Global Cuffless Blood Pressure Monitor Market Outlook to 2030

Region:Global

Author(s):Paribhasha Tiwari

Product Code:KROD7967

November 2024

100

About the Report

Global Cuffless Blood Pressure Monitor Market Overview

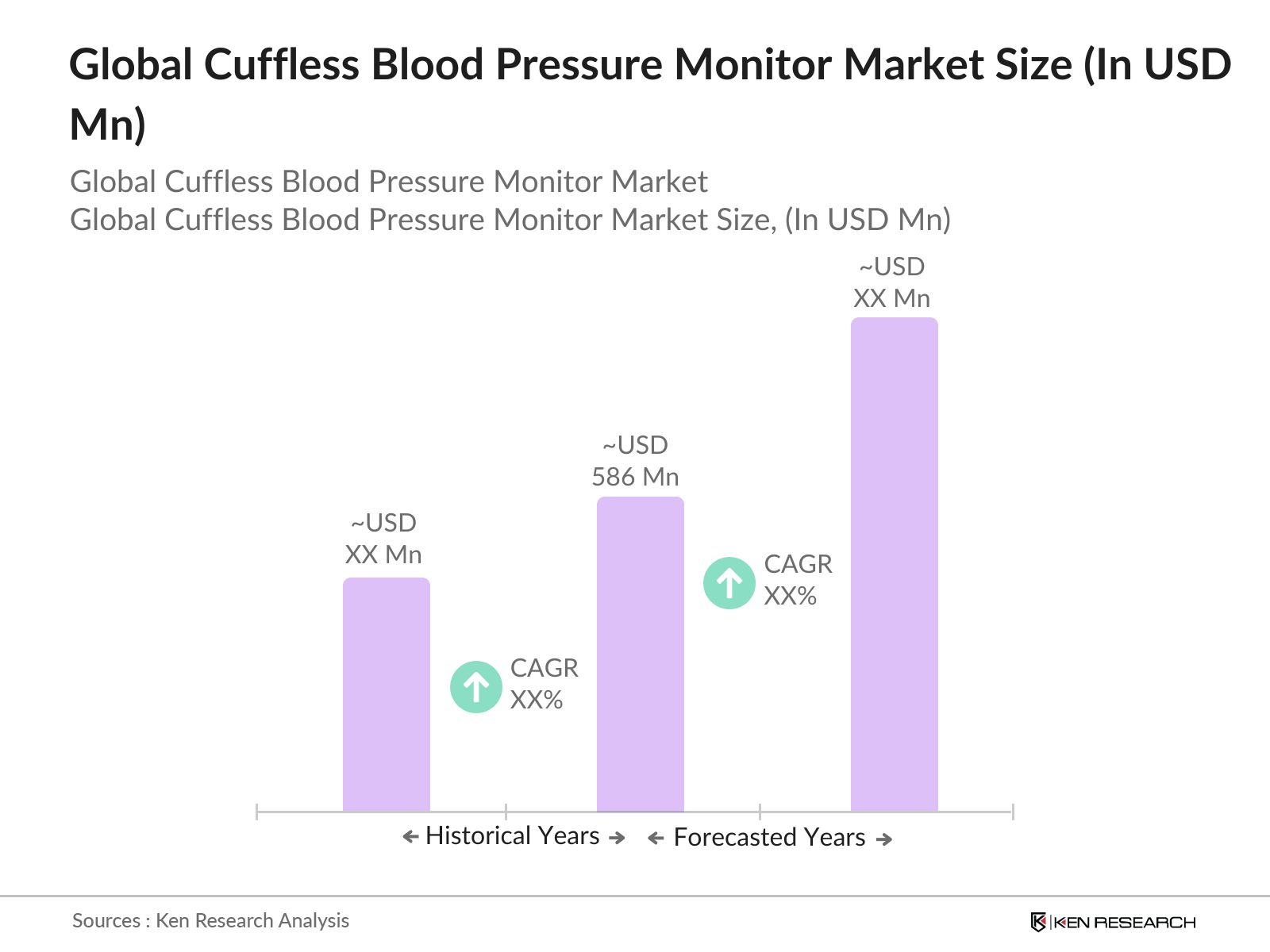

- The Global Cuffless Blood Pressure Monitor Market is valued at USD 586 million, based on a five-year historical analysis. This market is driven by the increasing prevalence of chronic diseases, such as hypertension and cardiovascular disorders, coupled with advancements in wearable health technologies. As healthcare shifts toward more personalized, non-invasive monitoring, cuffless monitors are increasingly preferred by patients and healthcare providers. The convenience of these devices and their integration with smartphones and telemedicine platforms further accelerates market growth.

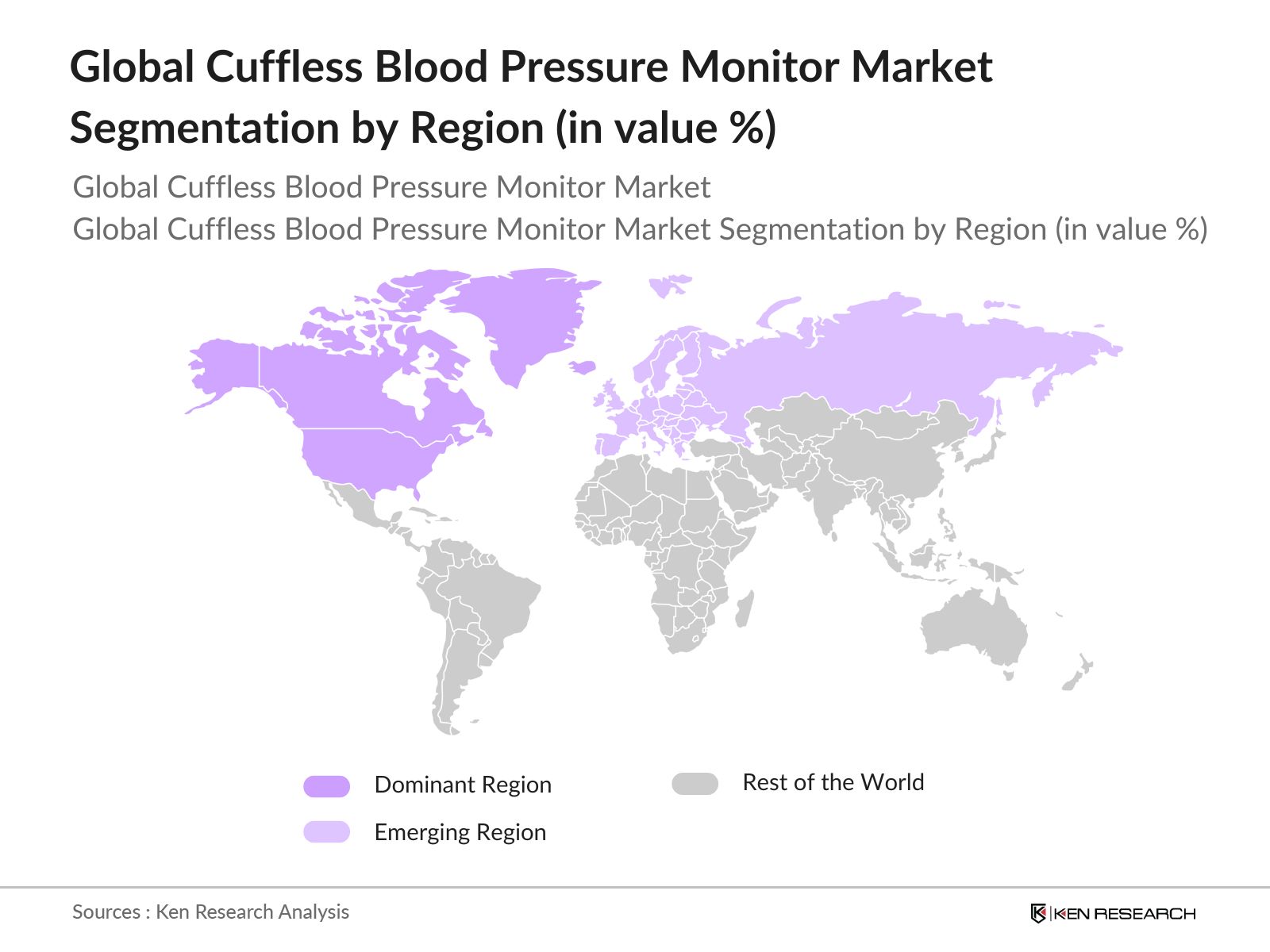

- Countries such as the United States, Japan, and Germany dominate the Global Cuffless Blood Pressure Monitor Market. The U.S. holds a strong position due to its robust healthcare infrastructure, high adoption rates of advanced medical technologies, and significant investment in healthcare innovations. Japan leads in Asia-Pacific due to its aging population and focus on preventive healthcare, while Germanys strong medical device manufacturing industry and government healthcare policies drive its market presence.

- The US CMS's reimbursement policies for remote patient monitoring devices, including cuffless monitors, will continue to evolve in 2024. This initiative encourages healthcare providers to adopt non-invasive monitoring solutions, facilitating faster adoption across various healthcare settings.

Global Cuffless Blood Pressure Monitor Market Segmentation

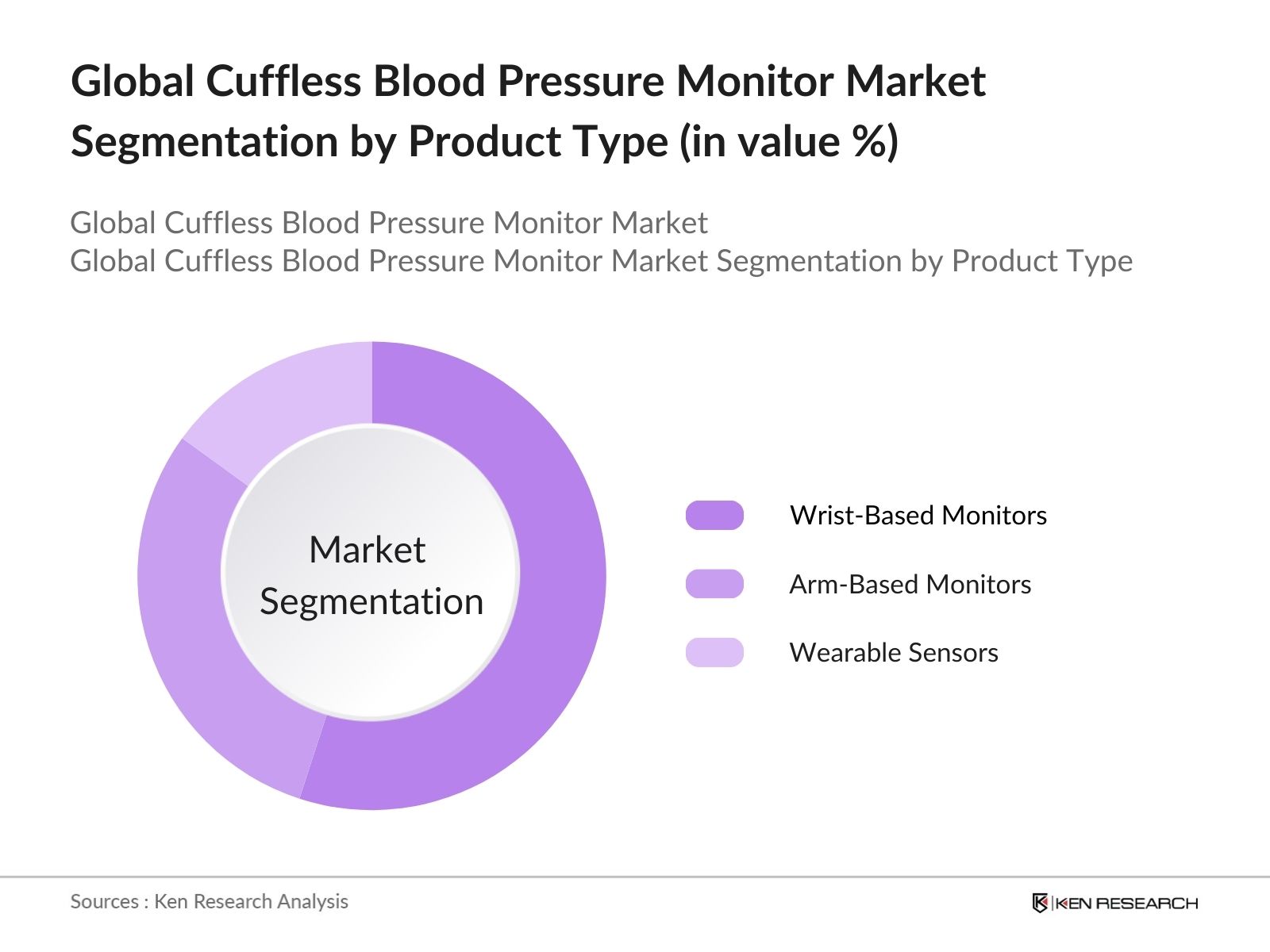

By Product Type: The Global Cuffless Blood Pressure Monitor Market is segmented by product type into wrist-based monitors, arm-based monitors, and wearable sensors. Wrist-based monitors dominate this segment due to their ease of use and integration with smartphones, making them popular among consumers for home-based monitoring. Additionally, wearable sensors are gaining traction, driven by advancements in sensor technology and the increasing demand for continuous, real-time health data monitoring.

By Region: The Global Cuffless Blood Pressure Monitor Market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominates the regional segment due to high adoption rates of advanced medical technologies, increased healthcare spending, and strong government support for healthcare innovation. Asia Pacific is expected to experience rapid growth due to rising healthcare awareness, a growing aging population, and increasing investments in healthcare infrastructure.

By End User: The Global Cuffless Blood Pressure Monitor Market is segmented by end user into homecare settings, hospitals, clinics, and ambulatory care centers. Homecare settings dominate the end-user segment due to the growing preference for home-based monitoring of chronic diseases like hypertension and the rise of telemedicine services. The availability of easy-to-use devices that provide accurate measurements without the need for clinical settings further boosts this segment.

Global Cuffless Blood Pressure Monitor Market Competitive Landscape

The Global Cuffless Blood Pressure Monitor Market is dominated by key players that have established strong market positions through innovation, product offerings, and strategic collaborations. These companies invest heavily in research and development to offer accurate and user-friendly monitoring solutions. The competition also includes emerging players leveraging advanced technologies like artificial intelligence and machine learning to enhance the accuracy and predictive capabilities of cuffless monitors.

|

Company |

Establishment Year |

Headquarters |

Revenue (2023) |

Product Innovation |

R&D Investment |

Regulatory Approvals |

Partnerships |

Global Presence |

Customer Base |

|---|---|---|---|---|---|---|---|---|---|

|

Omron Healthcare |

1933 |

Kyoto, Japan |

- | - | - | - | - | - | - |

|

Withings SA |

2008 |

Paris, France |

- | - | - | - | - | - | - |

|

Apple Inc. |

1976 |

Cupertino, USA |

- | - | - | - | - | - | - |

|

Biobeat Technologies |

2016 |

Petah Tikva, Israel |

- | - | - | - | - | - | - |

|

Aktiia |

2018 |

Neuchtel, Switzerland |

- | - | - | - | - | - | - |

Global Cuffless Blood Pressure Monitor Market Analysis

Growth Drivers

- Rise in Chronic Diseases: By 2024, global estimates indicate that over 1 billion individuals suffer from hypertension and other cardiovascular diseases, creating an urgent need for continuous and non-invasive monitoring solutions. The cuffless blood pressure monitor market is benefiting from increasing adoption by patients and healthcare providers alike. For instance, cardiovascular diseases alone cause approximately 17.9 million deaths annually, necessitating advanced monitoring devices to manage this patient load.

- Technological Advancements: The development and integration of artificial intelligence (AI) and advanced sensor technology in cuffless blood pressure monitors provide continuous, real-time monitoring. In 2024, the global AI healthcare technology market is projected to expand substantially, further accelerating the demand for cuffless monitoring. AI-driven devices are expected to offer improved accuracy and predictive analytics, making them integral in the management of chronic diseases and promoting more frequent adoption by hospitals and clinics.

- Growing Demand for Wearables: With the demand for wearable healthcare devices surging, the cuffless blood pressure monitor market is positioned to grow as an extension of this trend. In 2024, the global wearable technology market is projected to encompass hundreds of millions of active devices, driven by increasing awareness and adoption of personal health tracking. This expanding wearable ecosystem fuels demand for non-invasive blood pressure monitors integrated into smartwatches and fitness trackers.

Market Challenges

- Regulatory Barriers: Medical device regulations remain a significant challenge, with cuffless blood pressure monitors requiring stringent approvals from agencies such as the US FDA and the European CE. In 2024, approximately 30,000 medical devices worldwide will be subject to complex regulatory pathways. These processes slow market entry and limit the speed of product commercialization, particularly for small to mid-sized manufacturers.

- Data Privacy Concerns: With cuffless monitors increasingly integrated into wearable and smart devices, concerns regarding the security of patient data have grown. In 2024, the global healthcare sector will experience heightened scrutiny on cybersecurity, with an expected rise in data breaches across digital health platforms. Protecting sensitive medical information, particularly given the continuous nature of monitoring with cuffless devices, is a growing concern that manufacturers need to address to gain patient trust.

Global Cuffless Blood Pressure Monitor Market Future Outlook

Over the next five years, the Global Cuffless Blood Pressure Monitor Market is expected to witness significant growth. This will be driven by rising awareness regarding cardiovascular diseases, advancements in wearable technologies, and increased government support for non-invasive health monitoring solutions. The shift toward personalized and preventive healthcare will also spur demand for cuffless monitors, especially in developed economies with a high prevalence of lifestyle diseases.

Market Opportunities

- Integration with Telemedicine: Cuffless blood pressure monitors are well-positioned to benefit from the growing adoption of telemedicine. In 2024, telemedicine platforms are expected to service tens of millions of patients globally, particularly in regions with limited access to healthcare services. The ability of cuffless monitors to provide real-time data to healthcare providers, facilitating remote consultations and continuous patient monitoring, makes them a critical tool in telehealth ecosystems.

- Expansion into Emerging Markets: As awareness of hypertension and cardiovascular health increases in developing countries, there is growing demand for affordable health monitoring solutions. In 2024, the World Bank projects an increase in healthcare spending in regions like Asia-Pacific, with a focus on preventive care. Cuffless monitors, if priced competitively, could see significant adoption in countries like India and Brazil, where cardiovascular disease rates are rising rapidly.

Scope of the Report

|

By Product Type |

Wrist-Based Monitors |

|

By End User |

Homecare Settings |

|

By Region |

North America |

|

By Technology |

Optical Sensors |

|

By Distribution Channel |

Online Sales |

Products

Key Target Audience

Healthcare Providers (Hospitals, Clinics)

Medical Device Manufacturers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (FDA, CE)

Telemedicine Service Providers

Health Insurance Companies

Homecare Equipment Distributors

Technological Solution Providers

Companies

Players Mentioned in the Report:

Omron Healthcare

Withings SA

Apple Inc.

Biobeat Technologies

Aktiia

Samsung Electronics

Philips Healthcare

Valencell

Medtronic Plc

Masimo Corporation

Table of Contents

1. Global Cuffless Blood Pressure Monitor Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Market growth as per key health parameters like aging population, prevalence of cardiovascular diseases, and lifestyle changes)

1.4. Market Segmentation Overview (Segment by product type, technology, end-user, region)

2. Global Cuffless Blood Pressure Monitor Market Size (In USD Bn)

2.1. Historical Market Size (Analysis by adoption rates, technological penetration in healthcare)

2.2. Year-On-Year Growth Analysis (Key drivers including ease of use, convenience, and telemedicine integration)

2.3. Key Market Developments and Milestones (Innovations in sensor technology, regulatory approvals)

3. Global Cuffless Blood Pressure Monitor Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Chronic Diseases (Cardiovascular diseases, hypertension)

3.1.2. Technological Advancements (Use of AI and sensor technology for continuous monitoring)

3.1.3. Growing Demand for Wearables (Increased focus on remote monitoring)

3.1.4. Government Healthcare Initiatives (Health campaigns and support for non-invasive monitoring)

3.2. Market Challenges

3.2.1. Regulatory Barriers (Stringent FDA and CE approvals for medical devices)

3.2.2. Data Privacy Concerns (Issues related to patient data security)

3.2.3. High Costs of Advanced Devices (Affordability and accessibility challenges)

3.3. Opportunities

3.3.1. Integration with Telemedicine (Expansion of healthcare access through remote monitoring)

3.3.2. Expansion into Emerging Markets (Growing health awareness in developing countries)

3.3.3. Strategic Partnerships and Collaborations (Collaborations between device manufacturers and healthcare providers)

3.4. Trends

3.4.1. Adoption of Wearable Technology (Increase in health-conscious consumers using smartwatches, fitness trackers)

3.4.2. Use of Big Data Analytics (AI-based predictive analysis of blood pressure patterns)

3.4.3. Increased Focus on Preventive Healthcare (Shift toward early detection and lifestyle modification)

3.5. Government Regulation

3.5.1. Approval Process for Medical Devices (FDA, CE Mark, other international standards)

3.5.2. Guidelines for Data Security (GDPR, HIPAA compliance)

3.5.3. National Healthcare Policies (Healthcare initiatives and support for chronic disease monitoring)

3.5.4. Subsidies for Wearable Health Technologies (Government financial support and subsidies for device purchases)

3.6. SWOT Analysis (Industry-specific SWOT considering cuffless technology and market challenges)

3.7. Stakeholder Ecosystem (Key stakeholders like device manufacturers, healthcare providers, insurers, regulatory bodies)

3.8. Porters Five Forces (Analysis specific to medical device competition, supplier power, and industry barriers)

3.9. Competition Ecosystem (Detailed overview of competitive landscape, major competitors, and their strengths)

4. Global Cuffless Blood Pressure Monitor Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Wrist-Based Monitors

4.1.2. Arm-Based Monitors

4.1.3. Wearable Sensors

4.2. By Technology (In Value %)

4.2.1. Optical Sensors

4.2.2. PPG (Photoplethysmography)

4.2.3. Piezoelectric Sensors

4.2.4. Electrocardiography (ECG) Integration

4.3. By End User (In Value %)

4.3.1. Homecare Settings

4.3.2. Hospitals

4.3.3. Clinics

4.3.4. Ambulatory Care Centers

4.4. By Distribution Channel (In Value %)

4.4.1. Online Sales

4.4.2. Offline Retail (Pharmacies, Medical Device Stores)

4.4.3. Direct-to-Consumer Sales

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Cuffless Blood Pressure Monitor Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Omron Healthcare

5.1.2. Biobeat Technologies

5.1.3. Withings SA

5.1.4. Aktiia

5.1.5. Samsung Electronics

5.1.6. Apple Inc.

5.1.7. Philips Healthcare

5.1.8. Valencell

5.1.9. Medtronic Plc

5.1.10. A&D Medical

5.1.11. Huawei Technologies Co.

5.1.12. Masimo Corporation

5.1.13. Qardio Inc.

5.1.14. iHealth Labs

5.1.15. Omron Corporation

5.2. Cross Comparison Parameters

5.2.1 Company Size (No. of Employees)

5.2.2 Revenue

5.2.3 Headquarters

5.2.4 Inception Year

5.2.5 Product Innovation

5.2.6 R&D Spending

5.2.7 Regulatory Approvals

5.2.8 Global Market Presence

5.3. Market Share Analysis (Market share held by major players)

5.4. Strategic Initiatives (Key mergers, acquisitions, partnerships)

5.5. Investment Analysis (Investments in R&D, product innovation)

5.6. Venture Capital Funding

5.7. Government Grants

5.8. Private Equity Investments

6. Global Cuffless Blood Pressure Monitor Market Regulatory Framework

6.1. Medical Device Classification

6.2. Compliance Requirements (FDA, CE certifications)

6.3. Data Security and Privacy Regulations

7. Global Cuffless Blood Pressure Monitor Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Technological innovations, AI integration)

8. Global Cuffless Blood Pressure Monitor Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Technology (In Value %)

8.3. By End User (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. Global Cuffless Blood Pressure Monitor Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Analysis of customer demographics and market demand)

9.3. Marketing Initiatives (Strategic marketing recommendations for key players)

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins by constructing an ecosystem map that encompasses all major stakeholders within the Global Cuffless Blood Pressure Monitor Market. The objective is to identify critical variables influencing market dynamics, such as device adoption rates and technological innovations.

Step 2: Market Analysis and Construction

In this phase, historical data on market penetration and product innovation is compiled. Key metrics like device sales volumes, regional market concentration, and consumer behavior data are analyzed to understand market trends and revenue generation.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses are developed and validated through consultations with industry experts from leading medical device manufacturers. These consultations help to corroborate data, ensuring the accuracy of market forecasts and analysis.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing data gathered from primary and secondary sources. Comprehensive insights are obtained through direct engagement with manufacturers and healthcare providers, ensuring a holistic analysis of the markets current status and future potential.

Frequently Asked Questions

01. How big is the Global Cuffless Blood Pressure Monitor Market?

The Global Cuffless Blood Pressure Monitor Market is valued at USD 586 million, driven by technological advancements in wearable health monitoring devices and the increasing prevalence of chronic diseases like hypertension.

02. What are the key challenges in the Global Cuffless Blood Pressure Monitor Market?

Challenges in the Global Cuffless Blood Pressure Monitor Market include regulatory hurdles related to FDA and CE approvals, high costs of advanced wearable devices, and concerns regarding data privacy in patient health monitoring.

03. Who are the major players in the Global Cuffless Blood Pressure Monitor Market?

Key players in the Global Cuffless Blood Pressure Monitor Market include Omron Healthcare, Withings SA, Apple Inc., Biobeat Technologies, and Aktiia, who lead the market due to their technological innovations and extensive product offerings.

04. What are the growth drivers of the Global Cuffless Blood Pressure Monitor Market?

Growth of Global Cuffless Blood Pressure Monitor Market is driven by the increasing prevalence of chronic diseases, advancements in sensor technologies, and growing demand for non-invasive health monitoring devices, especially in developed countries.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.