Global Satellite Communication Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1022

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1022

December 2024

99

The global satellite communication market is dominated by several major players that are heavily invested in satellite launches, bandwidth expansion, and technology development. This consolidation highlights the significant influence of these key companies, who have established themselves as leaders through innovation, strategic partnerships, and government contracts.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD) |

Satellites Launched |

LEO/ GEO Focus |

Bandwidth Capacity |

Global Presence |

R&D Investments |

Strategic Partnerships |

|

SES S.A. |

1985 |

Luxembourg |

2.2 billion |

||||||

|

Intelsat S.A. |

1964 |

United States |

2.5 billion |

||||||

|

Viasat Inc. |

1986 |

United States |

2.4 billion |

||||||

|

Iridium Communications Inc. |

2000 |

United States |

0.8 billion |

||||||

|

Eutelsat Communications S.A. |

1977 |

France |

1.4 billion |

Global Satellite Communication Market Growth Drivers

Global Satellite Communication Market Challenges

Over the next five years, the global satellite communication market is expected to experience significant growth, driven by increasing demand for high-speed broadband services, the development of 5G infrastructure, and growing investment in satellite constellations such as SpaceXs Starlink. Additionally, the rising demand for satellite services in defense, remote communication, and IoT sectors will further propel market expansion.

Market Opportunities:

|

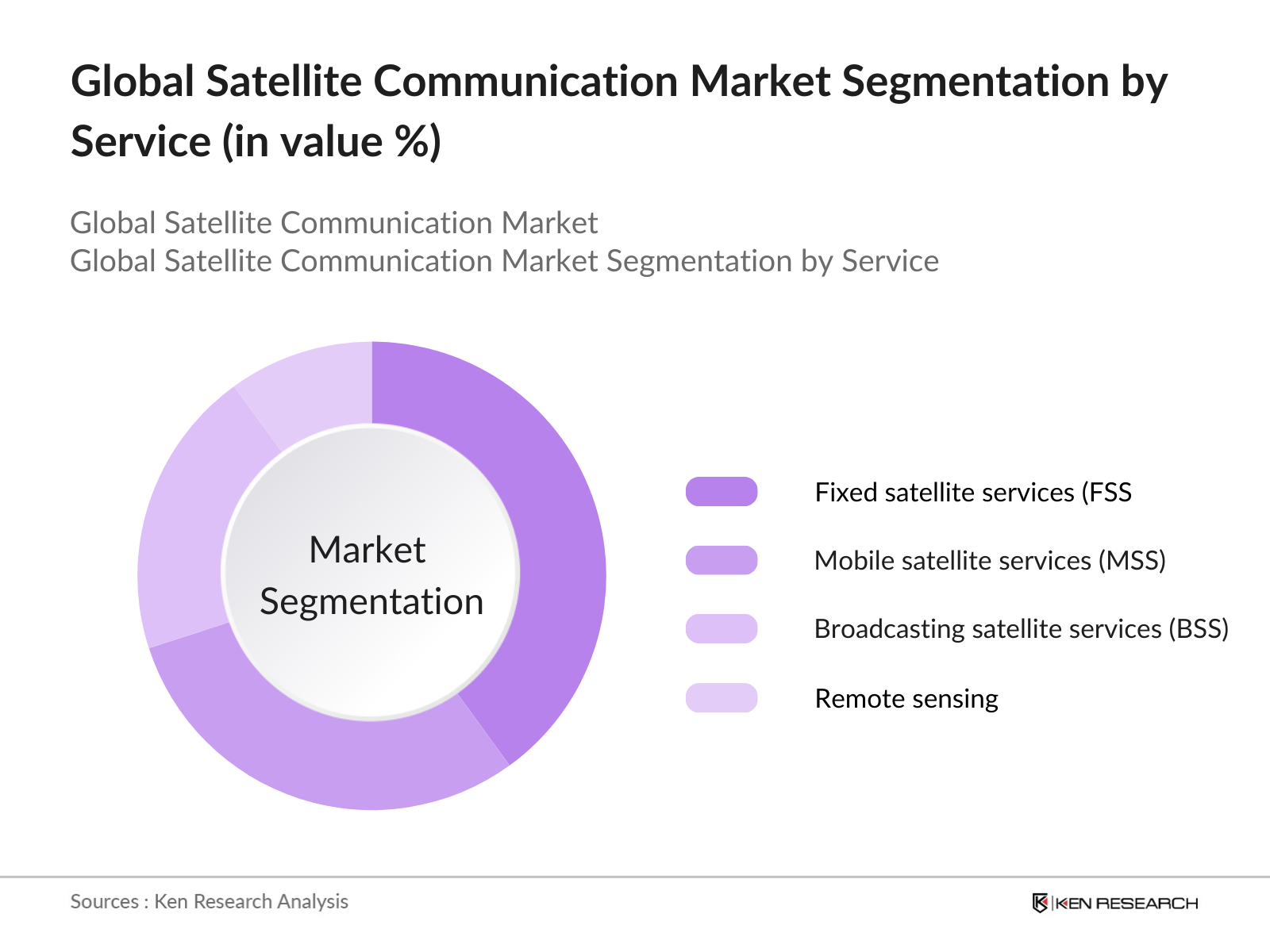

By Service |

Fixed Satellite Services Mobile Satellite Services Broadcasting Satellite Services Remote Sensing |

|

By Frequency Band |

C Band Ku Band Ka Band L Band |

|

By Component |

Satellite Terminals Satellite Antennas Satellite Transponders Satellite Ground Equipment |

|

By Application |

Commercial Military & Defense Maritime Aviation |

|

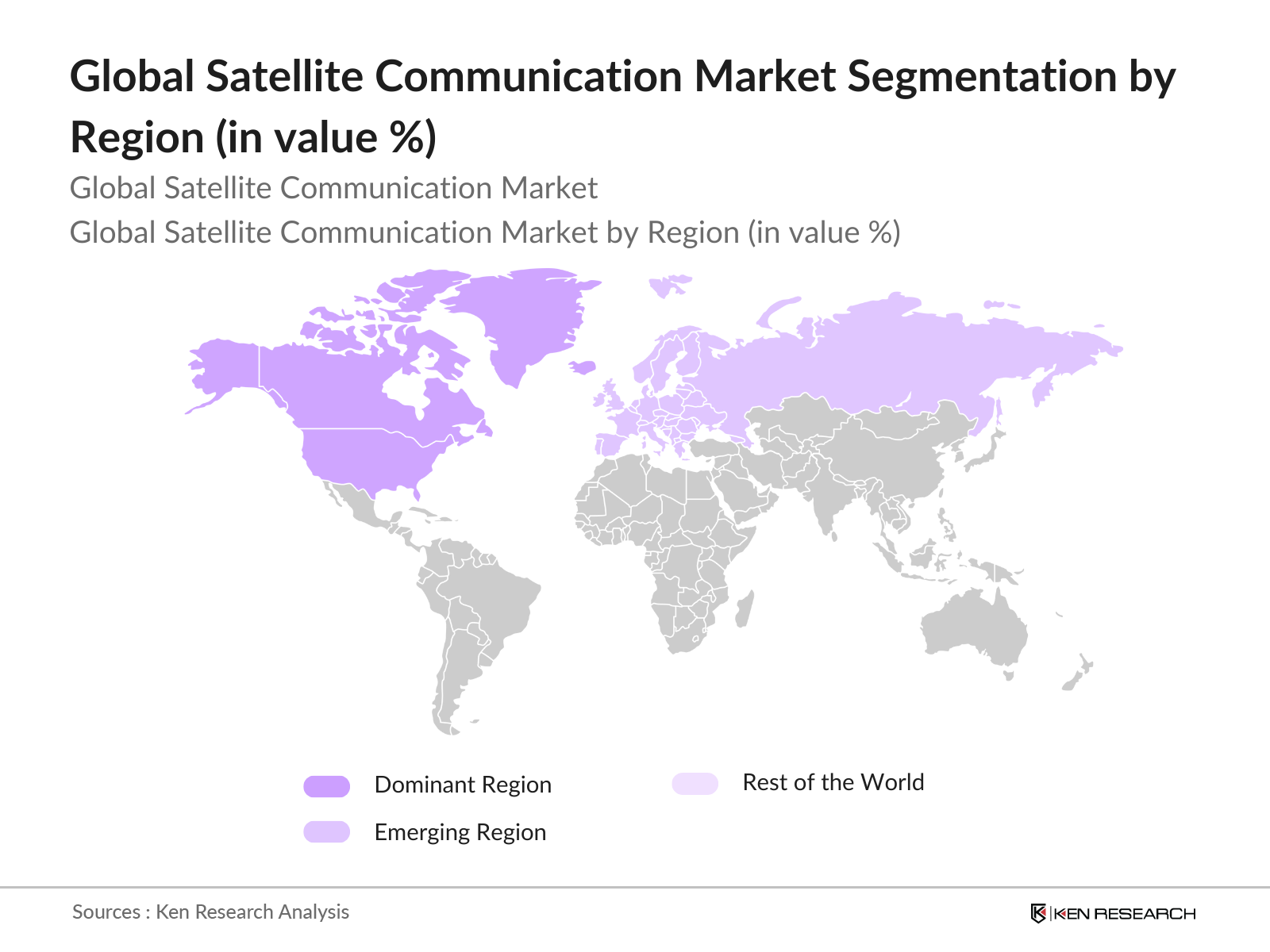

By Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1. Global Satellite Communication Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CAGR and Market Dynamics)

1.4. Market Segmentation Overview (By Service, By Frequency Band, By Component, By Application, By End-User, By Region)

2. Global Satellite Communication Market Size (In USD Billion)

2.1. Historical Market Size (Market Value & Volume)

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Launches, Innovations, Key Partnerships)

3. Global Satellite Communication Market Analysis

3.1. Growth Drivers (Technological Advancements, Demand for Broadband Services, IoT Expansion, Remote Communication Needs)

3.2. Market Challenges (Regulatory Issues, Spectrum Allocation, High Deployment Costs, Cybersecurity Threats)

3.3. Opportunities (Emerging Markets, Increased Use of Satellite IoT, Development of High-Throughput Satellites)

3.4. Trends (LEO Satellites Growth, Satellite Miniaturization, Expansion of Satellite Constellations)

3.5. Government Regulations and Initiatives (Spectrum Regulation, National Space Programs, Satellite Launch Incentives)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces (Bargaining Power, Threat of Substitutes, Competitive Rivalry)

3.9. Competitive Landscape

4. Global Satellite Communication Market Segmentation

4.1. By Service (In Value %)

4.1.1. Fixed Satellite Services

4.1.2. Mobile Satellite Services

4.1.3. Broadcasting Satellite Services

4.1.4. Remote Sensing

4.2. By Frequency Band (In Value %)

4.2.1. C Band

4.2.2. Ku Band

4.2.3. Ka Band

4.2.4. L Band

4.3. By Component (In Value %)

4.3.1. Satellite Terminals

4.3.2. Satellite Antennas

4.3.3. Satellite Transponders

4.3.4. Satellite Ground Equipment

4.4. By Application (In Value %)

4.4.1. Commercial

4.4.2. Military & Defense

4.4.3. Maritime

4.4.4. Aviation

4.5. By End-User (In Value %)

4.5.1. Aerospace

4.5.2. Defense

4.5.3. Telecom

4.5.4. Transportation

4.5.5. Media & Entertainment

4.5.6. Healthcare

4.6. By Region (In Value %)

4.6.1. North America

4.6.2. Europe

4.6.3. Asia-Pacific

4.6.4. Middle East & Africa

4.6.5. Latin America

5. Global Satellite Communication Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. SES S.A.

5.1.2. Intelsat S.A.

5.1.3. Viasat Inc.

5.1.4. Iridium Communications Inc.

5.1.5. L3Harris Technologies, Inc.

5.1.6. Thales Group

5.1.7. Eutelsat Communications S.A.

5.1.8. Inmarsat Global Limited

5.1.9. Hughes Network Systems LLC

5.1.10. Telesat

5.1.11. Lockheed Martin Corporation

5.1.12. Northrop Grumman Corporation

5.1.13. Cobham SATCOM

5.1.14. Orbital ATK (Northrop Grumman Innovation Systems)

5.1.15. Kongsberg Satellite Services (KSAT)

5.2. Cross Comparison Parameters (Revenue, Satellite Capacity, Market Share, Geographical Presence, Technological Innovation, Satellites Launched, Bandwidth Capacity, R&D Investments)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Expansion Strategies, Satellite Launch Programs, M&A, Joint Ventures)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Support

5.9. Private Equity Investments

6. Global Satellite Communication Market Regulatory Framework

6.1. Global Communication Satellite Regulations

6.2. Spectrum Allocation and Licensing

6.3. Certification Processes for Satellite Launches

6.4. Environmental Impact and Sustainability

7. Global Satellite Communication Future Market Size (In USD Billion)

7.1. Future Market Size Projections (Market Value & Volume)

7.2. Key Factors Driving Future Market Growth (Expanding LEO Constellations, 5G Integration, Enhanced Satellite Technologies)

8. Global Satellite Communication Future Market Segmentation

8.1. By Service (In Value %)

8.2. By Frequency Band (In Value %)

8.3. By Component (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. Global Satellite Communication Market Analysts Recommendations

9.1. Total Addressable Market (TAM)/ Serviceable Addressable Market (SAM) / Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Strategies and Key Positioning

9.4. White Space Opportunity Analysis

The initial step involved mapping the satellite communication ecosystem, identifying key stakeholders like telecom operators, satellite manufacturers, and regulatory bodies. A combination of proprietary and secondary research was employed to collect relevant data, including major players, service offerings, and regulatory frameworks.

This phase focused on collecting historical data on satellite launches, service deployments, and regional market penetration. Additionally, assessments of market drivers, such as the demand for high-bandwidth services, were conducted, followed by revenue analysis based on service offerings and geographical distribution.

Market hypotheses were formulated and validated through interviews with industry experts, including executives from leading satellite communication companies. These consultations offered operational insights into emerging technologies like low-latency satellite services and helped refine revenue estimates.

In the final phase, data from primary and secondary sources were synthesized to provide a comprehensive analysis. Feedback from satellite equipment manufacturers and service providers was integrated to validate findings and ensure the accuracy of market projections.

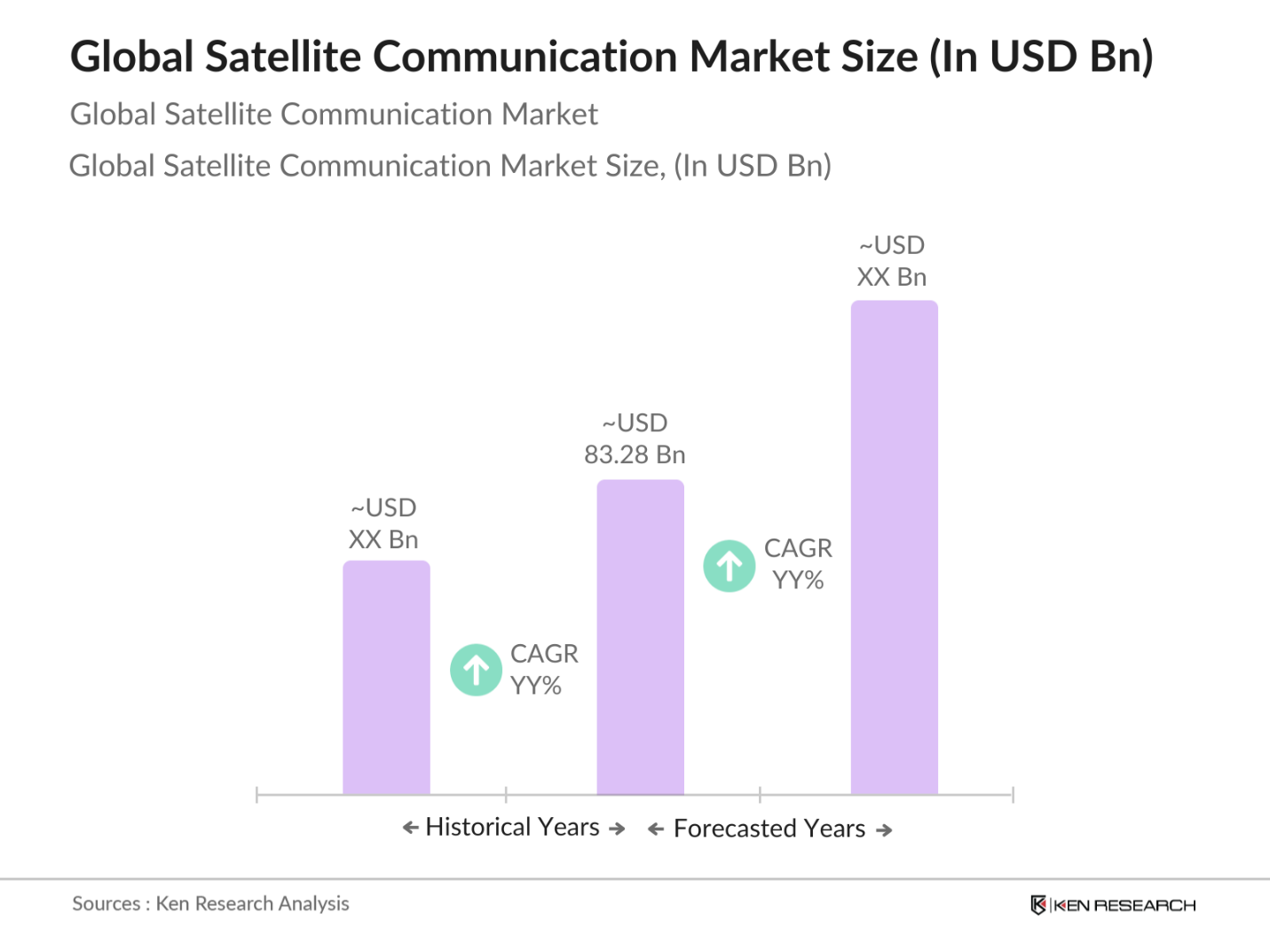

The global satellite communication market was valued at USD 83.28 billion in 2023, driven by rising demand for remote communication services and the rapid deployment of satellite constellations, such as those launched by SpaceX and other major providers.

Challenges in the satellite communication market include high deployment costs, spectrum allocation issues, and cybersecurity threats. The need for significant capital investments in satellite launches and infrastructure also acts as a barrier for smaller players.

Key players in the market include SES S.A., Intelsat S.A., Viasat Inc., Iridium Communications Inc., and Eutelsat Communications S.A. These companies dominate due to their extensive satellite fleets, advanced technological capabilities, and strategic partnerships.

Growth drivers include the integration of satellite services with 5G networks, the increasing demand for IoT and broadband services in remote regions, and the continued expansion of low-cost satellite constellations by companies like SpaceX.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.