Asia Pacific Plastic Containers Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD7637

November 2024

84

About the Report

Asia Pacific Plastic Containers Market Overview

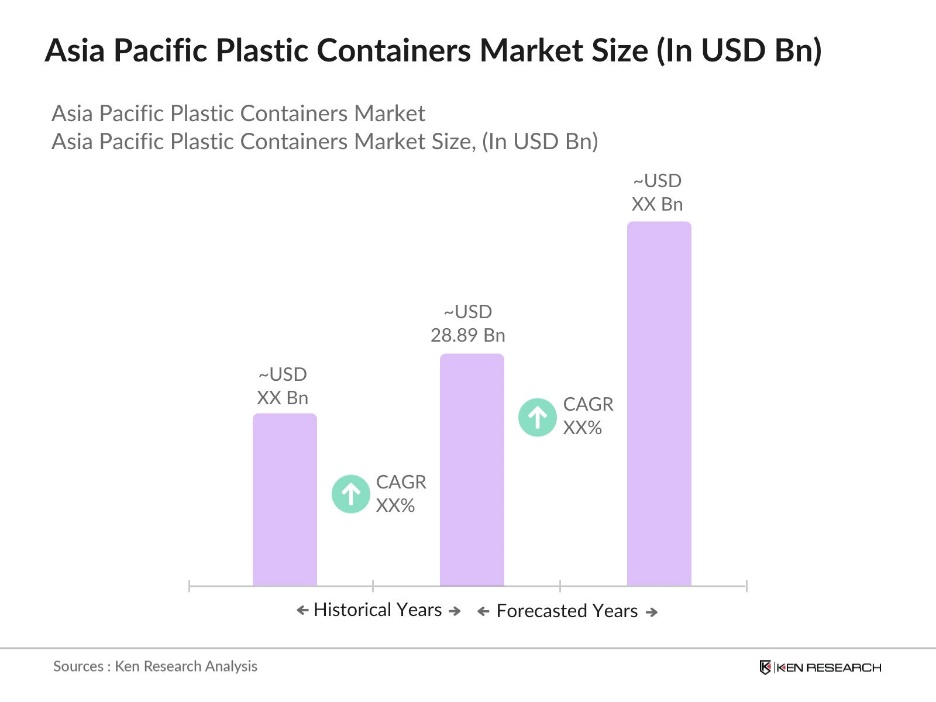

- The Asia Pacific Plastic Containers Market is valued at USD 28.89 billion, driven by the increasing demand for sustainable and lightweight packaging solutions across various industries such as food and beverages, pharmaceuticals, and personal care. The market's growth is bolstered by the region's rapid urbanization, expanding e-commerce industry, and the shift toward ready-to-consume packaged goods. Significant growth is also supported by technological advancements in plastic manufacturing, including biodegradable and recycled plastic solutions, helping companies meet environmental standards.

- Countries like China and India dominate the Asia Pacific plastic containers market due to their large populations, rapidly growing industrial sectors, and established manufacturing capabilities. China leads as the largest producer of plastic containers, supported by its robust manufacturing infrastructure and cost-effective production processes. India follows closely, with its growing middle-class population and rising demand for consumer goods, which has fueled the expansion of the packaging industry. Both countries benefit from lower production costs and favorable government regulations.

- Recycling and waste management standards have become more stringent across Asia Pacific. China's "Zero Waste City" initiative began with pilot programs in 11 cities and 5 special areas. The objective is to scale this initiative to 100 cities during the 14th Five-Year Plan period (2021-2025). Other countries, such as Singapore and Thailand, have introduced regulations mandating that companies recycle a significant portion of their plastic packaging. These regulations are driving investments in recycling technologies and encouraging companies to adopt sustainable practices.

Asia Pacific Plastic Containers Market Segmentation

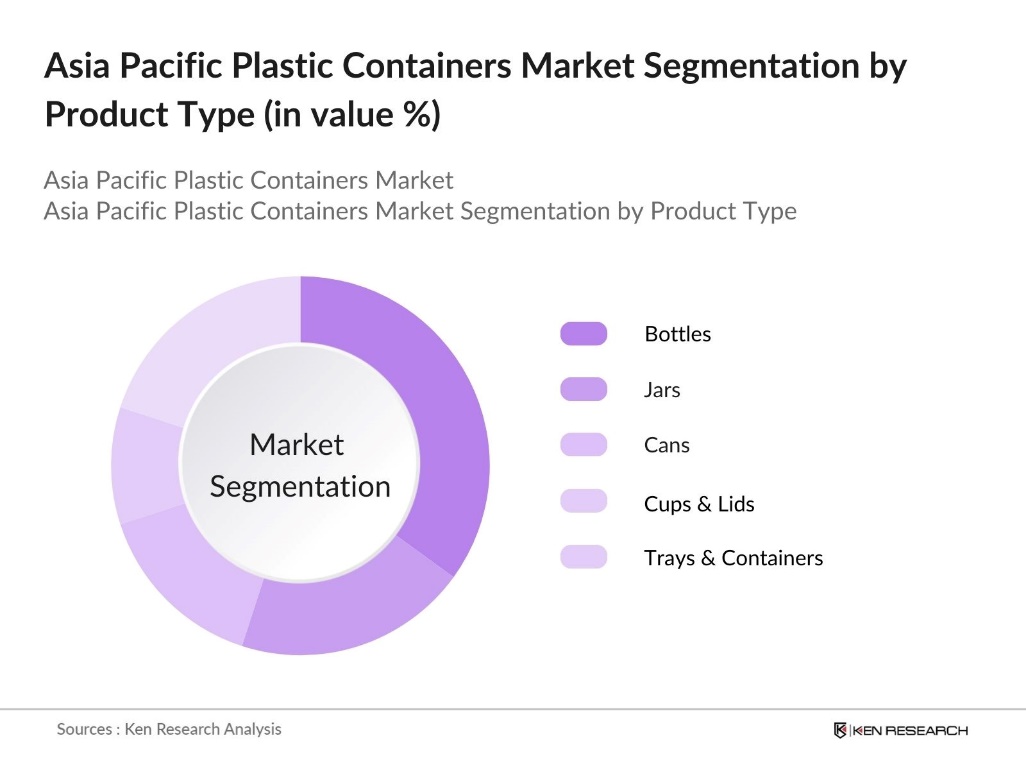

By Product Type: The Asia Pacific plastic containers market is segmented by product type into bottles, jars, cans, cups & lids, and trays & containers. Among these, bottles hold a dominant market share due to their extensive use in the beverage and personal care industries. The growth of the bottled water industry, combined with the rise in demand for convenient and portable packaging, has made bottles the preferred product type in the region. Additionally, bottles are widely used in the pharmaceutical industry, further solidifying their position in the market.

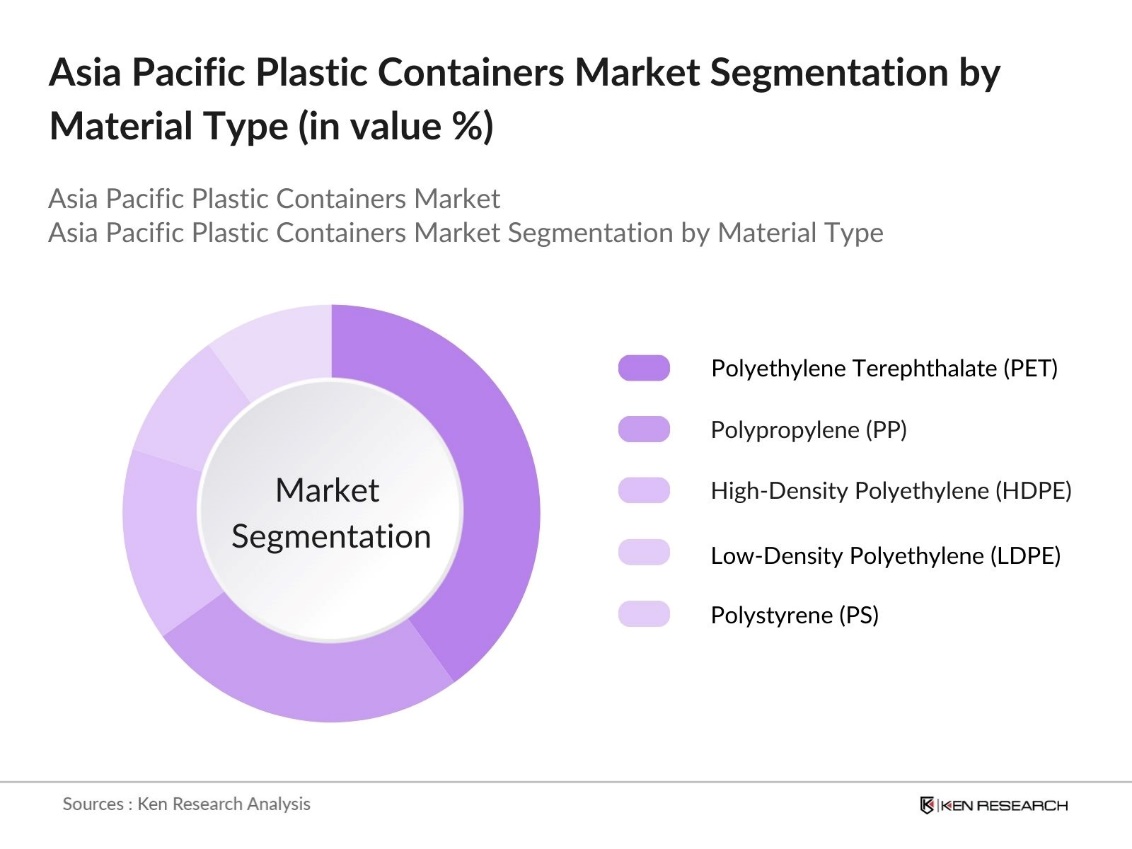

By Material Type: The Asia Pacific plastic containers market is also segmented by material type, including polyethylene terephthalate (PET), polypropylene (PP), high-density polyethylene (HDPE), low-density polyethylene (LDPE), and polystyrene (PS). Polyethylene terephthalate (PET) dominates the market due to its extensive application in food and beverage packaging. PET is known for its durability, recyclability, and barrier properties, making it a preferred choice for packaging soft drinks, water, and various other beverages. The widespread adoption of PET across multiple industries solidifies its dominance in the market.

Asia Pacific Plastic Containers Market Competitive Landscape

The market is dominated by a mix of global and regional players. These companies are highly competitive in terms of innovation, product quality, and sustainability initiatives. The markets competitive landscape is characterized by major players that hold significant shares due to their extensive production capacities, strong distribution networks, and continuous investment in R&D for eco-friendly packaging solutions. Companies like Amcor and Berry Global focus heavily on sustainable packaging innovations, while Huhtamaki leverages its extensive manufacturing footprint across the region.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Annual Revenue (USD Bn) |

Key Product Lines |

Sustainability Initiatives |

Global Footprint |

R&D Investments |

Recent Strategic Initiative |

|

Amcor Plc |

1860 |

Melbourne, Australia |

|||||||

|

Berry Global Group, Inc. |

1967 |

Evansville, USA |

|||||||

|

Huhtamaki Oyj |

1920 |

Espoo, Finland |

|||||||

|

ALPLA Group |

1955 |

Hard, Austria |

|||||||

|

Sealed Air Corporation |

1960 |

Charlotte, USA |

Asia Pacific Plastic Containers Industry Analysis

Growth Drivers

- Rise in Packaged Goods Demand (Food & Beverages, Pharmaceuticals, FMCG): The rise in demand for packaged goods, particularly in the food, beverages, and pharmaceuticals sectors, is a key driver of the plastic containers market in the Asia Pacific region. For instance, in India, the food and beverage industry contributes around 3% to the country's GDP. The demand for plastic packaging is directly linked to the growing consumer base, with the Asia Pacific region.

- Urbanization and Changing Lifestyles (Higher Consumption of Single-Use Plastics): Asia Pacific is experiencing rapid urbanization, with 54% of its population living in urban areas by 2024. This urban shift has led to an increase in the consumption of single-use plastics, particularly in the FMCG sector. The changing lifestyles and the growing demand for convenient, ready-to-consume products have fueled this demand. The urban population in countries like China and India increased that has driving the demand for plastic packaging.

- Expansion of E-Commerce (Increased Demand for Protective Packaging): The expansion of e-commerce has significantly increased the demand for protective plastic packaging in the Asia Pacific market. As online shopping becomes more prevalent, durable and lightweight plastic containers are essential for ensuring products are shipped securely. The rise of e-commerce giants and the growing volume of online transactions have driven the need for effective packaging solutions. This demand is further fueled by the increasing frequency of cross-border shipments, which require protective materials to ensure product safety during transit, particularly in sectors like electronics and consumer goods.

Market Challenges

- Environmental Concerns (Plastic Waste and Sustainability Issues): Plastic waste is a growing environmental challenge in the Asia Pacific region, leading to increased pressure from governments and organizations to implement stricter regulations. These efforts aim to reduce plastic waste and its negative environmental impact, posing challenges for industries that depend on plastic containers. Companies may need to adopt more sustainable practices to comply with emerging regulations.

- Government Regulations (Plastic Bans, Recycling Mandates): Governments in Asia Pacific have introduced regulations like single-use plastic bans and recycling mandates to address environmental concerns. These policies require companies to reduce plastic usage or invest in recycling technologies, creating operational challenges. Industries relying on plastic containers may face higher costs and logistical hurdles as they adapt to more sustainable practices.

Asia Pacific Plastic Containers Market Future Outlook

The Asia Pacific plastic containers market is expected to witness sustained growth, driven by the rising demand for sustainable packaging solutions, rapid urbanization, and expanding consumer goods industries. Technological advancements in material sciences, such as the development of biodegradable plastics and innovative recycling techniques, are anticipated to enhance market potential.

Market Opportunities

- Growing Adoption of Recycled Plastics: The increasing adoption of recycled plastics offers significant opportunities for the Asia Pacific plastic containers market. As sustainability becomes a priority, more companies are shifting toward using recycled materials to reduce reliance on virgin plastics. This move aligns with global sustainability trends, encouraging businesses to meet environmental goals while maintaining cost efficiency. The focus on using recycled plastics also helps reduce waste and promotes eco-friendly practices in the packaging industry.

- Technological Innovations in Manufacturing: Technological advancements in manufacturing, including the development of biodegradable plastics and advanced molding techniques, present growth opportunities for the plastic containers market. These innovations improve production efficiency, reduce waste, and create environmentally friendly packaging solutions. Companies adopting these technologies are better positioned to meet the growing demand for sustainable packaging, as consumers and businesses increasingly prioritize eco-friendly materials and manufacturing practices.

Scope of the Report

|

Product Type |

Bottles Jars Cans Cups & Lids Trays & Containers |

|

Material Type |

PET PP HDPE LDPE PS |

|

Application |

Food & Beverage Pharmaceuticals Personal Care & Cosmetics Industrial Household |

|

End User |

Consumer Packaging Industrial Packaging |

|

Region |

China India Japan Southeast Asia Australia & New Zealand |

Products

Key Target Audience

Plastic Manufacturers

Packaging Companies

Food & Beverage Manufacturers

Personal Care & Cosmetics Companies

Pharmaceutical Companies

Government and Regulatory Bodies (Environmental Protection Agencies, Packaging & Labeling Authorities)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Amcor Plc

Berry Global Group, Inc.

Huhtamaki Oyj

Graham Packaging Company

ALPLA Group

Sealed Air Corporation

Plastipak Holdings, Inc.

Coveris Holdings S.A.

Rexam Plc

Silgan Holdings Inc.

Table of Contents

1. Asia Pacific Plastic Containers Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Plastic Containers Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Plastic Containers Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Packaged Goods Demand (Food & Beverages, Pharmaceuticals, FMCG)

3.1.2. Urbanization and Changing Lifestyles (Higher Consumption of Single-Use Plastics)

3.1.3. Expansion of E-Commerce (Increased Demand for Protective Packaging)

3.1.4. Lightweight and Cost-Effective Material Preferences

3.2. Market Challenges

3.2.1. Environmental Concerns (Plastic Waste and Sustainability Issues)

3.2.2. Government Regulations (Plastic Bans, Recycling Mandates)

3.2.3. Fluctuating Raw Material Prices (Impact of Oil and Gas Prices)

3.3. Opportunities

3.3.1. Growing Adoption of Recycled Plastics (Sustainability Initiatives)

3.3.2. Technological Innovations in Manufacturing (Biodegradable Plastics, Advanced Molding)

3.3.3. Increasing Demand in Emerging Economies (Southeast Asia, India)

3.4. Trends

3.4.1. Shift Towards Eco-Friendly and Sustainable Packaging

3.4.2. Integration of Smart Packaging Technologies (Track & Trace, Freshness Indicators)

3.4.3. Customization and Aesthetic Design in Packaging Solutions

3.5. Government Regulations

3.5.1. Single-Use Plastic Bans

3.5.2. Extended Producer Responsibility (EPR) Frameworks

3.5.3. Recycling and Waste Management Standards

3.5.4. Import/Export Regulations for Plastic Containers

4. Asia Pacific Plastic Containers Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Bottles

4.1.2. Jars

4.1.3. Cans

4.1.4. Cups & Lids

4.1.5. Trays & Containers

4.2. By Material Type (In Value %)

4.2.1. Polyethylene Terephthalate (PET)

4.2.2. Polypropylene (PP)

4.2.3. High-Density Polyethylene (HDPE)

4.2.4. Low-Density Polyethylene (LDPE)

4.2.5. Polystyrene (PS)

4.3. By Application (In Value %)

4.3.1. Food & Beverage

4.3.2. Pharmaceuticals

4.3.3. Personal Care & Cosmetics

4.3.4. Industrial

4.3.5. Household

4.4. By End User (In Value %)

4.4.1. Consumer Packaging

4.4.2. Industrial Packaging

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Southeast Asia

4.5.5. Australia & New Zealand

5. Asia Pacific Plastic Containers Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Amcor Plc

5.1.2. Berry Global Group, Inc.

5.1.3. Huhtamaki Oyj

5.1.4. Graham Packaging Company

5.1.5. Sealed Air Corporation

5.1.6. Plastipak Holdings, Inc.

5.1.7. Coveris Holdings S.A.

5.1.8. Rexam Plc

5.1.9. ALPLA Group

5.1.10. Reynolds Group Holdings Limited

5.1.11. AptarGroup, Inc.

5.1.12. Silgan Holdings Inc.

5.1.13. Sabert Corporation

5.1.14. Serioplast S.p.A

5.1.15. Logoplaste Group

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Product Innovation, Global Footprint, Sustainability Initiatives, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Plastic Containers Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. Asia Pacific Plastic Containers Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Plastic Containers Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Material Type (In Value %)

8.3. By Application (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Plastic Containers Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research process begins with identifying the key variables influencing the Asia Pacific plastic containers market. This involves extensive secondary research using trusted databases and industry reports to map the entire ecosystem, covering manufacturers, suppliers, and regulatory bodies.

Step 2: Market Analysis and Construction

In this phase, historical data on the Asia Pacific plastic containers market is compiled and analyzed to assess key trends, technological advancements, and market penetration across different regions. The data is scrutinized to ensure accuracy in revenue estimates and market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Once hypotheses regarding market growth, demand trends, and consumer preferences are developed, consultations with industry experts are conducted to validate these assumptions. Interviews with key stakeholders provide insights into the market's operational and financial aspects.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing all research findings into a cohesive report. The data is corroborated through a bottom-up approach, ensuring that the report presents a comprehensive, accurate, and validated analysis of the Asia Pacific plastic containers market.

Frequently Asked Questions

01. How big is the Asia Pacific plastic containers market?

The Asia Pacific Plastic Containers Market is valued at USD 28.89 billion, driven by the growing demand for sustainable packaging solutions in sectors such as food and beverages, personal care, and pharmaceuticals.

02. What are the challenges in the Asia Pacific plastic containers market?

Challenges in the Asia Pacific plastic containers market include stringent environmental regulations, fluctuating raw material prices, and increasing demand for eco-friendly alternatives to traditional plastic containers.

03. Who are the major players in the Asia Pacific plastic containers market?

Major players in the Asia Pacific plastic containers market include Amcor Plc, Berry Global Group, Huhtamaki Oyj, ALPLA Group, and Sealed Air Corporation. These companies lead the market due to their robust production capabilities and commitment to sustainable practices.

04. What are the growth drivers of the Asia Pacific plastic containers market?

The Asia Pacific plastic containers market is driven by factors such as the rising consumption of packaged goods, increasing urbanization, and the expanding e-commerce industry. Additionally, the shift towards recyclable and biodegradable plastics is boosting demand for plastic containers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.