India Devices Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD7731

December 2024

84

About the Report

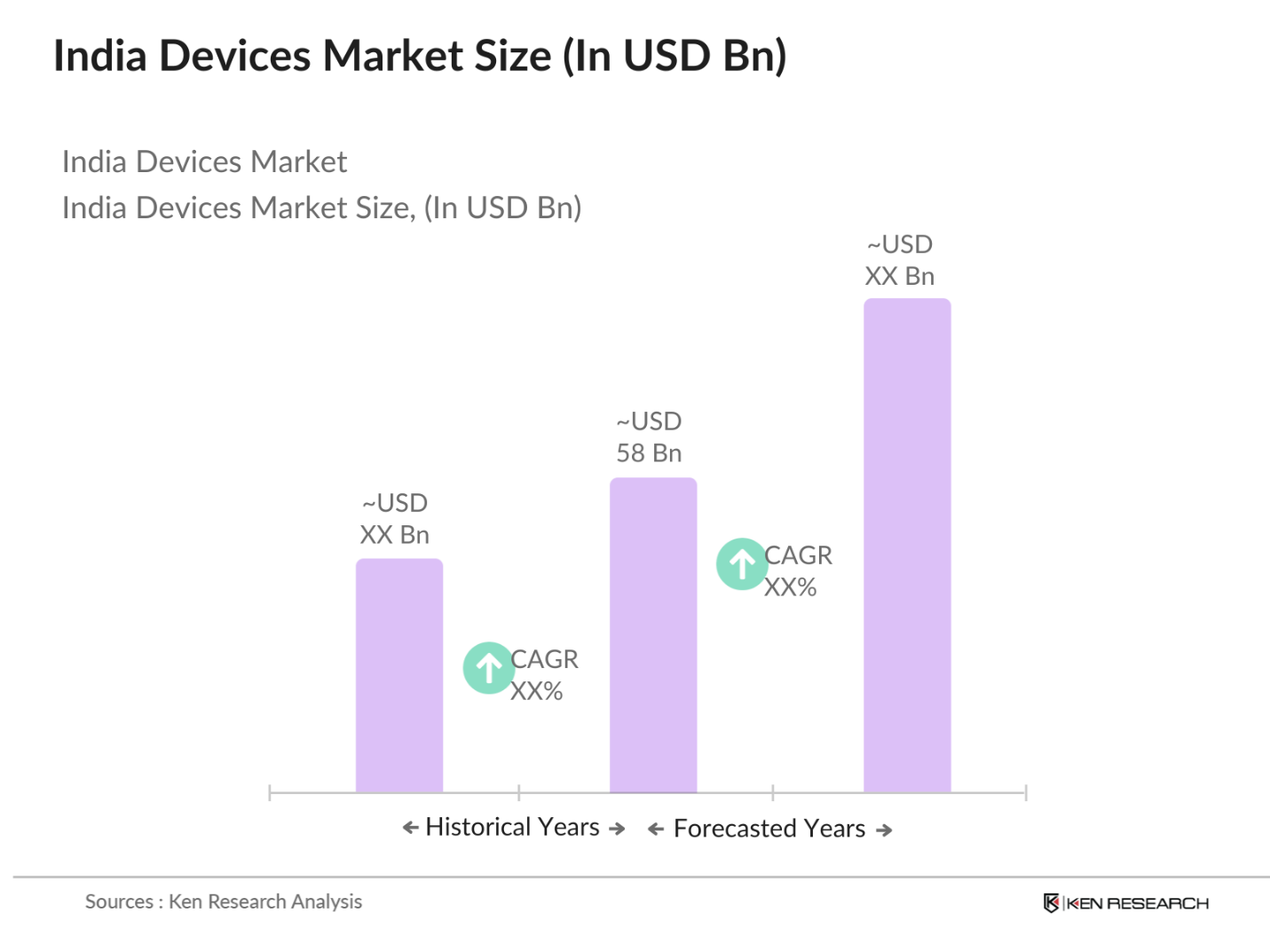

India Devices Market Overview

- The India devices market is valued at USD 58 billion, reflecting a strong growth trend driven by various factors. This growth is majorly fueled by the increasing penetration of smartphones, rapid technological advancements such as 5G, and rising disposable income across urban and rural areas. Government initiatives like Make in India have further accelerated the production and consumption of electronic devices. The surge in demand for connected devices, wearables, and smart home technologies also plays a significant role in boosting the market's size, providing ample opportunities for both local and international manufacturers.

- Indias largest metropolitan cities like Delhi, Mumbai, and Bengaluru, along with states like Maharashtra and Tamil Nadu, dominate the market due to their advanced technological infrastructure and high consumer demand for electronic products. These regions boast high digital literacy, strong distribution networks, and favorable government policies that attract significant investment. Additionally, these areas have a large base of tech-savvy consumers who actively drive the adoption of new devices, thus leading to their market dominance.

- The integration of artificial intelligence (AI) into consumer devices has gained momentum in India, especially in sectors like healthcare, manufacturing, and e-commerce. In 2023, AI-powered devices such as voice assistants, smart appliances, and personalized health monitors became increasingly common. This trend is driven by growing consumer demand for smart solutions that enhance convenience and productivity. With investments in AI technology rising, India is positioned to become a hub for AI-driven consumer devices.

India Devices Market Segmentation

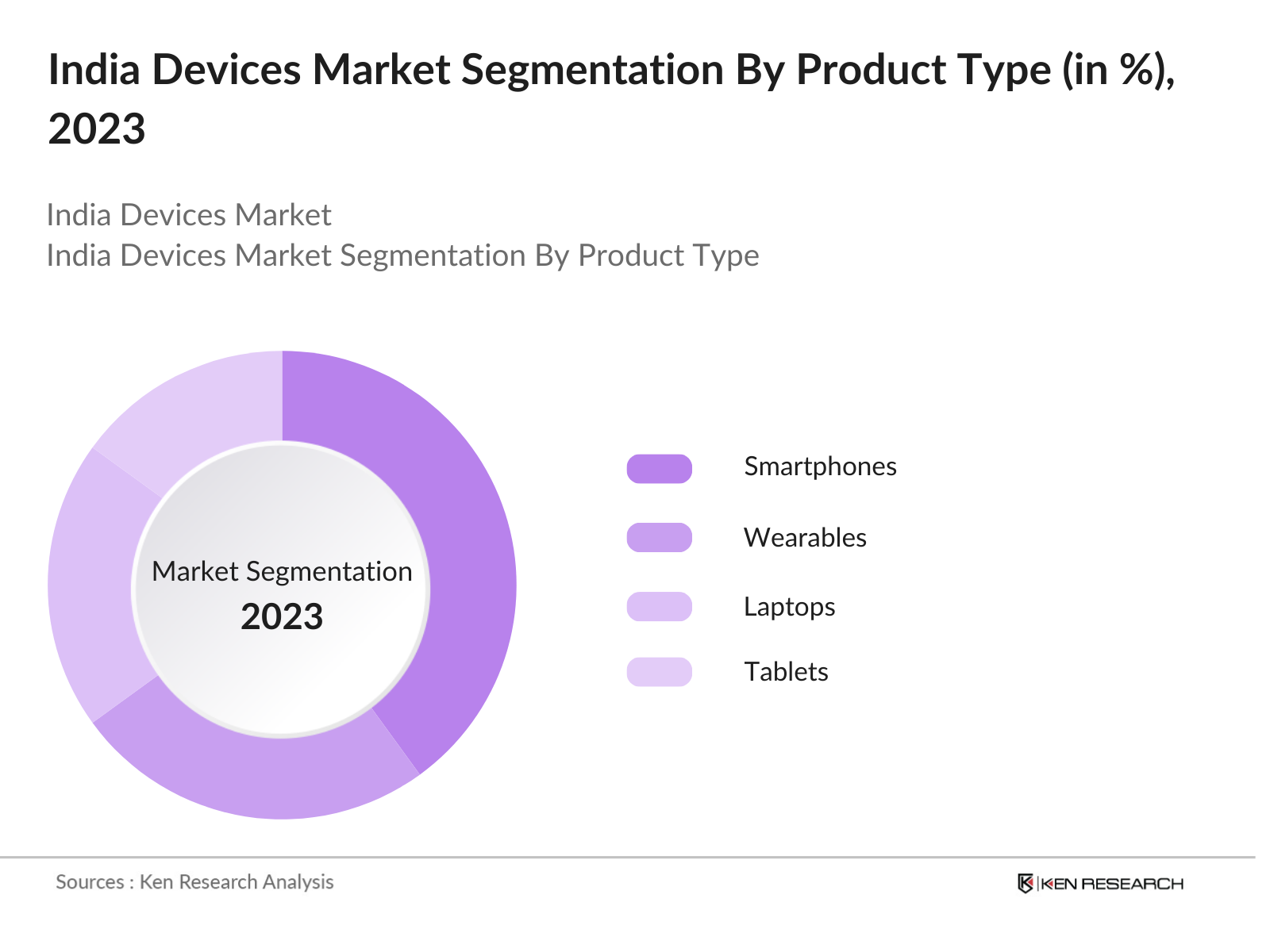

By Product Type: The India devices market is segmented by product type into smartphones, wearables, laptops, tablets, and medical devices. Among these, smartphones hold a dominant market share due to the continuous demand for upgraded models, improved network connectivity, and the growing popularity of 5G-enabled devices. Brands like Samsung, Xiaomi, and Apple have established a significant foothold in this segment, offering a range of models catering to different price points. Additionally, consumer trends toward higher functionality, such as better cameras and AI-powered features, continue to drive the demand for smartphones.

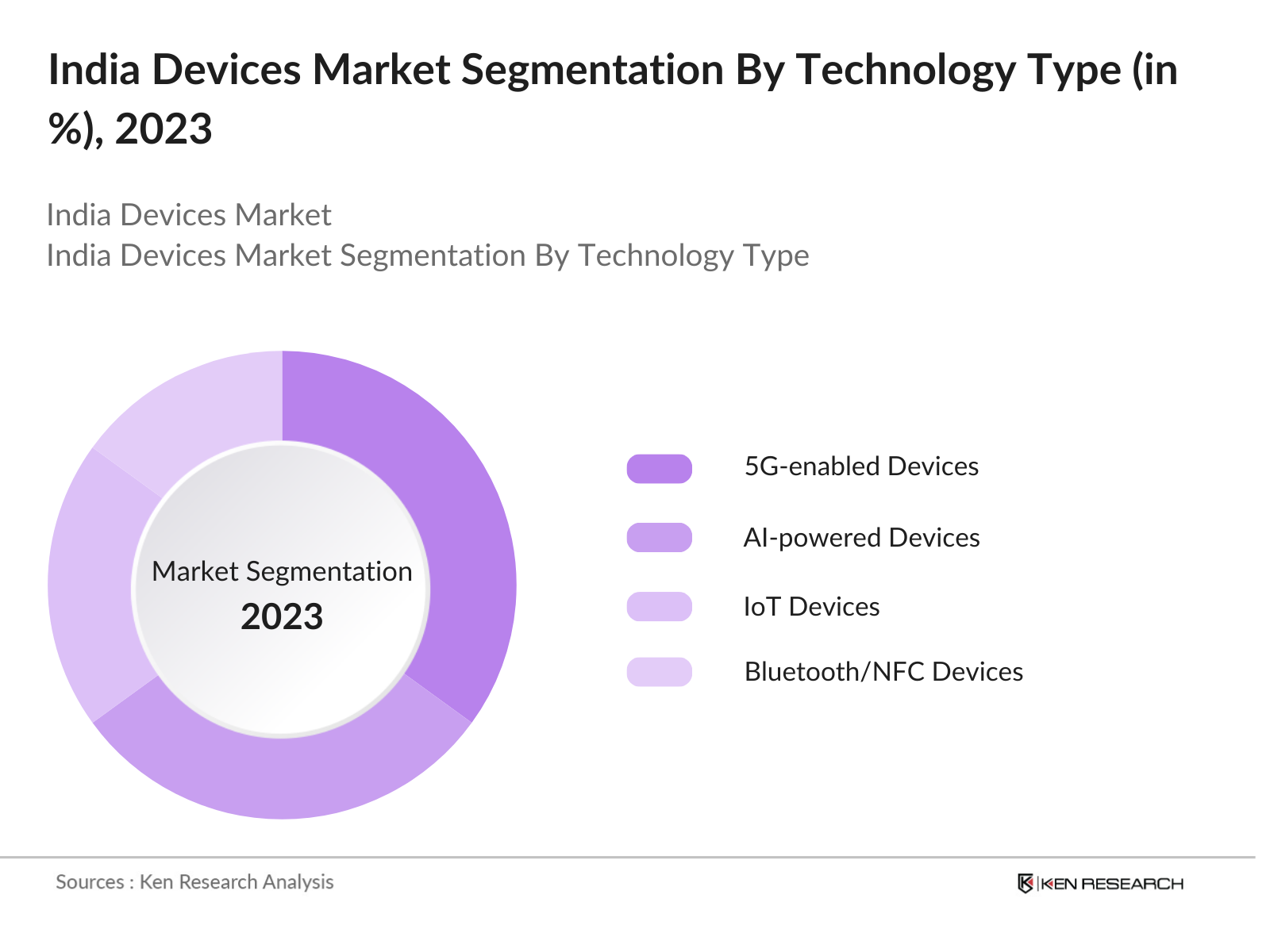

By Technology: The India devices market is also segmented by technology into 5G-enabled devices, AI-powered devices, IoT devices, and Bluetooth/NFC-enabled devices. 5G-enabled devices dominate the market share within this segment as telecom operators expand 5G services across India, creating a surge in demand for compatible devices. The rapid deployment of 5G infrastructure allows for faster internet speeds, low latency, and better device performance, making 5G devices highly sought after by both individual consumers and enterprises.

India Devices Market Competitive Landscape

The India devices market is dominated by both domestic and international players, with some companies leveraging the local manufacturing landscape while others rely on imports. Companies such as Samsung, Xiaomi, and Apple continue to hold a large share of the market, benefitting from their brand loyalty, wide product range, and innovation capabilities. Local manufacturers such as Lava and Micromax are increasingly gaining ground through affordable pricing and domestic production efforts under the "Make in India" initiative.

|

Company |

Established Year |

Headquarters |

Key Parameters |

|

Samsung Electronics |

1969 |

Suwon, South Korea |

Revenue, R&D spending, market share, product innovation |

|

Xiaomi Corporation |

2010 |

Beijing, China |

Market reach, price competitiveness, product quality |

|

Apple Inc. |

1976 |

Cupertino, USA |

Brand loyalty, product innovation, premium pricing |

|

Lava International |

2009 |

Noida, India |

Domestic production, affordability, government incentives |

|

Micromax Informatics |

2000 |

Gurugram, India |

Affordability, local manufacturing, distribution network |

India Devices Industry Analysis

Growth Drivers

- Rising Disposable Income: India's devices market is benefiting from rising disposable incomes, especially in urban regions. In 2022, India's gross national income (GNI) per capita stood at $2,400, reflecting a steady increase from previous years, driven by growing wages and employment opportunities. This rise in income levels enhances consumer spending power, particularly on electronic devices such as smartphones, laptops, and wearables. As of 2024, India's GNI continues to grow, spurring demand for advanced consumer technology products. This economic progress is fueled by robust industrial growth and expanding service sectors across the country.

- Increased Smartphone Penetration: India is the second-largest smartphone market globally, with over 750 million active users by the end of 2023. Smartphone penetration has risen sharply, largely driven by affordable devices and wide internet access through government-supported telecom infrastructure. With around 1.2 billion mobile connections in 2023, smartphone adoption continues to rise due to increasing access to 4G and expanding 5G networks. The countrys telecom sector plays a key role in supporting this growth, with data consumption skyrocketing as affordable data plans become widely available.

- Government Digitalization Initiatives: The Indian government's digital initiatives, such as the Digital India campaign, have propelled the devices market by fostering technology adoption at all levels. The governments investment of over INR 1 trillion in digital infrastructure by 2023 has significantly impacted the demand for devices supporting e-governance, online education, and digital payments. Initiatives like BharatNet, which aims to connect rural areas with broadband, further encourage the penetration of smartphones, tablets, and other devices across India. These efforts improve accessibility and tech literacy, pushing more people toward digital adoption.

Market Challenges

- High Import Tariffs on Components: Indias high import tariffs on electronic components, which can reach up to 20%, present a challenge for device manufacturers. These tariffs increase the cost of assembling electronic devices domestically, forcing companies to pass on higher costs to consumers. For example, components like semiconductors and display panels, primarily imported from countries like China and South Korea, have a significant impact on device pricing. This tariff structure hinders the competitiveness of domestic manufacturing in the global electronics supply chain.

- Supply Chain Disruptions: Supply chain disruptions, exacerbated by the COVID-19 pandemic and geopolitical tensions, have significantly affected Indias devices market. Shortages of key components like semiconductors led to delayed product launches and inflated costs in 2022 and 2023. Additionally, shipping delays and raw material shortages have impacted manufacturing timelines for devices like smartphones and laptops. These issues challenge Indias ambitions of becoming a global electronics manufacturing hub, despite government support through initiatives like "Make in India."

India Devices Market Future Outlook

Over the next five years, the India devices market is expected to experience significant growth driven by the continued expansion of the 5G network, increasing consumer demand for smart devices, and growing investments in research and development. The governments focus on digital infrastructure, coupled with the rise of connected ecosystems in homes and industries, will further bolster the market. Furthermore, the shift towards domestically manufactured devices, supported by the Make in India campaign, will help reduce import dependency and enhance the local market's competitive edge.

Opportunities

- Growing Demand for Wearable Devices: Indias wearable devices market has shown significant growth, driven by increased health awareness and fitness tracking trends. In 2023, the country saw sales of over 50 million units of wearables like fitness bands and smartwatches. This growing demand is supported by advancements in wearable technology, offering real-time health monitoring and smartphone connectivity. Companies are capitalizing on this trend by introducing affordable and feature-packed products. The growing middle class and health-conscious consumers offer a substantial growth opportunity for the wearable devices market.

- Growth of IoT and Smart Devices: The demand for IoT-enabled devices is expanding rapidly in India, driven by the growth of smart homes and industries. By 2023, India had over 200 million connected devices, including smart speakers, thermostats, and security systems. This trend is supported by an increasing number of households adopting smart home technology to enhance convenience, security, and energy efficiency. In industrial sectors, IoT devices are improving operational efficiency and enabling remote monitoring of equipment, fostering market growth.

Scope of the Report

|

Product Type |

Smartphones Wearables Tablets Laptops Medical Devices |

|

Technology |

5G-enabled Devices AI-powered Devices IoT Devices Bluetooth and NFC-enabled Devices |

|

Distribution Channel |

Online Offline Retail Stores Enterprise Solutions |

|

End User |

Consumer Healthcare Industrial Education |

|

Region |

North India South India East India West India |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Electronics and Information Technology, TRAI)

Consumer Electronics Manufacturing Companies

Telecom Operator Industries

E-commerce Platform Companies

Healthcare Provider Companies

Tech Startups Industries

Companies

Players Mentioned in the Report

Samsung Electronics

Xiaomi Corporation

Apple Inc.

Lava International

Micromax Informatics

Realme

OnePlus

Vivo Communication Technology Co., Ltd.

OPPO Electronics Corp.

Reliance Jio Infocomm Ltd.

Table of Contents

1. India Devices Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Devices Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Devices Market Analysis

3.1. Growth Drivers

3.1.1. Rising Disposable Income

3.1.2. Increased Smartphone Penetration

3.1.3. Government Digitalization Initiatives

3.1.4. Expanding 5G Network Infrastructure

3.2. Market Challenges

3.2.1. High Import Tariffs on Components

3.2.2. Supply Chain Disruptions

3.2.3. Price Sensitivity of Consumers

3.3. Opportunities

3.3.1. Growing Demand for Wearable Devices

3.3.2. Growth of IoT and Smart Devices

3.3.3. Increased Demand for Medical Devices

3.3.4. Expansion of E-commerce

3.4. Trends

3.4.1. Adoption of Artificial Intelligence in Devices

3.4.2. Increased Investment in Research and Development

3.4.3. Shift Toward Domestic Manufacturing

3.4.4. Growing Demand for Energy-efficient Devices

3.5. Government Regulations

3.5.1. Make in India Initiative

3.5.2. Electronics Manufacturing Clusters (EMC) Scheme

3.5.3. PLI (Production Linked Incentive) Scheme

3.5.4. Digital India Campaign

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. India Devices Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Smartphones

4.1.2. Wearables

4.1.3. Tablets

4.1.4. Laptops

4.1.5. Medical Devices

4.2. By Technology (In Value %)

4.2.1. 5G-enabled Devices

4.2.2. AI-powered Devices

4.2.3. IoT Devices

4.2.4. Bluetooth and NFC-enabled Devices

4.3. By Distribution Channel (In Value %)

4.3.1. Online

4.3.2. Offline Retail Stores

4.3.3. Enterprise Solutions

4.4. By End User (In Value %)

4.4.1. Consumer

4.4.2. Healthcare

4.4.3. Industrial

4.4.4. Education

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5. India Devices Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Samsung Electronics Co., Ltd.

5.1.2. Xiaomi Corporation

5.1.3. Apple Inc.

5.1.4. Reliance Jio Infocomm Ltd.

5.1.5. Vivo Communication Technology Co., Ltd.

5.1.6. OPPO Electronics Corp.

5.1.7. Lenovo Group Limited

5.1.8. Micromax Informatics Ltd.

5.1.9. Lava International Limited

5.1.10. Realme

5.1.11. HCL Technologies Limited

5.1.12. Acer Inc.

5.1.13. HP Inc.

5.1.14. Dell Technologies

5.1.15. Bosch India

5.2. Cross Comparison Parameters (Revenue, Market Share, Product Offerings, Manufacturing Capacity, R&D Spending, Technology Adoption, Market Reach, Innovation Capabilities)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. India Devices Market Regulatory Framework

6.1. Electronics and Information Technology Goods (Requirements for Compulsory Registration) Order

6.2. Import Licensing Requirements

6.3. Safety and Quality Certifications

6.4. Environmental Regulations (E-Waste Management Rules)

7. India Devices Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Devices Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Technology (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9. India Devices Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase focuses on mapping the ecosystem, identifying key stakeholders, and conducting desk research using proprietary and secondary databases. This helps identify critical variables like consumer demand, pricing trends, and technological advancements in the India Devices Market.

Step 2: Market Analysis and Construction

Historical data for the India devices market is analyzed, including market penetration and revenue generation trends. Market share of major players and device sales across different regions are compiled and evaluated.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses are validated through interviews with industry experts, such as device manufacturers, telecom operators, and distributors. These consultations provide operational insights that corroborate the collected market data.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing data from various sources, including expert interviews and market statistics, to create a comprehensive analysis. This includes validation of revenue and growth estimates through a bottom-up approach, ensuring the accuracy of the India Devices Market report.

Frequently Asked Questions

01. How big is the India Devices Market?

The India devices market is valued at USD 58 billion, driven by rising disposable incomes, expanding digital infrastructure, and increasing smartphone and IoT device adoption.

02. What are the challenges in the India Devices Market?

Challenges include high import tariffs on components, supply chain disruptions due to global factors, and the price sensitivity of Indian consumers, especially in rural areas.

03. Who are the major players in the India Devices Market?

Key players include Samsung Electronics, Xiaomi Corporation, Apple Inc., Lava International, and Micromax Informatics. These companies benefit from strong brand presence, innovative product offerings, and wide distribution networks.

04. What are the growth drivers of the India Devices Market?

The market is primarily driven by increasing smartphone penetration, the expansion of 5G technology, and rising demand for connected devices such as wearables and smart home systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.