Global Underground Mining Market Outlook to 2030

Region:Global

Author(s):Shreya Garg

Product Code:KROD9708

December 2024

82

About the Report

Global Underground Mining Market Overview

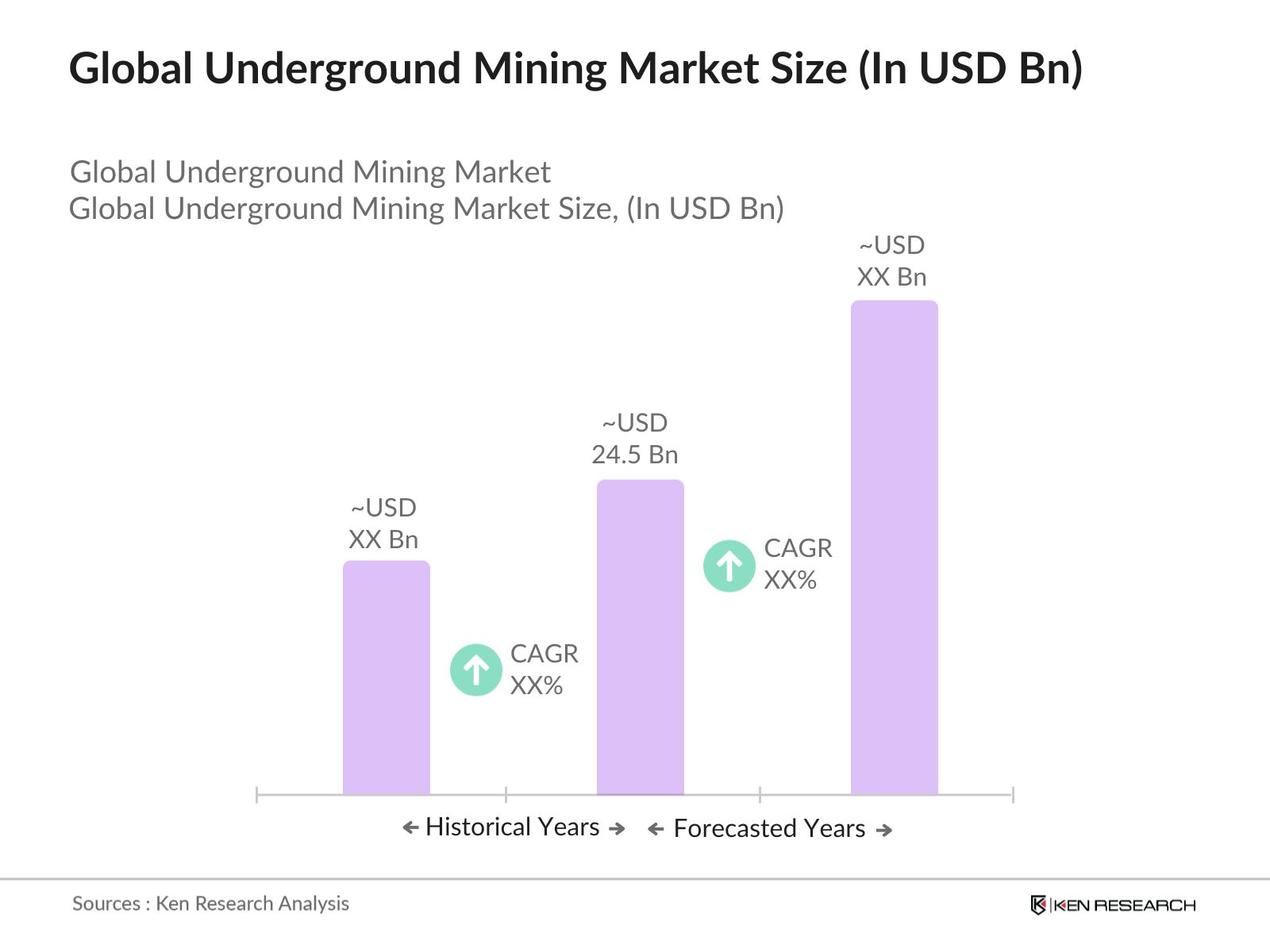

- The Global Underground Mining Market is valued at approximately USD 24.5 billion, driven by increasing global demand for minerals such as gold, copper, and coal. The rise in urbanization, industrialization, and technological advancements in mining techniques have significantly contributed to market growth. As mining operations expand deeper, the demand for high-efficiency underground mining equipment has surged, further pushing the market forward. Government regulations aimed at improving worker safety and reducing environmental impact have also stimulated the adoption of advanced mining equipment.

- In terms of regional dominance, countries like China, Australia, and South Africa are at the forefront of the underground mining market. Chinas dominance stems from its vast mineral reserves and strong governmental support for infrastructure projects. Australia is notable for its highly developed mining sector and its significant investment in automation technologies. South Africa remains a leader due to its extensive gold and platinum deposits and long-standing mining history, supported by favorable policies and a skilled workforce.

- Environmental regulations targeting carbon emissions and waste management are becoming increasingly stringent. In 2023, the European Union introduced new guidelines for carbon capture and storage (CCS) in mining, aimed at reducing the sectors carbon footprint. These regulations are compelling mining companies to adopt new technologies and processes, influencing the demand for compliant underground mining equipment.

Global Underground Mining Market Segmentation

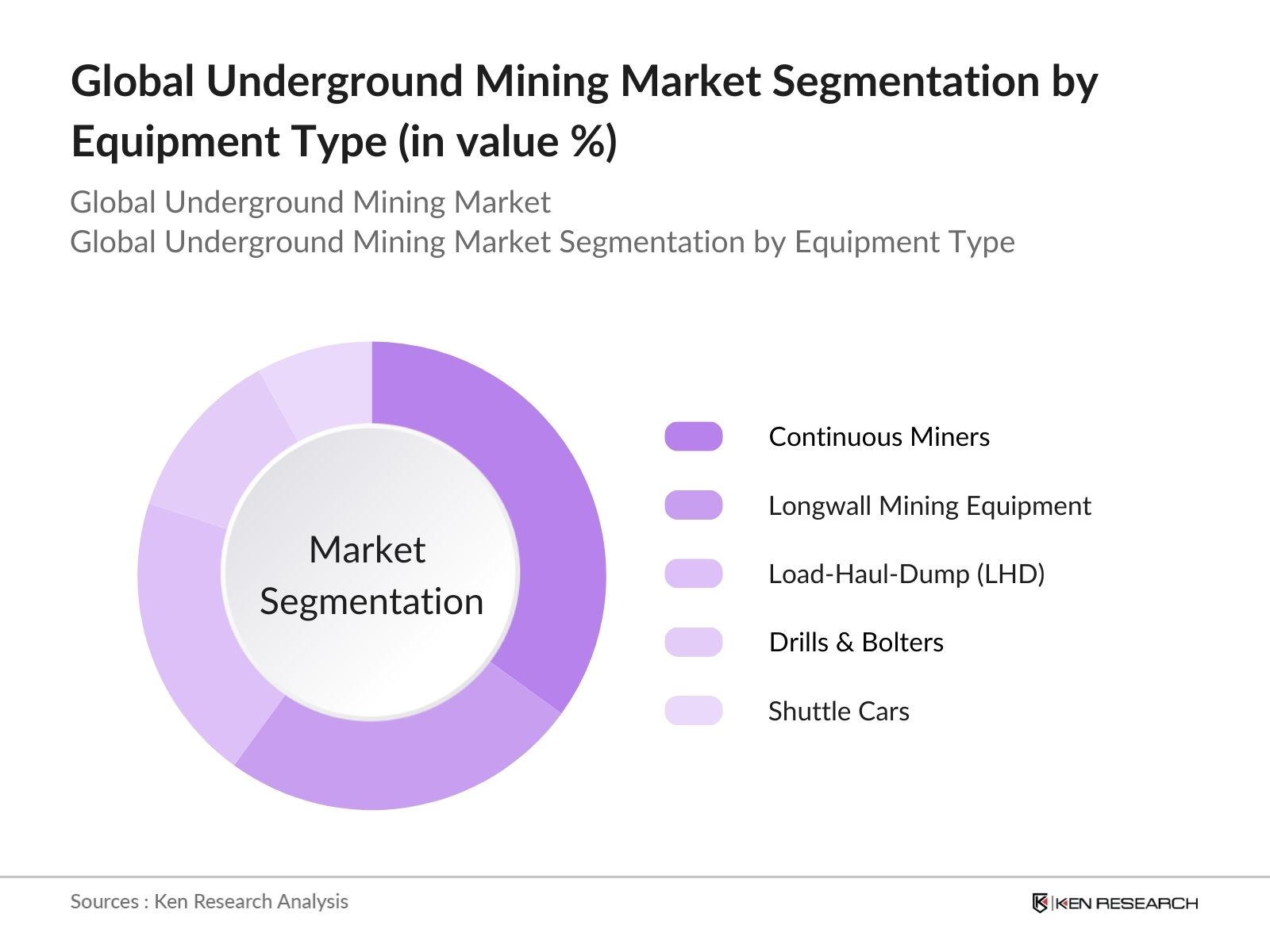

By Equipment Type: The market is segmented by equipment type into continuous miners, longwall mining equipment, load-haul-dump (LHD) machines, drills & bolters, and shuttle cars. Among these, continuous miners hold the dominant market share due to their efficiency in breaking and loading coal without the need for drilling and blasting. This equipment is particularly favored in coal mining operations where continuous, uninterrupted operations are critical for profitability. The ability of continuous miners to work seamlessly with conveyors adds to their dominance in the segment.

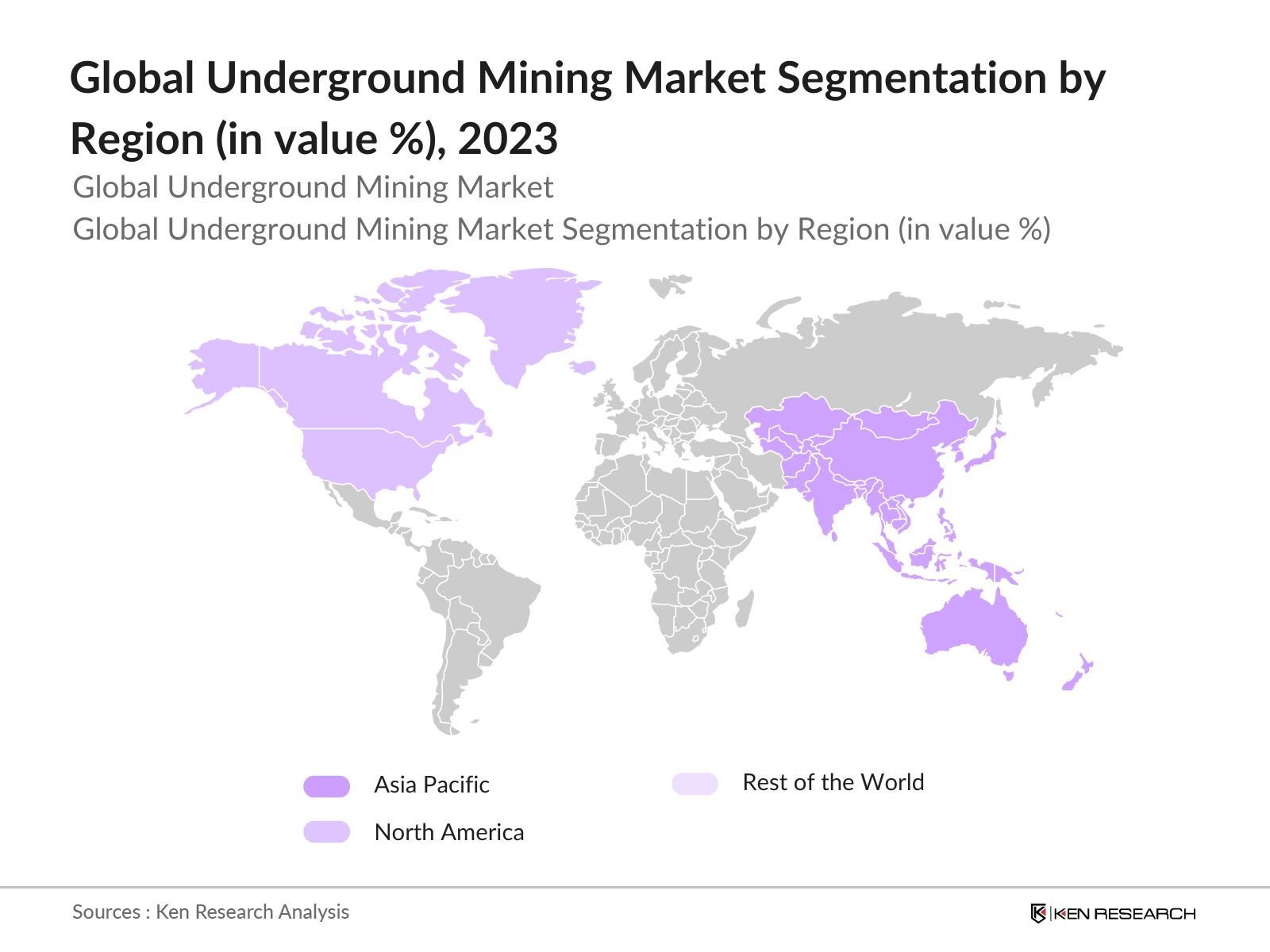

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the market, with China and Australia leading in terms of mining activity and equipment demand. This is due to the region's vast mineral resources, heavy investments in infrastructure projects, and strong governmental support for mining operations. Chinas focus on expanding its infrastructure and its role as the worlds leading producer of rare earth metals further supports the region's dominance.

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the market, with China and Australia leading in terms of mining activity and equipment demand. This is due to the region's vast mineral resources, heavy investments in infrastructure projects, and strong governmental support for mining operations. Chinas focus on expanding its infrastructure and its role as the worlds leading producer of rare earth metals further supports the region's dominance.

By Application: The market is segmented by application into coal mining, metal mining, mineral mining, and precious metal mining. Coal mining dominates the market primarily because coal remains a key source of energy in many regions, especially in countries like China, India, and the United States. Despite the global shift toward renewable energy, the demand for coal continues due to its use in power generation and steel production. Additionally, advancements in cleaner coal technologies have allowed for sustained demand in this segment.

Global Underground Mining Market Competitive Landscape

The Global Underground Mining Market is dominated by key players who are continuously innovating to stay competitive. Companies are focusing on automation, electrification, and hybrid solutions to reduce environmental impact and improve efficiency. The competitive landscape of the underground mining equipment market is marked by the presence of global giants like Caterpillar Inc., Komatsu Mining Corp., and Sandvik AB, all of which are investing heavily in automation technologies and R&D to stay ahead. These companies also benefit from a strong global presence and established relationships with major mining corporations.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

Employees |

Regional Presence |

R&D Investment |

Product Innovation |

Market Leadership |

|

Caterpillar Inc. |

1925 |

USA |

||||||

|

Komatsu Mining Corp. |

1921 |

Japan |

||||||

|

Sandvik AB |

1862 |

Sweden |

||||||

|

Epiroc AB |

2018 |

Sweden |

||||||

|

Hitachi Construction |

1951 |

Japan |

Global Underground Mining Equipment Industry Analysis

Growth Drivers

- Increasing Demand for Minerals: The global mining industry is experiencing increased demand for essential minerals such as copper, coal, and gold due to their growing application across multiple industries. In 2023, global copper production reached 21.6 million tons, driven by the expansion of electric vehicles and renewable energy sectors, both of which require substantial copper use. The rising need for coal, particularly in Asia-Pacific, also propels the underground mining equipment market, as China consumed 4.2 billion metric tons of coal in 2022. Gold mining remains steady with an annual output of around 3,500 tons, fueling equipment demand.

- Technological Advancements: The integration of advanced technologies like automation, the Internet of Things (IoT), and artificial intelligence (AI) in underground mining equipment has streamlined operations and reduced costs. In 2023, the global AI in mining market contributed $2.1 billion in efficiency gains by enabling real-time data monitoring and predictive maintenance, significantly improving machine uptime. The introduction of automated drilling machines and remotely operated equipment also decreased safety risks and downtime. For instance, Rio Tintos use of autonomous haulage systems has resulted in a 30% productivity increase.

- Environmental Regulations Driving Green Mining: Stringent environmental regulations across major mining economies, such as Australia and Canada, are pushing for greener mining practices. In 2023, the Canadian government implemented regulations that mandate a 40% reduction in mining emissions compared to 2005 levels, leading to increased demand for electric and hybrid underground mining equipment. Additionally, Australia introduced policies targeting a 43% reduction in carbon emissions by 2025, promoting the adoption of sustainable mining technologies. Government of Canada: Mining Regulations

Market Challenges

- High Capital Cost: Underground mining requires capital investment in machinery, infrastructure, and technology. The average cost to develop a new underground mine can exceed $1 billion, with ongoing maintenance and technology upgrades further increasing financial pressures. For example, the expansion of the Grasberg mine in Indonesia saw capital expenditures surpass $2.2 billion in 2023. High CAPEX can deter smaller companies from investing, limiting market entry.

- Fluctuating Commodity Prices: Commodity price volatility remains a significant challenge for the underground mining equipment market. In 2023, copper prices fluctuated between $7,000 and $9,000 per metric ton, influenced by global demand, geopolitical tensions, and supply chain disruptions. Similarly, gold prices oscillated between $1,800 and $2,000 per ounce, impacting investment in new equipment as companies hesitate during periods of price uncertainty. IMF: Commodity Prices Report

Global Underground Mining Market Future Outlook

Over the coming years, the Global Underground Mining Market is expected to show significant growth, driven by the continuous evolution of mining technologies, stricter environmental regulations, and the increasing depth of underground mining operations. The growing demand for minerals, particularly those critical for clean energy technologies (like lithium, cobalt, and nickel), will further drive demand for high-efficiency, low-emission underground mining equipment. Furthermore, increased investments in automation and electrification will shape the future of the industry, as companies aim to reduce operational costs and improve productivity.

Future Market Opportunities

- Emerging Markets: Emerging economies in Latin America, Africa, and Southeast Asia offer substantial opportunities for the underground mining equipment market. Peru, for example, produced 2.7 million tons of copper in 2022, while the Democratic Republic of Congo continues to dominate cobalt production. These regions are rapidly expanding mining activities to tap into their vast mineral reserves, with governments supporting infrastructure investment and equipment modernization, making them lucrative markets for mining equipment manufacturers.

- Technological Innovation: Technological advancements, particularly AI-driven data analytics and remote-controlled equipment, present significant opportunities for mining companies. In 2023, the adoption of hybrid power solutions increased by 15%, enabling mining operations to reduce energy consumption and carbon emissions. AI technologies used for resource mapping and predictive maintenance are helping companies enhance operational efficiency, particularly in remote and hazardous mining environments.

Scope of the Report

|

Equipment Type |

Continuous Miners Longwall Equipment LHD Machines Drills & Bolters Shuttle Cars |

|

Application |

Coal Mining Metal Mining Mineral Mining Precious Metal Mining |

|

Power Source |

Diesel-Powered Battery-Electric Hybrid |

|

Automation Level |

Manual Semi-Automated Fully Automated |

|

Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

OEMs (Original Equipment Manufacturers)

Mining Corporations

Government and Regulatory Bodies (e.g., U.S. Mine Safety and Health Administration, Australias Department of Industry, Science, Energy and Resources)

Energy and Utilities Companies

Mining Contractors

Investor and Venture Capitalist Firms

Environmental Agencies

Suppliers of Mining Technologies

Companies

Major Players

Komatsu Mining Corp.

Sandvik AB

Epiroc AB

Hitachi Construction

Atlas Copco

Liebherr Group

Boart Longyear

Joy Global

Volvo Construction Equipment

FLSmidth & Co. A/S

Doosan Infracore

JH Fletcher & Co.

SANY Group

BEML Limited

Table of Contents

1. Global Underground Mining Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (mining equipment utilization, production efficiency, and safety measures)

1.4. Market Segmentation Overview

2. Global Underground Mining Market Size (in USD Bn)

2.1. Historical Market Size (equipment demand, unit sales, and production volume)

2.2. Year-On-Year Growth Analysis (global mining output, capital expenditure trends)

2.3. Key Market Developments and Milestones (automation, new technologies, regulations)

3. Global Underground Mining Market Analysis

3.1. Growth Drivers

3.1.1. Increasing demand for minerals (copper, coal, gold)

3.1.2. Technological advancements (automated equipment, IoT, AI integration)

3.1.3. Environmental regulations driving green mining equipment

3.1.4. Growth in the electric vehicle (EV) industry and battery metals mining

3.2. Market Challenges

3.2.1. High capital costs (CAPEX)

3.2.2. Fluctuating commodity prices

3.2.3. Environmental sustainability issues (carbon footprint, land use)

3.2.4. Scarcity of skilled labor

3.3. Opportunities

3.3.1. Emerging markets (Latin America, Africa, Southeast Asia)

3.3.2. Technological innovation (AI, remote control, hybrid power solutions)

3.3.3. Government incentives for clean mining technologies

3.4. Trends

3.4.1. Shift toward electric and hybrid mining equipment

3.4.2. Automation and remote-controlled operations

3.4.3. Sustainability initiatives and emission-reducing technologies

3.4.4. Demand for smaller, more versatile equipment

3.5. Government Regulations

3.5.1. National mining policies (e.g., China, Australia, Canada)

3.5.2. Environmental regulations (carbon emissions, waste management)

3.5.3. Worker safety standards (mining safety regulations and equipment)

3.5.4. Renewable energy mandates for mining operations

3.6. SWOT Analysis (mining productivity, competitive pressure, environmental compliance)

3.7. Stakeholder Ecosystem (OEMs, mining corporations, governments, NGOs)

3.8. Porters Five Forces (market power of suppliers, industry competition, barriers to entry)

3.9. Competition Ecosystem (global and regional competitors, industry consolidation)

4. Global Underground Mining Market Segmentation

4.1. By Equipment Type (in Value %)

4.1.1. Continuous Miners

4.1.2. Longwall Mining Equipment

4.1.3. Load-Haul-Dump (LHD) Machines

4.1.4. Drills & Bolters

4.1.5. Shuttle Cars

4.2. By Application (in Value %)

4.2.1. Coal Mining

4.2.2. Metal Mining

4.2.3. Mineral Mining

4.2.4. Precious Metal Mining

4.3. By Power Source (in Value %)

4.3.1. Diesel-Powered Equipment

4.3.2. Battery-Electric Equipment

4.3.3. Hybrid Equipment

4.4. By Automation Level (in Value %)

4.4.1. Manual Operations

4.4.2. Semi-Automated Equipment

4.4.3. Fully Automated Equipment

4.5. By Region (in Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global Underground Mining Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Caterpillar Inc.

5.1.2. Komatsu Mining Corp.

5.1.3. Sandvik AB

5.1.4. Epiroc AB

5.1.5. Hitachi Construction Machinery

5.1.6. Atlas Copco

5.1.7. Liebherr Group

5.1.8. Boart Longyear

5.1.9. Joy Global

5.1.10. Volvo Construction Equipment

5.1.11. FLSmidth & Co. A/S

5.1.12. Doosan Infracore

5.1.13. JH Fletcher & Co.

5.1.14. SANY Group

5.1.15. BEML Limited

5.2. Cross Comparison Parameters

5.2.1. Market Capitalization

5.2.2. Production Capacity

5.2.3. Regional Presence

5.2.4. Product Diversification

5.2.5. Revenue from Mining Equipment

5.2.6. R&D Investment

5.2.7. Strategic Alliances

5.2.8. Technological Leadership

5.3. Market Share Analysis (OEMs, contract manufacturers)

5.4. Strategic Initiatives (expansion, partnerships, joint ventures)

5.5. Mergers and Acquisitions (industry consolidation)

5.6. Investment Analysis (venture capital, private equity)

5.7. Government Grants (grants for mining innovations)

5.8. Private Equity Investments (PE investments in mining equipment companies)

6. Global Underground Mining Market Regulatory Framework

6.1. Mining Standards and Certifications

6.2. Safety Compliance (worker safety regulations, equipment standards)

6.3. Emission Standards for Mining Equipment

6.4. Government Incentives for Energy-Efficient Mining Technologies

7. Global Underground Mining Equipment Future Market Size (in USD Bn)

7.1. Future Market Size Projections (demand for metals, mining CAPEX trends)

7.2. Key Factors Driving Future Market Growth

8. Global Underground Mining Equipment Future Market Segmentation

8.1. By Equipment Type (in Value %)

8.2. By Application (in Value %)

8.3. By Power Source (in Value %)

8.4. By Automation Level (in Value %)

8.5. By Region (in Value %)

9. Global Underground Mining Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Addressable Market)

9.2. Cost-Benefit Analysis for Investment in Automation

9.3. Marketing and Sales Strategy for OEMs

9.4. White Space Opportunities in Emerging Markets

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping out the underground mining ecosystem and key market stakeholders, including OEMs, contractors, and government agencies. This step is supported by a review of primary and secondary data from proprietary databases and public reports, identifying the critical factors that influence the market.

Step 2: Market Analysis and Construction

Historical data from major mining companies and equipment manufacturers are analyzed to estimate the underground mining equipment market. Key parameters such as market penetration, mining productivity, and financial performance are used to derive accurate estimates.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from mining companies and equipment suppliers are consulted through interviews and surveys to validate the data. This step ensures that our projections reflect real-world conditions.

Step 4: Research Synthesis and Final Output

In this final phase, all data is compiled and synthesized to create a comprehensive market report, ensuring that both quantitative and qualitative insights are aligned. We verify statistics with on-ground operations to ensure accuracy.

Frequently Asked Questions

01 How big is the Global Underground Mining Market?

The Global Underground Mining Market is valued at USD 24.5 billion, driven by increased demand for minerals such as gold, coal, and copper, as well as the adoption of automation technologies.

02 What are the challenges in the Global Underground Mining Market?

Challenges in the Global Underground Mining Market include high capital expenditure for equipment, fluctuating commodity prices, and the need for environmental compliance due to increasing regulations.

03 Who are the major players in the Global Underground Mining Market?

Major players in the Global Underground Mining Market include Caterpillar Inc., Komatsu Mining Corp., Sandvik AB, Epiroc AB, and Hitachi Construction, all of which are leaders in innovation and global reach.

04 What are the growth drivers of the Global Underground Mining Market?

Key drivers in the Global Underground Mining Market include the increasing demand for minerals used in clean energy technologies, automation and remote operation advancements, and growing concerns about worker safety in mining.

05 Which region dominates the Global Underground Mining Market?

Asia-Pacific dominates the Global Underground Mining Market due to Chinas significant mineral reserves, Australias advanced mining sector, and the regions large-scale investments in infrastructure projects.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.