Global Stem Cell Therapy Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD7636

December 2024

97

About the Report

Global Stem Cell Therapy Market Overview

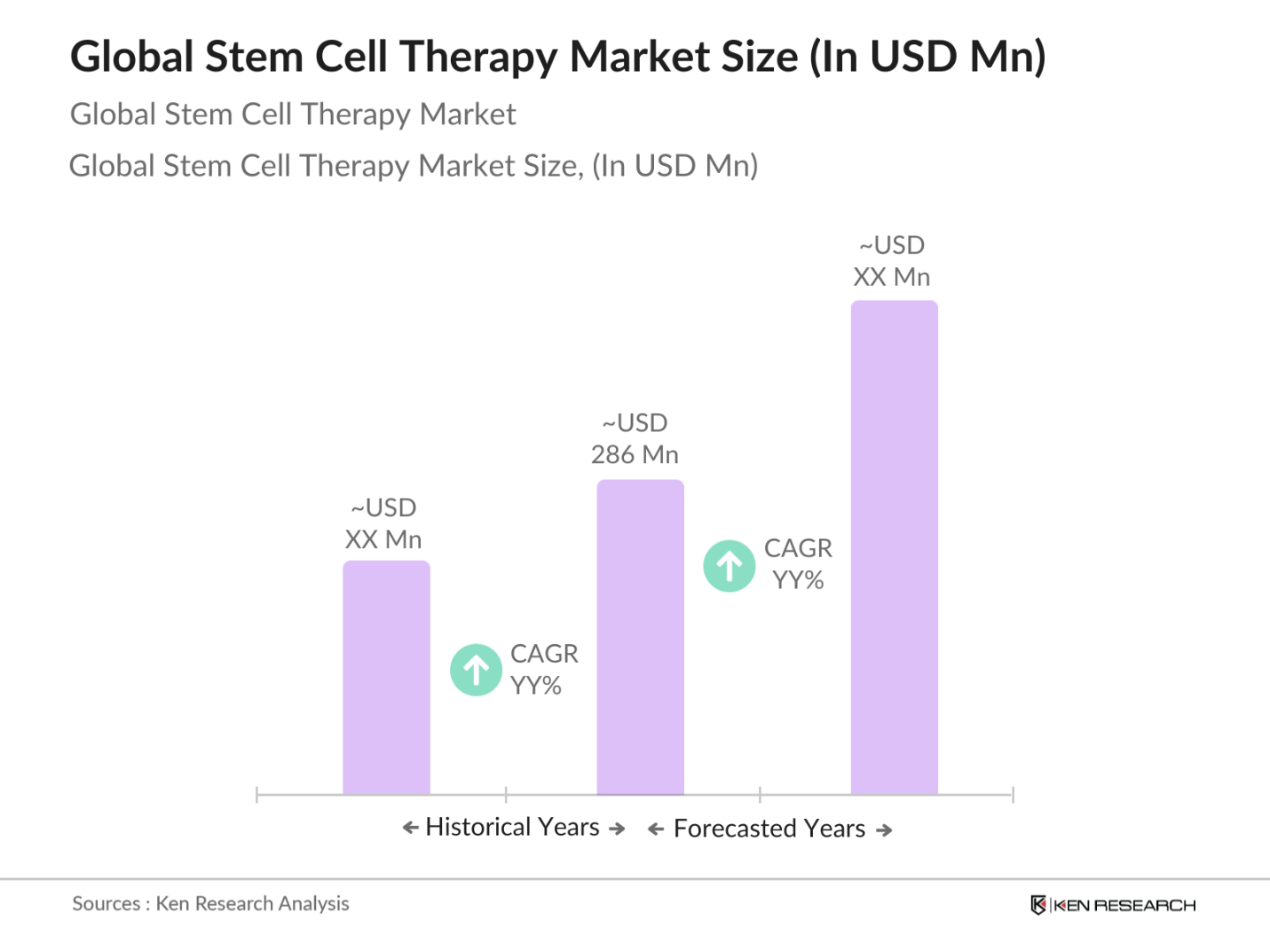

- The global stem cell therapy market is valued at USD 286 million, driven by increasing advancements in regenerative medicine and rising investments in cell-based research. This market is primarily fueled by the growing demand for therapies to treat chronic diseases such as cancer, neurological disorders, and cardiovascular diseases. With an increasing number of clinical trials, advancements in personalized medicine, and supportive government regulations, the market is witnessing steady growth across various applications and geographies.

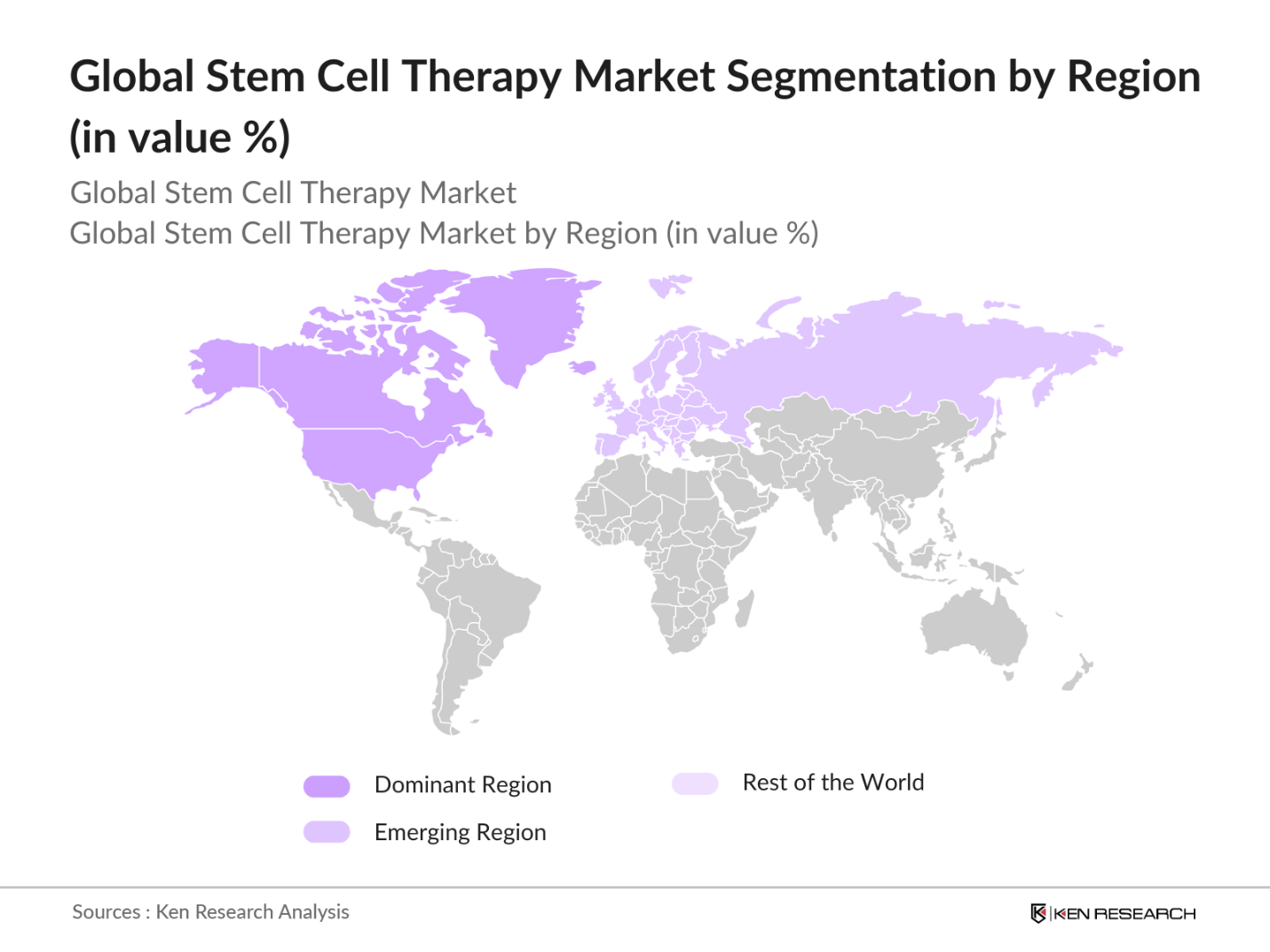

- North America dominates the global stem cell therapy market due to its well-established healthcare infrastructure, high research and development investments, and the presence of key players in the region. Countries such as the United States are major contributors, thanks to their advanced technological capabilities and large patient base seeking novel treatment options. Additionally, countries in Europe and Asia-Pacific, like Germany and Japan, are rising in prominence due to strong government support for biotech research and growing awareness regarding stem cell applications.

- The European Medicines Agency (EMA) enforces strict directives for stem cell-based therapies, particularly for autologous treatments. As of 2024, the EMA had approved 15 advanced therapy medicinal products (ATMPs), including stem cell-based treatments for rare diseases. The EMAs focus on maintaining rigorous safety standards while promoting innovation through the Priority Medicines (PRIME) scheme has positioned Europe as a leader in the global stem cell therapy market.

Global Stem Cell Therapy Market Segmentation

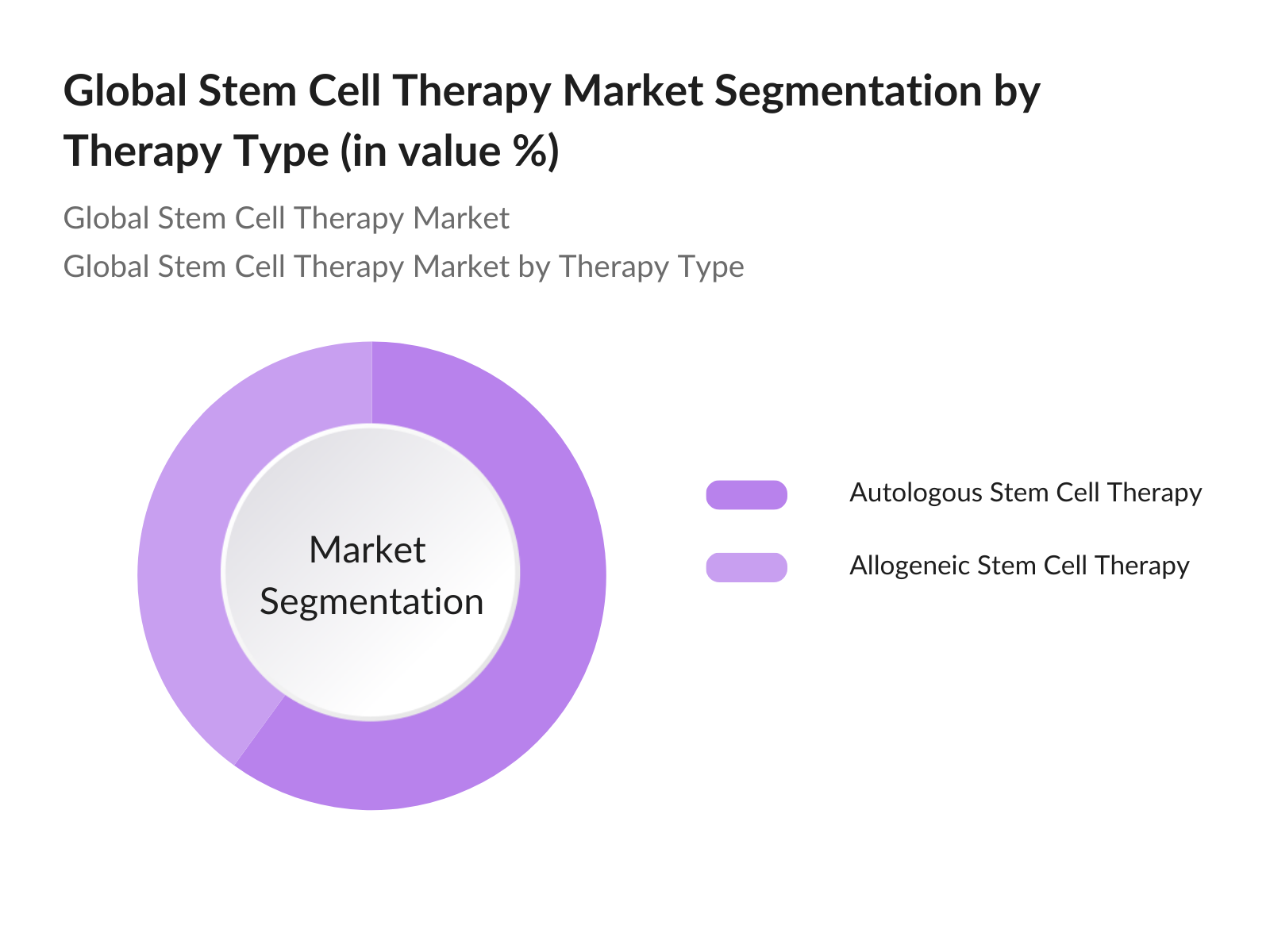

By Therapy Type: The global stem cell therapy market is segmented by therapy type into Autologous Stem Cell Therapy and Allogeneic Stem Cell Therapy. Autologous stem cell therapy holds a dominant market share due to its lower risk of immune rejection and fewer ethical concerns. This segment's popularity is driven by advancements in personalized treatments and its applications in treating various autoimmune and blood disorders. The growing trend of personalized healthcare, where cells from a patient's body are used for treatment, ensures the continued dominance of autologous therapies in the market.

By Region: The global stem cell therapy market due to its advanced healthcare infrastructure and high investments in stem cell research. The Asia-Pacific region is emerging as a strong competitor, particularly due to increasing government support in countries like Japan and China, where regenerative medicine is gaining attention. Europe also has a significant share, driven by favorable regulatory environments and a growing number of clinical trials.

Global Stem Cell Therapy Market Competitive Landscape

The global stem cell therapy market is dominated by several key players, including both established biotech companies and emerging firms specializing in regenerative medicine. These players are constantly innovating and expanding their product portfolios to remain competitive.

|

Company Name |

Establishment Year |

Headquarters |

R&D Investments |

Clinical Trial Pipeline |

Product Portfolio |

FDA Approvals |

Manufacturing Capabilities |

Strategic Alliances |

|

Mesoblast Ltd |

2004 |

Australia |

High |

|||||

|

Athersys, Inc. |

1995 |

USA |

Medium |

|||||

|

Pluristem Therapeutics |

2001 |

Israel |

High |

|||||

|

Lonza Group |

1897 |

Switzerland |

High |

|||||

|

Vericel Corporation |

1989 |

USA |

Medium |

Global Stem Cell Therapy Market Analysis

Market Growth Drivers:

- Increasing Prevalence of Chronic Diseases (Therapeutic Applications): The growing burden of chronic diseases such as diabetes, heart diseases, and neurological disorders is significantly driving the demand for stem cell therapies globally. According to the World Health Organization (WHO), over 422 million people suffer from diabetes worldwide, contributing to increased demand for regenerative treatments like stem cell therapy. Furthermore, cardiovascular diseases are the leading cause of death globally, with an estimated 17.9 million deaths annually as of 2022. This escalating prevalence directly impacts the demand for stem cell-based therapies that can address degenerative conditions, pushing the market forward.

- Rising Government and Private Funding (Research & Development): Government and private funding initiatives for stem cell research have surged in recent years, contributing to the expansion of therapeutic applications. The U.S. government alone allocated over $1.5 billion for stem cell research in 2022, according to the National Institutes of Health (NIH). Similarly, the European Commission invested 400 million for stem cell innovation as part of Horizon Europe. These substantial financial commitments foster advancements in stem cell research, promoting innovation and improving patient outcomes in regenerative medicine.

- Technological Advancements in Cell Engineering (Product Innovation): Technological innovations in cell engineering, including CRISPR-Cas9 and induced pluripotent stem cells (iPSCs), are revolutionizing the stem cell therapy landscape. The International Society for Stem Cell Research (ISSCR) highlights that gene-editing technologies like CRISPR have enabled scientists to manipulate stem cells with unprecedented precision, reducing the likelihood of rejection in allogeneic transplants. This advancement, coupled with biomanufacturing capabilities, has significantly boosted the scalability of stem cell production, ensuring more accessible therapies for chronic disease treatment.

Market Challenges:

- Regulatory Barriers (Approval Processes): The approval process for stem cell therapies remains a critical challenge, with stringent regulatory frameworks impeding market growth. The U.S. Food and Drug Administration (FDA) reported that only 23 stem cell-based therapies had been approved for clinical use by 2024, reflecting the complexity of meeting safety and efficacy standards. Moreover, regulatory bodies in Asia, like the Japan PMDA, have enacted even stricter guidelines, slowing down commercialization. These regulatory challenges create hurdles for market entry, particularly for smaller biotech firms.

- High Cost of Treatment (Cost Analysis): The high cost of stem cell therapies remains prohibitive for widespread adoption. In the U.S., stem cell transplants cost between $350,000 and $800,000 per patient, depending on the type of treatment and underlying condition, as reported by the American Society of Hematology. This pricing presents a significant barrier, particularly in emerging markets where healthcare budgets are limited. The lack of insurance coverage for experimental treatments further exacerbates this issue, restricting access to stem cell therapies.

Global Stem Cell Therapy Market Future Outlook

Over the next five years, the global stem cell therapy market is poised for significant growth, driven by continuous government support, advancements in cell therapy technologies, and increasing consumer demand for novel treatments. Innovations in personalized medicine, along with rising applications in chronic diseases like cancer, cardiovascular, and neurological disorders, will continue to fuel market expansion. Countries like Japan and China are expected to gain market share, while North America maintains its dominance through consistent research and development efforts.

Market Opportunities:

- Emerging Markets (Geographical Penetration): Emerging markets such as India and Brazil are witnessing increased demand for stem cell therapies due to growing healthcare infrastructure and supportive government policies. Indias Biotechnology Industry Research Assistance Council (BIRAC) reported an 80% increase in stem cell clinical trials in 2023, with substantial government support through initiatives like the National Biopharma Mission. Similarly, Brazil's Ministry of Health has allocated R$200 million to regenerative medicine, making the country a key player in Latin America for stem cell research and commercialization.

- Expansion of Therapeutic Applications (Regenerative Medicine): The scope of stem cell therapies is rapidly expanding beyond traditional applications such as hematology and oncology into new areas like neurology and orthopedics. According to the European Society for Cell and Gene Therapy, over 50 clinical trials are underway investigating the use of stem cells in treating neurodegenerative disorders like Parkinson's disease and multiple sclerosis. This expansion is creating new revenue streams for companies investing in the development of stem cell-based regenerative therapies.

Scope of the Report

|

By Therapy Type |

Autologous Allogeneic |

|

By Application |

Oncology Neurology Cardiovascular Musculoskeletal Others |

|

By Source |

Embryonic Adult iPSCs Cord Blood |

|

By End-User |

Hospitals Research Institutes Biotech Companies |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Hospitals and Healthcare Providers

Pharmaceutical and Biotech Companies

Contract Research Organizations (CROs)

Government and Regulatory Bodies (FDA, EMA, PMDA)

Investments and Venture Capitalist Firms

Stem Cell Research Institutes

Medical Device Manufacturers

Public and Private Healthcare Funding Organizations

Companies

Players Mention in the Report

Mesoblast Ltd

Athersys, Inc.

Pluristem Therapeutics

Lonza Group

Vericel Corporation

Stemcell Technologies

Cytori Therapeutics

BrainStorm Cell Therapeutics

Osiris Therapeutics

BioTime Inc.

Gamida Cell

TiGenix NV

MEDIPOST

Thermo Fisher Scientific

Cellular Biomedicine Group

Table of Contents

01. Global Stem Cell Therapy Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Market Penetration, Adoption Rates)

1.4. Market Segmentation Overview

02. Global Stem Cell Therapy Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Clinical Trials, FDA Approvals)

03. Global Stem Cell Therapy Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Prevalence of Chronic Diseases (Therapeutic Applications)

3.1.2. Rising Government and Private Funding (Research & Development)

3.1.3. Technological Advancements in Cell Engineering (Product Innovation)

3.2. Market Challenges

3.2.1. Regulatory Barriers (Approval Processes)

3.2.2. High Cost of Treatment (Cost Analysis)

3.2.3. Ethical Concerns and Public Perception (Ethical Framework)

3.3. Opportunities

3.3.1. Emerging Markets (Geographical Penetration)

3.3.2. Expansion of Therapeutic Applications (Regenerative Medicine)

3.3.3. Collaborations between Pharma and Biotech Firms (Strategic Partnerships)

3.4. Trends

3.4.1. Development of Allogeneic Stem Cell Therapies (Product Diversification)

3.4.2. Increasing Focus on Personalized Medicine (Precision Medicine)

3.4.3. Growing Use of Stem Cells in Clinical Trials (Clinical Advancement)

3.5. Regulatory Environment

3.5.1. FDA Guidelines for Stem Cell Therapies (Regulatory Compliance)

3.5.2. EMA Directives (European Market Approvals)

3.5.3. Global Harmonization Initiatives (Standardization)

3.6. SWOT Analysis

3.7. Porters Five Forces Analysis

3.8. Stakeholder Ecosystem (Key Stakeholders, Research Institutes)

3.9. Competition Ecosystem

04. Global Stem Cell Therapy Market Segmentation

4.1. By Therapy Type (In Value %)

4.1.1. Autologous Stem Cell Therapy

4.1.2. Allogeneic Stem Cell Therapy

4.2. By Application (In Value %)

4.2.1. Oncology

4.2.2. Neurology

4.2.3. Cardiovascular Disorders

4.2.4. Musculoskeletal Disorders

4.2.5. Other Applications

4.3. By Source (In Value %)

4.3.1. Embryonic Stem Cells

4.3.2. Adult Stem Cells

4.3.3. Induced Pluripotent Stem Cells (iPSCs)

4.3.4. Cord Blood Stem Cells

4.4. By End User (In Value %)

4.4.1. Hospitals

4.4.2. Research Institutes

4.4.3. Biotech Companies

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

05. Global Stem Cell Therapy Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Mesoblast Ltd

5.1.2. Athersys, Inc.

5.1.3. Pluristem Therapeutics

5.1.4. Thermo Fisher Scientific

5.1.5. Cytori Therapeutics

5.1.6. Lonza Group

5.1.7. Cellular Biomedicine Group

5.1.8. Vericel Corporation

5.1.9. Stemcell Technologies

5.1.10. BrainStorm Cell Therapeutics

5.1.11. Osiris Therapeutics

5.1.12. BioTime Inc.

5.1.13. Gamida Cell

5.1.14. TiGenix NV

5.1.15. MEDIPOST

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Clinical Trial Pipeline, R&D Investments, Strategic Alliances, Manufacturing Capabilities, Market Reach, FDA Approvals)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Collaborations, Partnerships, Mergers)

5.5. Mergers and Acquisitions (Investment Focus)

5.6. Investment Analysis (Venture Capital, Private Equity)

5.7. Government Grants and Funding

5.8. Intellectual Property Landscape (Patents, Licensing)

06. Global Stem Cell Therapy Market Regulatory Framework

6.1. Regulatory Landscape (FDA, EMA, Japans PMDA)

6.2. Compliance Requirements (Good Manufacturing Practices)

6.3. Certification Processes (Approval Pathways)

07. Global Stem Cell Therapy Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Technological Advancements, Adoption Rates)

08. Global Stem Cell Therapy Future Market Segmentation

8.1. By Therapy Type (In Value %)

8.2. By Application (In Value %)

8.3. By Source (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

09. Global Stem Cell Therapy Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Analysis

9.3. Product Positioning Strategy

9.4. Key Market Entry Barriers

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first step involved creating a comprehensive market map encompassing all the major stakeholders in the global stem cell therapy market. This step was carried out using secondary data sources, including industry reports, company publications, and public databases, to understand the critical variables influencing the market.

Step 2: Market Analysis and Construction

This phase focused on compiling historical data and analyzing trends within the stem cell therapy market, focusing on factors like market penetration, technological advancements, and clinical trial activity. The data gathered was used to generate accurate estimates for market size and growth potential.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses related to market growth, technological developments, and demand dynamics were validated through consultations with industry experts. These experts were contacted via telephonic interviews, and their insights were critical in validating the research findings.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing all collected data and insights to create a cohesive market report. This step also included data triangulation, combining primary and secondary data sources to ensure the accuracy and comprehensiveness of the findings.

Frequently Asked Questions

01. How big is the global stem cell therapy market?

The global stem cell therapy market is valued at USD 286 million, driven by advancements in regenerative medicine and increasing investments in research and clinical trials.

02. What are the challenges in the stem cell therapy market?

Challenges include regulatory hurdles, high costs of treatment, and ethical concerns regarding the use of stem cells. Moreover, ensuring the safety and efficacy of stem cell therapies remains a significant concern.

03. Who are the major players in the global stem cell therapy market?

Key players in the market include Mesoblast Ltd, Athersys, Inc., Lonza Group, Pluristem Therapeutics, and Vericel Corporation. These companies dominate due to their extensive R&D investments, strong product pipelines, and strategic partnerships.

04. What are the growth drivers of the stem cell therapy market?

Growth is driven by the increasing prevalence of chronic diseases, advancements in cell engineering technologies, and growing government support for regenerative medicine research.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.