Global Silicon Wafer Manufacturing Market Outlook to 2030

Region:Global

Author(s):Shubham Kashyap

Product Code:KROD4397

December 2024

86

About the Report

Global Silicon Wafer Manufacturing Market Overview

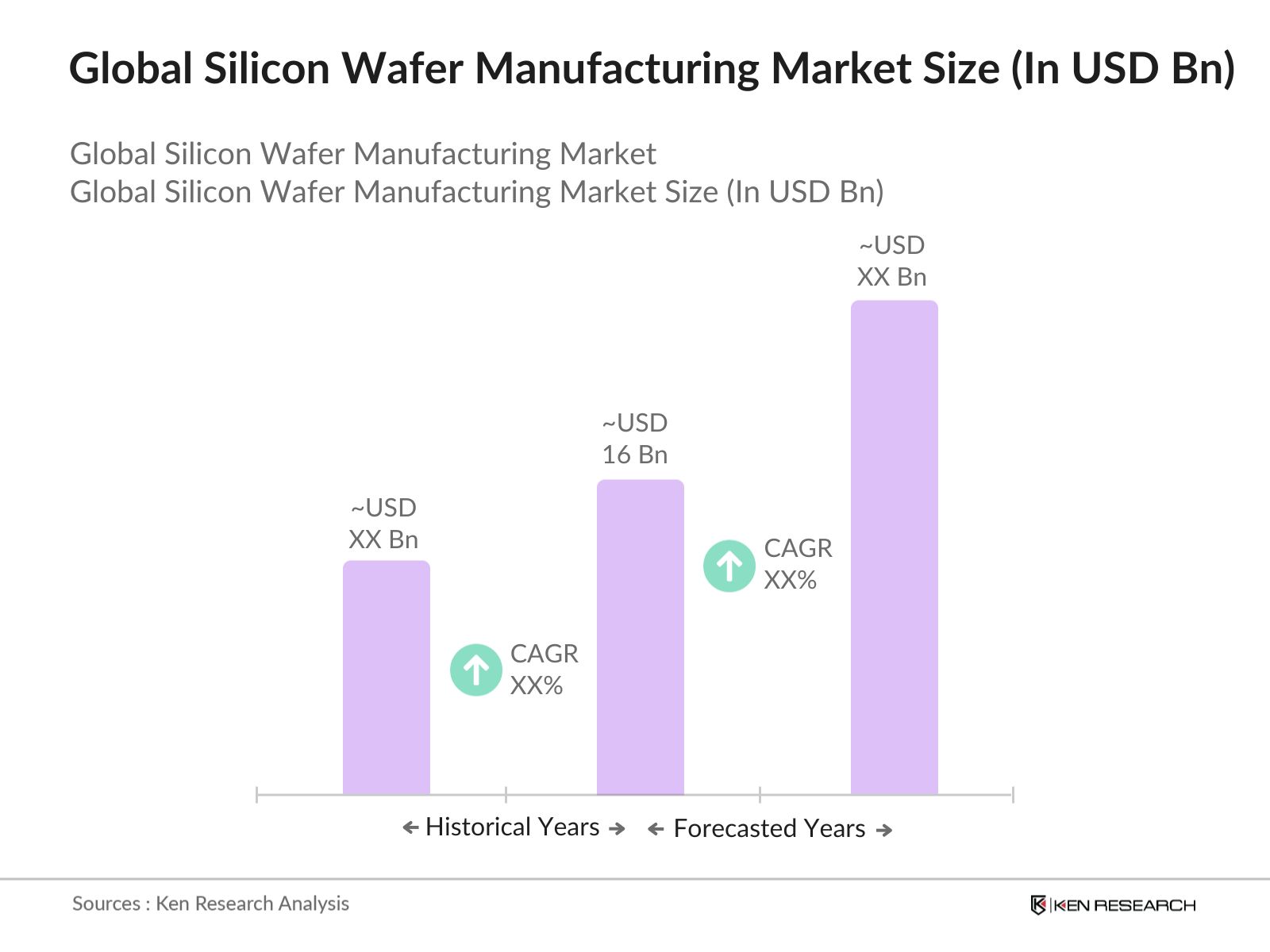

- The global silicon wafer manufacturing market is experiencing significant growth, currently valued at USD 16 Bn, driven by increasing demand from industries such as semiconductors, consumer electronics, automotive, and renewable energy. Silicon wafers, the fundamental building blocks for integrated circuits, play a critical role in the production of electronic devices, and their demand is growing as technological advancements continue. As of 2023, major regions such as the United States, China, and Europe are leading in silicon wafer production due to strong industrial bases and advanced technological infrastructure.

- Key countries dominating the global silicon wafer manufacturing market include the United States, China, and Japan. These countries have established themselves as leaders due to their advanced semiconductor industries, strong industrial infrastructure, and ongoing investments in R&D. The U.S. dominates through its innovations in high-end chip manufacturing, while China is aggressively expanding its domestic semiconductor production capacity, driven by its national focus on reducing reliance on imports. Japan, with its longstanding expertise in semiconductor materials, continues to be a leading supplier of high-purity silicon wafers.

- Governments across the globe are providing incentives and subsidies to support the semiconductor industry, recognizing its strategic importance. In 2023, the U.S. government launched initiatives to boost domestic chip production, including incentives for silicon wafer manufacturers. Similarly, China has implemented policies to reduce its reliance on foreign semiconductor imports by ramping up local production. The European Union also unveiled its European Chips Act in 2023, which aims to double its semiconductor market share by 2030, further fueling demand for silicon wafers.

Global Silicon Wafer Manufacturing Market Segmentation

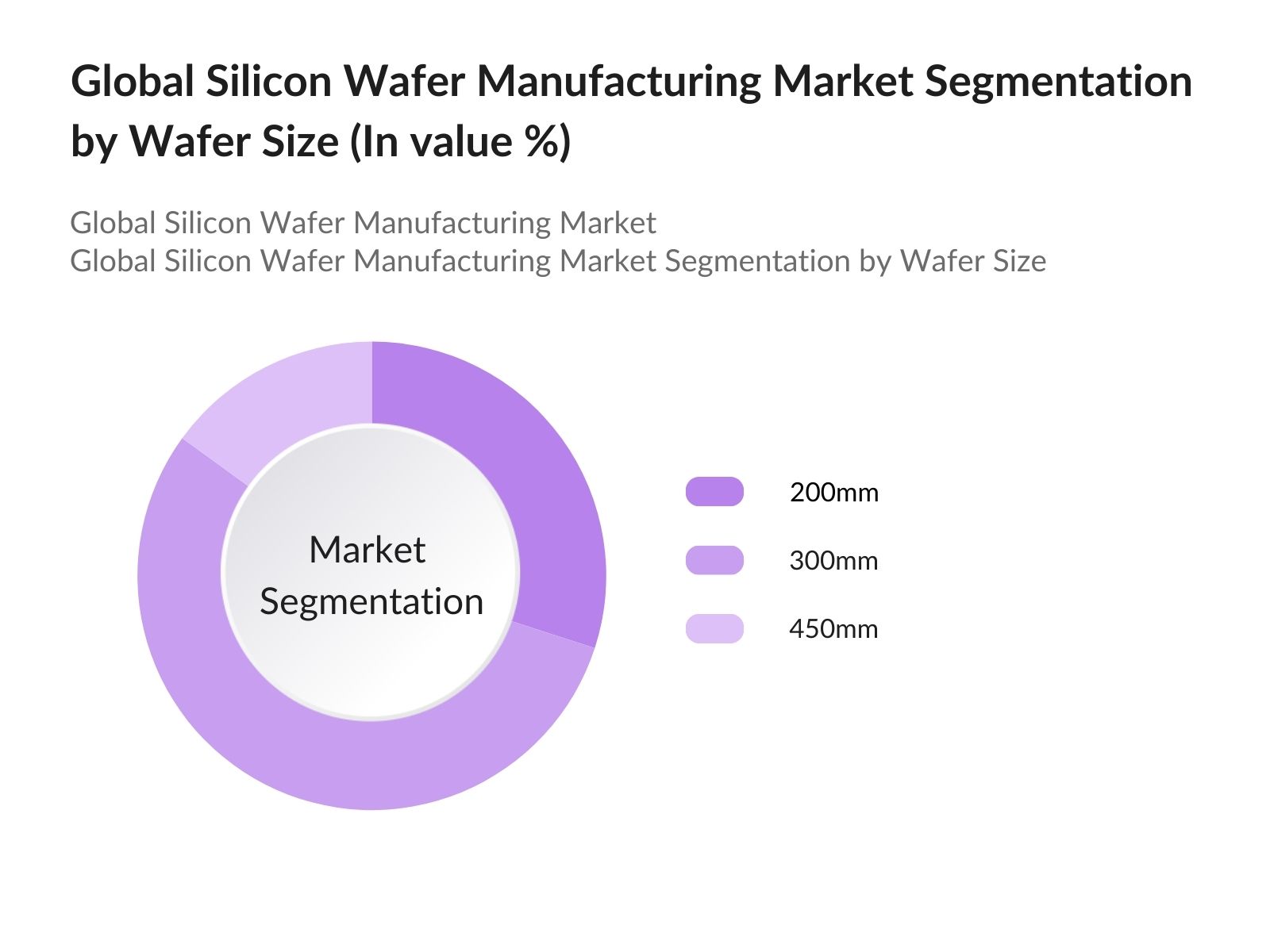

- By Wafer Size: The market is segmented by wafer size into 200mm, 300mm, and 450mm wafers. Currently, the 300mm wafers dominate the market due to their extensive use in modern semiconductor fabrication processes. These wafers offer higher yields and lower production costs, making them ideal for high-volume production of memory chips, processors, and sensors used in consumer electronics, automotive, and telecommunication applications. As more semiconductor manufacturers transition from 200mm to 300mm wafers, this segment is expected to maintain its dominance in the coming years.

- By Application: The market is driven by its diverse applications across multiple industries. The semiconductor sector remains the largest consumer, accounting for the majority of the market share due to the demand for integrated circuits and microchips in consumer electronics, data centers, and cloud computing. The automotive industry is also increasingly relying on silicon wafers for electric vehicles and autonomous driving systems, while the renewable energy sector is using them in solar cells for photovoltaic systems. The application of silicon wafers in 5G infrastructure development is another significant growth driver, particularly in North America and Asia-Pacific.

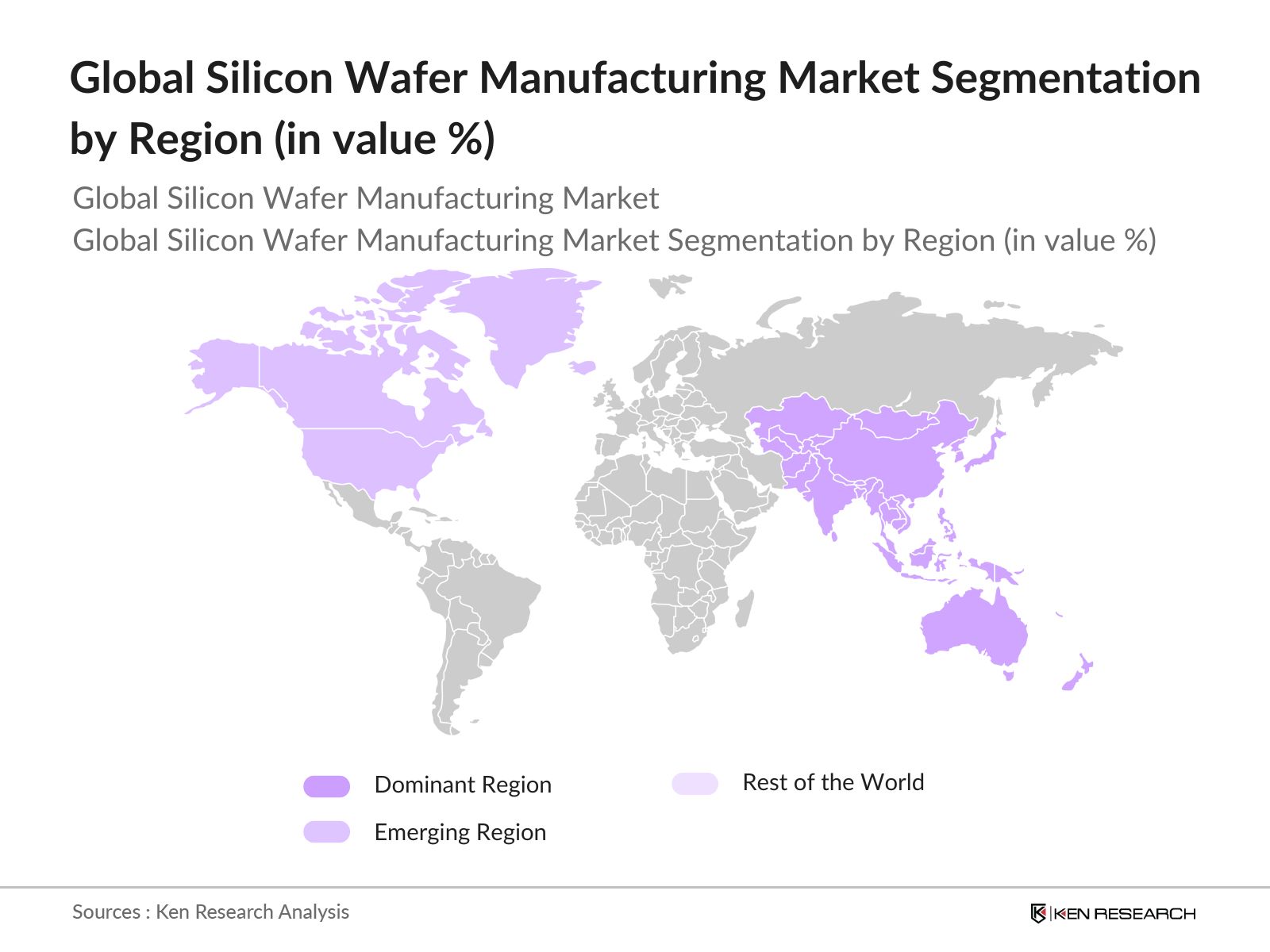

- By Region: The market is divided into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the market due to the presence of major semiconductor manufacturing hubs such as China, Taiwan, and South Korea. The regions strong industrial base and ongoing investments in new semiconductor fabrication plants make it the largest consumer and producer of silicon wafers. North America remains a significant player, driven by the presence of key technology companies and government initiatives to bolster domestic semiconductor production.

Global Silicon Wafer Manufacturing Market Competitive Landscape

The global silicon wafer manufacturing market is highly competitive, with major players investing in advanced technologies to improve wafer production efficiency and quality. Key manufacturers are focusing on expanding their production capacities and developing larger wafer sizes to meet the growing demand from the semiconductor industry. Many companies are also entering into strategic partnerships with semiconductor firms to ensure a steady supply of silicon wafers and to align their offerings with the latest technological advancements.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Market Presence |

R&D Investment |

Global Reach |

Product Portfolio |

Certifications |

|

Shin-Etsu Chemical |

1926 |

Tokyo, Japan |

||||||

|

SUMCO Corporation |

1999 |

Tokyo, Japan |

||||||

|

GlobalWafers Co., Ltd |

1981 |

Hsinchu, Taiwan |

||||||

|

Siltronic AG |

1968 |

Munich, Germany |

||||||

|

Wafer Works Corp |

1997 |

Taoyuan, Taiwan |

Global Silicon Wafer Manufacturing Market Analysis

Growth Drivers

- Demand for Advanced Semiconductors: The global demand for semiconductors, driven by applications in AI, IoT, and 5G technologies, is a key growth driver for silicon wafer manufacturing. In 2024, AI-based systems like smart devices and autonomous vehicles are projected to use over 70 billion semiconductor units annually, significantly boosting silicon wafer demand. The rapid adoption of 5G networks globally, with more than 1.8 billion connections by the end of 2024, is further increasing semiconductor requirements. Silicon wafers, the primary material for integrated circuits in AI and IoT devices, are vital in supporting this growing demand.

- Expansion of Electric Vehicles and Renewable Energy: The rise of electric vehicles (EVs) and renewable energy sources is significantly contributing to the demand for silicon wafers, especially for power electronics and solar cells. In 2024, the International Energy Agency (IEA) estimates that over 17 million electric cars will be sold globally, each containing critical semiconductor components made from silicon wafers. Solar energy is also growing rapidly, with over 593 GW of installed photovoltaic capacity expected in 2024. These sectors heavily rely on silicon wafers for high-performance, energy-efficient solutions.

- Government Initiatives to Boost Semiconductor Manufacturing: Government incentives are a significant driver for the silicon wafer market, particularly with policies like the U.S. CHIPS Act, which allocates over USD 52 billion in funding to bolster domestic semiconductor manufacturing. Similarly, China's National Integrated Circuit Industry Plan, with $150 billion earmarked for semiconductor self-reliance, aims to reduce dependency on foreign technology. These initiatives have led to the establishment of new fabrication plants, increasing the demand for silicon wafers in both the U.S. and China. This regulatory support will continue shaping the growth trajectory of the global wafer industry.

Market Challenges

- High Capital Investment and Manufacturing Costs: The silicon wafer manufacturing industry faces significant capital investment challenges, particularly in the development of new semiconductor fabrication plants. Advanced equipment, such as EUV lithography machines, required for cutting-edge wafer production, further adds to the financial burden. This high capital expenditure creates barriers for smaller companies, limiting their ability to enter the market and scale production. Even with government incentives aimed at boosting domestic semiconductor manufacturing, the financial hurdles remain a significant challenge for companies aiming to expand wafer manufacturing capabilities.

- Supply Chain Disruptions: Supply chain disruptions, particularly in sourcing critical raw materials such as high-purity silicon, pose a significant challenge for the silicon wafer manufacturing industry. In 2024, geopolitical tensions and export restrictions in key silicon-producing countries have led to raw material shortages, resulting in delays and increased production costs. For instance, disruptions in Ukraine, a major supplier of rare gases used in semiconductor manufacturing, have exacerbated the global shortage of neon gas, further affecting wafer production.

Global Silicon Wafer Manufacturing Market Future Outlook

The global silicon wafer manufacturing market is expected to experience continued growth through 2028, driven by advancements in semiconductor technology and increasing demand from the automotive, consumer electronics, and renewable energy sectors. Governments will continue to support the growth of local manufacturing industries, and manufacturers will focus on developing larger wafer sizes and improving production efficiency to meet rising demand.

Future Market Opportunities

- Expansion of AI and IoT Technologies: The global expansion of AI and IoT technologies presents a significant opportunity for the silicon wafer manufacturing market. In 2024, the number of connected IoT devices is expected to exceed 18.8 billion, driving the need for advanced semiconductors. Smart devices, data centres, and edge computing systems increasingly rely on silicon wafers to power complex AI algorithms and enhance real-time data processing capabilities. This surge in demand creates lucrative opportunities for silicon wafer manufacturers to cater to the growing AI and IoT ecosystems.

- Growth in Renewable Energy Sector: The renewable energy sector, particularly solar photovoltaic (PV) systems, offers significant growth opportunities for silicon wafer manufacturers. In 2024, the global solar energy capacity is forecast to reach 593 GW, with PV systems accounting for a substantial portion of this growth. Silicon wafers are the primary material used in solar cells, and as countries accelerate their renewable energy transition, the demand for solar-grade wafers will rise accordingly. This trend opens up new avenues for wafer producers to expand their market share in the renewable energy sector.

Scope of the Report

|

By Wafer Size |

200mm 300mm 450mm |

|

By Application |

Semiconductors Consumer Electronics Automotive Renewable Energy |

|

By Technology |

Lithography Etching Deposition Doping |

|

By End-User |

Integrated Device Manufacturers (IDMs) Foundries, OEMs Research Institutes |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Silicon Wafer Manufacturers

Semiconductor OEMs and Foundries

Electric Vehicle Manufacturers

Solar Energy Companies

Consumer Electronics Producers

Government and Regulatory Bodies (U.S. CHIPS Act, European Union Chips Act)

Investors and Venture Capitalist Firms

Automotive Industry Leaders

Banks and Financial Institutions

Companies

Major Players Mentioned in the Report

Shin-Etsu Chemical Co., Ltd.

SUMCO Corporation

GlobalWafers Co., Ltd.

Siltronic AG

Wafer Works Corporation

Soitec S.A.

SK Siltron Co., Ltd.

Okmetic

Episil Technologies Inc.

MEMC Electronic Materials, Inc.

Zhonghuan Semiconductor

Electronics and Materials Corporation (EMC)

LD Microelectronics Co., Ltd.

WaferPro

China Silicon Corporation

Table of Contents

1. Global Silicon Wafer Manufacturing Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy (Silicon Wafer Applications, Wafer Types, End-Users)

1.3. Market Growth Rate (Wafer Production Efficiency, Demand Trends)

1.4. Market Segmentation Overview

2. Global Silicon Wafer Manufacturing Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Demand for Semiconductors, Consumer Electronics, Automotive Demand)

2.3. Key Market Developments and Milestones (Wafer Size Transitions, Technological Milestones)

3. Global Silicon Wafer Manufacturing Market Analysis

3.1. Growth Drivers

3.1.1. Demand for Advanced Semiconductors (AI, IoT, 5G)

3.1.2. Expansion of Electric Vehicles and Renewable Energy (Power Electronics, Solar Cells)

3.1.3. Technological Advancements in Wafer Fabrication (450mm Wafers, Lithography)

3.1.4. Government Incentives for Semiconductor Manufacturing (U.S. CHIPS Act, Chinas Semiconductor Self-Reliance)

3.2. Market Challenges

3.2.1. High Capital Investment in Wafer Production (Machinery Costs, Facility Development)

3.2.2. Supply Chain Disruptions (Raw Material Shortages, Geopolitical Issues)

3.2.3. Competition from Alternative Materials (Gallium Nitride, Silicon Carbide)

3.2.4. Technological Complexity in Larger Wafer Production (450mm Technology Barriers)

3.3. Opportunities

3.3.1. Expansion of AI and IoT Technologies (Smart Devices, Data Centers)

3.3.2. Growth in Renewable Energy Sector (Solar Photovoltaic Systems)

3.3.3. Collaborative Innovations (Partnerships Between Semiconductor Manufacturers and Wafer Producers)

3.3.4. Increasing Demand for Power Semiconductors (Energy Efficiency, Electric Vehicles)

3.4. Trends

3.4.1. Transition from 200mm to 300mm and 450mm Wafer Sizes

3.4.2. Adoption of Advanced Lithography Techniques (EUV, DUV)

3.4.3. Integration of AI in Wafer Production Processes (Automation, Quality Control)

3.4.4. Regional Shifts in Wafer Production (Rise of APAC, Expansion in Europe)

3.5. Government Regulation

3.5.1. U.S. CHIPS Act

3.5.2. Chinas National Integrated Circuit Industry Plan

3.5.3. European Chips Act

3.5.4. Environmental Regulations Impacting Wafer Production (Energy Consumption, Waste Management)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Wafer Producers, Semiconductor Companies, Raw Material Suppliers, Equipment Manufacturers)

3.8. Porters Five Forces (Bargaining Power of Buyers, Suppliers, Threat of Substitutes, New Entrants, Industry Rivalry)

3.9. Competition Ecosystem

4. Global Silicon Wafer Manufacturing Market Segmentation

4.1. By Wafer Size (In Value %)

4.1.1. 200mm

4.1.2. 300mm

4.1.3. 450mm

4.2. By Application (In Value %)

4.2.1. Semiconductors

4.2.2. Consumer Electronics

4.2.3. Automotive

4.2.4. Renewable Energy

4.3. By Technology (In Value %)

4.3.1. Lithography

4.3.2. Etching

4.3.3. Deposition

4.3.4. Doping

4.4. By End-User (In Value %)

4.4.1. Integrated Device Manufacturers (IDMs)

4.4.2. Foundries

4.4.3. OEMs (Original Equipment Manufacturers)

4.4.4. Research Institutes

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Silicon Wafer Manufacturing Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Shin-Etsu Chemical Co., Ltd.

5.1.2. SUMCO Corporation

5.1.3. GlobalWafers Co., Ltd.

5.1.4. Siltronic AG

5.1.5. Wafer Works Corporation

5.1.6. Soitec S.A.

5.1.7. SK Siltron Co., Ltd.

5.1.8. Okmetic

5.1.9. Episil Technologies Inc.

5.1.10. LD Microelectronics Co., Ltd.

5.1.11. WaferPro

5.1.12. Electronics and Materials Corporation (EMC)

5.1.13. MEMC Electronic Materials, Inc.

5.1.14. Zhonghuan Semiconductor

5.1.15. China Silicon Corporation

5.2. Cross Comparison Parameters (Wafer Capacity, Fab Locations, Technology Portfolio, Revenue Distribution, Employee Count, Wafer Size Production, R&D Investment, Market Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global Silicon Wafer Manufacturing Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes (ISO Standards, Safety Regulations, Industry Certifications)

7. Global Silicon Wafer Manufacturing Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Advanced Wafer Technologies, Increased Semiconductor Demand, Electric Vehicle Growth)

8. Global Silicon Wafer Manufacturing Future Market Segmentation

8.1. By Wafer Size (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. Global Silicon Wafer Manufacturing Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first step involves identifying the major stakeholders in the global silicon wafer manufacturing market. This includes extensive desk research from secondary sources and proprietary databases to gather detailed information about wafer production and its applications across multiple industries. Key variables influencing the market, such as raw material costs, production technologies, and supply chain dynamics, are defined.

Step 2: Market Analysis and Construction

In this phase, historical market data is compiled and analyzed to assess the markets growth trajectory. This includes examining wafer production volumes, industry demand across sectors like semiconductors, and the impact of government initiatives on manufacturing capacities. The market analysis also covers production efficiency trends and geographical market penetration.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are tested through expert consultations with industry professionals. Interviews are conducted with executives from major silicon wafer manufacturers and semiconductor firms to validate production trends, wafer quality improvements, and supply chain developments. This provides a more accurate representation of market performance and growth drivers.

Step 4: Research Synthesis and Final Output

The final stage involves synthesizing research data and consulting multiple industry sources to verify trends in wafer size transitions, manufacturing technologies, and market demand. The research output presents a comprehensive and validated analysis of the global silicon wafer manufacturing market, ensuring reliability in market estimates.

Frequently Asked Questions

01. How big is the global silicon wafer manufacturing market?

The global silicon wafer manufacturing market was valued at USD 16 billion, driven by increasing demand from the semiconductor, automotive, and renewable energy sectors.

02. What are the challenges in the global silicon wafer manufacturing market?

Challenges in the global silicon wafer manufacturing market include high capital investment costs for advanced wafer production, supply chain disruptions due to geopolitical tensions, and competition from alternative materials like gallium nitride.

03. Who are the major players in the global silicon wafer manufacturing market?

Key players in the global silicon wafer manufacturing market include Shin-Etsu Chemical, SUMCO Corporation, GlobalWafers Co., Ltd., Siltronic AG, and Wafer Works Corporation. These companies dominate through technological innovation, extensive production capacities, and strategic partnerships with semiconductor manufacturers.

04. What are the growth drivers of the global silicon wafer manufacturing market?

Growth drivers in the global silicon wafer manufacturing market include increasing demand for semiconductors in 5G applications, AI, and IoT devices, as well as rising adoption of electric vehicles and solar photovoltaic systems, which rely on advanced silicon wafers for production.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.