Europe Data Center Market Outlook to 2030

Region:Europe

Author(s):Shreya Garg

Product Code:KROD2114

November 2024

94

About the Report

Europe Data Center Market Overview

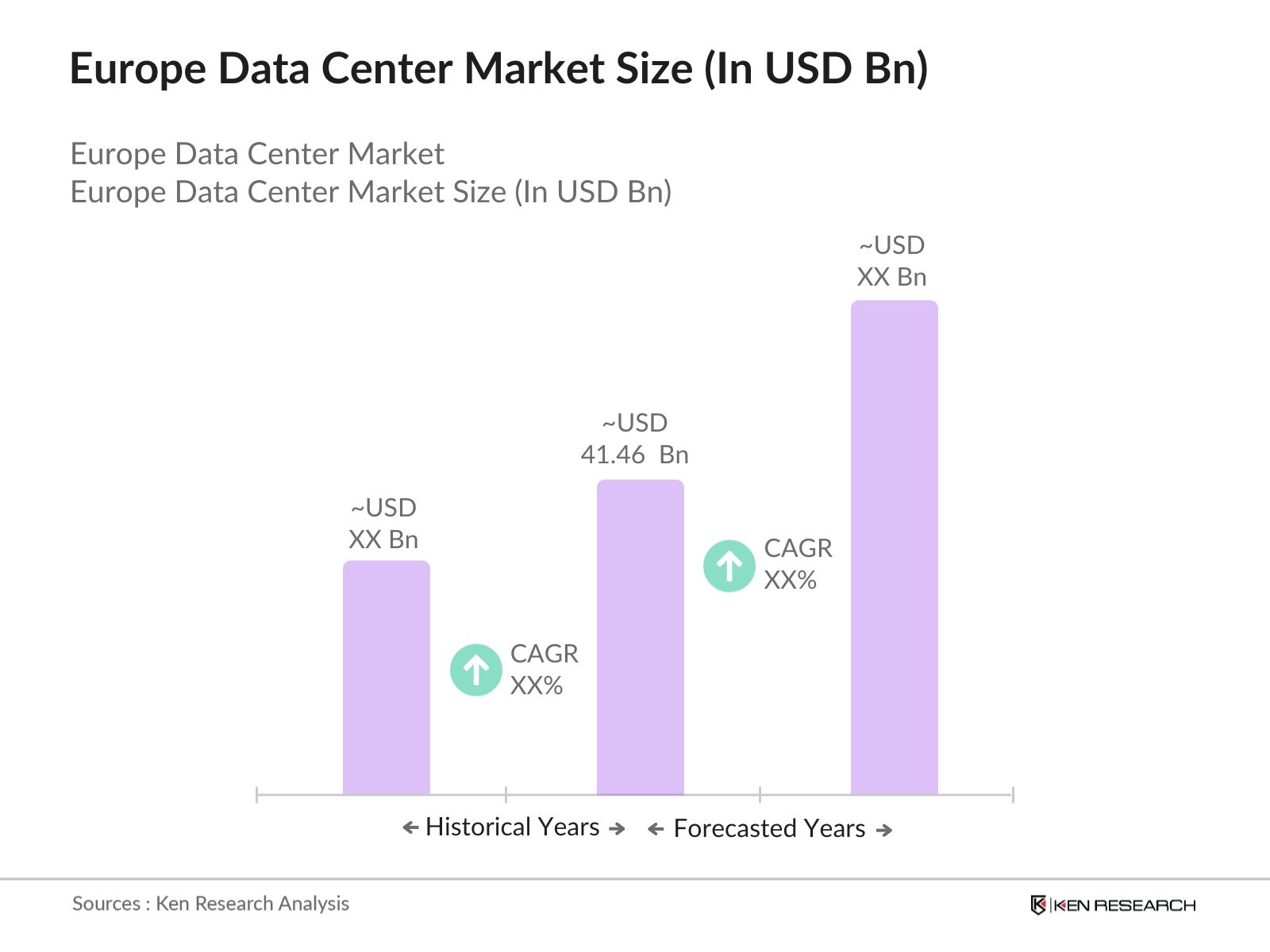

The Europe Data Center market was valued at USD 41.46 billion based on the historic data of past five years. The market has been primarily driven by the gush in demand for cloud storage, rising investments in IT infrastructure, and the enforcement of stringent data protection regulations like GDPR. These factors have made data center capacity a crucial element of modern economies. Additionally, edge computing has accelerated market growth as businesses demand faster processing power closer to their operational bases.

Major players in the Europe Data Center market include Equinix, Interxion (now a part of Digital Realty), NTT Communications, Google, and Amazon Web Services (AWS). These companies are at the forefront of market expansion through their investments in new facilities and data center upgrades to enhance their capabilities.

In September 2023, Equinix announced the opening of a new data center in Frankfurt, Germany. The FR8 facility, located in the west of the city, has an initial phase of 4,800 sq m (51,600 sq ft) of colocation space available.Equinix invested USD 103 million in the facility, which is powered by 100% renewable energy. This expansion highlights Equinix's commitment to supporting the growing demand for digital infrastructure connectivity in Europe.

Germany, particularly Frankfurt, is the dominant hub for data centers in Europe in 2023. The citys strategic location, robust IT infrastructure, and established financial industry have made it a prime location for data center expansions. In 2023, Frankfurt added over 500 MW of new data center capacity, reinforcing its leadership in the region.

Europe Data Center Market Segmentation

The Europe Data Center market is segmented into various sectors such as solution type, end user and region etc.

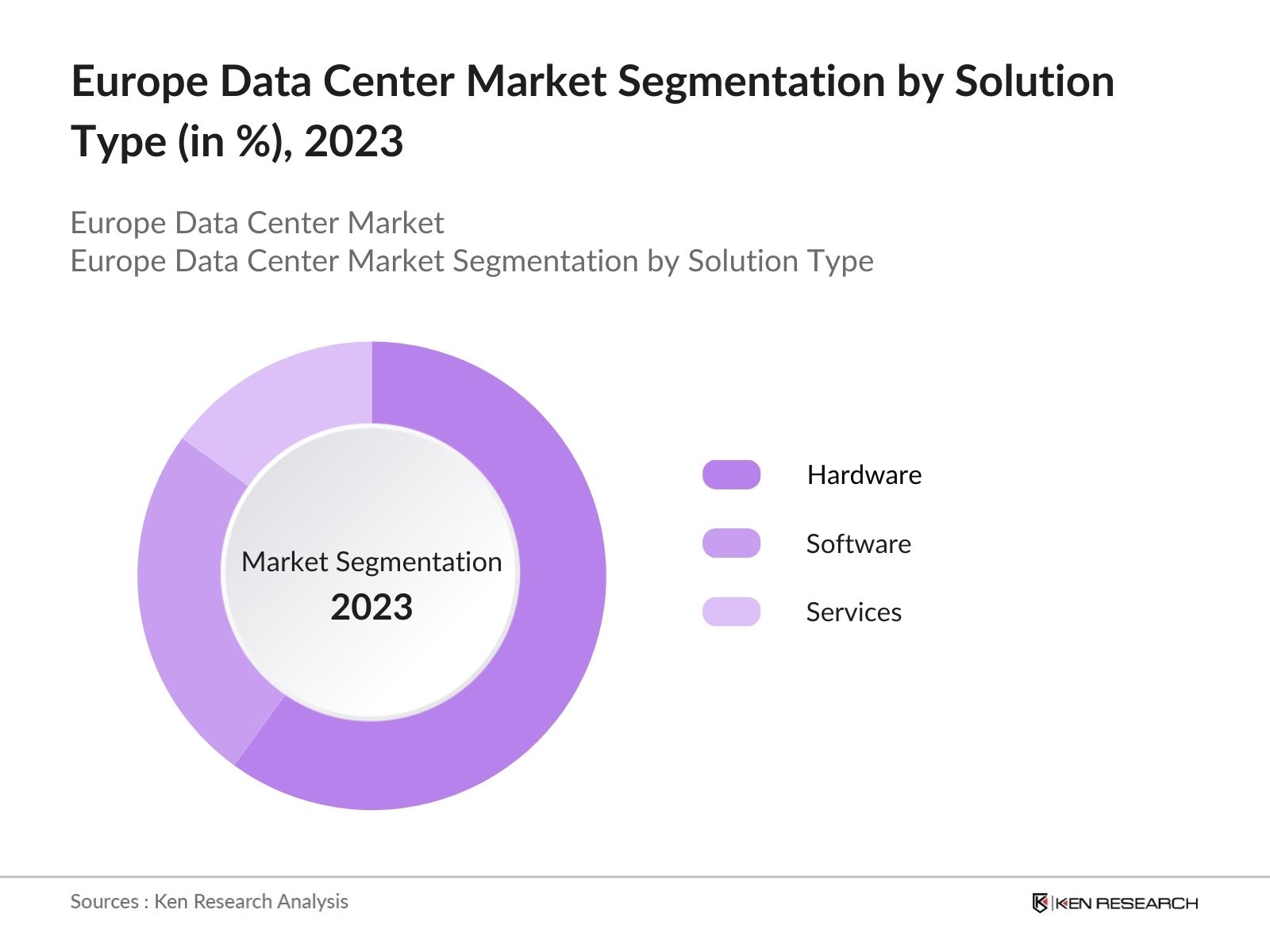

By Solution Type: The market is segmented by solution type into hardware, software, and services. The hardware segment dominated the market share, driven by the need for high-performance servers, storage systems, and networking equipment. With the rise in edge computing and cloud migration, hardware investments have become crucial to expanding data center capacity.

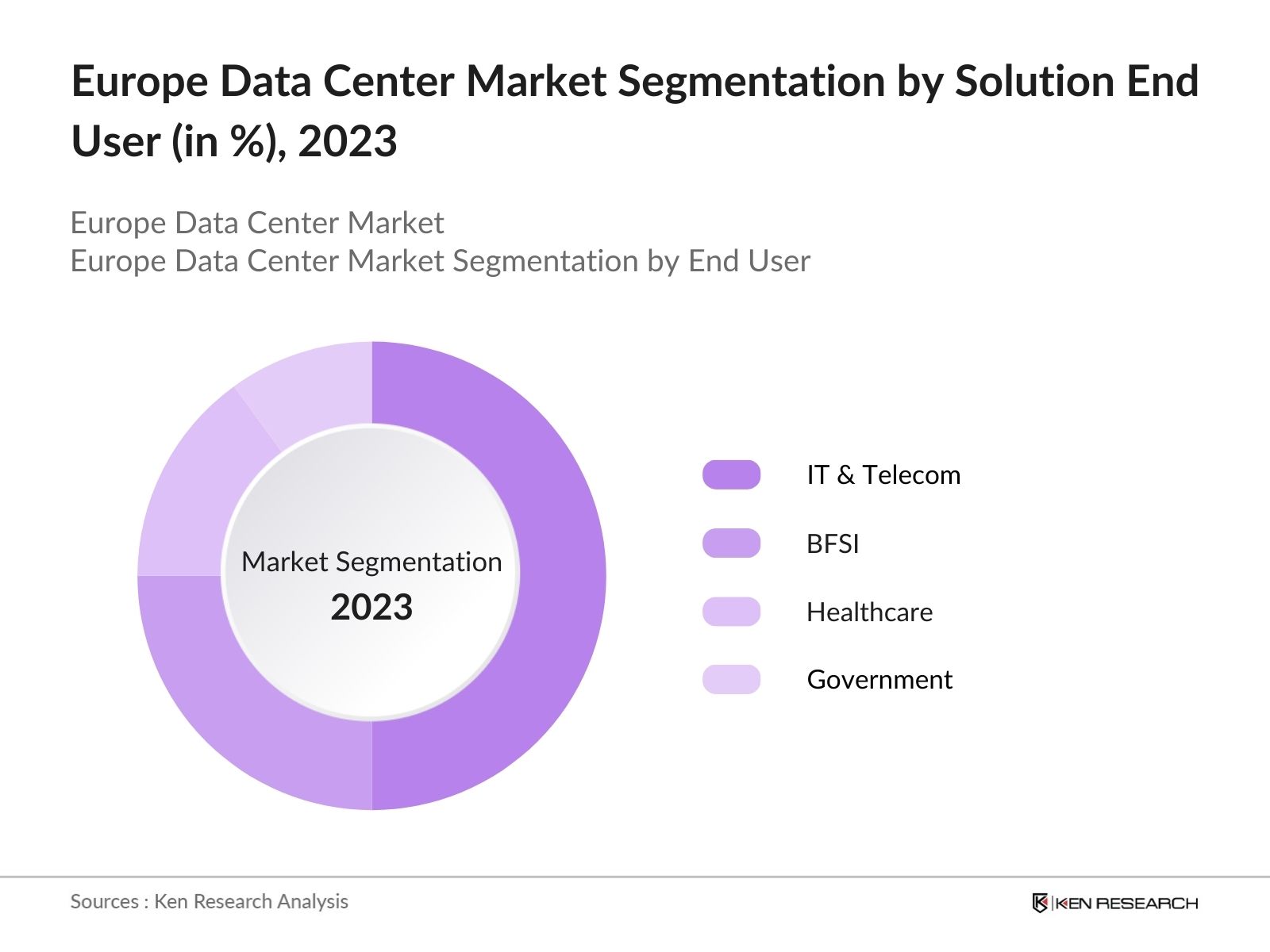

By End-User: The market is segmented by end-user into IT & Telecom, BFSI, Healthcare, and Government. The IT & Telecom sector held the largest share. The dominance of the IT & Telecom sector is primarily due to the rapid growth in cloud computing and the increasing rollout of 5G networks across Europe. These sectors are investing heavily in data centers to support the increasing demand for data storage and high-speed connectivity.

By Region: The market is segmented by region into Germany, France, United Kingdom, Sweden, Italy, and Rest of Europe. Germanys data center dominance stems from its strategic position in the European Union, its excellent connectivity infrastructure. Frankfurt, in particular, has emerged as a key location due to its role as Europes financial hub and its robust digital infrastructure.

Europe Data Center Market Competitive Landscape

|

Company Name |

Year of Establishment |

Headquarters |

|---|---|---|

|

Equinix |

1998 |

Redwood City, USA |

|

Interxion |

1998 |

Amsterdam, Netherlands |

|

NTT Communications |

1999 |

Tokyo, Japan |

|

|

1998 |

Mountain View, USA |

|

Amazon Web Services (AWS) |

2006 |

Seattle, USA |

- Interxions New Data Center in Paris: Interxion has opened a new facility, PAR12, located less than 30 kilometers east of Paris in Ferrires-en-Brie. This facility is designed to provide up to 12 megawatts of IT load capacity and includes eight data halls with over 690 square meters of colocation space. This marks Interxion's 12th data center in the Paris region, enhancing its ability to serve cloud service providers and enterprises with disaster recovery solutions and low-latency network access along the A4 motorway.

- Huaweis Expansion in Sweden: Huaweis 2023 investment of USD 400 million in a new data center facility in Stockholm focuses on serving the Nordic regions growing demand for AI and big data applications. By 2024, the facility is expected to add 50 MW of capacity, making it one of the largest in Sweden. This expansion supports Huaweis strategy to strengthen its presence in Europes data center market amid increasing competition.

Europe Data Center Industry Analysis

Growth Drivers

- Increased Cloud Adoption: The demand for cloud services in Europe surged in 2023, with cloud infrastructure-related revenues exceeding USD 25 billion across the region. Cloud providers such as AWS and Microsoft Azure have announced new data center facilities across Europe, increasing their investment in IT infrastructure. The European Commissions Digital Europe program in 2024 is also allocating EUR 7.5 billion for digital transformation projects, further fueling demand for cloud storage and computing power.

- Artificial Intelligence (AI) and Machine Learning (ML) Integration: AI and ML applications require enormous data processing power, which is boosting demand for high-performance data centers. Data centers are becoming essential to support these computational needs, prompting hyperscale data center investments. Nvidias establishment of an AI-focused data center in the Netherlands in 2023 was a strategic move to meet this rising demand.

- Energy-Efficient Data Center Solutions: The average electricity cost for data centers in Northern Europe reached USD 150 per MWh. To counter rising operational costs, companies are increasingly adopting renewable energy sources and efficient cooling technologies. By 2024, the European Green Deal will further mandate sustainable data center operations, leading to investments in solar and wind-powered facilities to reduce carbon emissions.

Challenges

- Energy Costs and Supply Constraints: The ongoing geopolitical situation in Eastern Europe has led to disruptions in energy supplies, increasing electricity costs across regions like Germany and France. These rising costs are a significant challenge for data center operators, especially those running high-performance computing workloads. The European Commission's energy crisis response measures, introduced in 2024, aim to stabilize prices but continue to affect operational expenses.

- Infrastructure and Real Estate Costs: The cost of building a new facility in Frankfurt has increased, driven by real estate demand and inflation. Furthermore, obtaining permits and fulfilling regulatory requirements adds to these costs. As a result, companies are exploring less expensive locations in Eastern Europe, although this comes with challenges related to connectivity and infrastructure.

Government Initiatives

- Energy Efficiency Reporting: The EU is implementing new reporting rules that require data centers to disclose their energy and water consumption, as well as measures taken to reduce these figures. This is part of a broader regulatory package aimed at reducing energy consumption by 11.7% between 2020 and 2030, as data centers are responsible for approximately 2-3% of the EU's total energy use.

- Power Usage Effectiveness (PUE) Standards: Under the EU's Energy Efficiency Act, existing data centers must achieve a PUE of 1.5 by July 2027 and 1.3 by 2030. New data centers must aim for a PUE of 1.2 to commence operations from 2026 onwards. These standards are designed to promote energy efficiency across the industry.

Europe Data Center Market Future Outlook

The Europe Data Center market is projected to grow exponentially. The adoption of AI, 5G, and quantum computing is expected to push demand for more advanced, high-capacity data centers. Additionally, growing sustainability concerns will drive a focus on green data centers, increasing investments in energy-efficient cooling systems and renewable energy sources.

Future Trends

- Growth of Green Data Centers: Sustainability will be a major focus for data centers over the next five years. By 2026, Europe will see new green data centers built with renewable energy sources such as solar and wind. These green facilities will benefit from investments from both governments and private companies, driven by increasing regulatory pressure and consumer demand for environmentally-friendly solutions.

- AI-Powered Automation in Data Centers: AI-powered automation will become standard practice in data center operations. Companies like Google and AWS are already investing in AI-driven management tools, which are projected to save operational costs across European data centers. This trend will reduce human intervention in data center management, improving efficiency and reducing errors.

Scope of the Report

|

By Solution type |

Hardware Software services |

|

By End User |

IT & Telecom BFSI Healthcare Government |

|

By Region |

Germany France United Kingdom Sweden Italy Rest of Europe |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Data Center Operators

IT & Telecom Companies

Cloud Service Providers

Telecom Operators

IT Infrastructure Providers

Colocation Providers

National Cyber Security Centers (NCSC)

National Telecommunications and Information Administration (NTIA)

Investors and VC Firms

Banks and Financial Institutions

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Equinix

Interxion (Digital Realty)

Google

Amazon Web Services (AWS)

NTT Communications

Digital Realty

OVHcloud

Colt Data Center Services

Global Switch

Microsoft Azure

IBM Cloud

Huawei Technologies

Atos SE

Schneider Electric

CyrusOne

Table of Contents

1. Europe Data Center Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Europe Data Center Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Europe Data Center Market Analysis

3.1. Growth Drivers

3.1.1. Cloud Adoption and Digital Transformation

3.1.2. 5G Network Expansion

3.1.3. AI and Machine Learning Implementation

3.1.4. Shift Towards Energy Efficiency

3.2. Restraints

3.2.1. High Energy Costs

3.2.2. Data Sovereignty and Compliance

3.2.3. Skilled Workforce Shortage

3.2.4. Real Estate Costs

3.3. Opportunities

3.3.1. Green Data Centers

3.3.2. Edge Computing Expansion

3.3.3. Increased Adoption of Quantum Computing

3.4. Trends

3.4.1. AI-driven Automation in Data Centers

3.4.2. Adoption of Renewable Energy Sources

3.4.3. Expansion of Edge Data Centers

3.5. Government Regulation

3.5.1. European Green Deal for Data Centers

3.5.2. Frances Digital Infrastructure Investment Plan

3.5.3. Germanys Data Security Act

3.5.4. UKs Data Economy Strategy

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competition Ecosystem

4. Europe Data Center Market Segmentation, 2023

4.1. By Solution Type (in Value %)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. By End-User (in Value %)

4.2.1. IT & Telecom

4.2.2. BFSI

4.2.3. Healthcare

4.2.4. Government

4.3. By Region (in Value %)

4.3.1. Germany

4.3.2. France

4.3.3. United Kingdom

4.3.4. Sweden

4.3.5. Italy

4.3.6. Rest of Europe

5. Europe Data Center Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. Equinix

5.1.2. Interxion (Digital Realty)

5.1.3. Amazon Web Services (AWS)

5.1.4. Google

5.1.5. NTT Communications

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. Europe Data Center Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7. Europe Data Center Market Regulatory Framework

7.1. Energy Efficiency Standards

7.2. Data Protection and Compliance Requirements

7.3. Certification Processes

8. Europe Data Center Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. Europe Data Center Future Market Segmentation, 2028

9.1. By Solution Type (in Value %)

9.2. By End-User (in Value %)

9.3. By Region (in Value %)

10. Europe Data Center Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step:1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step:2 Market Building:

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Europe data center industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step:3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different data center companies to validate statistics and seek operational and financial information from company representatives.

Step:4 Research output:

Our team will approach multiple data center products companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such data center companies.

Frequently Asked Questions

1. How big is the Europe Data Center Market?

The Europe Data Center market was valued at USD 41.46 billion, driven by the increasing demand for cloud services, digital transformation, and stricter data protection regulations across the continent.

2. What are the challenges in the Europe Data Center Market?

Challenges in the Europe Data Center market include high energy costs, data sovereignty issues, and regulatory compliance. Additionally, the shortage of skilled workforce and rising real estate costs for new data center developments pose significant obstacles.

3. Who are the major players in the Europe Data Center Market?

Key players in the Europe Data Center market include Equinix, Interxion (Digital Realty), NTT Communications, Google, and Amazon Web Services (AWS). These companies dominate due to their significant investments in infrastructure and innovative solutions.

4. What are the growth drivers of the Europe Data Center Market?

Growth drivers in the Europe Data Center market include increased adoption of cloud computing, the rollout of 5G networks, the rise of AI and machine learning applications, and the shift towards energy-efficient data center operations.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.