Global IMU (Inertial Measurement Unit) Market Outlook to 2030

Region:Global

Author(s):Naman Rohilla

Product Code:KROD8187

December 2024

97

About the Report

Global IMU Market Overview

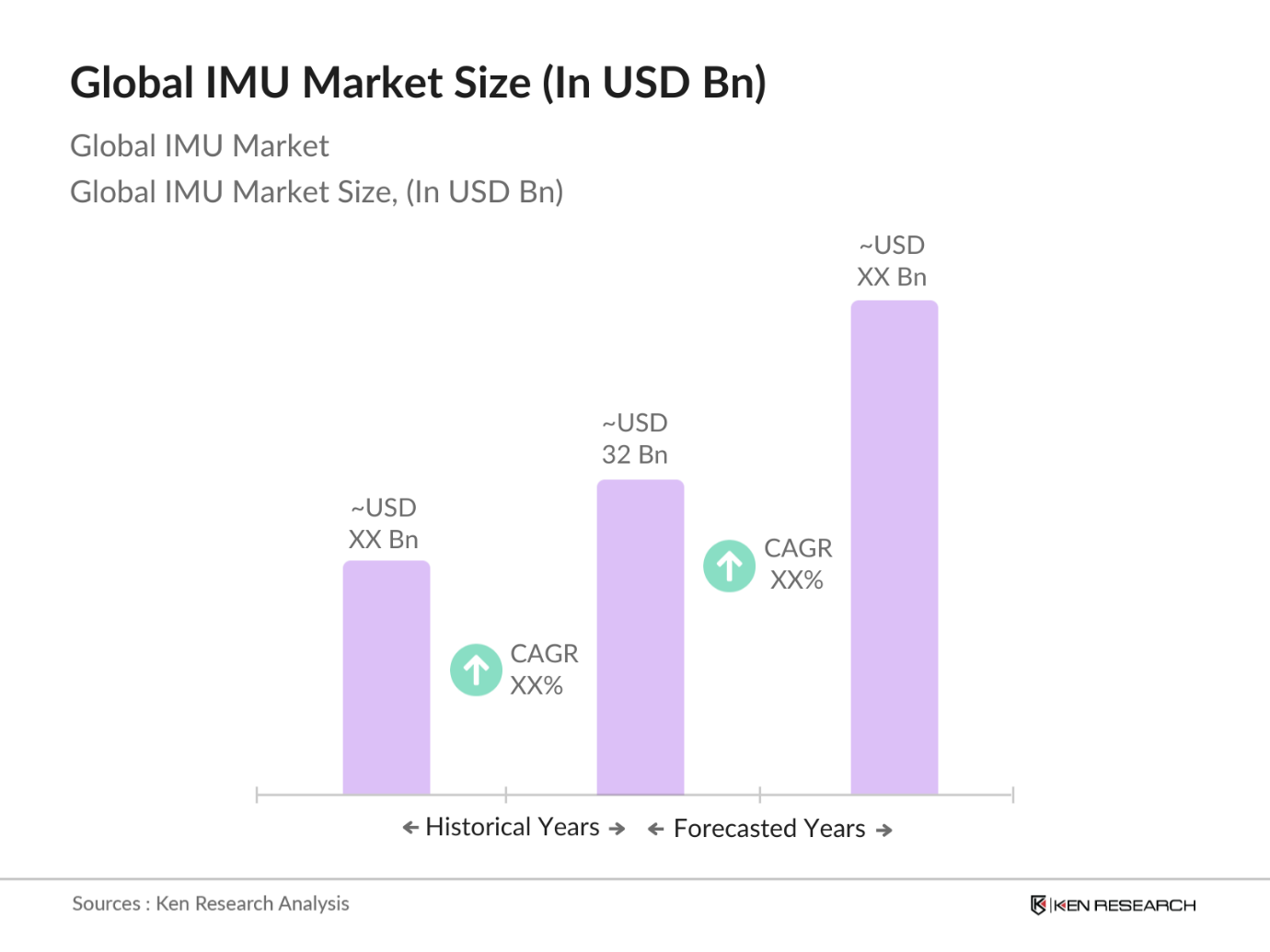

- The global Inertial Measurement Unit (IMU) market is valued at USD 32 billion, driven by the growing demand for IMU technology in a variety of industries, including aerospace, defense, automotive, and consumer electronics. The integration of IMUs in UAVs (unmanned aerial vehicles) and autonomous vehicles, combined with advancements in MEMS (Micro-Electro-Mechanical Systems) technology, has further propelled market growth. The push for more compact, accurate, and cost-effective IMUs has increased the adoption of these sensors across several sectors.

- Countries like the United States, China, and Germany are dominating the IMU market due to their advanced defense sectors, widespread automotive applications, and strong technological ecosystems. The U.S. leads due to its established defense and aerospace industries, while China benefits from its large-scale manufacturing capabilities and automotive production. Germany's dominance stems from its automotive industry and engineering expertise. These countries are early adopters of technological advancements, which further fuels their leadership in the IMU market.

- The International Traffic in Arms Regulations (ITAR) governs the export and import of defense-related articles, including IMUs used in military applications. In 2024, over 60% of IMUs produced globally were subject to ITAR controls, limiting their availability to certain countries and restricting the global trade of IMU technology. This regulatory framework ensures that sensitive IMU technologies used in defense and aerospace are not exported to adversaries, maintaining national security protocols.

Global IMU (Inertial Measurement Unit) Market Segmentation

- By Application: The IMU market is also segmented by application into aerospace and defense, automotive, marine, industrial, and consumer electronics. Aerospace and defense dominate the application segment due to the critical need for highly accurate and reliable IMUs in aircraft navigation, missiles, and space exploration missions. These systems demand robust performance under harsh conditions, which is why IMUs play an integral role in defense and aerospace systems worldwide.

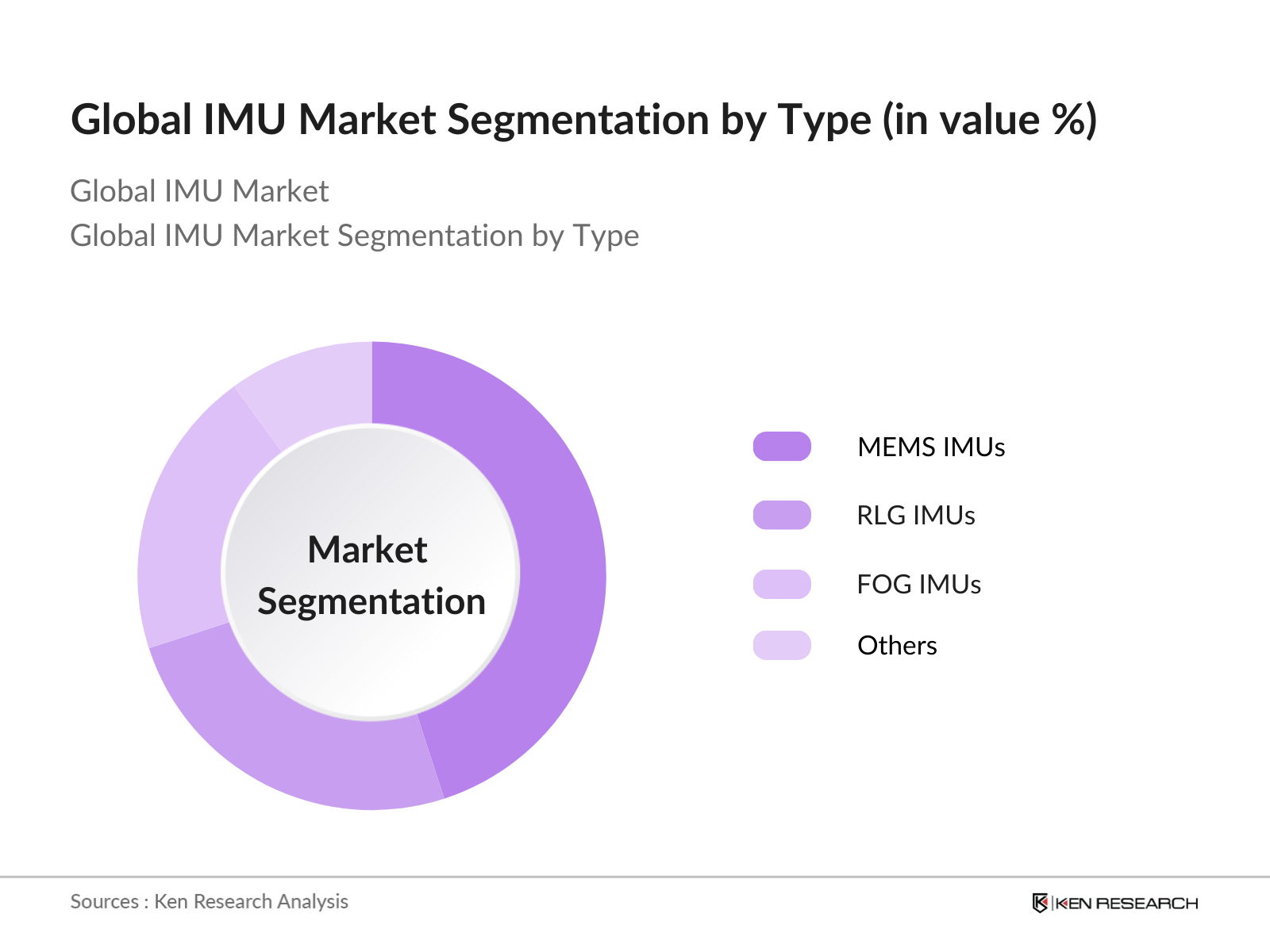

- By Type: The global IMU market is segmented by type into MEMS IMUs, Ring Laser Gyroscope (RLG) IMUs, Fiber Optic Gyroscope (FOG) IMUs, and others. MEMS IMUs hold the dominant market share, largely due to their miniaturization, lower costs, and growing integration into consumer electronics and automotive systems. The ability of MEMS IMUs to provide high precision at a reduced size and cost has made them the preferred choice for both commercial and military applications.

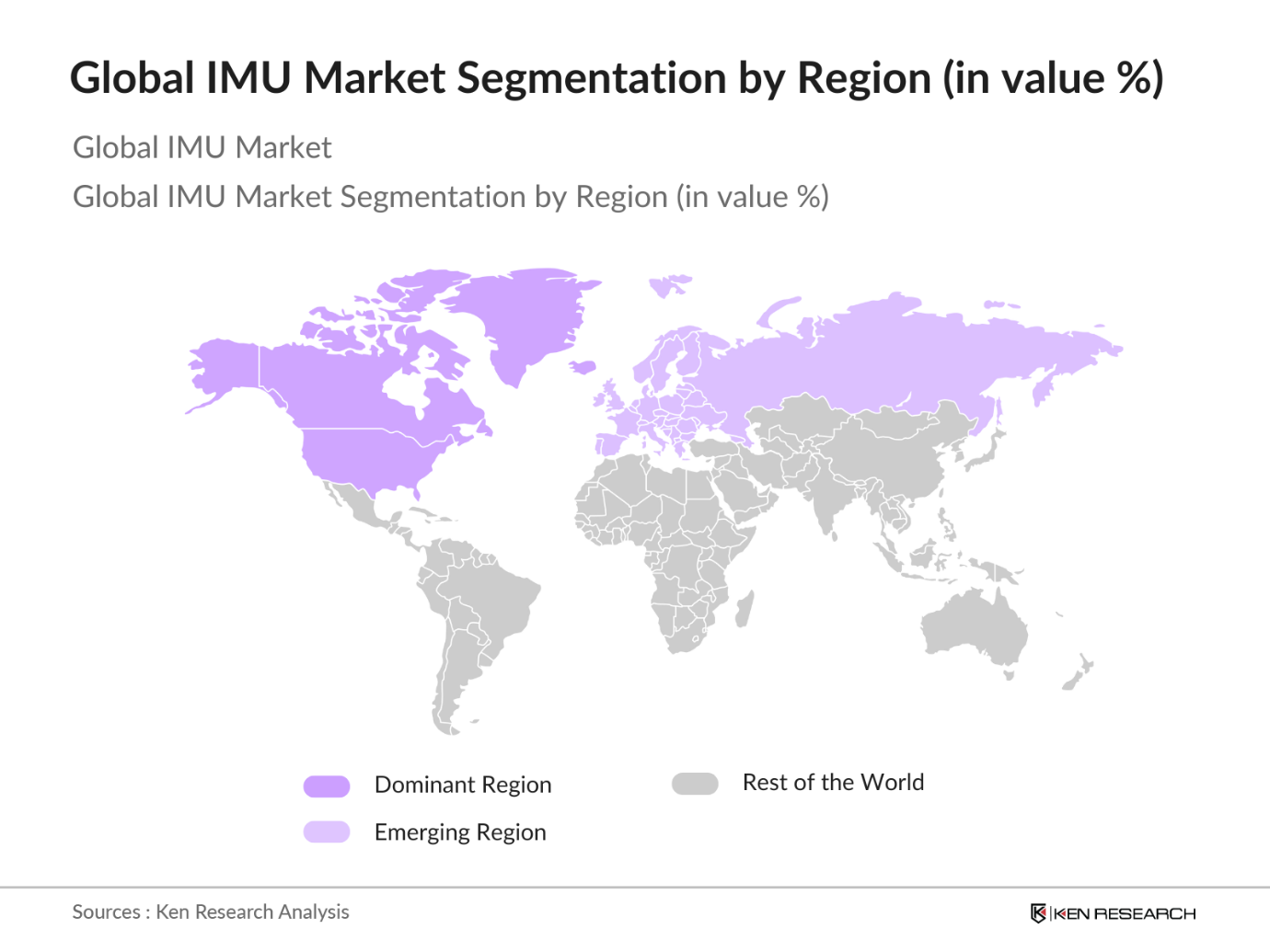

- By Region: Geographically, the IMU market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and Latin America. North America leads the global market, supported by the strong presence of aerospace, defense, and automotive sectors in the U.S. and Canada. Europe follows closely, driven by demand from the automotive and aerospace industries, particularly in countries like Germany and France. Asia-Pacific is expected to emerge as a growing market due to increasing investments in defense, consumer electronics, and autonomous vehicle technologies.

Global IMU (Inertial Measurement Unit) Market Competitive Landscape

The global IMU market is consolidated, with key players dominating various segments. The competition primarily focuses on technological innovations, collaborations with defense sectors, and the development of miniaturized, high-performance IMUs. Leading companies are continuously investing in R&D to gain a competitive advantage, with a focus on improving accuracy, reducing size, and integrating with other sensor technologies.

Global IMU (Inertial Measurement Unit) Market Analysis

Global IMU (Inertial Measurement Unit) Market Growth Drivers

- Rising Applications in Aerospace and Defense: In 2024, the aerospace and defense sectors accounted for over 20% of the IMU market's demand. The increasing use of IMUs in fighter jets, missiles, and spacecraft for precise positioning and navigation is a key driver. NASA's Artemis program, aiming to establish a sustainable lunar presence, significantly relies on IMUs for space navigation systems. The European Union, with its defense budget of 8 billion, also emphasizes the integration of IMUs in defense programs such as the European Defence Funds PESCO projects.

- Miniaturization of IMU Systems: Technological advancements in microelectromechanical systems (MEMS) are leading to the miniaturization of IMUs, making them more efficient for various applications, including drones, autonomous vehicles, and wearable technology. In 2024, global MEMS production surpassed 14 billion units, indicating widespread adoption. The miniaturization of IMUs has reduced the size and power consumption, enabling their use in small devices like consumer electronics and compact defense systems, aligning with current trends in energy efficiency and system integration.

- Integration with Advanced Sensors in Automotive Systems: IMUs are increasingly integrated into advanced driver assistance systems (ADAS) and autonomous vehicle platforms. The automotive sector, which saw the production of over 85 million vehicles in 2023, is adopting IMU technology to enhance vehicle safety and autonomous navigation. The global push toward electric vehicles, which represented 10% of total vehicle sales in 2023, is further driving demand for IMUs as these systems are crucial for electric and autonomous vehicle functionality.

Global IMU (Inertial Measurement Unit) Market Challenges

- High R&D Costs in IMU Development: The development of high-precision IMUs involves significant R&D expenditure due to the complexity of the technology and the need for advanced manufacturing techniques. In 2024, R&D spending in the aerospace and defense sectors exceeded $90 billion globally. This high cost of development limits the ability of smaller firms to enter the IMU market, as they struggle to match the technological capabilities of larger corporations, creating a barrier to market entry.

- Complexity of Integration with AI-driven Systems: IMUs play a critical role in AI-driven systems, particularly in robotics and autonomous vehicles, where they assist with navigation and orientation. However, integrating these systems is complex, as it requires synchronization between IMUs and AI algorithms. In 2023, AI-related sectors experienced a 35% increase in software and hardware integration challenges, impacting the deployment of IMUs in advanced robotics. As a result, delays in technology implementation are common, slowing the potential market growth for IMU applications.

Global IMU (Inertial Measurement Unit) Market Future Outlook

Over the next five years, the global IMU market is expected to experience substantial growth driven by advancements in MEMS technology, the rising adoption of autonomous vehicles, and the growing demand for UAVs in both commercial and military applications. The increasing use of IMUs in consumer electronics, particularly in gaming, wearables, and VR/AR, will also contribute to the markets expansion. The defense and aerospace sectors will continue to dominate, supported by rising global defense expenditures and technological innovations.

Global IMU (Inertial Measurement Unit) Market Opportunities

- Growth in Medical Robotics Applications: IMUs are increasingly being integrated into medical robotics for surgical precision and patient monitoring. In 2023, the medical robotics market reached 25,000 units worldwide, with IMUs playing a critical role in enhancing robotic functionality. The growing adoption of robotics in surgery, with over 2 million robotic-assisted surgeries performed annually, presents significant opportunities for the IMU market to expand into healthcare applications, particularly in minimally invasive procedures.

- Expanding Usage in Consumer Electronics: Consumer electronics, such as smartphones, wearables, and gaming devices, are incorporating IMUs to enhance user experience through motion sensing and tracking. In 2024, global smartphone shipments exceeded 1.4 billion units, with IMUs integrated into 70% of high-end models. Wearable devices, which are projected to reach 500 million active users by the end of the year, further drive the demand for miniaturized IMU systems. The integration of IMUs in these devices creates substantial growth opportunities in the consumer electronics market.

Scope of the Report

|

By Type |

MEMS IMU RLG IMU FOG IMU Others |

|

By Application |

Aerospace & Defense Automotive Marine Consumer Electronics Industrial |

|

By Technology |

MEMS Technology FOG Technology RLG Technology |

|

By End-user |

Military Civil Aviation Industrial Manufacturing Commercial Applications |

|

By Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

Products

Key Target Audience

Defense Contractors (U.S. Department of Defense, NATO)

Automotive Manufacturers (General Motors, Tesla, BMW)

Aerospace & Aviation Companies (Boeing, Airbus)

UAV & Robotics Companies (DJI, Lockheed Martin)

Consumer Electronics Companies (Apple, Samsung)

Banks and Financial Institutions

Marine Navigation Companies (Navico, Raytheon)

Government and Regulatory Bodies (FAA, EASA, U.S. Defense Department)

Investors and Venture Capitalist Firms

Companies

Players Mentioned in the Report

Honeywell International Inc.

Bosch Sensortec GmbH

Northrop Grumman Corporation

STMicroelectronics

Safran S.A.

Analog Devices Inc.

Thales Group

VectorNav Technologies

Lord MicroStrain

TDK Corporation

Table of Contents

1. Global IMU Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (IMU adoption, technological innovation, industry adoption rates)

1.4. Market Segmentation Overview

2. Global IMU Market Size (in USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Analysis of market growth drivers and key milestones)

2.3. Key Market Developments and Milestones

3. Global IMU Market Analysis

3.1. Growth Drivers (Technological advancements, demand for precision navigation, sector-specific growth)

3.1.1. Increasing demand for UAVs and autonomous vehicles

3.1.2. Rising applications in aerospace and defense

3.1.3. Miniaturization of IMU systems for consumer electronics

3.1.4. Growing automotive sector demand for ADAS and driver assistance systems

3.2. Market Challenges (Supply chain constraints, manufacturing complexities, technological bottlenecks)

3.2.1. High R&D costs in developing advanced IMUs

3.2.2. Complex integration with AI-driven systems

3.2.3. Dependence on high-precision raw materials

3.3. Opportunities (Emerging applications, expanding sectors, global adoption)

3.3.1. Growth in medical robotics and wearable technologies

3.3.2. Expanding usage in augmented reality (AR) and virtual reality (VR)

3.3.3. Increased application in mining and energy exploration

3.4. Trends (Technological innovations, product development, industry shifts)

3.4.1. Development of MEMS-based IMUs

3.4.2. Focus on lightweight, compact IMUs with higher accuracy

3.4.3. Rising demand for tactical-grade IMUs in industrial applications

3.5. Government Regulations (Compliance frameworks, certification processes, regulatory landscape)

3.5.1. ITAR regulations (US Department of Defense export controls)

3.5.2. EU defense-related IMU standards

3.5.3. FAA guidelines for aerospace IMU integration

3.5.4. Military and aerospace certification requirements for IMUs

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Suppliers, manufacturers, distributors, end-users)

3.8. Porters Five Forces Analysis (Market competition, supplier power, threat of substitutes)

3.9. Competitive Ecosystem

4. Global IMU Market Segmentation

4.1. By Type (in Value %)

4.1.1. MEMS IMU

4.1.2. RLG IMU (Ring Laser Gyroscope)

4.1.3. FOG IMU (Fiber Optic Gyroscope)

4.1.4. Mechanical IMU

4.1.5. Others

4.2. By Application (in Value %)

4.2.1. Aerospace & Defense

4.2.2. Automotive (ADAS, Autonomous Driving Systems)

4.2.3. Marine

4.2.4. Consumer Electronics (AR/VR, mobile devices)

4.2.5. Industrial Automation

4.3. By Technology (in Value %)

4.3.1. MEMS Technology

4.3.2. RLG Technology

4.3.3. FOG Technology

4.3.4. Hybrid Technology

4.4. By End-user (in Value %)

4.4.1. Military

4.4.2. Civil Aviation

4.4.3. Automotive Manufacturing

4.4.4. Robotics and Automation

4.4.5. Industrial Manufacturing

4.5. By Region (in Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5. Global IMU Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Honeywell International Inc.

5.1.2. Bosch Sensortec GmbH

5.1.3. Northrop Grumman Corporation

5.1.4. STMicroelectronics

5.1.5. Analog Devices Inc.

5.1.6. Thales Group

5.1.7. Safran S.A.

5.1.8. VectorNav Technologies

5.1.9. Lord MicroStrain

5.1.10. TDK Corporation

5.1.11. Sensonor AS

5.1.12. Trimble Inc.

5.1.13. Kearfott Corporation

5.1.14. Xsens Technologies B.V.

5.1.15. KVH Industries

5.2. Cross Comparison Parameters (R&D Investments, Technological Expertise, Product Range, Global Reach, Manufacturing Capacity, Key Partnerships, Customer Base, Financial Performance)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Collaborations, Product Launches)

5.5. Mergers & Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Support

5.9. Private Equity Investments

6. Global IMU Market Regulatory Framework

6.1. Defense Certifications

6.1.1. MIL-STD-810 (Environmental Standards)

6.1.2. MIL-STD-461 (Electromagnetic Compatibility)

6.1.3. ISO Certification for Industrial Applications

6.1.4. FAA and EASA Compliance for Aviation

7. Global IMU Future Market Size (in USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Increased adoption in autonomous systems, Industry 4.0 applications)

8. Global IMU Future Market Segmentation

8.1. By Type (in Value %)

8.2. By Application (in Value %)

8.3. By Technology (in Value %)

8.4. By End-user (in Value %)

8.5. By Region (in Value %)

9. Global IMU Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Key customer segments, new use cases, and buying behavior)

9.3. Marketing Initiatives (Product positioning, value proposition for emerging markets)

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase focuses on constructing an ecosystem map involving all major stakeholders in the global IMU market. Extensive desk research using both secondary and proprietary databases was conducted to gather comprehensive information. The main objective was to define the key variables influencing market growth and dynamics.

Step 2: Market Analysis and Construction

This phase involved analyzing historical data related to the IMU market, evaluating market penetration across sectors like defense and automotive, and understanding revenue generation trends. This step ensures that reliable and accurate market forecasts and revenue estimates are constructed.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through consultations with industry experts, which included engineers, product developers, and key executives from IMU manufacturing companies. These consultations provided direct insights into operational challenges and market drivers.

Step 4: Research Synthesis and Final Output

In the final stage, data from direct engagements with IMU manufacturers and defense contractors were synthesized to ensure comprehensive coverage. This phase also involved validating the gathered information through bottom-up approaches to provide accurate market analysis.

Frequently Asked Questions

01. How big is the Global IMU Market?

The global IMU market is valued at USD 32 billion, driven by applications across aerospace, defence, automotive, and consumer electronics sectors.

02. What are the challenges in the Global IMU Market?

Challenges include high R&D costs, complex integration with advanced systems, and supply chain dependencies, particularly for materials like MEMS components.

03. Who are the major players in the Global IMU Market?

Key players include Honeywell International Inc., Bosch Sensortec GmbH, Northrop Grumman Corporation, STMicroelectronics, and Safran S.A., all of whom have a strong presence in both commercial and defence markets.

04. What are the growth drivers in the Global IMU Market?

The market is driven by increased demand for autonomous vehicles, UAVs, and military-grade navigation systems. The miniaturization of sensors and advancements in MEMS technology have further contributed to growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.