Drones, Hybrid Drones |

|

Application |

Crop Monitoring, Soil and Field Analysis, Precision Spraying, Irrigation Management, Livestock Monitoring |

|

Technology |

AI and Machine Learning, GPS and GNSS Integration, Remote Sensing, Real-Time Data Analytics |

|

Component |

Hardware (Drones, Sensors, Cameras), Software (Mapping, Flight Control, Data Analytics), Services (Drone-as-a-Service, Maintenance) |

|

Region |

China, Japan, India, South Korea, Southeast Asia |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (Precision Agriculture Adoption Rate, Technological Advancements)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increasing Demand for Precision Farming

3.1.2 Government Subsidies and Policies Supporting Agriculture

3.1.3 Technological Advancements (AI, IoT Integration)

3.1.4 Rising Focus on Sustainable Farming Practices

3.2 Market Challenges

3.2.1 High Initial Investment and Maintenance Costs

3.2.2 Lack of Technical Know-How Among Farmers

3.2.3 Regulatory Challenges in Drone Usage

3.3 Opportunities

3.3.1 Expansion of Drone-as-a-Service Models

3.3.2 Growth in Smart Farming Solutions

3.3.3 Collaboration between Drone Manufacturers and Agri-tech Firms

3.4 Trends

3.4.1 Increasing Use of Multispectral and Hyperspectral Imaging

3.4.2 Integration of AI and Machine Learning in Drones

3.4.3 Autonomous Drone Operations

3.5 Government Regulations

3.5.1 UAV Certification Requirements

3.5.2 Air Traffic and Flight Restrictions for Agricultural Drones

3.5.3 Government Initiatives for Smart Farming Adoption

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

4.1 By Drone Type (In Value %)

4.1.1 Fixed-Wing Drones

4.1.2 Rotary-Wing Drones

4.1.3 Hybrid Drones

4.2 By Application (In Value %)

4.2.1 Crop Monitoring

4.2.2 Soil and Field Analysis

4.2.3 Precision Spraying

4.2.4 Irrigation Management

4.2.5 Livestock Monitoring

4.3 By Technology (In Value %)

4.3.1 AI and Machine Learning

4.3.2 GPS and GNSS Integration

4.3.3 Remote Sensing

4.3.4 Real-Time Data Analytics

4.4 By Component (In Value %)

4.4.1 Hardware (Drones, Sensors, Cameras)

4.4.2 Software (Mapping, Flight Control, Data Analytics)

4.4.3 Services (Drone-as-a-Service, Maintenance)

4.5 By Region (In Value %)

4.5.1 China

4.5.2 Japan

4.5.3 India

4.5.4 South Korea

4.5.5 Southeast Asia

5.1 Detailed Profiles of Major Companies

5.1.1 DJI

5.1.2 Parrot SA

5.1.3 Trimble Inc.

5.1.4 Yamaha Motor Co., Ltd.

5.1.5 AgEagle Aerial Systems Inc.

5.1.6 AeroVironment, Inc.

5.1.7 DroneDeploy

5.1.8 PrecisionHawk

5.1.9 senseFly

5.1.10 Kespry Inc.

5.1.11 Sentera, LLC

5.1.12 Ag Leader Technology

5.1.13 Delair

5.1.14 XAG Co., Ltd.

5.1.15 Aerialtronics

5.2 Cross Comparison Parameters (Revenue, Drone Units Shipped, Drone Features, Regional Presence, Certifications, Customer Base, R&D Expenditure, Strategic Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 UAV Licensing and Certification

6.2 Compliance with Local Aviation Regulations

6.3 Environmental Impact and Sustainability Standards

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Drone Type (In Value %)

8.2 By Application (In Value %)

8.3 By Technology (In Value %)

8.4 By Component (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The initial phase involved mapping out the major stakeholders in the APAC Agricultural Drone Market, backed by extensive desk research. This included using secondary and proprietary databases to gather critical market data and define the variables that influence market growth and trends.

In this phase, historical data pertaining to the market was compiled. Market penetration rates, the ratio of drone service providers to end-users, and revenue generation metrics were analyzed. Data reliability was ensured through cross-verification of service quality statistics.

Market hypotheses were tested through expert interviews conducted via telephone, gathering insights from key industry players such as manufacturers and service providers. This helped in refining market estimates and verifying on-ground trends.

This final phase involved direct engagement with agricultural drone manufacturers to gain deeper insights into product segment performance and customer preferences. The results were synthesized to ensure the report provided comprehensive, data-backed analysis.

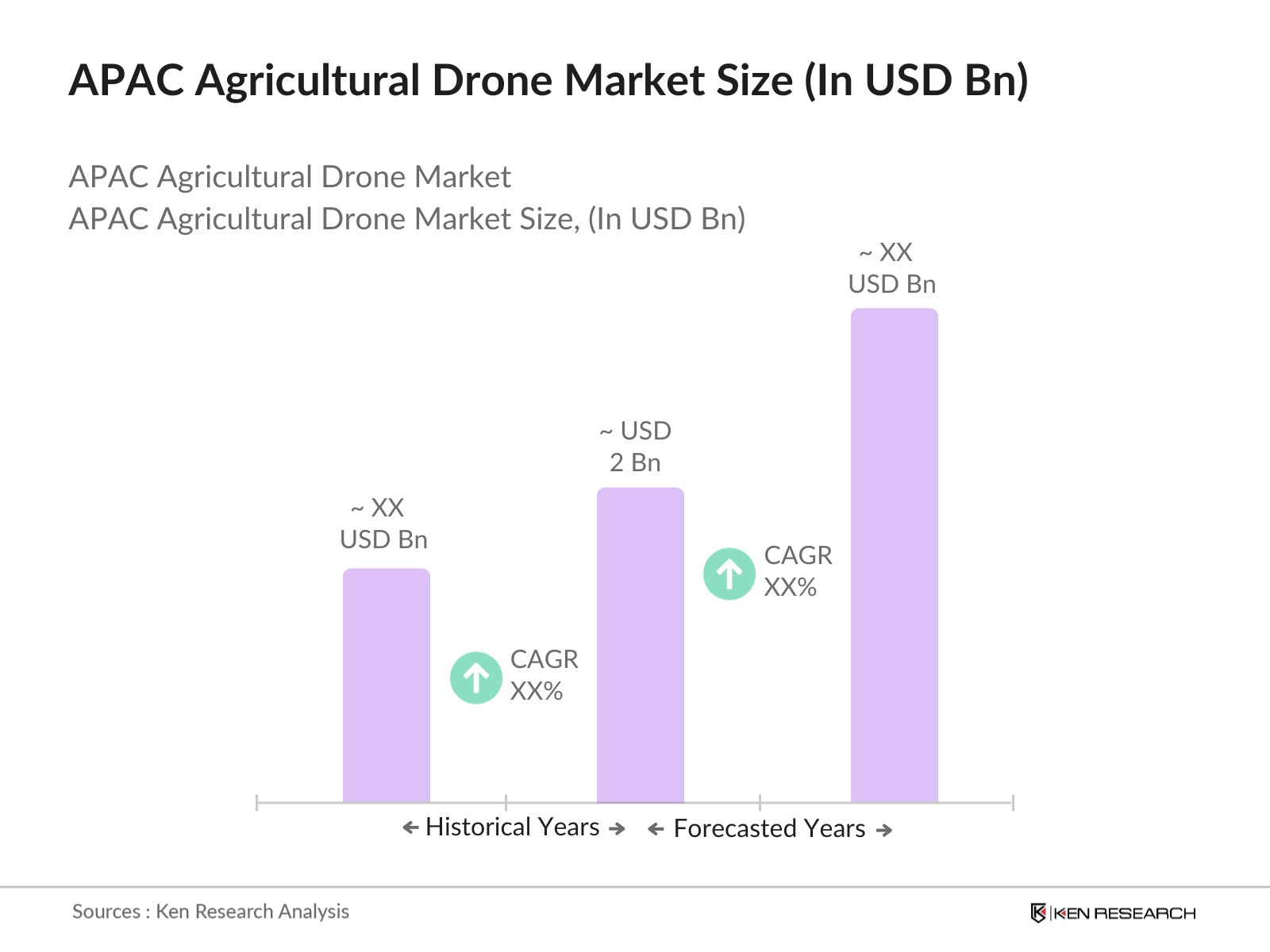

The APAC agricultural drone market is valued at USD 2 billion in 2023, driven by rising adoption of precision farming and government incentives for modernizing agricultural practices across the region.

Challenges include high initial costs of drone equipment, lack of technical expertise among small-scale farmers, and stringent regulatory requirements for drone usage in agriculture.

Major players in the market include DJI, Parrot SA, Trimble Inc., Yamaha Motor Co., Ltd., and AgEagle Aerial Systems, all of whom have a significant presence and continue to dominate the market through innovation and strategic partnerships.

Key growth drivers include the increasing demand for precision farming, government policies promoting smart farming, advancements in drone technologies, and rising interest in sustainable farming solutions.

Drones are primarily used for crop monitoring, precision spraying, soil analysis, irrigation management, and livestock monitoring. Precision spraying is a key application, helping farmers optimize chemical usage and increase crop yields.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.