Asia Pacific E-Health Market Outlook to 2030

Region:Asia

Author(s):Meenakshi

Product Code:KROD4303

November 2024

82

About the Report

Asia Pacific E-Health Market Overview

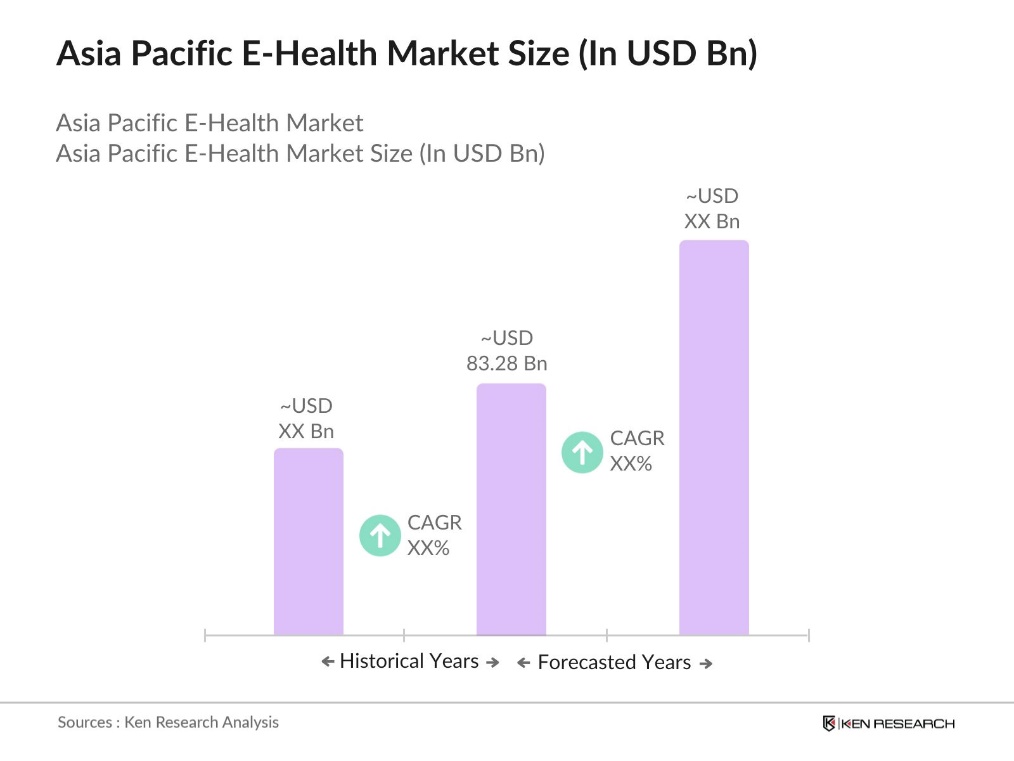

- The Asia Pacific E-Health market is valued at USD 83.28 billion, driven by an increasing focus on digital health services and rising healthcare expenditures across the region. With the growing integration of advanced technologies such as AI, IoT, and cloud computing, healthcare delivery models have shifted towards more accessible and efficient solutions.

- Countries such as China, India, and Japan are dominating the Asia Pacific E-Health market due to their advanced healthcare infrastructure and large patient populations. China leads the market owing to its massive investment in telemedicine and AI healthcare initiatives, while Japan benefits from its aging population and high demand for advanced healthcare solutions.

- In 2024, Australia is indeed advancing its healthcare infrastructure through partnerships with private technology companies, focusing on digitization efforts that are expected to impact a significant number of patients. The Australian Digital Health Agency has been actively involved in transforming the national digital health infrastructure, emphasizing the need for modernized systems that can connect various healthcare settings and improve patient outcomes

Asia Pacific E-Health Market Segmentation

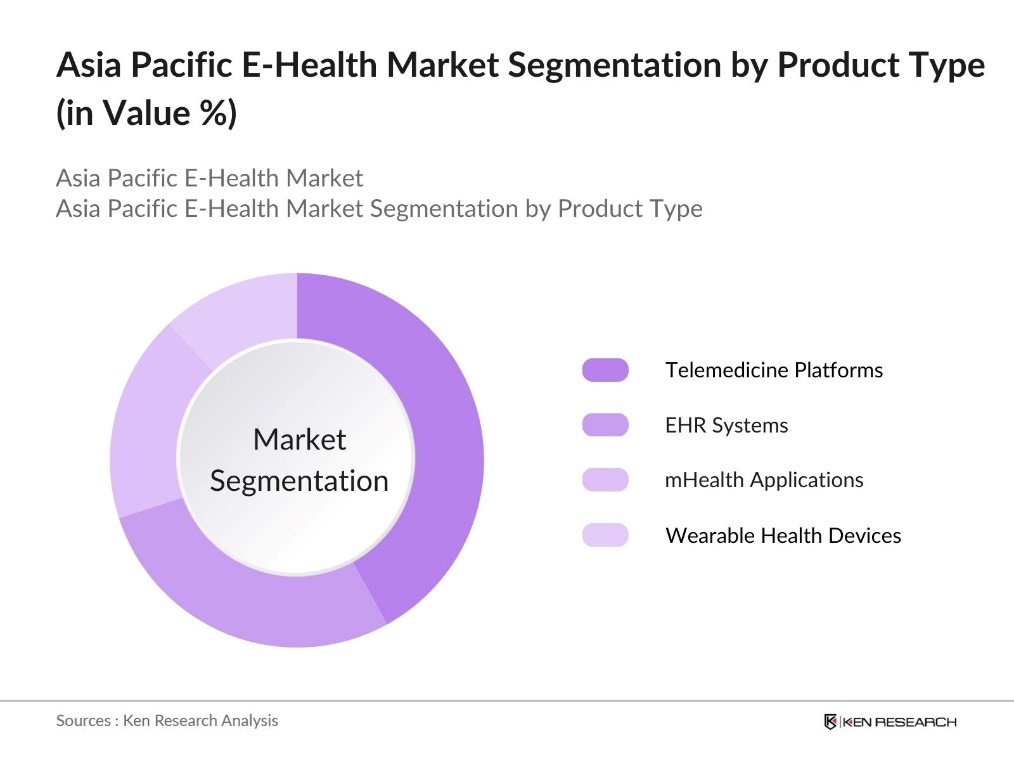

By Product Type: The Asia Pacific E-Health market is segmented by product type into telemedicine platforms, electronic health records (EHR) systems, mHealth applications, and wearable health devices. Among these, telemedicine platforms hold the largest market share due to the increasing demand for remote healthcare services. Telemedicine has gained prominence as it enables access to healthcare professionals from any location, significantly reducing the need for physical hospital visits. This demand is particularly strong in rural areas, where healthcare facilities are limited, and telemedicine is viewed as a viable alternative to traditional care.

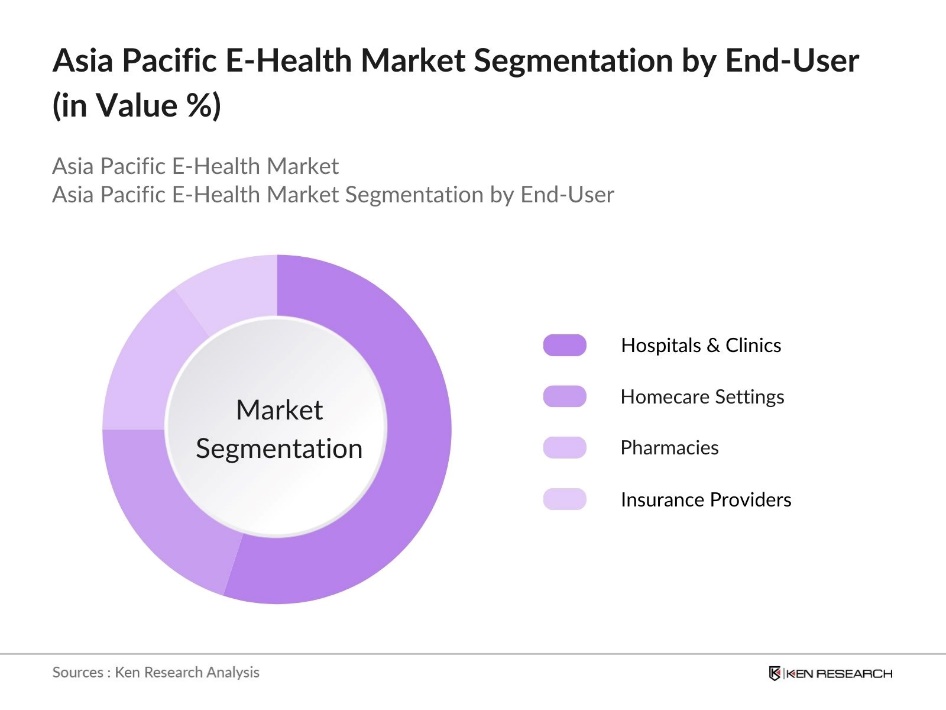

By End-User: The market is further segmented by end-user into hospitals & clinics, homecare settings, pharmacies, and insurance providers. Hospitals and clinics hold a dominant market share in this segment due to their adoption of comprehensive digital health systems for patient management and hospital workflow optimization. With the growing focus on digitization, hospitals are leveraging e-health solutions to improve the efficiency of clinical operations and patient outcomes. Moreover, the adoption of EHR systems in hospitals facilitates seamless information exchange across departments, making it a critical component in the e-health ecosystem.

Asia Pacific E-Health Market Competitive Landscape

The Asia Pacific E-Health market is dominated by major technology and healthcare companies, along with regional players specializing in e-health solutions. The competitive landscape highlights the consolidation of key players through strategic collaborations and mergers, leading to a highly competitive environment. Companies such as GE Healthcare, Philips, and Tencent Healthcare are leveraging their strong R&D capabilities and expansive digital portfolios to maintain a competitive edge. The market is also witnessing the emergence of new players focusing on AI-based healthcare solutions and telemedicine services.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD bn) |

No. of Employees |

Key Product |

R&D Investment |

Geographical Presence |

Market Share |

|

GE Healthcare |

1892 |

Chicago, USA |

||||||

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

||||||

|

Tencent Healthcare |

1998 |

Shenzhen, China |

||||||

|

IBM Watson Health |

1911 |

Armonk, USA |

||||||

|

Teladoc Health Inc. |

2002 |

Purchase, USA |

Asia Pacific E-Health Industry Analysis

Growth Drivers

- Digital Health Infrastructure Expansion (Cloud Integration, Data Security): The Asia Pacific region has experienced rapid growth in its digital health infrastructure, driven by cloud integration and an increasing focus on data security. Governments in countries like India and Australia have invested heavily in cloud infrastructure to support e-health platforms. In 2024, India committed $2.3 billion to the National Digital Health Mission, aiming to provide universal digital health IDs, while Australia has allocated $500 million toward expanding its My Health Record system. These initiatives focus on integrating Electronic Health Records (EHR) with cloud solutions, ensuring better healthcare data management.

- Increasing Internet Penetration and Smartphone Adoption: Internet penetration in the Asia Pacific region has been a key driver for the expansion of e-health services. By 2025, India has surpassed 900 million internet users. This connectivity enables wider access to telemedicine, remote patient monitoring, and mobile health applications, significantly driving the e-health market.

- Demand for Telemedicine and Remote Patient Monitoring: The growth of telemedicine in the Asia Pacific region is driven by increasing demand for remote patient monitoring, particularly in underserved rural areas. Telemedicine enables patients to access medical consultations and ongoing health monitoring without needing to travel, easing the burden on urban healthcare systems. This expansion improves healthcare accessibility and efficiency, making it a vital component of modern healthcare delivery in the region.

Market Challenges

- Data Privacy Concerns (Compliance with GDPR, Local Regulations): Data privacy is a major challenge in the Asia Pacific e-health market, as compliance with local regulations can hinder expansion. Different countries in the region have introduced stringent data protection laws to safeguard patient information, but the lack of uniformity across borders makes it difficult to implement these on a regional scale. Ensuring compliance with these varying regulations is essential to prevent breaches and maintain consumer trust.

- Interoperability Issues (EHR Integration): Interoperability between healthcare systems presents a significant barrier to the growth of e-health in the Asia Pacific. Fragmented Electronic Health Record (EHR) systems across different countries limit the exchange of patient data, both internally and across borders. The lack of a unified system hampers seamless healthcare delivery and reduces the effectiveness of data-driven healthcare solutions, posing a challenge to broader market expansion

Asia Pacific E-Health Market Future Outlook

Over the next five years, the Asia Pacific E-Health market is expected to grow significantly due to several factors. These include advancements in healthcare technologies such as AI, 5G-enabled telemedicine, and the increasing integration of cloud-based platforms for patient management. Government initiatives aimed at improving healthcare accessibility, such as Chinas Healthy China 2030 plan and India's Digital Health Mission, will continue to drive market growth. In addition, the rising demand for personalized medicine and predictive healthcare analytics is anticipated to accelerate the adoption of e-health solutions across the region.

Market Opportunities

Growth of AI in Healthcare (AI-driven Diagnostics, Personalized Medicine): AI is playing a transformative role in healthcare across the Asia Pacific region, with its application in diagnostics and personalized medicine seeing substantial growth. AI-driven technologies are improving diagnostic accuracy and enabling predictive analytics, which support personalized treatment plans tailored to individual patients. This shift toward AI-enabled healthcare presents significant opportunities for enhanced medical outcomes, especially in areas like early disease detection and customized therapies.

Expansion of 5G Networks Enabling Real-time Remote Healthcare: The rollout of 5G networks in the Asia Pacific is revolutionizing real-time healthcare services. With faster connectivity and lower latency, 5G enables more advanced telemedicine capabilities, including real-time remote surgeries and continuous patient monitoring. This advancement is particularly beneficial for expanding healthcare access in remote and underserved areas, allowing for timely and effective medical interventions.

Scope of the Report

|

By Product Type |

Telemedicine Platforms EHR Systems mHealth Apps Wearables |

|

By Service Type |

Clinical Services Administrative Services Remote Monitoring |

|

By Delivery Mode |

On-Premise Cloud-based |

|

By End User |

Hospitals Homecare Pharmacies Insurance Providers |

|

By Region |

China Japan India Australia ASEAN |

Products

Key Target Audience

Health Tech Startups

Pharmaceutical Companies

Telemedicine Industry

Medical Device Manufacturers

Government and Regulatory Bodies (e.g., Ministry of Health, Medical Regulatory Authorities)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

GE Healthcare

Philips Healthcare

Tencent Healthcare

IBM Watson Health

Teladoc Health Inc.

Cerner Corporation

Medtronic Plc

Samsung Healthcare

Fujitsu Limited

Alibaba Health Information Technology Limited

Table of Contents

1. Asia Pacific E-Health Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific E-Health Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific E-Health Market Analysis

3.1. Growth Drivers

3.1.1. Digital Health Infrastructure Expansion (Cloud Integration, Data Security)

3.1.2. Increasing Internet Penetration and Smartphone Adoption

3.1.3. Government Initiatives Promoting Digital Healthcare (National eHealth Policies)

3.1.4. Demand for Telemedicine and Remote Patient Monitoring

3.2. Market Challenges

3.2.1. Data Privacy Concerns (Compliance with GDPR, Local Regulations)

3.2.2. Interoperability Issues (EHR Integration)

3.2.3. Limited Digital Literacy in Rural Areas

3.2.4. Cybersecurity Threats

3.3. Opportunities

3.3.1. Growth of AI in Healthcare (AI-driven Diagnostics, Personalized Medicine)

3.3.2. Expansion of 5G Networks Enabling Real-time Remote Healthcare

3.3.3. Investment in Health Tech Startups

3.3.4. Partnerships Between Hospitals and Tech Giants

3.4. Trends

3.4.1. Rise in Mobile Health Apps Adoption

3.4.2. Growing Focus on Patient-Centric Platforms

3.4.3. Increasing Use of Wearable Health Devices

3.4.4. Cloud-based Healthcare Solutions

3.5. Government Regulations

3.5.1. National Telemedicine Guidelines

3.5.2. Data Localization Laws

3.5.3. Regulatory Framework for AI in Healthcare

3.5.4. Public-Private Partnerships for Healthcare Digitization

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Healthcare Providers, Tech Vendors, Patients)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Asia Pacific E-Health Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Telemedicine Platforms

4.1.2. Electronic Health Records (EHR) Systems

4.1.3. Mobile Health (mHealth) Apps

4.1.4. Wearable Health Devices

4.2. By Service Type (In Value %)

4.2.1. Clinical Services

4.2.2. Administrative Services

4.2.3. Remote Monitoring Services

4.2.4. Wellness Services

4.3. By Delivery Mode (In Value %)

4.3.1. On-Premise

4.3.2. Cloud-based

4.4. By End User (In Value %)

4.4.1. Hospitals & Clinics

4.4.2. Homecare Settings

4.4.3. Pharmacies

4.4.4. Insurance Providers

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. Australia

4.5.5. ASEAN

5. Asia Pacific E-Health Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Allscripts Healthcare Solutions, Inc.

5.1.2. Cerner Corporation

5.1.3. Epic Systems Corporation

5.1.4. GE Healthcare

5.1.5. IBM Watson Health

5.1.6. Medtronic Plc

5.1.7. Philips Healthcare

5.1.8. Siemens Healthineers AG

5.1.9. Cisco Systems, Inc.

5.1.10. Teladoc Health, Inc.

5.1.11. McKesson Corporation

5.1.12. Samsung Healthcare

5.1.13. Fujitsu Limited

5.1.14. Alibaba Health Information Technology Limited

5.1.15. Tencent Healthcare

5.2. Cross Comparison Parameters

5.2.1. Revenue

5.2.2. Market Share

5.2.3. Number of Employees

5.2.4. Research & Development Investment

5.2.5. Partnerships & Collaborations

5.2.6. Technology Adoption (AI, Cloud, IoT)

5.2.7. Geographic Presence

5.2.8. Customer Base

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific E-Health Market Regulatory Framework

6.1. Healthcare Data Privacy Laws

6.2. Telemedicine Guidelines Compliance

6.3. AI in Healthcare Certification Processes

6.4. Digital Health Standards Compliance

7. Asia Pacific E-Health Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific E-Health Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Service Type (In Value %)

8.3. By Delivery Mode (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific E-Health Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 2: Market Analysis and Construction

In this step, we analyze historical data and examine market penetration in key regions. Additionally, we assess the impact of new healthcare technologies and government policies on market dynamics. This phase involves a detailed study of market structure, revenue growth, and competitive positioning to provide an accurate market forecast.

Step 3: Hypothesis Validation and Expert Consultation

We develop market hypotheses based on collected data and validate these through in-depth interviews with industry experts. These consultations, conducted through computer-assisted telephone interviews (CATI), provide valuable insights from healthcare professionals and technology providers, ensuring accuracy in market projections.

Step 4: Research Synthesis and Final Output

In the final phase, we synthesize the collected data, integrating both top-down and bottom-up approaches to ensure a comprehensive analysis of the Asia Pacific E-Health market. The final output is validated through consultations with healthcare professionals and technology providers to ensure the accuracy and reliability of the report.

Frequently Asked Questions

01. How big is the Asia Pacific E-Health Market?

The Asia Pacific E-Health market is valued at USD 83.28 billion, driven by rising digital health services, increasing healthcare expenditures, and growing demand for telemedicine and EHR systems.

02. What are the challenges in the Asia Pacific E-Health Market?

Key challenges in Asia Pacific E-Health market include data privacy concerns, limited digital literacy in rural areas, and interoperability issues with existing healthcare systems.

03. Who are the major players in the Asia Pacific E-Health Market?

Major players in Asia Pacific E-Health market include GE Healthcare, Philips Healthcare, Tencent Healthcare, IBM Watson Health, and Teladoc Health Inc. These companies are prominent due to their strong R&D capabilities and broad geographic presence.

04. What are the growth drivers of the Asia Pacific E-Health Market?

The Asia Pacific E-Health market is driven by the growing adoption of telemedicine, mHealth apps, and wearable health devices. Government initiatives promoting digital healthcare and increasing investments in healthcare infrastructure are also significant drivers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.