India Veterinary Healthcare Market Outlook to 2030

Region:Asia

Author(s):Sanjna

Product Code:KROD5097

November 2024

88

About the Report

India Veterinary Healthcare Market Overview

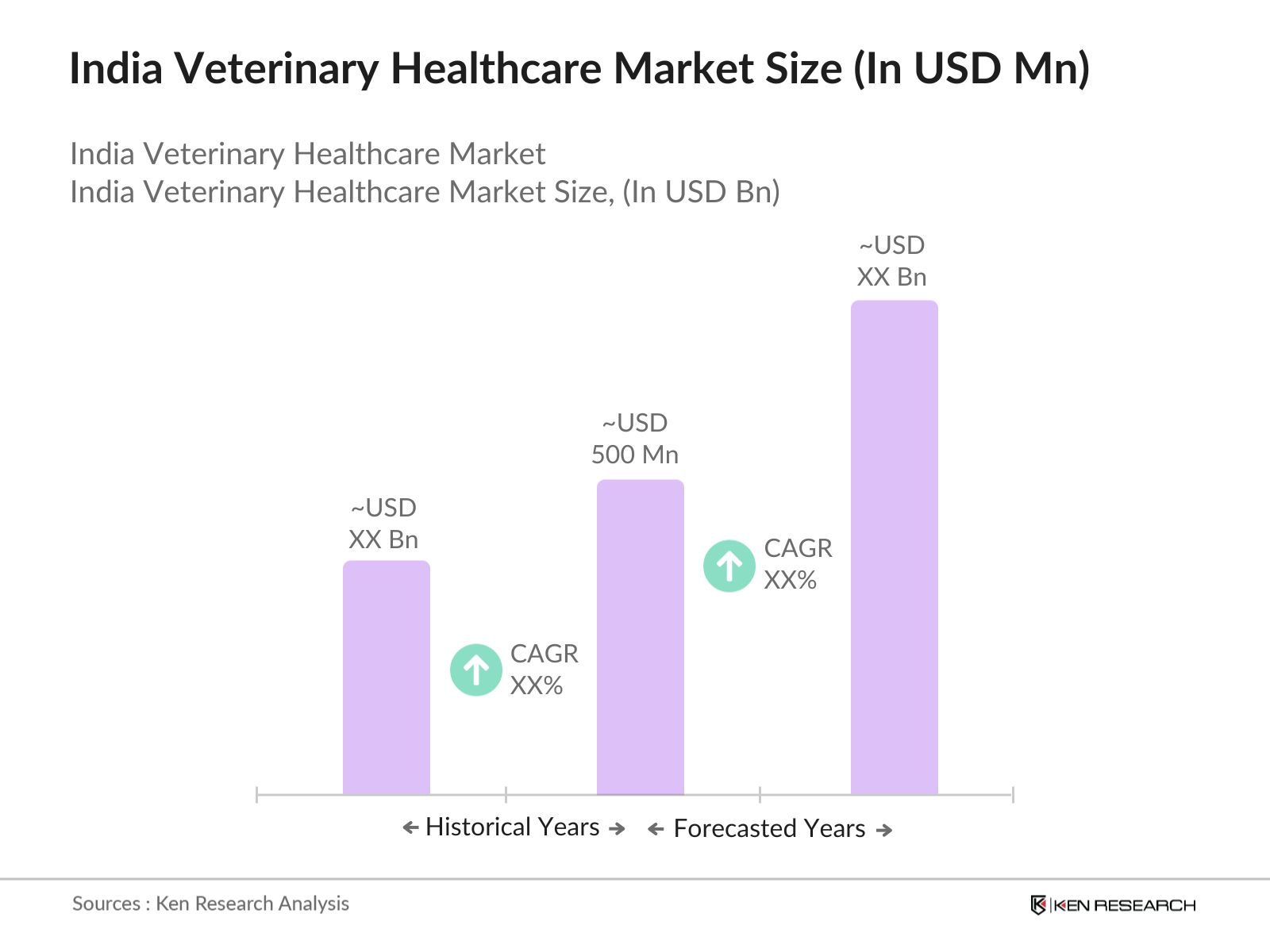

- India Veterinary Healthcare Market is valued at USD 500 million, driven by the growing awareness of animal health and welfare. Increasing livestock farming, rising pet ownership, and a focus on veterinary healthcare have contributed to this growth. Pharmaceuticals and diagnostic tools are essential segments within the market, addressing both companion animals and livestock needs. Factors like the rising prevalence of zoonotic diseases and the governments push for better animal health infrastructure are further driving the market.

- India's veterinary healthcare market sees dominance in regions like Maharashtra, Karnataka, and Gujarat. These regions lead due to the concentration of livestock farming, the presence of large veterinary hospitals, and higher pet ownership rates. Additionally, these states have established animal welfare policies, advanced veterinary infrastructure, and proactive government initiatives supporting both rural and urban veterinary care. The agricultural and livestock economies in these areas are robust, adding to their importance within the market.

- The veterinary pharmaceutical industry in India is regulated by the Ministry of Health & Family Welfare under the Drugs and Cosmetics Act, 1940. As of 2024, the government has introduced stricter quality control measures for veterinary drugs and vaccines to ensure their safety and efficacy. Approximately 80% of veterinary drugs sold in India must meet the latest standards for Good Manufacturing Practices (GMP). This regulatory framework helps maintain the quality of medicines available in the market, ensuring that animals receive safe and effective treatment.

India Veterinary Healthcare Market Segmentation

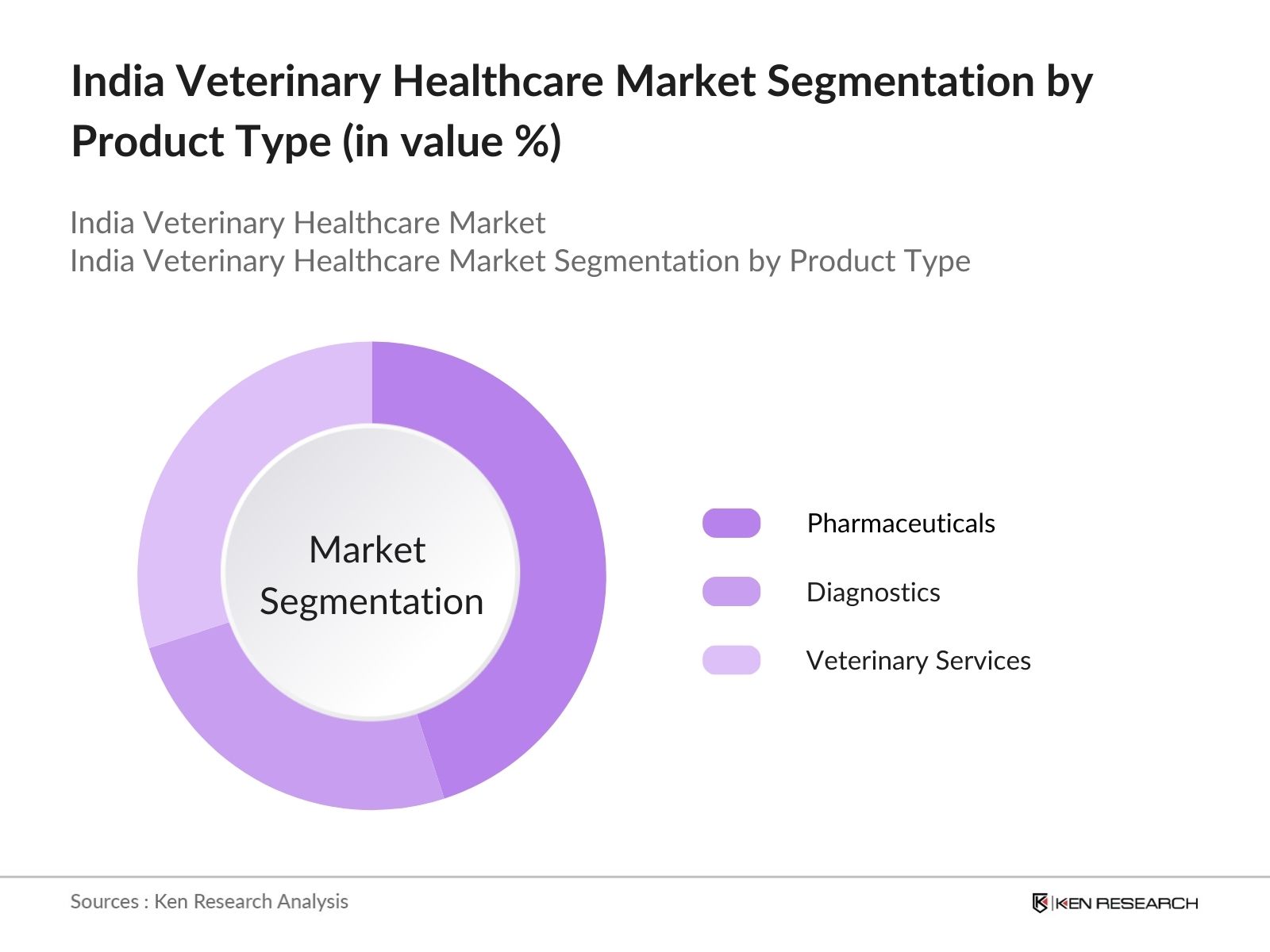

By Product Type: Indias veterinary healthcare market is segmented by product type into pharmaceuticals, diagnostics, and veterinary services. Pharmaceuticals hold a dominant market share, owing to the increasing demand for vaccines, antibiotics, and antiparasitics. The livestock sector's demand for preventive medicines and companion animal owners reliance on pet medications further contribute to this dominance. The rapid rise in zoonotic diseases like avian influenza has also pushed the use of pharmaceuticals to ensure the health of farm animals, thus maintaining a strong market position.

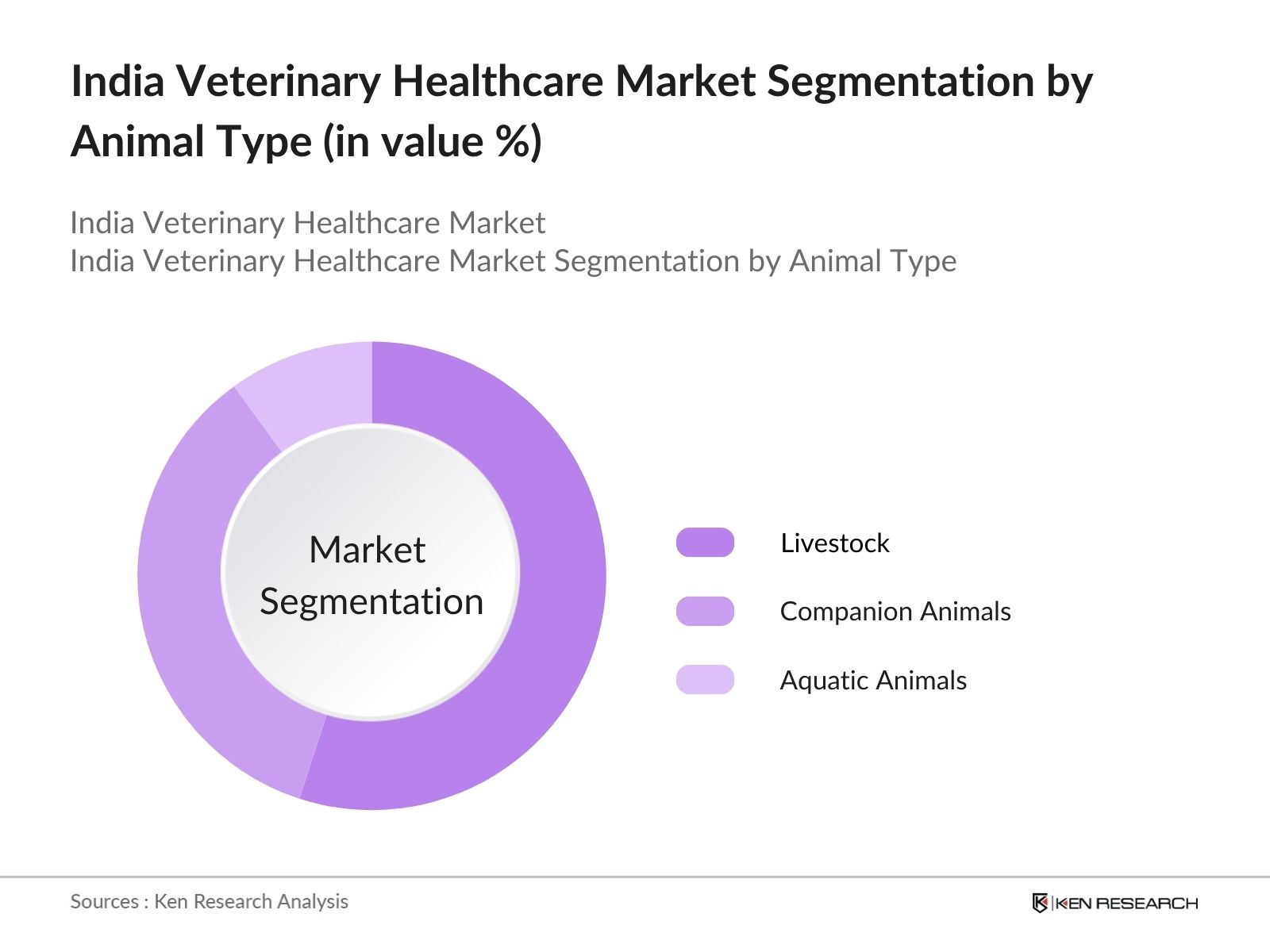

By Animal Type: Indias veterinary healthcare market is segmented by animal type into companion animals, livestock, and aquatic animals. Livestock dominates the market, driven by the nations dependence on agriculture and dairy farming. Livestock farming is a significant contributor to the economy, and the growing demand for high-quality animal products has increased the focus on veterinary healthcare in this segment. Moreover, government initiatives supporting livestock farming and disease control programs for animals have strengthened the importance of livestock in this sector.

India Veterinary Healthcare Market Competitive Landscape

The India veterinary healthcare market is dominated by a mix of local and international players. Large multinational companies like Zoetis and Merck Animal Health have strong footholds in the pharmaceuticals and diagnostics segments. Meanwhile, domestic players such as Hester Biosciences and Indian Immunologicals have established strong networks in the livestock health space. The market is consolidated around a few key players, with local manufacturers focusing on specific regions and niches.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

R&D Spending |

Revenue |

Product Portfolio |

Geographical Reach |

Strategic Collaborations |

|

Zoetis Inc. |

1952 |

New Jersey, USA |

- |

- |

- |

- |

- |

- |

|

Merck Animal Health |

1891 |

New Jersey, USA |

- |

- |

- |

- |

- |

- |

|

Hester Biosciences |

1987 |

Ahmedabad, India |

- |

- |

- |

- |

- |

- |

|

Indian Immunologicals Ltd. |

1982 |

Hyderabad, India |

- |

- |

- |

- |

- |

- |

|

Virbac |

1968 |

Carros, France |

- |

- |

- |

- |

- |

- |

India Veterinary Healthcare Market Analysis

Growth Drivers

- Rising Pet Ownership: The growing trend of pet ownership in India has significantly driven the demand for veterinary healthcare services. There are over31 million pet dogsin the country, making them the most common pets among Indian households, where63% of pet owners have at least one dog This increase in pet ownership has resulted in higher demand for veterinary services, including vaccinations, preventive care, and treatment for chronic diseases.

- Livestock Farming Expansion: Livestock farming plays a critical role in Indias economy, contributing significantly to the countrys rural employment and GDP. According to the20th Livestock Census, the total livestock population in India was reported to be535.78 million. Livestock farming has expanded due to increasing demand for dairy products, meat, and poultry. This growth has driven investments in veterinary healthcare to ensure the health of livestock, as the economic losses from diseases can be devastating for farmers.

- Increase in Zoonotic Diseases: Zoonotic diseases, which spread between animals and humans, have seen a rise in India, driving the need for advanced veterinary healthcare. TheWorld Health Organization (WHO)estimates that India accounts for36% of global rabies deaths, with an estimated18,000 to 20,000 human rabies casesoccurring annually due to dog bites. This alarming statistic has underscored the importance of preventing zoonotic diseases, leading to an increase in demand for veterinary vaccines and treatments.

Challenges

- High Cost of Veterinary Medicines: Veterinary medicines in India, especially for advanced treatments, remain costly, which limits accessibility for many pet owners and livestock farmers. The cost of certain imported veterinary drugs can be 20-30% higher than their human medicine counterparts. This price disparity is partly due to the lack of domestic manufacturing capabilities for specialized animal drugs.

- Lack of Veterinary Infrastructure in Rural Areas: Despite the rise in pet ownership and livestock farming, rural India still faces significant challenges in accessing veterinary services. Only about 30% of Indias rural areas have veterinary hospitals or clinics, according to a report from the Ministry of Rural Development. Rural farmers often face difficulties in receiving timely healthcare for their livestock, leading to preventable losses from diseases. The government's veterinary extension programs are still underfunded and underdeveloped in many rural parts of the country.

India Veterinary Healthcare Future Market Outlook

Over the next five years, the India veterinary healthcare market is expected to experience significant growth, driven by the increasing demand for livestock products, expansion of veterinary diagnostics, and continuous government support for animal health infrastructure. Technological advancements, particularly in diagnostic tools and telemedicine for veterinary services, are expected to further drive market expansion. Moreover, growing pet ownership in urban areas is likely to boost the demand for companion animal healthcare solutions.

Market Opportunities

- Growth in Veterinary Diagnostics: The veterinary diagnostics sector is witnessing significant growth, driven by the increased focus on early disease detection and preventive care. As of 2024, India has seen a rise in diagnostic centers for animals, with over 1,500 new facilities established in the last three years. These centers offer services such as blood tests, imaging, and molecular diagnostics. The increase in pet ownership and livestock farming has necessitated a robust diagnostic framework to ensure animal health. Government-backed programs like NADCP also support the development of diagnostic tools for livestock.

- Technological Advancements in Animal Health Solutions: In 2024, India has seen the introduction of AI-based diagnostic tools, wearable health monitoring devices for pets, and mobile apps for remote veterinary consultations. Over 500 veterinary clinics across India now use AI-assisted diagnostic tools to enhance the accuracy of disease detection. Additionally, tech-driven companies are partnering with veterinary hospitals to offer digital health platforms for continuous monitoring of pets and livestock.

Scope of the Report

|

Segments |

Sub-Segments |

|

Product Type |

Pharmaceuticals |

|

Diagnostics |

|

|

Veterinary Services |

|

|

Animal Type |

Companion Animals (Dogs, Cats, Horses) |

|

Livestock (Cattle, Poultry, Swine, Sheep) |

|

|

Aquatic Animals (Fish, Shellfish) |

|

|

Mode of Delivery |

Oral Administration |

|

Injectable |

|

|

Topical |

|

|

End User |

Veterinary Clinics |

|

Veterinary Hospitals |

|

|

Research Institutions |

|

|

Home Care Settings |

|

|

Region |

North |

|

South |

|

|

West |

|

|

East |

Products

India Veterinary Healthcare Market Key Target Audience

Pet Food Manufacturers

Animal Healthcare Product Manufacturers

Veterinary Equipment Manufacturers

Veterinary Pharmaceutical Companies

E-commerce Companies in Veterinary Products

Government and Regulatory Bodies (Animal Welfare Board of India, Ministry of Agriculture & Farmers Welfare)

Investors and Venture Capitalist Firms

Companies

India Veterinary Healthcare Market Key Players

Zoetis Inc.

Merck Animal Health

Elanco Animal Health

Boehringer Ingelheim

Virbac

Hester Biosciences

Bayer Animal Health

Vetoquinol SA

Dechra Pharmaceuticals

Indian Immunologicals Ltd.

Neogen Corporation

SeQuent Scientific Ltd.

Intas Pharmaceuticals

Himalaya Animal Healthcare

Zoivane Livestock

Table of Contents

1. India Veterinary Healthcare Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Compounded Annual Growth Rate, Market Revenue)

1.4. Market Segmentation Overview

2. India Veterinary Healthcare Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Acquisition, Partnerships, Major Investments)

3. India Veterinary Healthcare Market Analysis

3.1. Growth Drivers

3.1.1. Rising Pet Ownership

3.1.2. Livestock Farming Expansion

3.1.3. Government Initiatives for Animal Health

3.1.4. Increase in Zoonotic Diseases

3.2. Market Challenges

3.2.1. High Cost of Veterinary Medicines

3.2.2. Lack of Veterinary Infrastructure in Rural Areas

3.2.3. Limited Access to Modern Healthcare for Animals

3.3. Opportunities

3.3.1. Growth in Veterinary Diagnostics

3.3.2. Increasing Focus on Companion Animal Health

3.3.3. Technological Advancements in Animal Health Solutions

3.4. Trends

3.4.1. Telemedicine for Veterinary Care

3.4.2. Increasing Demand for Natural and Organic Pet Healthcare Products

3.4.3. Use of AI in Veterinary Diagnostics

3.5. Government Regulation

3.5.1. Regulations on Animal Welfare and Safety

3.5.2. Veterinary Pharmaceuticals and Products Regulations

3.5.3. Standards for Veterinary Clinics and Animal Healthcare Facilities

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Veterinarians, Farmers, Pet Owners, Suppliers, Government)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. India Veterinary Healthcare Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Pharmaceuticals (Vaccines, Antibiotics, Antiparasitics)

4.1.2. Diagnostics (Imaging, Molecular Testing, Blood Tests)

4.1.3. Veterinary Services (Clinical Services, Surgical Services, Emergency Care)

4.2. By Animal Type (In Value %)

4.2.1. Companion Animals (Dogs, Cats, Horses)

4.2.2. Livestock (Cattle, Poultry, Swine, Sheep)

4.2.3. Aquatic Animals (Fish, Shellfish)

4.3. By Mode of Delivery (In Value %)

4.3.1. Oral Administration

4.3.2. Injectable

4.3.3. Topical

4.4. By End User (In Value %)

4.4.1. Veterinary Clinics

4.4.2. Veterinary Hospitals

4.4.3. Research Institutions

4.4.4. Home Care Settings

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. West

4.5.4. East

5. India Veterinary Healthcare Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Zoetis Inc.

5.1.2. Merck Animal Health

5.1.3. Elanco Animal Health

5.1.4. Boehringer Ingelheim

5.1.5. Virbac

5.1.6. Bayer Animal Health

5.1.7. Vetoquinol SA

5.1.8. Dechra Pharmaceuticals

5.1.9. Hester Biosciences

5.1.10. Indian Immunologicals Ltd.

5.1.11. Neogen Corporation

5.1.12. SeQuent Scientific Ltd.

5.1.13. Intas Pharmaceuticals

5.1.14. Himalaya Animal Healthcare

5.1.15. Zoivane Livestock

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, R&D Investments, Geographical Presence, Strategic Collaborations)

5.3. Market Share Analysis

5.4. Strategic Initiatives (New Product Launches, Partnerships, Collaborations, Geographical Expansion)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6. India Veterinary Healthcare Market Regulatory Framework

6.1. Animal Health Standards (Mandatory Vaccinations, Disease Control)

6.2. Compliance Requirements for Veterinary Pharmaceuticals

6.3. Certification Processes for Veterinary Products and Services

7. India Veterinary Healthcare Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Veterinary Healthcare Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Animal Type (In Value %)

8.3. By Mode of Delivery (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9. India Veterinary Healthcare Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step in our research methodology is to identify the key variables influencing the India veterinary healthcare market. This includes comprehensive desk research to gather information from industry stakeholders like veterinary clinics, pharmaceutical companies, and regulatory bodies. Market drivers, challenges, and opportunities are identified during this phase.

Step 2: Market Analysis and Construction

During this phase, historical data is analyzed to understand market penetration and trends. We gather data on veterinary services, pharmaceutical sales, and diagnostic tool adoption in both urban and rural regions of India. This helps construct a reliable and accurate market forecast.

Step 3: Hypothesis Validation and Expert Consultation

We validate our findings through consultations with industry experts, including veterinarians and professionals from leading pharmaceutical companies. This provides insight into market dynamics and the practical aspects of veterinary healthcare.

Step 4: Research Synthesis and Final Output

Finally, we compile the research and provide detailed insights into the India veterinary healthcare market. The data from interviews and expert consultations are cross-verified with secondary sources to ensure accuracy.

Frequently Asked Questions

01. How big is India Veterinary Healthcare Market?

The India veterinary healthcare market is valued at USD 500 million, driven by the rising demand for animal health solutions, growing pet ownership, and the need for better livestock care.

02. What are the key challenges in India Veterinary Healthcare Market?

The key challenges include high costs of veterinary drugs and diagnostics, lack of advanced veterinary infrastructure in rural areas, and limited access to modern healthcare solutions for animals.

03. Who are the major players in India Veterinary Healthcare Market?

Major players in the market include Zoetis Inc., Merck Animal Health, Hester Biosciences, Indian Immunologicals, and Virbac, all of which have a strong presence due to their extensive product portfolios and market reach.

04. What are the growth drivers of India Veterinary Healthcare Market?

Growth drivers include the rising awareness of animal health, increasing pet ownership, expanding livestock farming, and advancements in veterinary diagnostics and pharmaceuticals.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.