APAC Lactose-Free Butter Market Outlook to 2030

Region:Asia

Author(s):Mukul

Product Code:KROD7200

October 2024

97

About the Report

APAC Lactose-Free Butter Market Overview

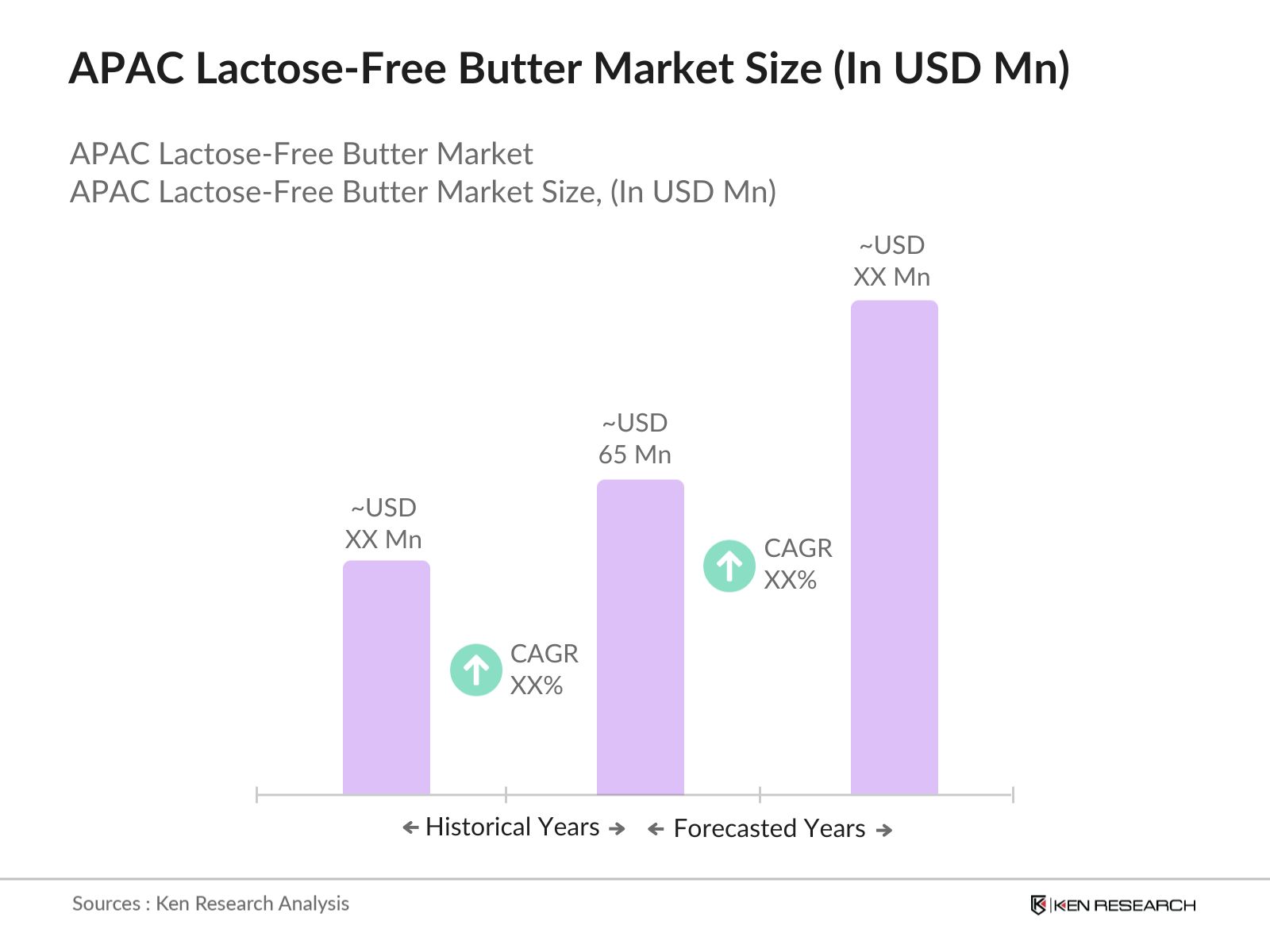

- The APAC Lactose-Free Butter market is valued at USD 65 million, driven by an increasing number of consumers adopting lactose-free diets due to rising lactose intolerance cases across key countries such as China, Japan, and Australia. The demand for healthier alternatives is further stimulated by growing health consciousness and consumer preferences for dairy products that cater to specific dietary needs. This shift is expected to sustain market growth over the coming years, as more consumers turn toward lactose-free alternatives that fit within their health and wellness goals.

- Countries like China and Japan dominate the lactose-free butter market due to their advanced dairy industry infrastructure, large urban populations, and high awareness about lactose intolerance. Japan, for instance, benefits from its strong food manufacturing sector, while China is seeing growth due to its evolving consumer preferences and the adoption of lactose-free dairy products across both urban and rural areas. Australia's strong focus on dairy innovation also makes it a key player in the region.

- Government regulations on dairy safety and labeling in APAC countries are stringent, especially for lactose-free products. In 2024, the Food Safety and Standards Authority of India (FSSAI) implemented new labeling regulations requiring lactose-free products to display detailed nutritional information, ensuring transparency for consumers. Similarly, Australias dairy safety standards, as enforced by Dairy Food Safety Victoria, mandate that all lactose-free dairy products meet strict processing and contamination standards before entering the market.

APAC Lactose-Free Butter Market Segmentation

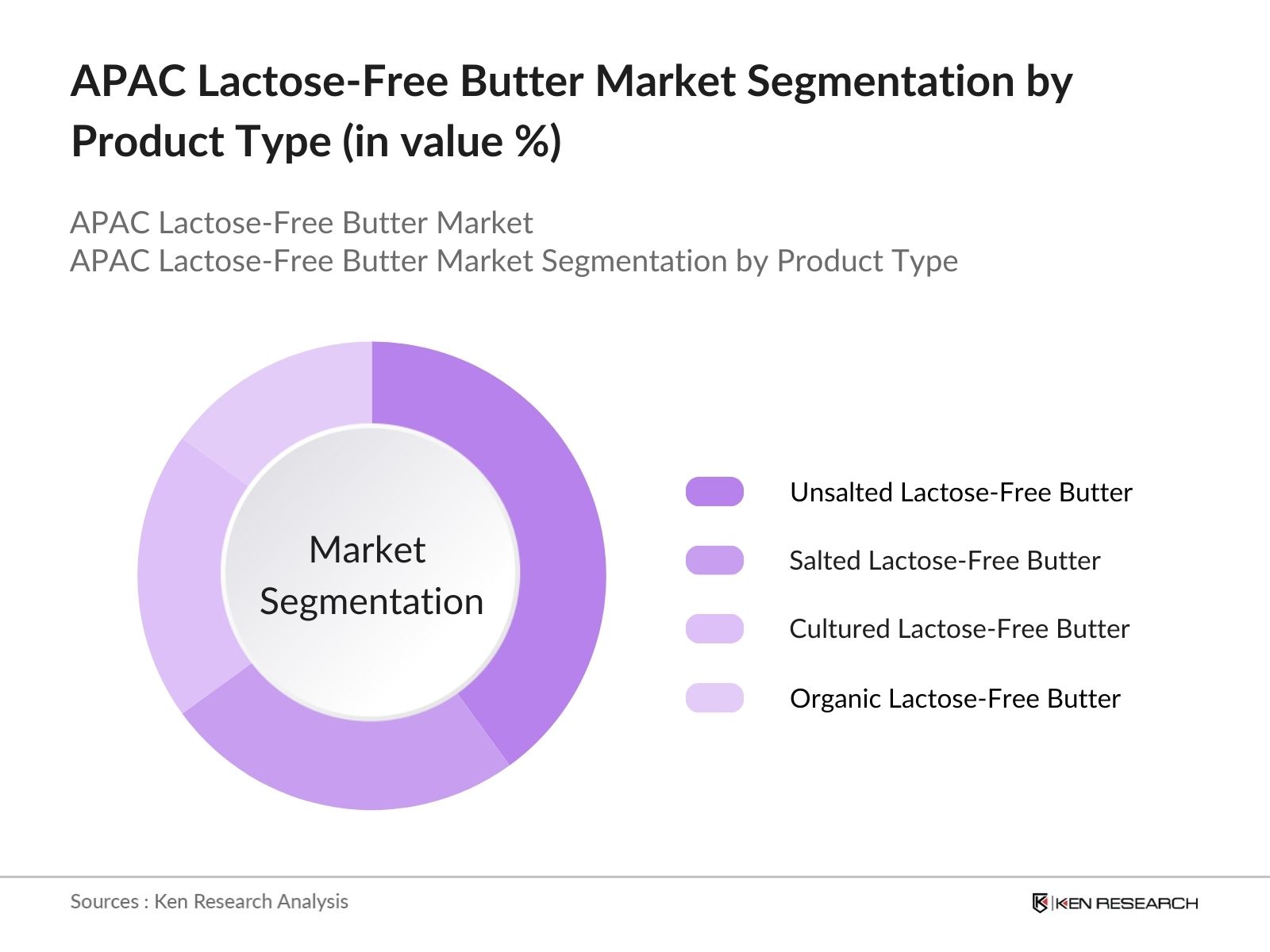

- By Product Type: The APAC Lactose-Free Butter market is segmented by product type into unsalted, salted, cultured, and organic lactose-free butter. The unsalted lactose-free butter holds a dominant share in this segment. Its popularity stems from its versatile use in both cooking and baking, allowing consumers to control the amount of salt in their diets. Moreover, unsalted lactose-free butter is a preferred choice among consumers with specific dietary restrictions, and its growing availability in major supermarkets and online platforms has bolstered its market position.

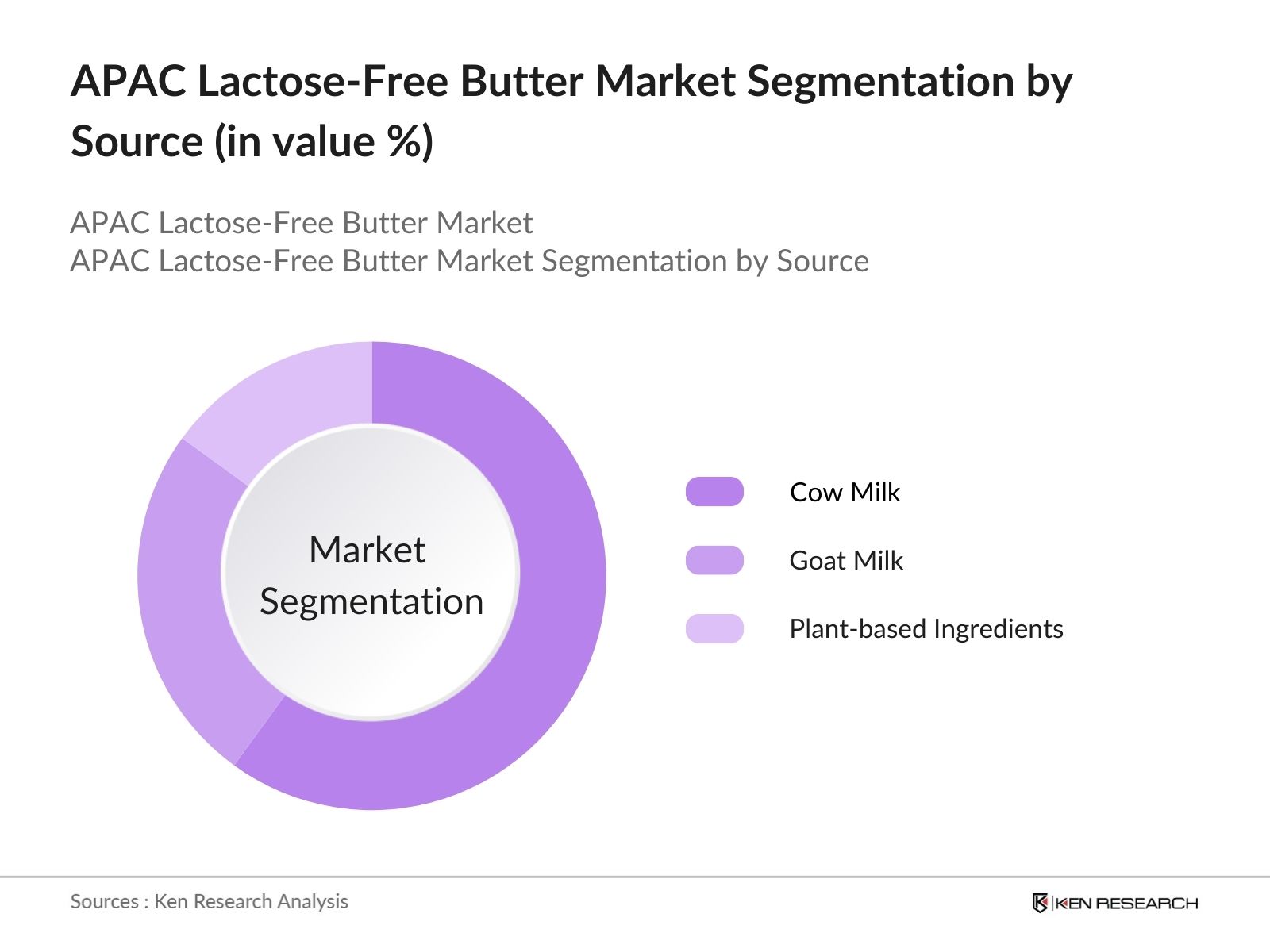

- By Source: The APAC Lactose-Free Butter market is also segmented by source into cow milk, goat milk, and alternative plant-based ingredients. Lactose-free butter made from cow milk continues to lead this segment, driven by its widespread availability and established consumer trust. Dairy from cow milk is a staple across many Asian markets, and lactose-free versions are increasingly being promoted by leading dairy brands. Additionally, cow milk-based butter retains the traditional taste and texture that consumers are accustomed to, making it a popular option in households and foodservice applications.

APAC Lactose-Free Butter Market Competitive Landscape

The APAC Lactose-Free Butter market is characterized by the presence of both regional and global players. Companies are focusing on innovation and expanding their product portfolios to meet the growing demand for lactose-free dairy products. Key market leaders are investing in research and development to produce butter with better taste and nutritional value.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD) |

Product Portfolio |

Innovation Rate |

Market Penetration |

Sustainability Practices |

Strategic Initiatives |

|

Fonterra Co-operative Group |

2001 |

Auckland, New Zealand |

||||||

|

Arla Foods |

1881 |

Aarhus, Denmark |

||||||

|

Lactalis Group |

1933 |

Laval, France |

||||||

|

Saputo Inc. |

1954 |

Montreal, Canada |

||||||

|

Valio Ltd. |

1905 |

Helsinki, Finland |

APAC Lactose-Free Butter Industry Analysis

Growth Drivers

- Rise in Lactose Intolerance (Incidence rate, Dietary Shift): Lactose intolerance is a significant driver for the demand for lactose-free butter in the APAC region. A 2022 study by the National Institutes of Health (NIH) indicated that up to 90% of East Asians are lactose intolerant, with similar patterns found in South Asia. This high prevalence, coupled with dietary shifts toward lactose-free options, is propelling the market growth for alternatives like lactose-free butter. The health implications of lactose intolerance, such as digestive discomfort and bloating, are pushing consumers to seek out dairy alternatives. This trend is reflected in rising healthcare expenditures across APAC, which reached $1.7 trillion in 2022.

- Growing Health Consciousness (Nutritional Preferences, Consumer Trends): Health consciousness in APAC is fueling the adoption of lactose-free butter as consumers become more aware of digestive health and nutrition. A study by the World Bank in 2023 noted that the average life expectancy in East Asia has risen to 76 years, with increasing emphasis on lifestyle diseases, prompting consumers to adopt healthier diets. Lactose-free butter, with fewer digestive side effects, fits well into this trend. Moreover, the rise in healthcare expenditures, particularly in countries like Japan and South Korea, reinforces the demand for nutritious, dairy-alternative products.

- Increasing Product Availability (Product Innovation, Supply Chain Development)

In 2024, lactose-free butter became widely available in retail outlets across major APAC markets, facilitated by supply chain improvements and product innovation. Trade data from the International Trade Centre (ITC) shows a 20% increase in lactose-free dairy product imports into the region between 2022 and 2024. This uptick is driven by improved cold storage logistics and advanced food processing technologies, enabling wider distribution and shelf-life extension. Countries like Australia and New Zealand, known for dairy exports, have also begun focusing on lactose-free options, enhancing product availability in the region.

Market Restraints

- Regulatory Barriers (Food Safety Regulations, Import/Export Constraints): Stringent food safety regulations across APAC pose a challenge for the growth of the lactose-free butter market. Each country has its own set of regulatory requirements, complicating cross-border trade. For instance, Japans Food Sanitation Law mandates strict labeling and safety standards for dairy imports, while India imposes high tariffs on foreign dairy products, as per World Trade Organization (WTO) data. These regulatory hurdles increase the complexity of market entry and limit the speed at which lactose-free butter can penetrate new markets.

- Limited Consumer Awareness (Branding, Educational Efforts): Despite the growing incidence of lactose intolerance, awareness of lactose-free alternatives remains low in certain parts of APAC. In rural areas of Southeast Asia, limited access to nutritional education hampers consumer understanding of lactose intolerance and its symptoms. A 2023 report from the United Nations Educational, Scientific and Cultural Organization (UNESCO) found that 60% of the population in rural Indonesia and the Philippines had low literacy on food-related health issues. This lack of awareness limits the market potential for lactose-free butter in these regions.

APAC Lactose-Free Butter Market Future Outlook

Over the next five years, the APAC Lactose-Free Butter market is expected to show steady growth driven by rising awareness of lactose intolerance, growing consumer demand for health-conscious products, and the continuous introduction of innovative lactose-free dairy alternatives. Companies are focusing on expanding their presence in emerging economies and increasing their product offerings, which will further bolster market growth. As consumer preferences shift toward plant-based and organic dairy alternatives, the lactose-free butter market will benefit from this evolving demand.

Market Opportunities

- Expansion into Emerging Markets: Emerging markets in APAC present significant growth opportunities for lactose-free butter, driven by demographic changes and rising disposable income. In 2022, the World Bank reported that Vietnam's GDP per capita crossed the $4,000 threshold, indicating an expanding middle class with greater purchasing power for premium and health-oriented products like lactose-free butter. Countries like Indonesia, with a population of 273 million, are also experiencing similar trends, making them prime targets for market expansion.

- Technological Advancements in Dairy Alternatives: Technological innovations in the production of lactose-free butter, such as enzyme-based lactose removal and advances in plant-based dairy alternatives, are creating opportunities for more cost-efficient production. According to data from the FAO, new enzyme technologies introduced in 2023 have reduced lactose removal costs by 10%, making lactose-free dairy products more affordable for consumers. Additionally, countries like China are investing in research and development (R&D) to improve the production of dairy alternatives, further supporting market growth.

Scope of the Report

|

Product Type |

Unsalted Lactose-Free Butter |

|

Salted Lactose-Free Butter |

|

|

Cultured Lactose-Free Butter |

|

|

Organic Lactose-Free Butter |

|

|

Application |

Retail (Supermarkets, Online) |

|

Food Service (Hotels, Restaurants) |

|

|

Industrial (Bakery, Confectionery) |

|

|

Source |

Cow Milk |

|

Goat Milk |

|

|

Alternative Plant-based Ingredients |

|

|

Distribution Channel |

Online Channels |

|

Offline Channels (Retail, Specialty) |

|

|

Foodservice Distributors |

|

|

Region |

East Asia |

|

South Asia |

|

|

Southeast Asia |

|

|

Oceania |

Products

Key Target Audience

Lactose-free dairy manufacturers

Food and beverage companies

Retail and online distribution chains

Government and regulatory bodies (Food Safety and Standards Authority of India, Ministry of Agriculture)

Health-conscious consumers

Foodservice and hospitality industry

Investors and venture capitalist firms

Sustainability-focused organizations

Companies

Players Mentioned in the Report:

Fonterra Co-operative Group

Arla Foods

Lactalis Group

Saputo Inc.

Valio Ltd.

Green Valley Creamery

Anchor Foods

The Organic Dairy Co.

Kerry Group

Miyokos Creamery

Lurpak

Vitalite Dairy-Free

Follow Your Heart

FrieslandCampina

Danone S.A.

Table of Contents

1. APAC Lactose-Free Butter Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. APAC Lactose-Free Butter Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. APAC Lactose-Free Butter Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Lactose Intolerance (Incidence rate, Dietary Shift)

3.1.2. Growing Health Consciousness (Nutritional Preferences, Consumer Trends)

3.1.3. Increasing Product Availability (Product Innovation, Supply Chain Development)

3.1.4. Retail and Online Expansion (Market Penetration, Channel Growth)

3.2. Market Challenges

3.2.1. High Production Costs (Cost of Raw Materials, Manufacturing Processes)

3.2.2. Regulatory Barriers (Food Safety Regulations, Import/Export Constraints)

3.2.3. Limited Consumer Awareness (Branding, Educational Efforts)

3.3. Opportunities

3.3.1. Expansion into Emerging Markets (Market Penetration, Demographic Shifts)

3.3.2. Technological Advancements in Dairy Alternatives (Product Innovation, Production Efficiency)

3.3.3. Partnerships with Retail Chains (Distribution Channels, Consumer Reach)

3.4. Trends

3.4.1. Premiumization of Lactose-Free Butter Products (Organic, Grass-Fed, Fortified Options)

3.4.2. Adoption of Plant-Based Ingredients (Hybrid Butter, Alternative Ingredients)

3.4.3. Rise in Private Label Offerings (Retailer-led Innovation, Price Competition)

3.5. Government Regulations

3.5.1. APAC Dairy Regulations (Safety Standards, Labeling Requirements)

3.5.2. Import-Export Policies (Trade Barriers, Tariff Structures)

3.5.3. Nutritional Standards and Guidelines (Fortification, Health Claims)

3.6. SWOT Analysis

3.7. Value Chain and Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. APAC Lactose-Free Butter Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Unsalted Lactose-Free Butter

4.1.2. Salted Lactose-Free Butter

4.1.3. Cultured Lactose-Free Butter

4.1.4. Organic Lactose-Free Butter

4.2. By Application (In Value %)

4.2.1. Retail (Supermarkets, Hypermarkets, Online)

4.2.2. Food Service (Hotels, Restaurants, Cafes)

4.2.3. Industrial (Bakery, Confectionery, Packaged Food)

4.3. By Source (In Value %)

4.3.1. Cow Milk

4.3.2. Goat Milk

4.3.3. Alternative Plant-based Ingredients

4.4. By Distribution Channel (In Value %)

4.4.1. Online Channels

4.4.2. Offline Channels (Retailers, Supermarkets, Specialty Stores)

4.4.3. Foodservice Distributors

4.5. By Region (In Value %)

4.5.1. East Asia (China, Japan, South Korea)

4.5.2. South Asia (India, Sri Lanka, Bangladesh)

4.5.3. Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia)

4.5.4. Oceania (Australia, New Zealand)

5. APAC Lactose-Free Butter Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Fonterra Co-operative Group

5.1.2. Arla Foods

5.1.3. Lactalis Group

5.1.4. Saputo Inc.

5.1.5. FrieslandCampina

5.1.6. Anchor Foods

5.1.7. The Organic Dairy Co.

5.1.8. Green Valley Creamery

5.1.9. Valio Ltd.

5.1.10. Miyokos Creamery

5.1.11. Kerry Group

5.1.12. Danone S.A.

5.1.13. Lurpak

5.1.14. Vitalite Dairy-Free

5.1.15. Follow Your Heart

5.2 Cross Comparison Parameters (Revenue, Production Volume, Regional Presence, Product Portfolio, Innovation Rate, Sustainability Practices, Strategic Partnerships, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. APAC Lactose-Free Butter Market Regulatory Framework

6.1. Dairy Production Standards

6.2. Compliance Requirements

6.3. Certification Processes (Organic, Lactose-Free Labels, Non-GMO)

7. APAC Lactose-Free Butter Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. APAC Lactose-Free Butter Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Source (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. APAC Lactose-Free Butter Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In the initial phase, a comprehensive market ecosystem map was developed, identifying all stakeholders such as dairy producers, lactose-free product manufacturers, and distribution networks. Data were collected using secondary research methods, including reports from industry associations and government databases, to identify the key variables that drive the APAC Lactose-Free Butter market.

Step 2: Market Analysis and Construction

In this stage, historical market data related to lactose-free butter production, distribution, and consumption were analyzed. The assessment included the evaluation of product penetration rates and regional market dynamics. This enabled the team to construct a precise revenue generation model based on existing market conditions.

Step 3: Hypothesis Validation and Expert Consultation

Market experts and representatives from leading dairy companies were consulted through computer-assisted telephone interviews (CATIs) to validate the hypotheses derived from desk research. These consultations provided in-depth operational insights into product performance, distribution challenges, and consumer preferences.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing the data collected from interviews, market analysis, and proprietary databases to generate a comprehensive analysis of the APAC Lactose-Free Butter market. This phase ensured accuracy in the final market projections and segmentation.

Frequently Asked Questions

01. How big is the APAC Lactose-Free Butter market?

The APAC Lactose-Free Butter market is valued at USD 65 million, driven by rising consumer demand for lactose-free products due to increasing cases of lactose intolerance and health-conscious dietary choices.

02. What are the challenges in the APAC Lactose-Free Butter market?

The market faces challenges such as high production costs, stringent government regulations, and limited consumer awareness, particularly in less urbanized areas. Additionally, the cost of raw materials is a significant challenge for producers.

03. Who are the major players in the APAC Lactose-Free Butter market?

Key players include Fonterra Co-operative Group, Arla Foods, Lactalis Group, Saputo Inc., and Valio Ltd. These companies dominate the market due to their extensive distribution networks, strong R&D initiatives, and product innovation.

04. What are the growth drivers of the APAC Lactose-Free Butter market?

Key growth drivers include the increasing prevalence of lactose intolerance, rising health consciousness, and the expansion of retail and online channels for lactose-free dairy products. Moreover, continuous product innovations are bolstering market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.