KSA Food Safety Testing Market Outlook to 2030

Region:Middle East

Author(s):Shubham Kashyap

Product Code:KROD3691

Region:Middle East

Author(s):Shubham Kashyap

Product Code:KROD3691

November 2024

99

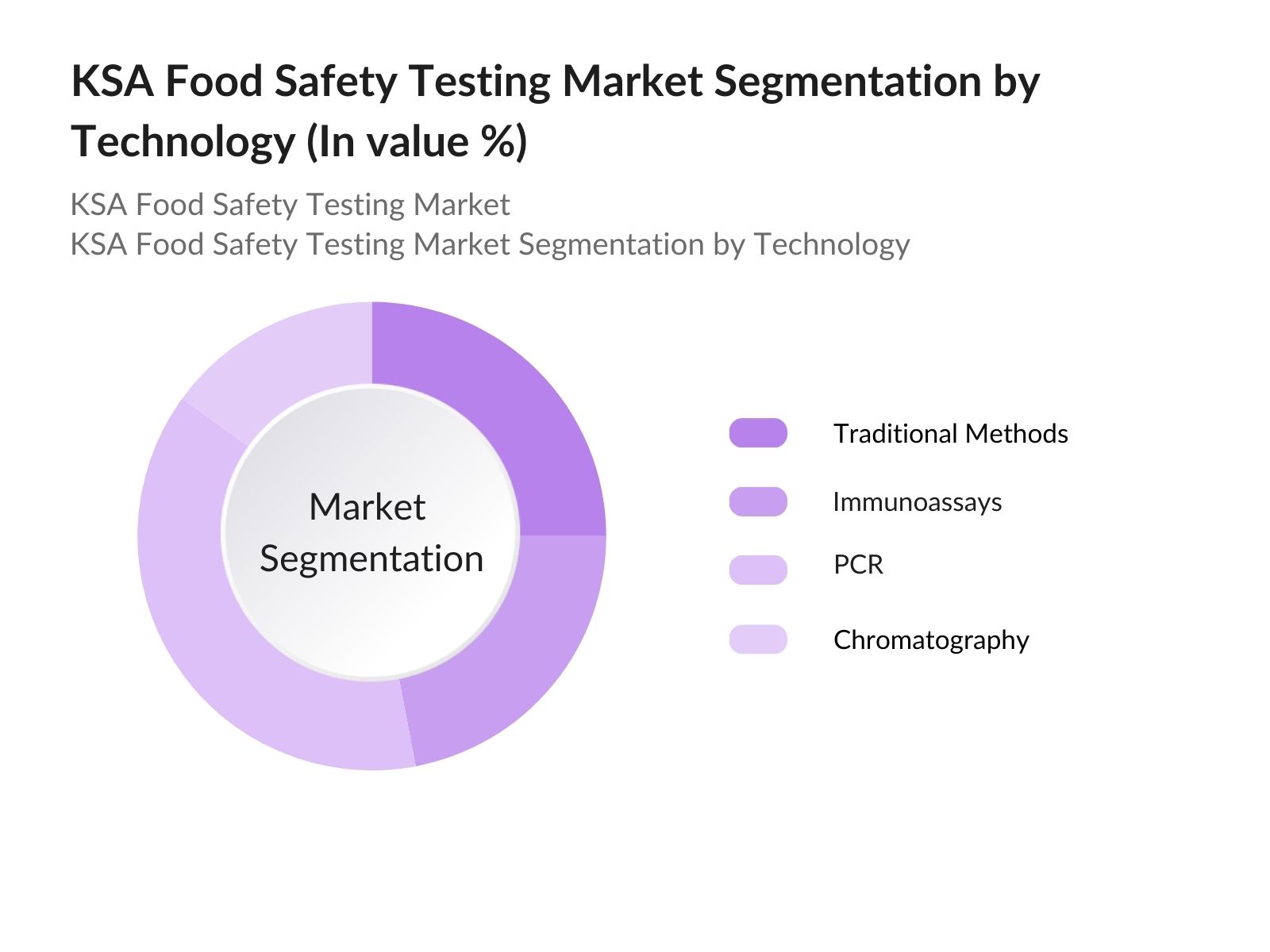

By Technology: The market is also segmented by technology into traditional methods, immunoassays, PCR (Polymerase Chain Reaction), and chromatography. PCR technology holds the largest market share due to its high accuracy in detecting microbial contaminants and genetically modified organisms (GMOs). Its ability to provide quick and reliable results has made it the preferred choice for laboratories across the Kingdom, particularly in testing for pathogens in both imported and domestically produced food products.

The KSA food safety testing market is competitive, with both global and local players offering a wide range of services. Major companies in this sector include Eurofins Scientific, SGS, and Bureau Veritas, which have established a strong presence in KSA by providing comprehensive testing services and state-of-the-art laboratories.

Local companies, such as Saudi Specialized Laboratories (Motabaqah), play a key role in the market by offering tailored testing services that cater specifically to the needs of the KSA market. These companies benefit from deep knowledge of local regulations and closer proximity to domestic food producers and suppliers.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

No. of Employees |

Key Services |

R&D Investment |

Major Clients |

Laboratory Locations |

|

Eurofins Scientific |

1987 |

Luxembourg |

||||||

|

SGS |

1878 |

Switzerland |

||||||

|

Bureau Veritas |

1828 |

France |

||||||

|

Saudi Specialized Labs |

2001 |

Saudi Arabia |

||||||

|

Intertek Group |

1885 |

United Kingdom |

Growth Drivers:

Market Challenges:

The KSA food safety testing market is poised for significant growth over the forecast period, driven by the increasing awareness of foodborne illnesses, government regulations, and the demand for safe and high-quality food products. The governments Vision 2030 initiative, which emphasizes public health and food security, will continue to shape the markets future direction.

Future Market Opportunities:

|

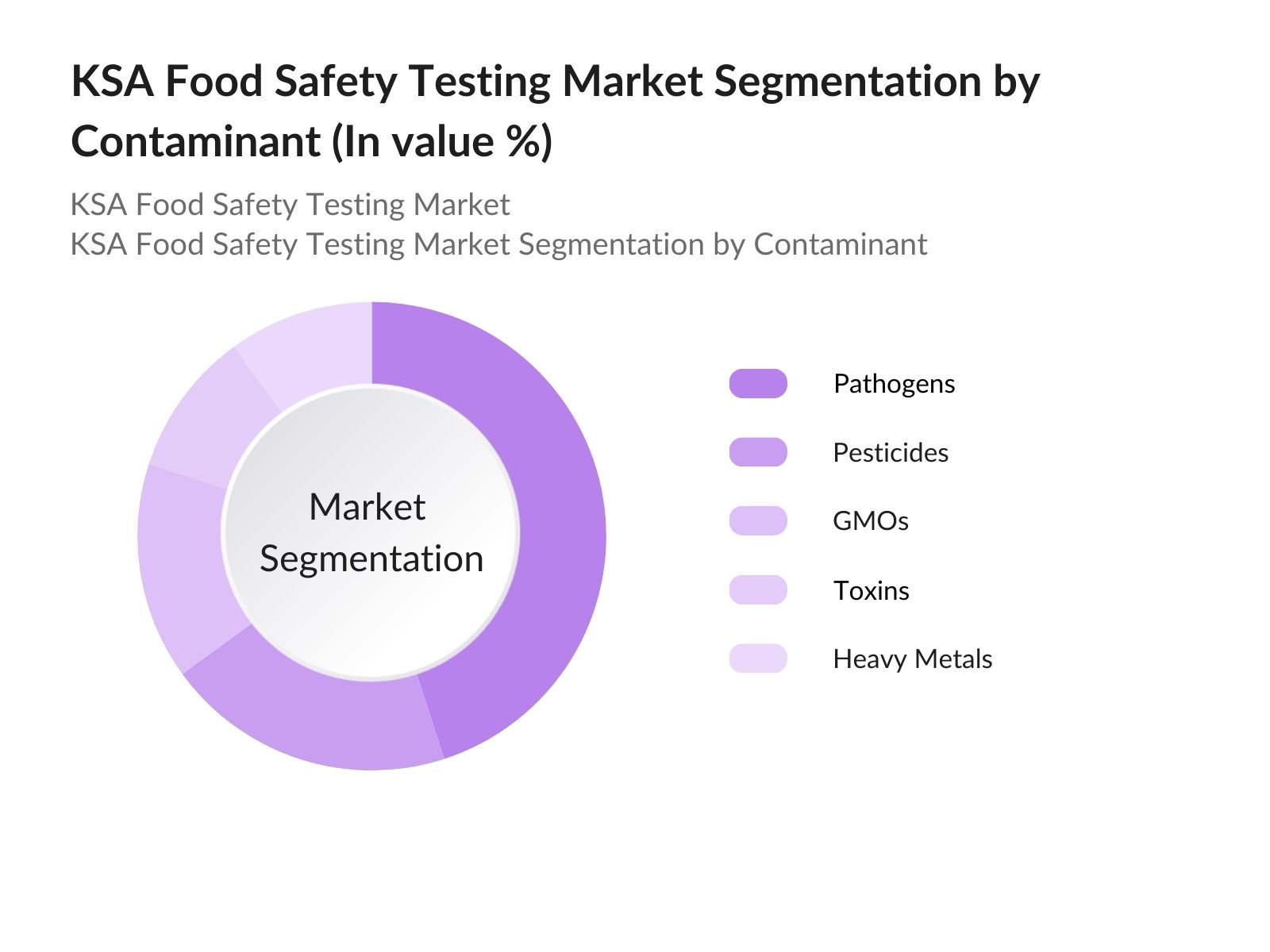

By Contaminant Type |

Pathogens Pesticides Genetically Modified Organisms (GMOs) Toxins Heavy Metals |

|

By Technology |

Traditional Methods Immunoassays Polymerase Chain Reaction (PCR) Chromatography |

|

By Food Tested |

Meat and Poultry Dairy Products Processed Foods Fruits and Vegetables Seafood |

|

By End-User |

Food Manufacturers Food Retailers Testing Laboratories Government Agencies |

|

By Region |

Riyadh Jeddah Dammam Mecca Eastern Province |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rise in Foodborne Illnesses (Contamination Detection)

3.1.2. Regulatory Compliance (SFDA Regulations)

3.1.3. Technological Advancements in Testing (PCR, Chromatography, Immunoassays)

3.1.4. Government Support and Vision 2030 (Food Security Initiative)

3.2. Market Challenges

3.2.1. High Cost of Testing Equipment (Cost-Effectiveness and Accessibility)

3.2.2. Lack of Skilled Workforce (Need for Specialized Technicians)

3.2.3. Complex Regulatory Environment (International Standards Compliance)

3.3. Opportunities

3.3.1. Expansion of Local Testing Facilities (Infrastructure Development)

3.3.2. Growing Demand for Processed Foods (Processed Foods Market Growth)

3.3.3. Increasing Focus on Allergen and Heavy Metal Testing (Emerging Contaminants)

3.4. Trends

3.4.1. Adoption of AI and Automation in Testing (Smart Labs)

3.4.2. Increased Collaboration Between Laboratories and Government (Public-Private Partnerships)

3.4.3. Shift Towards Rapid Testing Solutions (On-Site Testing)

3.5. Government Regulations

3.5.1. SFDA Regulations and Compliance Requirements

3.5.2. Vision 2030 and Food Safety Strategy (National Initiatives)

3.5.3. Certification and Quality Assurance (ISO Standards)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

4.1. By Contaminant Type (In Value %)

4.1.1. Pathogens

4.1.2. Pesticides

4.1.3. Genetically Modified Organisms (GMOs)

4.1.4. Toxins

4.1.5. Heavy Metals

4.2. By Technology (In Value %)

4.2.1. Traditional Methods

4.2.2. Immunoassays

4.2.3. Polymerase Chain Reaction (PCR)

4.2.4. Chromatography

4.3. By Food Tested (In Value %)

4.3.1. Meat and Poultry

4.3.2. Dairy Products

4.3.3. Processed Foods

4.3.4. Fruits and Vegetables

4.3.5. Seafood

4.4. By End-User (In Value %)

4.4.1. Food Manufacturers

4.4.2. Food Retailers

4.4.3. Testing Laboratories

4.4.4. Government Agencies

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Dammam

4.5.4. Mecca

4.5.5. Eastern Province

5.1. Detailed Profiles of Major Companies

5.1.1. Eurofins Scientific

5.1.2. SGS

5.1.3. Bureau Veritas

5.1.4. Saudi Specialized Laboratories (Motabaqah)

5.1.5. Intertek Group

5.1.6. ALS Limited

5.1.7. Merieux NutriSciences

5.1.8. Romer Labs

5.1.9. TV SD

5.1.10. EnviroLogix

5.1.11. NSF International

5.1.12. Microbac Laboratories

5.1.13. FoodChain ID

5.1.14. Neogen Corporation

5.1.15. Agilent Technologies

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Market Share, Laboratory Capacity, R&D Investments, Regional Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Food Safety Standards (SFDA Regulations, ISO Certifications)

6.2. Compliance Requirements (Mandatory Testing, Product Recall Procedures)

6.3. Certification Processes (Laboratory Accreditation, Third-Party Certification)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Government Regulations, Rising Consumer Awareness, Technological Innovation)

8.1. By Contaminant Type

8.2. By Technology

8.3. By Food Tested

8.4. By End-User

8.5. By Region

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

This initial step involves identifying critical market variables such as regulatory frameworks, key players, and testing technologies. Extensive desk research, including data from proprietary databases and secondary sources, is conducted to establish an industry-level ecosystem for the KSA food safety testing market.

Historical data on market growth, technology adoption, and food safety incidents is analyzed to construct a detailed market model. This phase also examines testing capacities, service provider statistics, and demand drivers within the food industry.

Market assumptions and hypotheses are validated through interviews and consultations with industry professionals, including laboratory managers and food safety experts. These consultations provide operational insights that refine our market estimates.

In this final stage, collected data is synthesized into actionable insights. A bottom-up approach is used to ensure comprehensive market analysis, validated through direct feedback from industry stakeholders and food manufacturers.

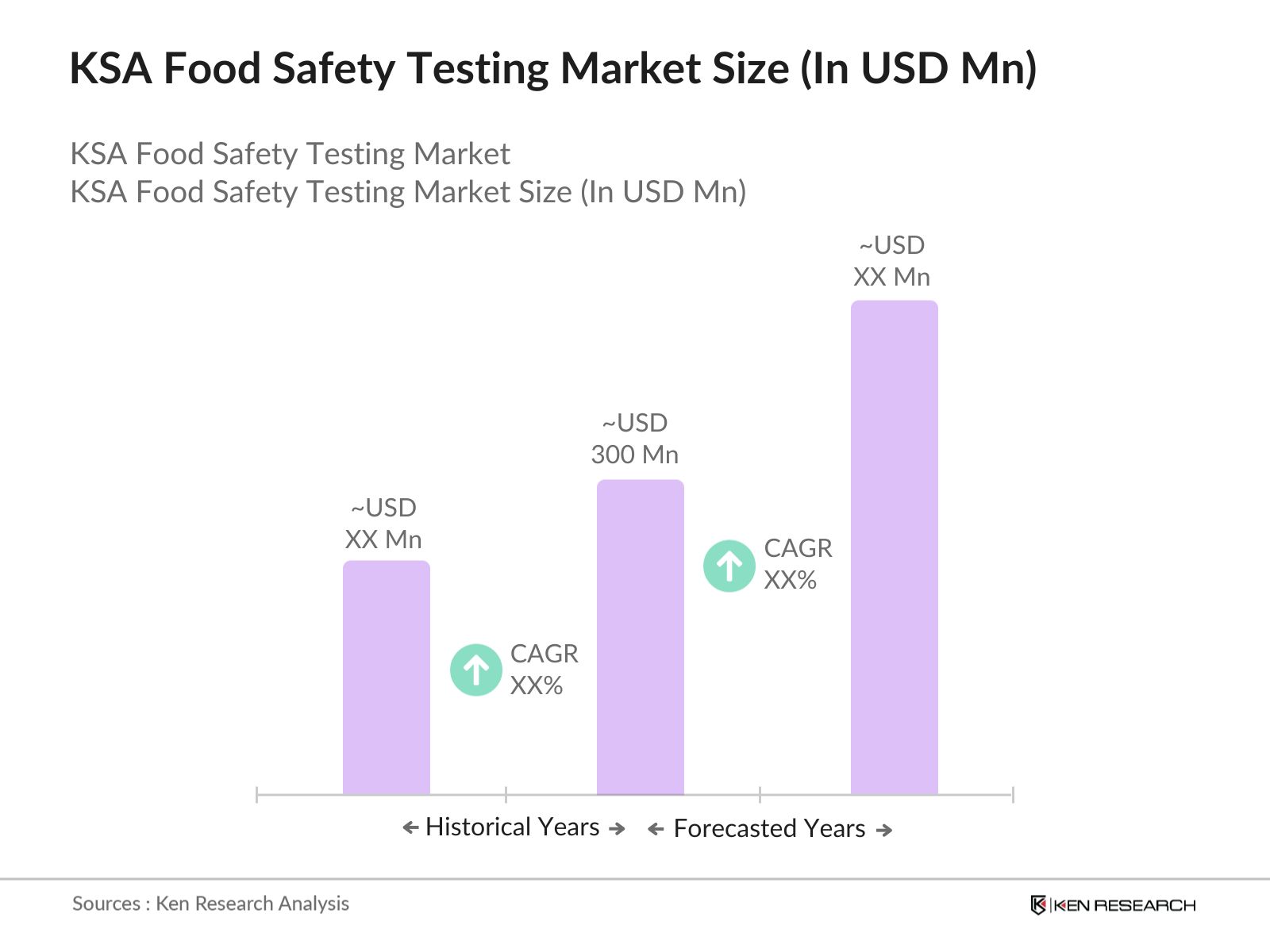

The KSA food safety testing market is valued at USD 300 million, driven by stringent regulations, increasing food imports, and the adoption of advanced testing technologies.

Challenges in the KSA food safety testing market include the high cost of testing equipment, a shortage of skilled technicians, and the complex regulatory environment which requires compliance with both national and international food safety standards.

Key players in the KSA food safety testing market include Eurofins Scientific, SGS, Bureau Veritas, Saudi Specialized Laboratories (Motabaqah), and Intertek Group, dominating the market due to their advanced laboratory infrastructure and compliance with SFDA regulations.

KSA food safety testing market growth is driven by increasing consumer awareness, rising food imports, government initiatives under Vision 2030, and the rapid adoption of advanced testing technologies like PCR and immunoassays.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.