Indonesia Beer and Cider Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD5968

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD5968

November 2024

88

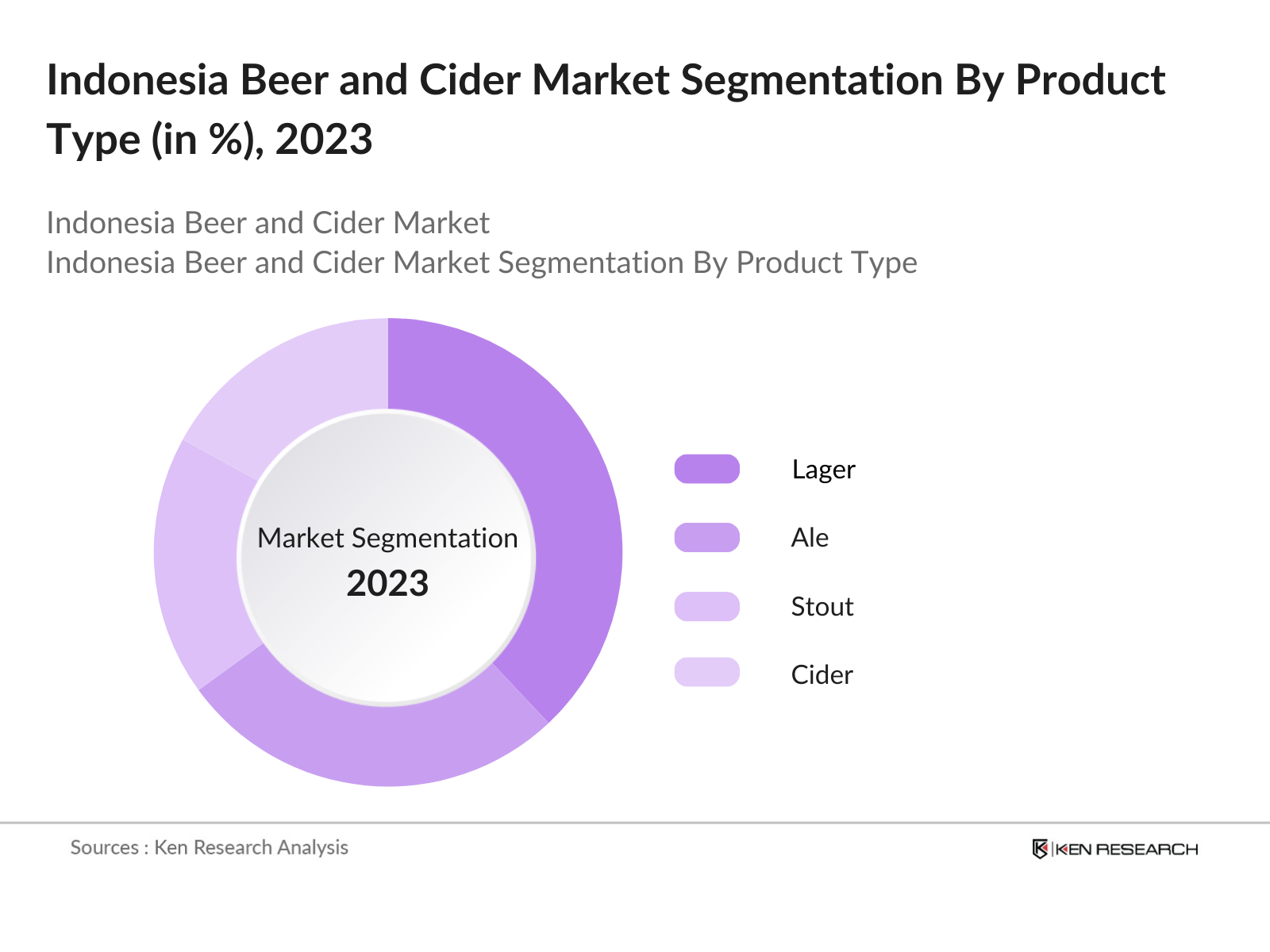

By Product Type: The Indonesia Beer and Cider market is segmented by product type into Lager, Ale, Stout, Cider, and Craft Beer. Craft Beer has gained a dominant market share due to the increasing consumer preference for premium, artisanal beverages. Local breweries are gaining traction by offering unique flavors that resonate with consumers seeking something different from mass-market beers. With increasing disposable income, consumers are more willing to spend on high-quality craft beers, pushing this sub-segment to the forefront of the market.

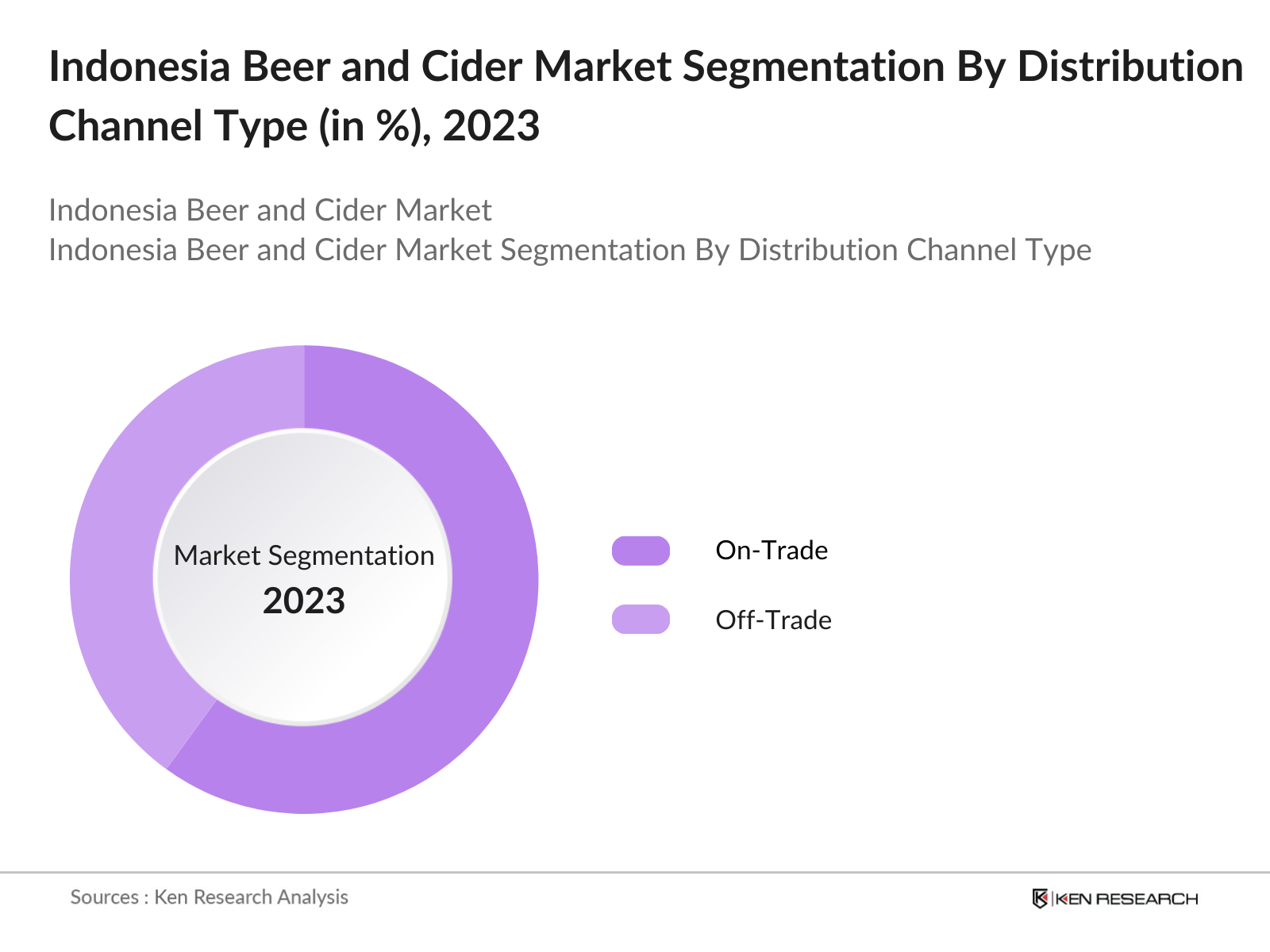

By Distribution Channel: The market is also segmented by distribution channel into On-Trade and Off-Trade. The On-Trade segment, which includes bars, restaurants, and hotels, holds a dominant share of the market. This is due to the strong presence of tourist-heavy regions such as Bali and Jakarta, where the hospitality sector thrives. Tourists and local consumers alike enjoy these beverages in social settings, driving sales. Additionally, premium products are often preferred in these settings, contributing to the higher market share of the On-Trade segment.

The Indonesia Beer and Cider market is highly competitive with the presence of both global and local players. Global brands like Heineken and Anheuser-Busch have established strong footholds in the market, leveraging their extensive distribution networks and brand recognition. Local players such as PT Multi Bintang Indonesia also play a crucial role, particularly with their deep understanding of local consumer preferences and cultural nuances.

The Indonesia Beer and Cider market is expected to show significant growth over the next five years. Increasing disposable income, continued tourism growth, and a rising preference for premium and craft beers are anticipated to drive the market further. Additionally, innovations in flavor profiles, packaging, and distribution methods will help cater to the growing demand among younger, affluent consumers. The expansion of e-commerce channels will also play a significant role in increasing the reach of these products, particularly among urban populations.

|

Product Type |

Lager Ale Stout Cider Craft Beer |

|

Distribution Channel |

On-Trade Off-Trade |

|

Alcohol Content |

Low-Alcohol/Non-Alcoholic Regular Alcohol |

|

Consumer Demographics |

Millennials Generation X Baby Boomers |

|

Region |

Java Bali Sumatra Kalimantan Sulawesi |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Urbanization Impact on Beer and Cider Consumption

3.1.2. Rising Disposable Income and Middle-Class Expansion

3.1.3. Tourism Growth Driving Alcoholic Beverage Demand

3.1.4. Increasing Demand for Premium and Craft Beers

3.2. Market Challenges

3.2.1. Stringent Alcohol Regulations (Licensing Restrictions, Import Duties)

3.2.2. Competition from Traditional Beverages (Arak, Tuak)

3.2.3. High Operational Costs (Supply Chain, Raw Materials)

3.3. Opportunities

3.3.1. Expanding E-commerce Distribution Channels

3.3.2. Rising Health Consciousness and Low-Alcohol Beverages

3.3.3. Craft Beer and Cider Innovations (Flavored Variants, Local Ingredients)

3.4. Trends

3.4.1. Shift to Premium and Luxury Beers and Ciders

3.4.2. Consumer Preference for Sustainability (Eco-friendly Packaging, Local Sourcing)

3.4.3. Growth of Cider Segment Among Younger Consumers

3.5. Government Regulation

3.5.1. Alcohol Production and Distribution Licensing

3.5.2. Tax Policies on Alcoholic Beverages

3.5.3. Import Restrictions and Quotas on Alcoholic Products

3.5.4. Marketing and Advertising Restrictions

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Brewers, Distributors, Retailers)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Lager

4.1.2. Ale

4.1.3. Stout

4.1.4. Cider

4.1.5. Craft Beer

4.2. By Distribution Channel (In Value %)

4.2.1. On-Trade (Bars, Restaurants)

4.2.2. Off-Trade (Supermarkets, Liquor Stores, E-Commerce)

4.3. By Alcohol Content (In Value %)

4.3.1. Low-Alcohol/Non-Alcoholic

4.3.2. Regular Alcohol Content

4.4. By Consumer Demographics (In Value %)

4.4.1. Millennials

4.4.2. Generation X

4.4.3. Baby Boomers

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Bali

4.5.3. Sumatra

4.5.4. Kalimantan

4.5.5. Sulawesi

5.1.1. PT Multi Bintang Indonesia

5.1.2. PT Delta Djakarta Tbk

5.1.3. Heineken N.V.

5.1.4. Anheuser-Busch InBev

5.1.5. Carlsberg Group

5.1.6. Diageo PLC

5.1.7. PT Bali Hai Brewery Indonesia

5.1.8. PT Muria Sumba Manis

5.1.9. Sabeco (Saigon Beer-Alcohol-Beverage Corporation)

5.1.10. Asahi Breweries, Ltd.

5.1.11. Kirin Holdings Company, Limited

5.1.12. San Miguel Corporation

5.1.13. PT Dima Indonesia

5.1.14. Siam Winery Trading Plus Co., Ltd.

5.1.15. Diageo Indonesia

5.2. Cross Comparison Parameters (Revenue, Market Share, Distribution Network, Product Portfolio, Sustainability Initiatives, Pricing Strategy, Consumer Engagement, R&D Investments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Incentives and Support

5.8. Venture Capital and Private Equity Funding

6.1. Alcoholic Beverage Taxation Policies

6.2. Import Quotas and Duties

6.3. Compliance with Health and Safety Standards

6.4. Alcohol Labeling and Advertising Restrictions

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Alcohol Content (In Value %)

8.4. By Consumer Demographics (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial phase involved constructing a comprehensive ecosystem map of the Indonesia Beer and Cider Market, identifying key stakeholders like manufacturers, distributors, and consumers. Desk research using secondary and proprietary databases helped gather insights into market dynamics and trends.

Historical data was compiled and analyzed to understand market penetration, key revenue streams, and major product categories. This step involved evaluating distribution networks, pricing trends, and consumption patterns to ensure an accurate market size assessment.

Hypotheses regarding market drivers and challenges were validated through interviews with industry experts, including executives from leading beer and cider manufacturers and distributors. These consultations provided firsthand insights into the market landscape.

The final phase synthesized primary data with secondary research to develop detailed insights into product segmentation, market competition, and consumer preferences. The data was further validated by interacting with local brewers and distributors to ensure comprehensive market coverage.

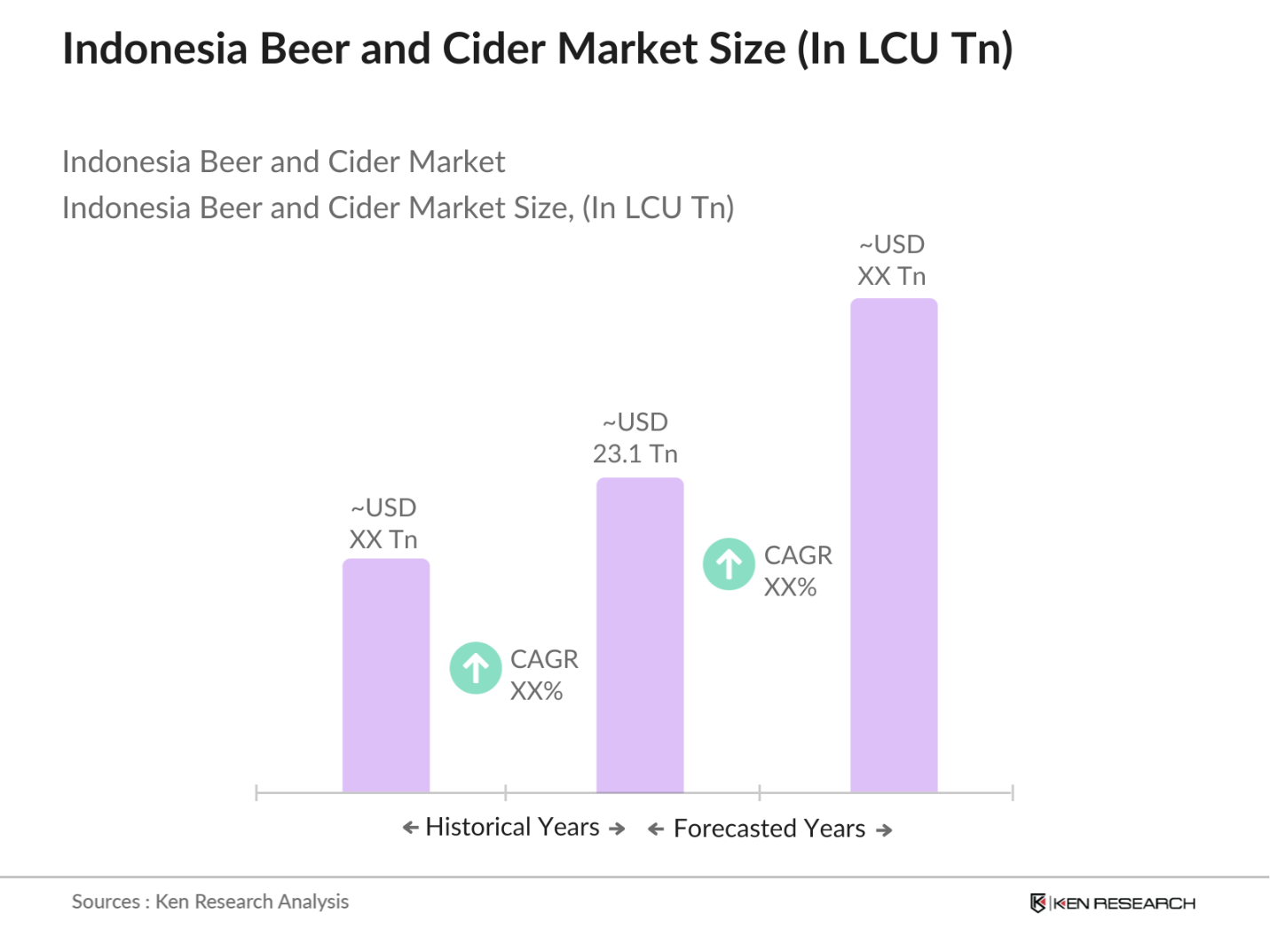

The Indonesia Beer and Cider market is valued at USD LCU23.1 Trillion, driven by factors like rising disposable income, increased tourism, and growing demand for premium alcoholic beverages.

Challenges include stringent government regulations on alcohol distribution and sales, high import duties on foreign brands, and competition from traditional beverages like Arak and Tuak.

Major players include PT Multi Bintang Indonesia, Heineken N.V., Anheuser-Busch InBev, Carlsberg Group, and Diageo PLC. These companies dominate due to their strong distribution networks and established consumer bases.

The market is driven by rising consumer interest in premium and craft beers, growing tourism, and increased disposable income among urban consumers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.