APAC Digital Agriculture Market Outlook to 2030

Region:Afganistan

Author(s):Shambhavi

Product Code:KROD4930

Region:Afganistan

Author(s):Shambhavi

Product Code:KROD4930

November 2024

82

Listen to the audio summary

By Technology: The APAC digital agriculture market is segmented by technology into precision farming, IoT and connected devices, big data analytics and others. Precision farming currently holds a dominant market share due to its widespread adoption in large-scale farming operations across key regions like China and Australia. The use of AI-driven solutions to optimize irrigation and fertilization has significantly enhanced crop yield and reduced input costs, making precision farming a leading technology in the digital agriculture landscape.

By Application: The market is further segmented by application into crop monitoring, livestock monitoring, aquaculture management and others. Crop monitoring dominates the application segment, primarily due to the increasing use of sensor-based technologies and AI-driven analytics, allowing farmers to monitor crop health and optimize field operations. This has become critical in addressing challenges related to climate change and resource optimization in key APAC regions.

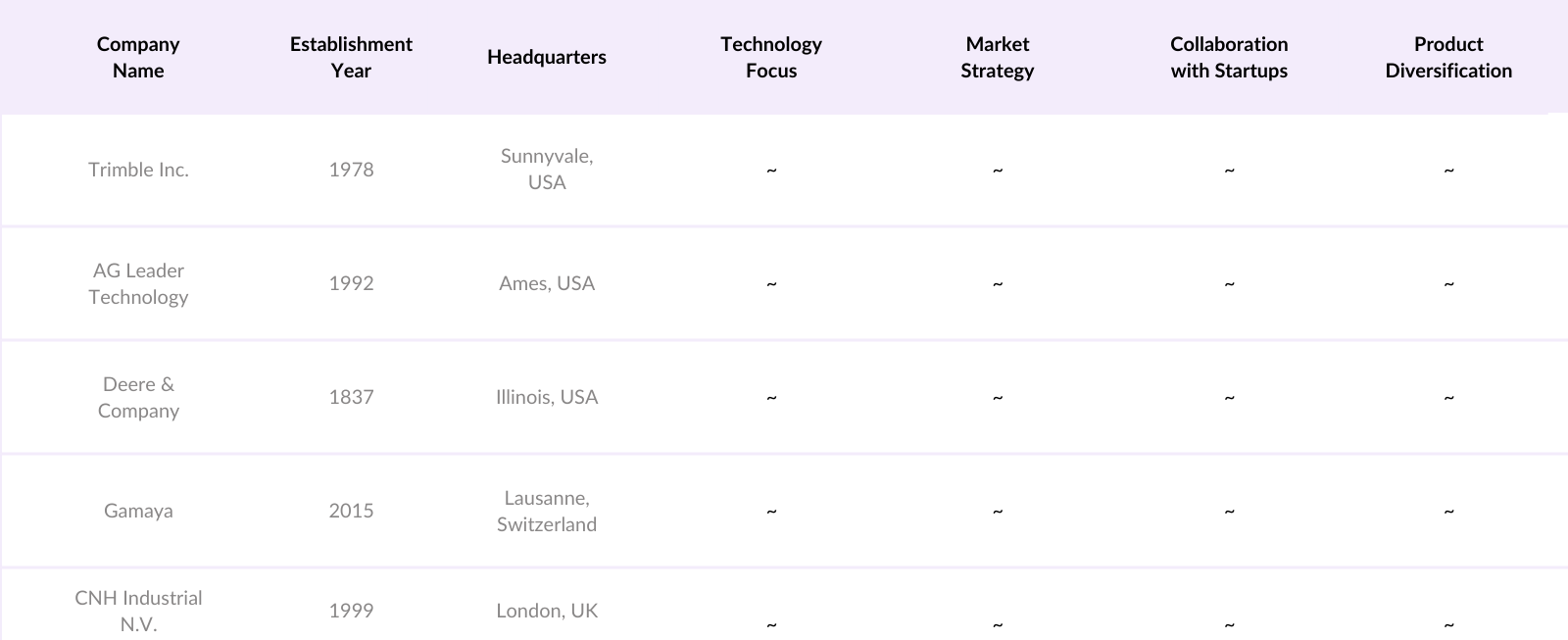

The APAC digital agriculture market is dominated by both regional and global players. These key companies have established strong presences in various APAC countries, contributing to market consolidation. Companies like Trimble and AG Leader Technology have been key in providing precision farming solutions, while startups like Gamaya are introducing AI-driven crop monitoring systems. This diversity of players, from established global firms to innovative startups, showcases the competitive nature of the market.

Growth Drivers

The APAC digital agriculture market is poised for rapid growth, driven by technological advancements and increasing government support for digital farming initiatives. Over the next five years, the adoption of AI, IoT, and blockchain technologies is expected to transform the agriculture industry in the region. Governments in China, India, and Australia are providing incentives and funding to promote smart farming practices. In addition, the rising demand for sustainable farming solutions will push the market towards more innovation in digital agriculture tools and platforms.

|

Segment |

Sub-segment |

|

By Technology |

Precision Farming, Remote Sensing, Big Data, IoT, Blockchain |

|

By Application |

Crop Monitoring, Livestock Monitoring, Smart Irrigation, Aquaculture Monitoring, Weather Forecasting |

|

By Component |

Hardware (Sensors, Drones), Software (AI Platforms), Services (Consulting, Maintenance) |

|

By End-User |

Smallholder Farmers, Commercial Farming Enterprises, Cooperatives, Government Agencies, Research Institutions |

|

By Region |

Southeast Asia, East Asia, South Asia, Oceania, Central Asia |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (e.g., Precision Farming, Remote Sensing Technology, AI and Big Data Integration, Government Subsidies, Climate-Smart Agriculture)

3.2. Market Challenges (e.g., High Initial Investment, Data Privacy Issues, Limited Connectivity in Rural Areas)

3.3. Opportunities (e.g., Collaboration with Agritech Startups, Expansion of Smart Irrigation Systems, Adoption of IoT in Agriculture)

3.4. Trends (e.g., AI-based Crop Monitoring, Blockchain for Traceability, Cloud Platforms for Data Management, Rise of Agribots)

3.5. Government Regulations (e.g., Agricultural Digitalization Policies, Subsidies for Smart Farming, Regulatory Framework for Agritech Startups)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (e.g., Farmers, Agritech Companies, Government Agencies, Investors, Agronomists)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Technology (In Value %)

4.1.1. Precision Farming

4.1.2. Remote Sensing and Satellite Imaging

4.1.3. Big Data and Analytics

4.1.4. IoT Devices and Platforms

4.1.5. Blockchain

4.2. By Application (In Value %)

4.2.1. Crop Monitoring and Management

4.2.2. Livestock Monitoring

4.2.3. Aquaculture Monitoring

4.2.4. Smart Irrigation

4.2.5. Weather Forecasting

4.3. By Component (In Value %)

4.3.1. Hardware (Sensors, Drones, GPS Devices)

4.3.2. Software (Farm Management Systems, AI Analytics Platforms)

4.3.3. Services (Consulting, Data Analytics, Maintenance)

4.4. By End-User (In Value %)

4.4.1. Smallholder Farmers

4.4.2. Commercial Farming Enterprises

4.4.3. Cooperatives and Associations

4.4.4. Government Agencies

4.4.5. Research Institutions

4.5. By Region (In Value %)

4.5.1. Southeast Asia

4.5.2. East Asia

4.5.3. South Asia

4.5.4. Oceania

4.5.5. Central Asia

5.1 Detailed Profiles of Major Companies

5.1.1. Trimble Inc.

5.1.2. AG Leader Technology

5.1.3. Deere & Company

5.1.4. Topcon Agriculture

5.1.5. Raven Industries

5.1.6. Hexagon Agriculture

5.1.7. The Climate Corporation

5.1.8. CNH Industrial N.V.

5.1.9. AgJunction

5.1.10. PrecisionHawk

5.1.11. Granular

5.1.12. Farmers Edge

5.1.13. Gamaya

5.1.14. AgEagle Aerial Systems

5.1.15. Kubota Corporation

5.2 Cross Comparison Parameters (Technology Adoption Rate, R&D Investment, Geographic Presence, Market Share, Product Portfolio, Collaboration with Agritech Startups, Customer Base, Revenue Growth)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Environmental and Data Privacy Standards

6.2 Compliance Requirements

6.3 Certification Processes

6.4 Government Incentives for Smart Farming Adoption

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Technology (In Value %)

8.2 By Application (In Value %)

8.3 By Component (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The initial phase involves mapping the key stakeholders within the APAC Digital Agriculture Market. This includes desk research leveraging proprietary databases and public sources to gather critical industry data. The primary goal is to identify the variables impacting market growth, such as government policies, technological advancements, and industry challenges.

This phase focuses on analyzing historical market data, evaluating market penetration of digital agriculture technologies, and assessing revenue generation. A thorough review of regional dynamics in major APAC countries helps construct accurate market estimates and identify trends shaping the market.

Expert consultations are conducted through interviews with key industry participants, including agritech startups, digital platform providers, and government officials. These discussions are crucial in validating our hypotheses and refining the market insights.

In the final stage, we integrate data from both primary and secondary research to deliver a comprehensive market report. This includes validation of market estimates through consultations with key industry stakeholders and refining data points to ensure a holistic view of the APAC Digital Agriculture Market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.