APAC Stationary Fuel Cell Market Outlook to 2030

Region:Asia

Author(s):Mukul

Product Code:KROD3439

October 2024

94

About the Report

APAC Stationary Fuel Cell Market Overview

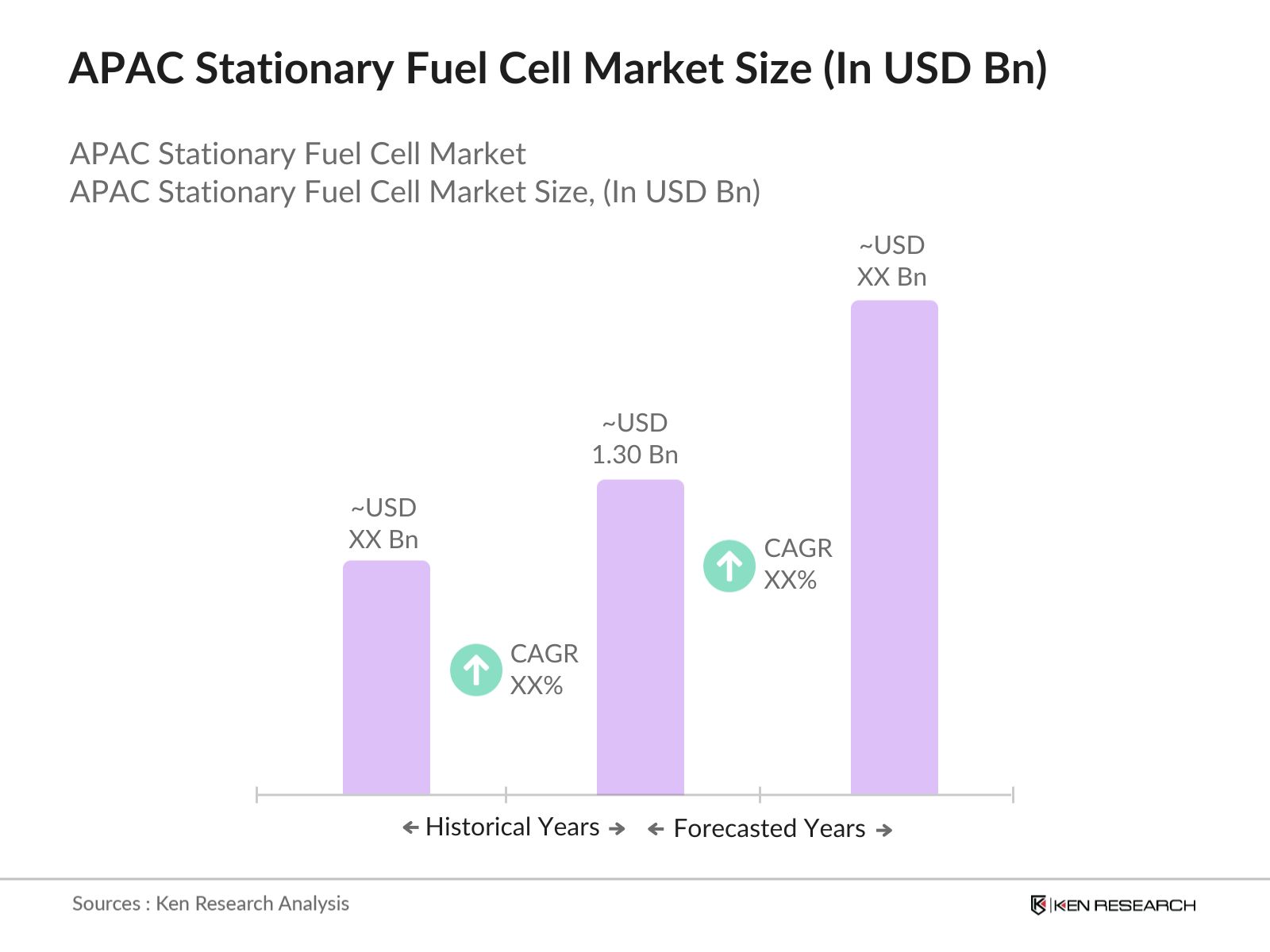

- The APAC stationary fuel cell market is valued at USD 1.30 billion in 2023, driven primarily by the demand for clean and efficient energy solutions across residential, commercial, and industrial sectors. Fuel cells are increasingly recognized for their role in reducing carbon emissions, and many governments in the region are incentivizing their adoption through subsidies and tax credits. Key drivers include rising energy demands and the growing push for renewable energy alternatives.

- Japan and South Korea dominate the APAC stationary fuel cell market due to their early adoption of hydrogen energy solutions and substantial investments in fuel cell research and development. These countries are also home to several leading fuel cell manufacturers, which further contributes to their market dominance. Japan's strategic push for a hydrogen-based economy, alongside South Koreas hydrogen roadmap, are key factors in their leadership positions.

- Several APAC countries have established hydrogen roadmaps that emphasize the development of fuel cell technologies. Japan's Basic Hydrogen Strategy, launched in 2020 and ongoing through 2024, sets a goal of expanding hydrogen utilization in fuel cells, with a projected investment of $1.5 billion annually. Similarly, South Koreas Hydrogen Economy Roadmap supports hydrogen adoption in energy systems, including stationary fuel cells, by establishing hydrogen clusters and refueling stations.

APAC Stationary Fuel Cell Market Segmentation

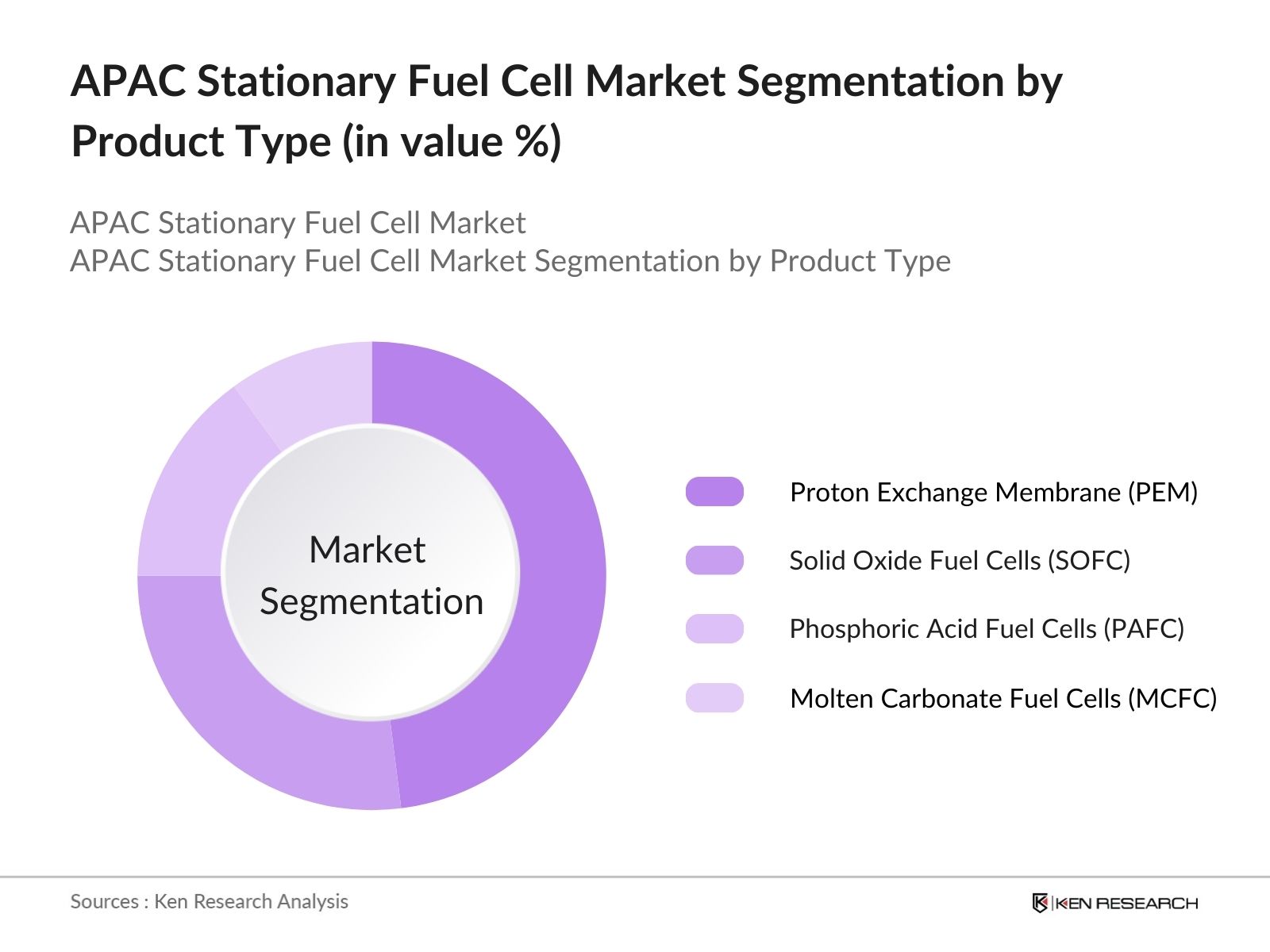

- By Product Type: The APAC stationary fuel cell market is segmented by product type into Proton Exchange Membrane (PEM) Fuel Cells, Solid Oxide Fuel Cells (SOFC), Phosphoric Acid Fuel Cells (PAFC), and Molten Carbonate Fuel Cells (MCFC). PEM fuel cells hold the dominant market share due to their high efficiency and suitability for a wide range of applications, from small residential systems to large-scale commercial and industrial power generation. The increasing demand for decentralized energy systems further propels the growth of PEM fuel cells in the APAC region.

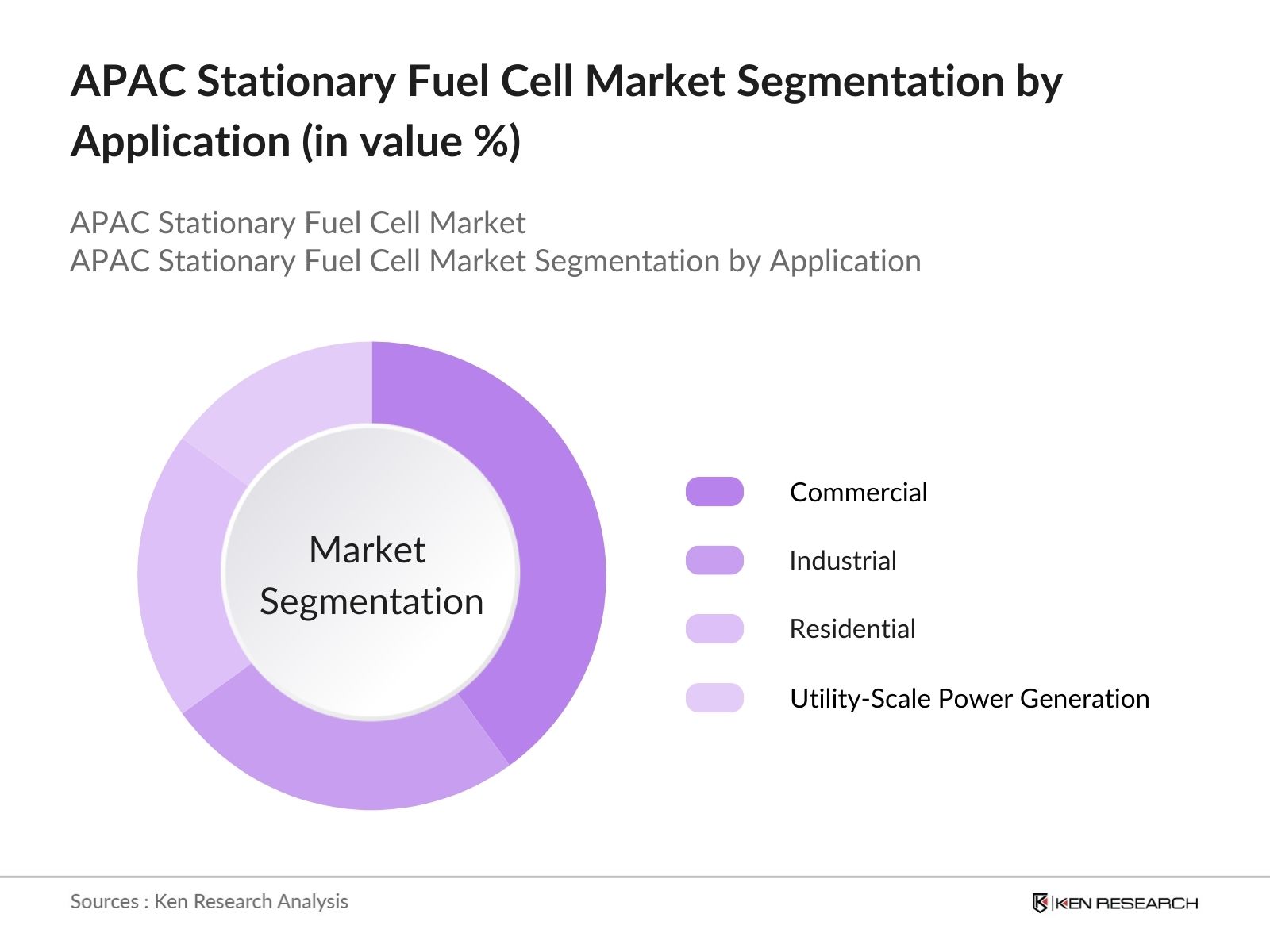

- By Application: The APAC stationary fuel cell market is segmented by application into Residential, Commercial, Industrial, and Utility-Scale Power Generation. The commercial sector dominates the market, driven by increasing adoption of fuel cells as backup power systems for data centers, hospitals, and office buildings. Commercial establishments are opting for fuel cells to ensure a continuous power supply while reducing their carbon footprint, which contributes to the dominance of this sub-segment.

APAC Stationary Fuel Cell Market Competitive Landscape

The APAC stationary fuel cell market is dominated by key players who are pioneering the commercialization of fuel cells across various applications. Companies such as Panasonic Corporation, Toshiba Energy Systems, and FuelCell Energy hold a strong position due to their extensive research, technological advancements, and large-scale production capabilities. The consolidation of market share among these players underscores their influence on market direction and development.

APAC Stationary Fuel Cell Industry Analysis

APAC Stationary Fuel Cell Market Growth Drivers

- Government Support for Renewable Energy Transition: Government support has been pivotal in driving the growth of stationary fuel cell technology in the Asia-Pacific region. For example, Japans Ministry of Economy, Trade, and Industry (METI) offers subsidies for renewable energy installations, including fuel cells, under its "Energy Efficiency and Conservation" program. In 2022, Japan allocated $2.5 billion for renewable energy projects, including hydrogen fuel cell initiatives. Similarly, South Korea has introduced tax credits under the Renewable Portfolio Standards (RPS), which are aimed at enhancing the adoption of fuel cells in residential and industrial applications.

- Increasing Energy Efficiency Demands: The demand for energy efficiency across industries is rising rapidly, primarily due to the growing pressure to reduce energy consumption. Stationary fuel cells can achieve an energy efficiency rate of 60%, significantly higher than conventional energy sources. In South Korea, energy consumption per capita stood at approximately 5,900 kWh in 2023, necessitating the adoption of more efficient technologies like fuel cells. Additionally, fuel cells offer combined heat and power (CHP) systems, which can optimize overall energy utilization, making them an attractive solution for reducing waste.

- Growing Industrial and Residential Applications: The application of stationary fuel cells is expanding in both industrial and residential sectors, particularly in countries like Japan and China. In Japan, over 400,000 households had adopted micro-CHP fuel cells (Ene-Farm) by the end of 2023. Additionally, China's industrial sector is increasingly adopting stationary fuel cells for backup power systems in critical infrastructure, with over 300 MW of installed capacity in 2023. This growing usage across sectors highlights the versatility of fuel cells as an energy solution.

APAC Stationary Fuel Cell Market Restraints

- Competition from Alternative Technologies: Stationary fuel cells face strong competition from alternative technologies such as solar energy and battery storage systems. In China, the cumulative installed capacity of solar power was 393 GW by mid-2024, compared to the growing but still smaller stationary fuel cell capacity. Additionally, the rapid growth of battery storage systems, which have become 50% cheaper in the last decade, makes them a strong alternative to stationary fuel cells in both industrial and residential applications.

- Infrastructure Limitations for Hydrogen Supply: The infrastructure for hydrogen supply is still in its infancy across many APAC countries. While Japan and South Korea have made strides in establishing hydrogen refueling stations, with Japan operating 166 stations by 2023, other countries in the region lag behind. For instance, in 2023, China had only 36 operational hydrogen refueling stations for stationary fuel cells, hindering large-scale deployment. The lack of hydrogen transportation and storage infrastructure remains a bottleneck for further market growth.

APAC Stationary Fuel Cell Market Future Outlook

Over the next five years, the APAC stationary fuel cell market is expected to witness significant growth, driven by advancements in fuel cell technology, increasing energy efficiency demands, and growing government support for clean energy initiatives. Major economies in the region, such as Japan, South Korea, and China, are actively investing in hydrogen infrastructure and fuel cell commercialization to meet their energy sustainability goals. Additionally, technological innovations, such as the development of hybrid fuel cell systems, are likely to further accelerate market growth.

Market Opportunities

- Technological Advancements in Fuel Cell Efficiency: Recent advancements in fuel cell efficiency, particularly in solid oxide and proton exchange membrane fuel cells, are expected to create new market opportunities. For example, fuel cells in Japan achieved efficiency rates above 65% in 2023, surpassing the global average of 50%. As these efficiency improvements continue, companies are exploring the potential of utilizing fuel cells for large-scale industrial applications, particularly in remote or off-grid areas where energy reliability is critical.

- Expansion into Remote and Off-Grid Areas: Stationary fuel cells offer a viable solution for energy generation in remote and off-grid areas, particularly in countries like Indonesia and the Philippines, where over 70 million people lack reliable access to electricity. In Indonesia, the governments Rural Electrification Program is expected to support fuel cell deployments in isolated regions, providing clean and efficient energy. As of 2023, the Indonesian government allocated $700 million for energy infrastructure in these areas, including support for alternative energy solutions like stationary fuel cells.

Scope of the Report

|

By Product Type |

Proton Exchange Membrane (PEM) Fuel Cells |

|

Solid Oxide Fuel Cells (SOFC) |

|

|

Phosphoric Acid Fuel Cells (PAFC) |

|

|

Molten Carbonate Fuel Cells (MCFC) |

|

|

By Application |

Residential |

|

Commercial |

|

|

Industrial |

|

|

Utility-Scale Power Generation |

|

|

By Capacity |

Below 1 kW |

|

1 kW to 10 kW |

|

|

10 kW to 100 kW |

|

|

Above 100 kW |

|

|

By Fuel Type |

Hydrogen |

|

Natural Gas |

|

|

Biogas |

|

|

By Region |

East Asia |

|

Southeast Asia |

|

|

South Asia |

|

|

Oceania |

Products

Key Target Audience

Investors and Venture Capital Firms

Government and Regulatory Bodies (Ministry of Energy, Ministry of Industry and Trade)

Hydrogen Fuel Suppliers

Fuel Cell Manufacturers

Energy Infrastructure Developers

Utility Companies

Commercial and Industrial End-Users

Renewable Energy Policy Makers

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Panasonic Corporation

Toshiba Energy Systems & Solutions Corporation

FuelCell Energy, Inc.

Bloom Energy Corporation

Doosan Fuel Cell Co., Ltd.

Ballard Power Systems

Plug Power Inc.

Mitsubishi Power, Ltd.

Siemens Energy

Ceres Power Holdings plc

Table of Contents

1. APAC Stationary Fuel Cell Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. APAC Stationary Fuel Cell Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. APAC Stationary Fuel Cell Market Analysis

3.1.Growth Drivers

3.1.1. Government support for renewable energy transition (Subsidies, Tax Credits)

3.1.2. Increasing energy efficiency demands

3.1.3. Growing industrial and residential applications

3.1.4. Declining costs of fuel cell technology

3.2.Market Challenges

3.2.1. High initial investment costs

3.2.2. Competition from alternative technologies (Batteries, Solar Energy)

3.2.3. Infrastructure limitations for hydrogen supply

3.3.Opportunities

3.3.1. Technological advancements in fuel cell efficiency

3.3.2. Expansion into remote and off-grid areas

3.3.3. Growing partnerships with utilities and energy companies

3.4.Trends

3.4.1. Adoption of green hydrogen in fuel cells

3.4.2. Integration of fuel cells into smart grids

3.4.3. Development of hybrid fuel cell systems (Fuel Cell + Battery)

3.5.Government Regulations

3.5.1. National hydrogen roadmaps and policies

3.5.2. Emission reduction targets and compliance

3.5.3. Fuel cell vehicle deployment incentives

4. APAC Stationary Fuel Cell Market Segmentation

4.1.By Product Type (In Value %)

4.1.1. Proton Exchange Membrane (PEM) Fuel Cells

4.1.2. Solid Oxide Fuel Cells (SOFC)

4.1.3. Phosphoric Acid Fuel Cells (PAFC)

4.1.4. Molten Carbonate Fuel Cells (MCFC)

4.2.By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.2.4. Utility-Scale Power Generation

4.3.By Capacity (In Value %)

4.3.1. Below 1 kW

4.3.2. 1 kW to 10 kW

4.3.3. 10 kW to 100 kW

4.3.4. Above 100 kW

4.4.By Fuel Type (In Value %)

4.4.1. Hydrogen

4.4.2. Natural Gas

4.4.3. Biogas

4.5.By Region (In Value %)

4.5.1. East Asia

4.5.2. Southeast Asia

4.5.3. South Asia

4.5.4. Oceania

5. APAC Stationary Fuel Cell Market Competitive Analysis

(Revenue, Installed Capacity, Hydrogen Production, Technology Portfolio, Strategic Partnerships, Sustainability Initiatives, Market Share, Employee Count)

6. APAC Stationary Fuel Cell Market Regulatory Framework

6.1. Hydrogen safety standards

6.2. Certification processes

6.3. Environmental impact regulations

7. APAC Stationary Fuel Cell Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. APAC Stationary Fuel Cell Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Capacity (In Value %)

8.4. By Fuel Type (In Value %)

8.5. By Region (In Value %)

9. APAC Stationary Fuel Cell Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involved constructing a comprehensive ecosystem map, encompassing all major stakeholders in the APAC stationary fuel cell market. This was supported by extensive desk research using secondary and proprietary databases to collect reliable industry-level information. The primary objective was to identify and define the critical variables influencing market dynamics, such as hydrogen production capacity, government policies, and technological advancements.

Step 2: Market Analysis and Construction

In this phase, historical data on the APAC stationary fuel cell market was compiled and analyzed. Key parameters such as market penetration, the proportion of fuel cells used in residential vs. industrial applications, and revenue generation were examined. An evaluation of service quality statistics ensured the accuracy and reliability of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed and validated through expert consultations. These consultations, conducted via computer-assisted telephone interviews (CATIs) with representatives from leading companies, provided valuable financial and operational insights, ensuring the accuracy of the market data and projections.

Step 4: Research Synthesis and Final Output

The final phase involved direct engagement with multiple fuel cell manufacturers to obtain detailed insights into product segments, sales performance, and technological innovations. This interaction helped verify and complement the bottom-up approach used in estimating market size and projections, resulting in a comprehensive and validated analysis of the APAC stationary fuel cell market.

Frequently Asked Questions

1. How big is the APAC Stationary Fuel Cell Market?

The APAC stationary fuel cell market is valued at USD 1.30 billion in 2023, driven by the growing demand for clean energy solutions across multiple sectors, including residential, commercial, and industrial applications.

2. What are the challenges in the APAC Stationary Fuel Cell Market?

Challenges include high initial investment costs, competition from alternative energy storage technologies like batteries, and the lack of a developed hydrogen infrastructure in many APAC countries.

3. Who are the major players in the APAC Stationary Fuel Cell Market?

Key players include Panasonic Corporation, Toshiba Energy Systems & Solutions Corporation, FuelCell Energy, Inc., Bloom Energy Corporation, and Doosan Fuel Cell Co., Ltd.

4. What are the growth drivers of the APAC Stationary Fuel Cell Market?

Key drivers include increasing government support for renewable energy technologies, advancements in fuel cell efficiency, and growing demand for decentralized power generation systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.