India Gas Insulated Switchgear Market Outlook to 2030

Region:Asia

Author(s):Shreya Garg

Product Code:KROD4973

November 2024

84

About the Report

India Gas Insulated Switchgear Market Overview

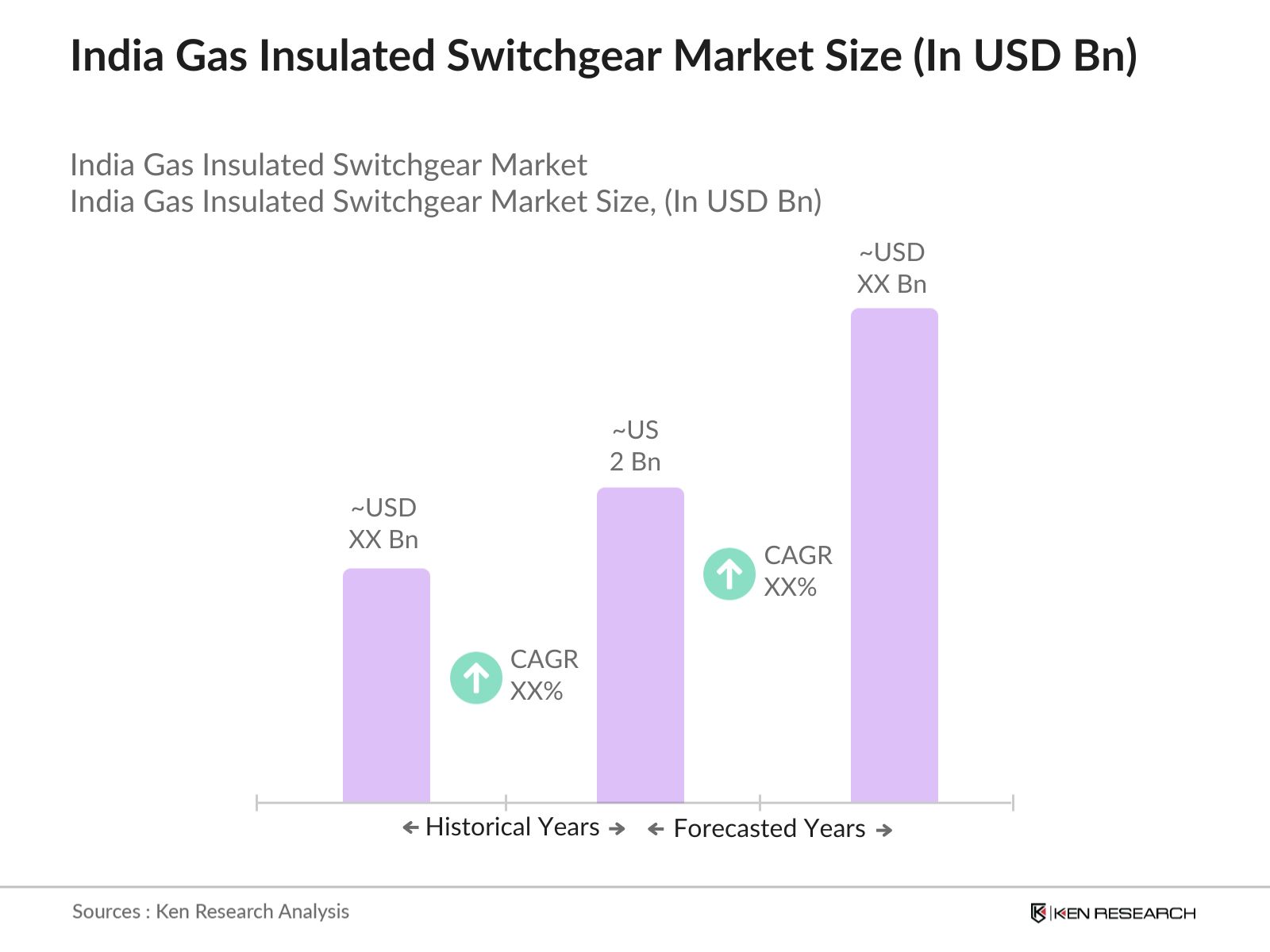

- The India gas insulated switchgear market, valued at USD 2 billion, has witnessed steady growth driven by increasing infrastructure development, government investments in power grid expansions, and the demand for reliable and compact electrical systems. The market's growth is also fueled by the shift toward renewable energy sources and Indias Smart City initiatives, which require robust transmission and distribution infrastructure. Moreover, the compact design of gas-insulated switchgear compared to traditional air-insulated alternatives is a significant factor driving its adoption in urban areas where space is a constraint.

- The dominance of cities like Delhi, Mumbai, and Bangalore in the gas-insulated switchgear market is attributed to their rapid urbanization, growing industrial activities, and higher electricity demand. These cities are key power hubs, home to major commercial establishments and industrial centers, requiring advanced electrical infrastructure. Additionally, government policies in these regions encourage the modernization of substations to support smart grids and sustainable energy transitions.

- The Indian government's National Electricity Plan (2022-2027) emphasizes the expansion and modernization of the power grid, including increased investments in advanced switchgear technologies like GIS. The plan outlines an investment of over INR 2 trillion for the expansion of transmission and distribution networks, with a focus on reducing technical losses and enhancing grid reliability through advanced technologies.

India Gas Insulated Switchgear Market Segmentation

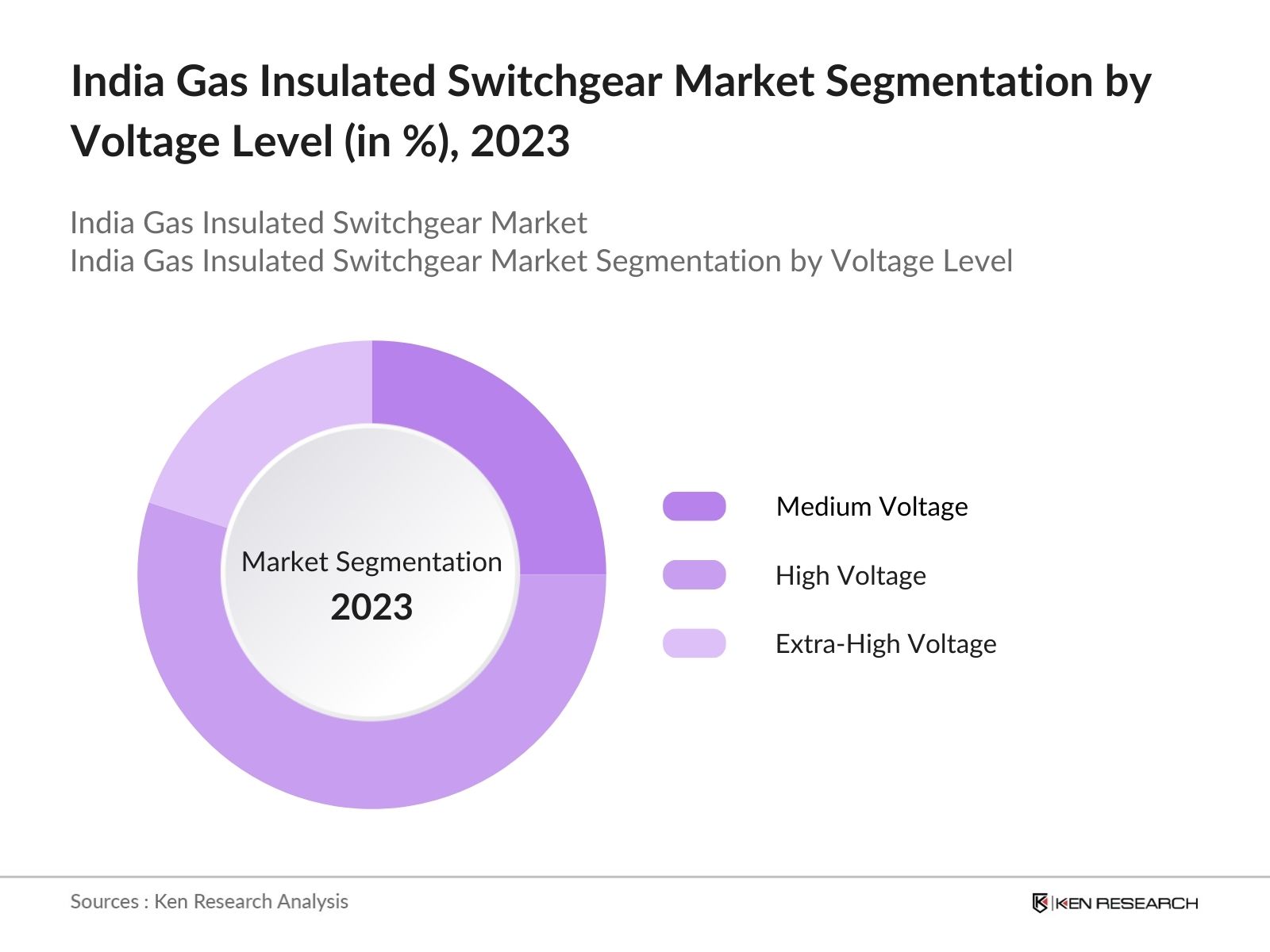

By Voltage Level: The market is segmented by voltage level into medium voltage (up to 36kV), high voltage (36kV150kV), and extra-high voltage (above 150kV). High voltage gas insulated switchgear holds the dominant market shares due to its widespread application in large-scale power projects and substations across India. This segment benefits from the countrys large-scale transmission infrastructure upgrades, especially in urban regions, to accommodate the rising demand for uninterrupted electricity. Moreover, the high efficiency and lower maintenance requirements of high voltage switchgear systems make them a preferred choice for power distribution in major industrial areas.

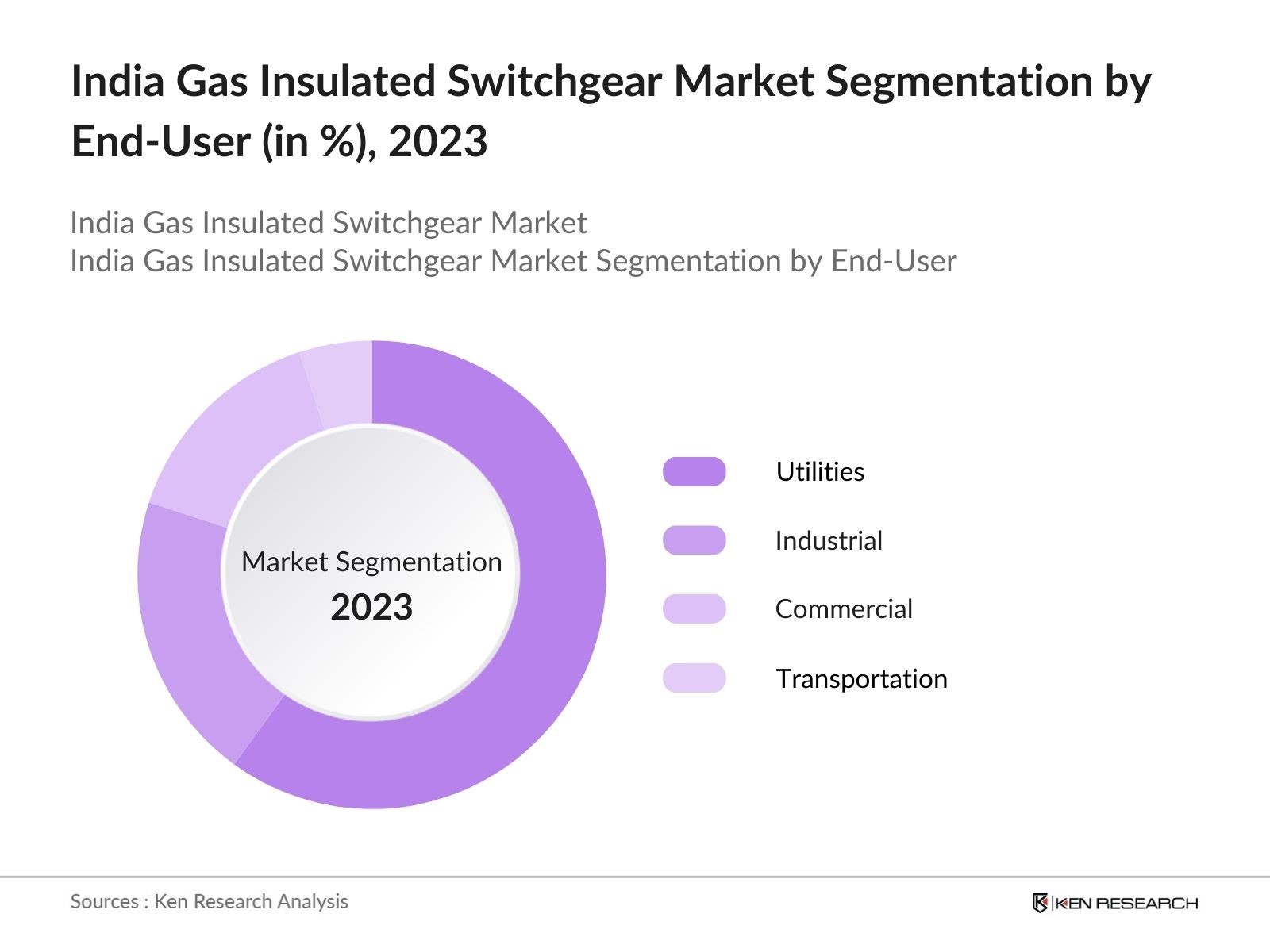

By End-User: The market is also segmented by end-users, including utilities, industrial, commercial, and transportation sectors. The utility sector accounts for the largest share, driven by India's ongoing efforts to improve its electrical grid and transmission systems. The growing demand for reliable and efficient power in urban areas and the expansion of renewable energy projects, such as wind and solar farms, has led to increased installations of gas-insulated switchgear by utility companies. The industrial sector follows, with increasing demand from manufacturing units and factories requiring high-performance electrical infrastructure.

India Gas Insulated Switchgear Market Competitive Landscape

The India gas insulated switchgear market is dominated by a combination of global players and local manufacturers. Major companies like Siemens Ltd. and ABB India Ltd. have established strong positions due to their extensive R&D capabilities and technological advancements. Additionally, local companies like Larsen & Toubro have leveraged their understanding of regional market dynamics to secure contracts for large-scale infrastructure projects. This competitive landscape reflects the balance between global innovation and localized service delivery, which is critical for addressing India's unique market demands.

|

Company |

Establishment Year |

Headquarters |

Employees |

Revenue (USD Bn) |

R&D Investment |

Technology Focus |

Key Contracts |

Regional Presence |

|

Siemens Ltd. |

1847 |

Munich, Germany |

||||||

|

ABB India Ltd. |

1988 |

Bangalore, India |

||||||

|

Larsen & Toubro |

1938 |

Mumbai, India |

||||||

|

General Electric India |

1892 |

Boston, USA |

||||||

|

Schneider Electric India |

1836 |

Rueil-Malmaison, France |

India Gas Insulated Switchgear Industry Analysis

Growth Drivers

- Urbanization and Infrastructure Development: India's rapid urbanization has driven substantial infrastructure development, increasing the demand for gas-insulated switchgear (GIS). As of 2023, India's urban population exceeded 497 million, creating the need for efficient power systems in cities. The Indian government has allocated over INR 10 trillion towards urban infrastructure under initiatives like the Smart Cities Mission and AMRUT. These programs emphasize robust power transmission and distribution networks, stimulating demand for GIS solutions that offer compact and efficient infrastructure, particularly in space-constrained urban areas.

- Growing Demand for Renewable Energy: India's renewable energy sector continues to grow rapidly, with installed capacity reaching 174 GW by September 2023, driven by solar and wind power expansion. GIS technology is crucial for renewable energy integration due to its reliability and minimal space requirements. The governments target of 500 GW of non-fossil fuel energy capacity by 2030 further supports the deployment of GIS systems to ensure the stability of renewable power generation and distribution grids. The emphasis on renewable energy integration offers significant growth opportunities for GIS manufacturers in India.

- Technological Advancements in Switchgear Efficiency: Recent technological advancements in GIS have significantly improved efficiency and operational safety, driving their adoption in India. Modern GIS systems now offer features like condition monitoring and real-time diagnostics, which reduce maintenance costs and improve grid reliability. Indias power utilities have begun adopting these technologies as part of digital transformation efforts. In 2023, over 50 substations in India adopted GIS with enhanced monitoring systems, highlighting the shift towards more advanced and reliable switchgear technology in the Indian power sector.

Market Challenges

- High Initial Capital Cost: Despite the long-term benefits of GIS, the initial capital cost remains a challenge. For instance, GIS systems are up to 40% more expensive than traditional air-insulated switchgear due to their advanced technology and space-saving design. This cost barrier can be prohibitive for smaller utilities and rural projects, where budget constraints limit the adoption of advanced switchgear systems. However, government subsidies and financial incentives are helping mitigate some of these costs, particularly in infrastructure projects under central and state initiatives.

- Environmental Regulations: SF6 (sulfur hexafluoride) gas, widely used in GIS for insulation, is a potent greenhouse gas, with a global warming potential approximately 23,500 times greater than CO2. Due to its environmental impact, India has introduced stricter regulations around SF6 usage, particularly under the 2022 update to the Environment Protection Act. This regulatory pressure has increased the need for GIS manufacturers to explore alternative insulation technologies, driving up compliance costs and slowing adoption rates in some sectors.

India Gas Insulated Switchgear Market Future Outlook

Over the next five years, the India gas insulated switchgear market is expected to experience significant growth driven by rapid urbanization, expansion of renewable energy projects, and increasing investments in electrical infrastructure. The Indian governments push for modernizing the transmission and distribution network, along with the growing adoption of smart grid technology, will further propel the demand for gas-insulated switchgear. Additionally, the emphasis on sustainability and reducing carbon emissions will likely result in a shift toward eco-friendly alternatives to traditional SF6 switchgear.

Future Market Opportunities

- Expansion of Smart Grids: Indias smart grid initiatives, underpinned by projects like the National Smart Grid Mission (NSGM), have created a significant opportunity for GIS. By 2024, over 25 smart grid pilot projects are operational in India, requiring advanced switchgear systems to handle data-driven and automated power distribution networks. GIS, with its compact design and high reliability, plays a crucial role in the success of these smart grids, helping utilities enhance grid stability and reduce transmission losses.

- Rural Electrification Projects: Indias rural electrification drive, under schemes like DDUGJY, aims to provide universal access to electricity. As of 2023, over 99% of India's villages have been electrified, but improving the quality and reliability of supply remains a priority. The governments ongoing investments in rural power infrastructureexceeding INR 45,000 croresnecessitate the adoption of advanced technologies like GIS to reduce technical losses and ensure reliable power supply to rural areas, where land availability is also a constraint.

Scope of the Report

|

Voltage Level |

Medium Voltage High Voltage Extra-High Voltage |

|

Installation Type |

Indoor Outdoor |

|

End-User |

Utilities Industrial Commercial Transportation |

|

Technology |

SF6 Switchgear Non-SF6 Alternatives |

|

Region |

North South East West |

Products

Key Target Audience

Utilities Companies

Power Generation Companies

Industrial Manufacturers

Government and Regulatory Bodies (Central Electricity Regulatory Commission, Ministry of Power)

Electrical Contractors and Engineers

Renewable Energy Project Developers

Transmission and Distribution Companies

Investor and Venture Capitalist Firms

Companies

Major Players

Siemens Ltd.

ABB India Ltd.

Larsen & Toubro

Schneider Electric India

General Electric India

Mitsubishi Electric India

Toshiba Transmission & Distribution

Hyosung Heavy Industries

Bharat Heavy Electricals Limited (BHEL)

Nissin Electric Co., Ltd.

Fuji Electric India

Alstom T&D India

Eaton India

Hyosung Heavy Industries

Hitachi Energy India

Table of Contents

1. India Gas Insulated Switchgear Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (based on installation base, voltage level, and regional demand)

1.4. Market Segmentation Overview

2. India Gas Insulated Switchgear Market Size (In USD Bn)

2.1. Historical Market Size (segmented by application and product type)

2.2. Year-On-Year Growth Analysis (growth rates by region and voltage level)

2.3. Key Market Developments and Milestones (specific technological advancements, regulatory changes)

3. India Gas Insulated Switchgear Market Analysis

3.1. Growth Drivers

3.1.1. Urbanization and Infrastructure Development

3.1.2. Growing Demand for Renewable Energy

3.1.3. Government Initiatives and Investments in Power Sector

3.1.4. Technological Advancements in Switchgear Efficiency

3.2. Market Challenges

3.2.1. High Initial Capital Cost (cost parameters for gas-insulated switchgear in India)

3.2.2. Environmental Regulations (impact of SF6 regulations in India)

3.2.3. Limited Awareness and Technical Know-How

3.3. Opportunities

3.3.1. Expansion of Smart Grids

3.3.2. Rural Electrification Projects

3.3.3. Adoption of Green Technologies (alternative insulation gases)

3.4. Trends

3.4.1. Hybrid Switchgear Adoption

3.4.2. Digitalization in Substations (Indias growing adoption of digital substations)

3.4.3. Demand for Compact Substation Solutions

3.5. Regulatory Environment

3.5.1. National Electricity Plan

3.5.2. Tariff Guidelines for Transmission Projects

3.5.3. Environmental Impact Regulations (SF6 gas usage)

3.5.4. Public-Private Partnership Initiatives

3.6. SWOT Analysis (industry-specific: efficiency, environmental risks, etc.)

3.7. Stakeholder Ecosystem (Government, OEMs, EPC contractors, end-users)

3.8. Porters Five Forces (supplier dynamics, competitive landscape, substitutes)

3.9. Competition Ecosystem (focus on Indian market players)

4. India Gas Insulated Switchgear Market Segmentation

4.1. By Voltage Level (In Value %)

4.1.1. Medium Voltage (up to 36kV)

4.1.2. High Voltage (36kV-150kV)

4.1.3. Extra-High Voltage (above 150kV)

4.2. By Installation Type (In Value %)

4.2.1. Indoor

4.2.2. Outdoor

4.3. By End-User (In Value %)

4.3.1. Utilities

4.3.2. Industrial

4.3.3. Commercial

4.3.4. Transportation

4.4. By Technology (In Value %)

4.4.1. SF6 Switchgear

4.4.2. Non-SF6 Alternatives (vacuum, air-insulated switchgear)

4.5. By Region (In Value %)

4.5.1. Northern India

4.5.2. Southern India

4.5.3. Eastern India

4.5.4. Western India

5. India Gas Insulated Switchgear Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Siemens Ltd.

5.1.2. ABB India Ltd.

5.1.3. Larsen & Toubro

5.1.4. Schneider Electric India

5.1.5. General Electric India

5.1.6. Toshiba Transmission & Distribution

5.1.7. Hitachi Energy India

5.1.8. CG Power and Industrial Solutions Ltd.

5.1.9. Alstom T&D India

5.1.10. Nissin Electric Co., Ltd.

5.1.11. Hyosung Heavy Industries

5.1.12. Bharat Heavy Electricals Limited (BHEL)

5.1.13. Eaton India

5.1.14. Mitsubishi Electric India

5.1.15. Fuji Electric India

5.2. Cross Comparison Parameters (Employees, Revenue, Switchgear Sales, Product Range, Technology Focus, Key Contracts, Regional Presence, R&D Investment)

5.3. Market Share Analysis (by voltage level and technology type)

5.4. Strategic Initiatives (joint ventures, technology partnerships, product launches)

5.5. Mergers and Acquisitions (relevant market consolidations in India)

5.6. Investment Analysis (capex and opex in new installations)

5.7. Venture Capital Funding

5.8. Government Grants (for local manufacturing, R&D)

5.9. Private Equity Investments

6. India Gas Insulated Switchgear Market Regulatory Framework

6.1. Environmental Standards (SF6 emissions guidelines)

6.2. Compliance Requirements (Bureau of Indian Standards certifications)

6.3. Certification Processes

7. India Gas Insulated Switchgear Future Market Size (In USD Bn)

7.1. Future Market Size Projections (regional breakdown and demand drivers)

7.2. Key Factors Driving Future Market Growth (smart grid integration, sustainable switchgear solutions)

8. India Gas Insulated Switchgear Future Market Segmentation

8.1. By Voltage Level (In Value %)

8.2. By Installation Type (In Value %)

8.3. By End-User (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. India Gas Insulated Switchgear Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (segmented by demand patterns, industry verticals)

9.3. Marketing Initiatives (tailored strategies for Indian industrial and utility customers)

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying key variables influencing the India Gas Insulated Switchgear Market, such as transmission infrastructure upgrades, government initiatives, and technological innovations. Extensive desk research and analysis of secondary databases are used to gather critical data and map the market ecosystem.

Step 2: Market Analysis and Construction

In this phase, we analyze historical market data related to installations, technological advancements, and regional demand variations. This step includes the study of revenue generation from key players and an assessment of market penetration in the utility and industrial sectors.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with industry experts through telephonic interviews and surveys are conducted to validate hypotheses developed during the research. This includes gathering expert opinions on regulatory impacts, technological developments, and customer preferences.

Step 4: Research Synthesis and Final Output

In the final phase, insights from manufacturers and key stakeholders are integrated with statistical analysis to produce a comprehensive report on the India Gas Insulated Switchgear Market. This ensures the final output is accurate, validated, and useful for business professionals.

Frequently Asked Questions

01. How big is the India Gas Insulated Switchgear Market?

The India Gas Insulated Switchgear market is valued at USD 2 billion, driven by the countrys push for smart grid modernization and increasing electricity demand in urban centers.

02. What are the challenges in the India Gas Insulated Switchgear Market?

Challenges in the India Gas Insulated Switchgear market include the high initial capital costs associated with gas insulated switchgear, as well as strict environmental regulations regarding SF6 usage, which is a greenhouse gas used in some systems.

03. Who are the major players in the India Gas Insulated Switchgear Market?

Major players in the in the India Gas Insulated Switchgear market include Siemens Ltd., ABB India Ltd., Larsen & Toubro, Schneider Electric India, and General Electric India, all of which dominate due to their strong R&D capabilities and comprehensive service offerings.

04. What are the growth drivers of the India Gas Insulated Switchgear Market?

Growth drivers in the in the India Gas Insulated Switchgear market include government investments in power infrastructure, the increasing demand for compact and efficient electrical systems, and the expansion of renewable energy projects.

05. What is the future outlook for the India Gas Insulated Switchgear Market?

The in the India Gas Insulated Switchgear market is expected to experience strong growth in the coming years, driven by the push for smart grid development and the modernization of Indias transmission and distribution infrastructure.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.