Asia Pacific Diagnostic Imaging Market Outlook to 2030

Region:Asia

Author(s):Shreya Garg

Product Code:KROD2777

November 2024

96

About the Report

Asia Pacific Diagnostic Imaging Market Overview

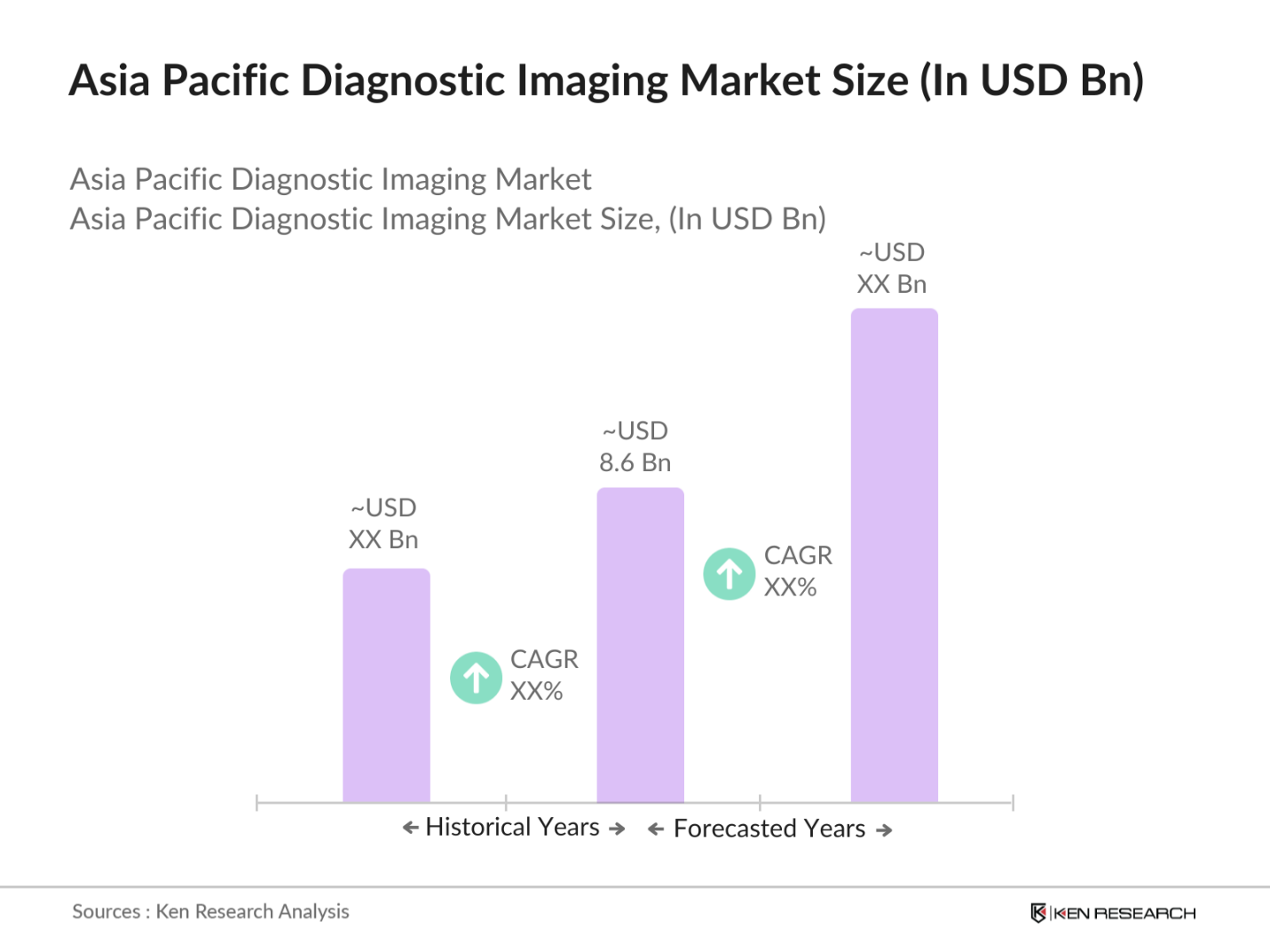

- The Asia Pacific Diagnostic Imaging Market was valued at USD 8.6 billion in 2023. This growth is primarily driven by the increasing prevalence of chronic diseases, advancements in imaging technologies, and the rising demand for early and accurate diagnosis. Additionally, the growing aging population, particularly in countries like Japan and China, contributes significantly to the market expansion.

- Prominent players in the Asia Pacific Diagnostic Imaging Market include GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings Corporation. These companies have established strong footholds in the market through continuous innovation, strategic partnerships, and extensive distribution networks.

- In January 2023, Siemens Healthineers launched the MAGNETOM Free.Max MRI scanner in the Asia Pacific region. This scanner is notable for being the world's first ultra-low-field MRI system, operating at a field strength of 0.55 Tesla. Its design aims to enhance accessibility to MRI technology, particularly in developing regions, due to its lower cost and improved safety profile.

- Japan dominates the Asia Pacific Diagnostic Imaging Market in 2023. This dominance is attributed to the country's advanced healthcare infrastructure, high healthcare expenditure, and early adoption of cutting-edge imaging technologies. Additionally, the presence of leading diagnostic imaging companies and a strong focus on R&D activities further bolster Japan's leading position in the market.

Asia Pacific Diagnostic Imaging Market Segmentation

The Asia Pacific Diagnostic Imaging Market can be segmented by various factors like modality, application, and region.

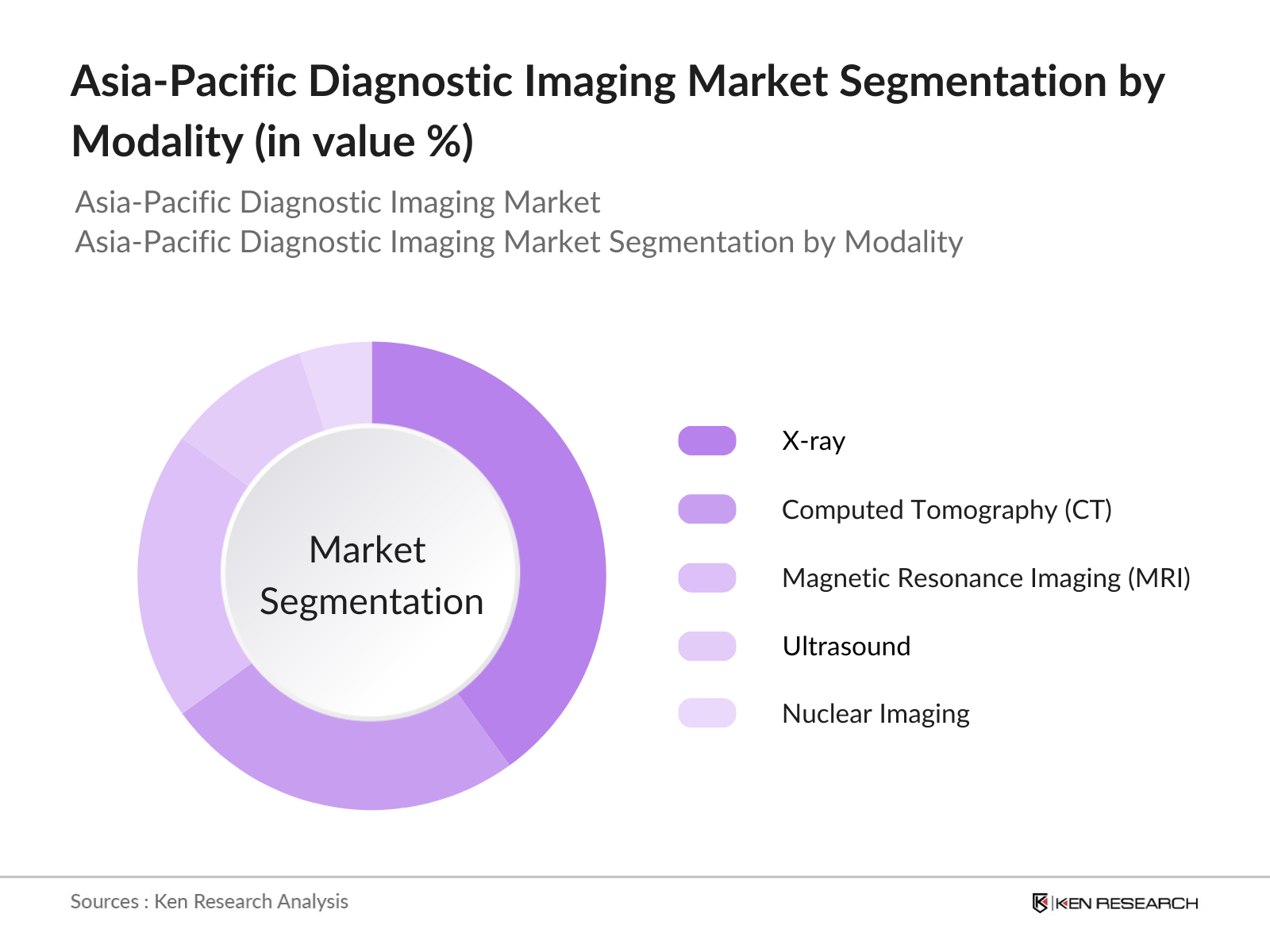

- By Modality: This market is segmented by modality into X-ray, computed tomography (CT), magnetic resonance imaging (MRI), ultrasound, and nuclear imaging. In 2023, X-ray held the largest market share, driven by its widespread use in diagnosing fractures, infections, and tumors. This dominance is due to its cost-effectiveness, quick imaging capability, and extensive application across various medical conditions.

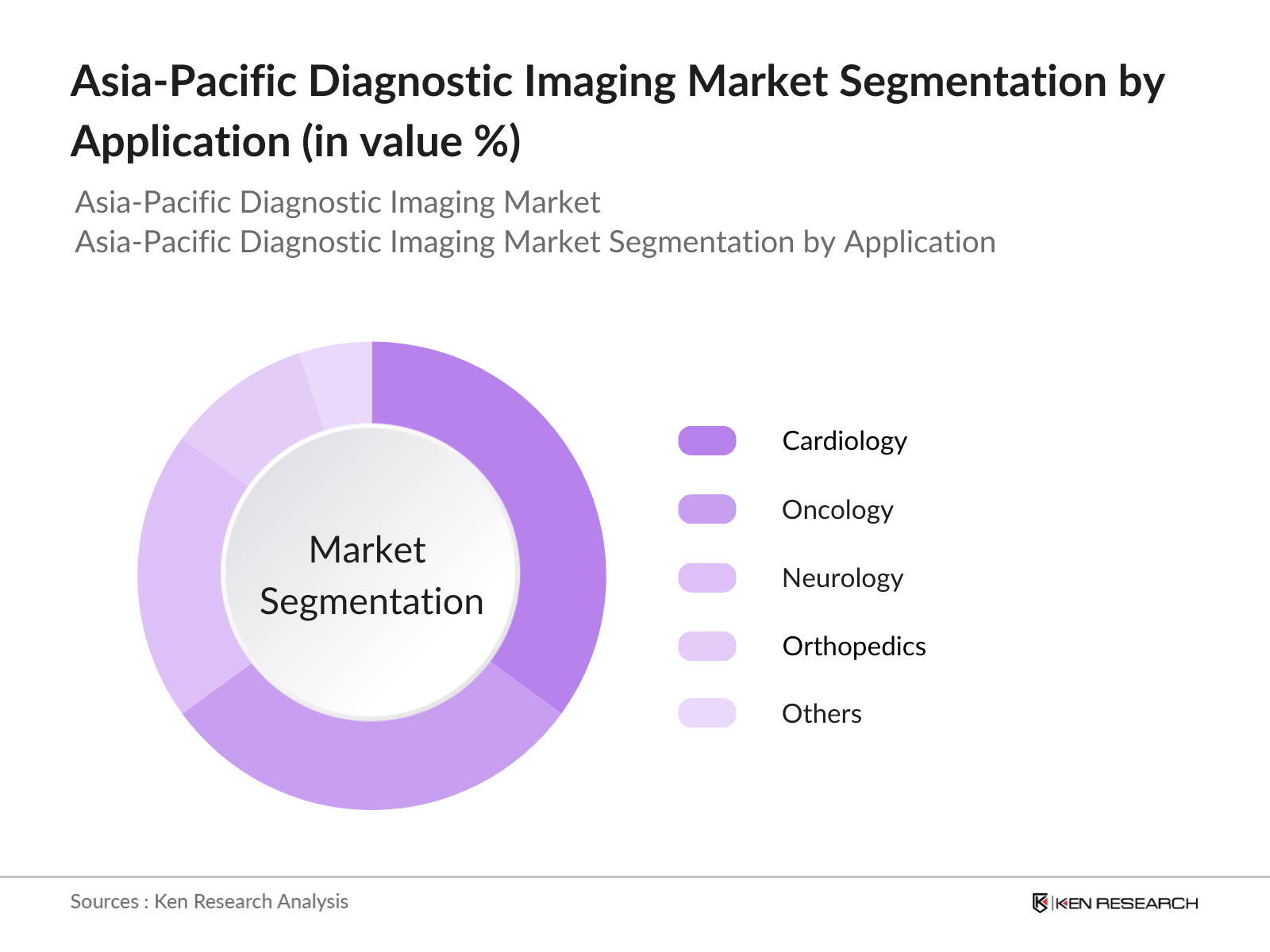

- By Application: This market is segmented by application into cardiology, oncology, neurology, orthopedics. In 2023, cardiology held a dominant market share, driven by the increasing prevalence of cardiovascular diseases and the need for accurate diagnosis. Advanced imaging technologies enable early detection and management of heart conditions, ensuring better patient outcomes.

By Region: This market is segmented by country into China, Japan, India, South Korea, and Australia. In 2023, China held the largest market share, driven by substantial government investment in healthcare infrastructure, rapid urbanization, and a growing aging population. The government's Healthy China 2030 initiative has boosted the adoption of advanced imaging technologies across the country.

Asia Pacific Diagnostic Imaging Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

GE Healthcare |

1892 |

Chicago, USA |

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

|

Canon Medical Systems |

1930 |

Otawara, Japan |

|

Fujifilm Holdings Corp. |

1934 |

Tokyo, Japan |

- Philips: Carestream Health signed an agreement to sell its healthcare information systems business to Philips on March 7, 2019. This acquisition aimed to enhance Philips' healthcare IT portfolio and improve its position in the diagnostic imaging market by integrating Carestream's enterprise imaging solutions into its offerings. It strengthens Philips' capabilities in providing advanced imaging IT solutions to healthcare providers.

- Canon Medical Systems: Canon Medical Systems introduced the "Aquilion ONE PRISM" CT scanner in 2024, combining advanced AI capabilities with high-speed imaging. The Aquilion ONE PRISM utilizes the Advanced Intelligent Clear-IQ Engine (AiCE) for CT reconstruction, leveraging deep learning to differentiate between true signals and noise, resulting in clear images delivered quickly.

Asia Pacific Diagnostic Imaging Industry Analysis

Growth Drivers

- Increasing Prevalence of Chronic Diseases: The number of deaths due to cancer in the WHO South-East Asia Region was 1.5 million in 2022, an increase by almost one third compared to ten years before. The rising incidence of chronic diseases is driving the demand for diagnostic imaging as early detection is critical for effective treatment. The burden of chronic diseases is expected to increase, necessitating more advanced diagnostic imaging solutions to improve patient outcomes.

- Expansion of Healthcare Infrastructure: In 2024, countries like India and China heavily invested in healthcare infrastructure, with India allocating USD 10 billion and China investing hugely in healthcare facilities. These investments aim to improve access to healthcare services, including diagnostic imaging. As new hospitals and diagnostic centers are established, the demand for advanced imaging technologies is set to rise, facilitating market growth.

- Rising Medical Tourism: The Asia Pacific region, particularly countries like Thailand and Singapore, saw increase in no. of medical tourists in 2024, driven by the availability of high-quality and cost-effective medical services. The influx of medical tourists seeking advanced diagnostic services has spurred the demand for state-of-the-art imaging technologies, contributing to the market's growth.

Challenges

- Lack of Skilled Professionals: The Asia Pacific region faces a shortage of trained radiologists and imaging technicians. In 2024, it was reported that India has one radiologist to about every 220,000 inhabitants. China has one for about every 42,000 inhabitants. This lack of skilled personnel hampers the effective utilization of advanced diagnostic imaging equipment, affecting the overall market performance.

- Limited Reimbursement Policies: Reimbursement policies for diagnostic imaging procedures vary across the Asia Pacific region. Countries like Indonesia and Vietnam had limited reimbursement schemes, covering only basic imaging procedures. This lack of comprehensive reimbursement policies can discourage patients from opting for advanced imaging services, thereby constraining market growth.

Government Initiatives

- China's Healthy China 2030 Plan: The Healthy China 2030 initiative, launched in 2016, aims to improve health outcomes and healthcare infrastructure across China, focusing on equitable access and the integration of advanced technologies in healthcare including diagnostic imaging. This plan focuses on improving healthcare infrastructure, integrating advanced imaging technologies, and training healthcare professionals, thus driving market growth.

- Japan's AI-Powered Imaging Initiative: Japan is indeed advancing in AI applications within healthcare, with a massive emphasis on diagnostic imaging. The market for AI healthcare tools is projected to grow, with estimates suggesting it could be worth around USD 114 million by 2027, driven by startups and innovations in AI technology. The governments support for AI-driven technologies is expected to accelerate the adoption of advanced imaging solutions in the country.

Asia Pacific Diagnostic Imaging Market Future Outlook

The Asia Pacific Diagnostic Imaging Market is projected to increase exponentially by 2028. The future growth will be driven by ongoing technological advancements, such as AI integration in imaging systems, the increasing adoption of minimally invasive procedures, and expanding healthcare infrastructure in emerging economies.

Future Market Trends

Advancements in Portable Imaging Devices: Portable imaging devices are anticipated to gain traction over the next five years, driven by the need for point-of-care diagnostics. These devices will enable immediate diagnostic capabilities in emergency settings and remote locations, enhancing healthcare delivery. By 2028, portable imaging devices are expected to represent a substantial segment of the market, with increasing adoption in both urban and rural areas.

Expansion of Precision Medicine: The rise of precision medicine will drive the demand for advanced diagnostic imaging technologies that provide detailed and accurate diagnostic information. Imaging technologies will play a crucial role in personalized treatment plans, leading to better patient outcomes. The precision medicine initiatives are projected to drive investments in advanced imaging technologies, further boosting market growth.

Scope of the Report

|

By Modality |

X-ray Computed tomography (CT) Magnetic resonance imaging (MRI) Ultrasound Nuclear imaging |

|

By Application |

Cardiology Oncology Neurology Orthopedics Others |

|

By Region |

North South East West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Hospitals and Clinics

Diagnostic Centers

Medical Equipment Manufacturers

Pharmaceutical Companies

Health Insurance Companies

Healthcare IT Companies

Telemedicine Providers

Banks and Financial Institutions

Investors and VC Firms

Ministry of Health (various countries)

National Health Service Agencies

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

GE Healthcare

Siemens Healthineers

Philips Healthcare

Canon Medical Systems

Fujifilm Holdings Corporation

Hitachi Medical Systems

Shimadzu Corporation

Hologic Inc.

Mindray Medical International Limited

Samsung Medison

Carestream Health

Konica Minolta Healthcare

Agfa Healthcare

Toshiba Medical Systems

Esaote S.p.A.

Table of Contents

1. Asia Pacific Diagnostic Imaging Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Diagnostic Imaging Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Diagnostic Imaging Market Analysis

3.1. Growth Drivers

3.1.1. Technological Advancements

3.1.2. Rising Prevalence of Chronic Diseases

3.1.3. Increasing Geriatric Population

3.1.4. Government Initiatives and Funding

3.2. Market Challenges

3.2.1. High Equipment Costs

3.2.2. Shortage of Skilled Radiologists

3.2.3. Regulatory and Compliance Issues

3.3. Opportunities

3.3.1. Emerging Markets Expansion

3.3.2. Integration of Artificial Intelligence

3.3.3. Development of Portable Imaging Devices

3.4. Trends

3.4.1. Adoption of Hybrid Imaging Systems

3.4.2. Shift Towards Value-Based Imaging

3.4.3. Growth in Teleradiology Services

3.5. Government Regulations

3.5.1. Medical Device Approval Processes

3.5.2. Radiation Safety Standards

3.5.3. Reimbursement Policies

3.5.4. Import and Export Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter's Five Forces Analysis

3.9. Competitive Landscape

4. Asia Pacific Diagnostic Imaging Market Segmentation

4.1. By Modality (In Value %)

4.1.1. X-ray Imaging

4.1.2. Computed Tomography (CT)

4.1.3. Magnetic Resonance Imaging (MRI)

4.1.4. Ultrasound

4.1.5. Nuclear Imaging

4.1.6. Mammography

4.2. By Application (In Value %)

4.2.1. Cardiology

4.2.2. Oncology

4.2.3. Neurology

4.2.4. Orthopedics

4.2.5. Gastroenterology

4.2.6. Obstetrics/Gynecology

4.2.7. Others

4.3. By End User (In Value %)

4.3.1. Hospitals

4.3.2. Diagnostic Imaging Centers

4.3.3. Ambulatory Surgical Centers

4.3.4. Research Institutes

4.4. By Technology (In Value %)

4.4.1. Digital Imaging

4.4.2. Analog Imaging

4.4.3. 3D/4D Imaging

4.4.4. Portable Imaging

4.5. By Country (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. South Korea

4.5.5. Australia

4.5.6. Rest of Asia Pacific

5. Asia Pacific Diagnostic Imaging Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. GE Healthcare

5.1.2. Siemens Healthineers

5.1.3. Philips Healthcare

5.1.4. Canon Medical Systems Corporation

5.1.5. Fujifilm Holdings Corporation

5.1.6. Hitachi Medical Corporation

5.1.7. Shimadzu Corporation

5.1.8. Hologic, Inc.

5.1.9. Carestream Health

5.1.10. Samsung Medison

5.1.11. Agfa-Gevaert N.V.

5.1.12. Esaote S.p.A.

5.1.13. Mindray Medical International Limited

5.1.14. Konica Minolta, Inc.

5.1.15. Neusoft Medical Systems Co., Ltd.

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Presence, R&D Investment, Recent Developments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6. Asia Pacific Diagnostic Imaging Market Regulatory Framework

6.1. Medical Device Regulations

6.2. Compliance Requirements

6.3. Certification Processes

7. Asia Pacific Diagnostic Imaging Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Diagnostic Imaging Future Market Segmentation

8.1. By Modality (In Value %)

8.2. By Application (In Value %)

8.3. By End User (In Value %)

8.4. By Technology (In Value %)

8.5. By Country (In Value %)

9. Asia Pacific Diagnostic Imaging Market Analysts’ Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This stage involved constructing a comprehensive ecosystem map of the Asia Pacific diagnostic imaging market. Extensive desk research was conducted to identify variables influencing market dynamics, including key stakeholders and technologies.

Step 2: Market Analysis and Construction

In this step, historical data on market penetration and revenue generation were compiled and analyzed. This process included assessing the ratio of imaging modalities to end-users across different healthcare settings.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts were consulted through computer-assisted interviews to validate hypotheses. Their insights refined the data on operational and financial aspects, contributing to a robust analysis.

Step 4: Research Synthesis and Final Output

Data synthesis included inputs from diagnostic imaging manufacturers to verify insights. This comprehensive analysis was finalized to provide accurate and actionable intelligence for the Asia Pacific diagnostic imaging market.

Frequently Asked Questions

01 How big is Asia-Pacific Diagnostic Imaging Market?

The Asia Pacific Diagnostic Imaging Market was valued at USD 8.6 billion in 2023. This growth is primarily driven by the increasing prevalence of chronic diseases, advancements in imaging technologies, and the rising demand for early and accurate diagnosis. Additionally, the growing aging population, particularly in countries like Japan and China, contributes significantly to the market expansion.

02 What are the growth drivers of the Asia-Pacific Diagnostic Imaging Market?

Growth drivers in the Asia-Pacific diagnostic imaging market include the increasing prevalence of chronic diseases like cancer and cardiovascular diseases, substantial investments in healthcare infrastructure, important government healthcare expenditure, and the rising number of medical tourists seeking advanced diagnostic services.

03 What are challenges faced by Asia-Pacific Diagnostic Imaging Market?

Challenges in the Asia-Pacific diagnostic imaging market include the high cost of advanced imaging equipment, a shortage of trained radiologists and imaging technicians, complex regulatory requirements, and limited reimbursement policies for advanced imaging procedures in certain regions.

04 Who are the major players in the Asia-Pacific Diagnostic Imaging Market?

Major players in the Asia-Pacific diagnostic imaging market include GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings Corporation. These companies lead the market through continuous innovation, strategic partnerships, and extensive distribution networks.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.