KSA Hydrogen Energy Storage Market Outlook to 2030

Region:Middle East

Author(s):Vijay Kumar

Product Code:KROD3789

December 2024

81

About the Report

KSA Hydrogen Energy Storage Market Overview

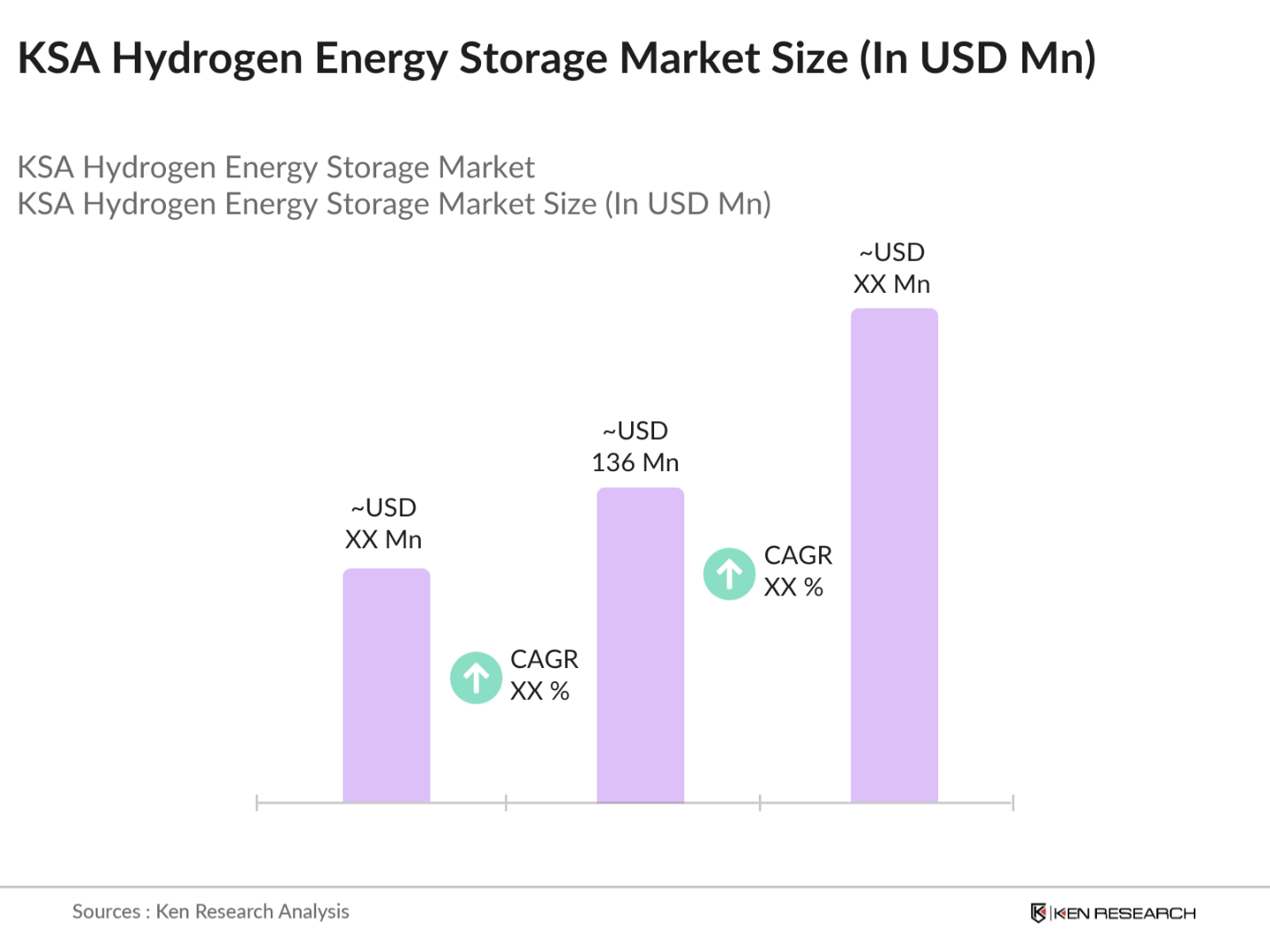

- The KSA hydrogen energy storage market is valued at USD 136 million, based on a five-year historical analysis. This market is driven by the Kingdoms increasing focus on diversifying its energy sources and reducing its dependency on crude oil. The growth is primarily supported by large-scale investments in renewable energy projects such as NEOMs green hydrogen facility and other hydrogen-based industrial applications, aimed at meeting the goals outlined in Saudi Vision 2030. The markets expansion is further bolstered by favorable government policies promoting green hydrogen production and storage, as well as strategic partnerships with global energy leaders

- Key cities driving the market growth include Riyadh and the Eastern Province, due to their strategic locations and the presence of major industrial and energy infrastructures. Riyadh, being the administrative capital, is central to decision-making and policy formulation, while the Eastern Province, home to the oil and gas industry, is now diversifying into renewable energy storage solutions. This dominance is also facilitated by strong investments in infrastructure and research hubs in these regions.

- Saudi Arabias Vision 2030 has positioned hydrogen storage as a central element in the countrys energy transition strategy. In 2024, the government announced the integration of hydrogen storage solutions within its existing natural gas infrastructure to enhance energy security and reduce emissions. This integration is backed by investments of over 10 billion USD into hydrogen research and storage projects, making Saudi Arabia a leader in hydrogen adoption within the Middle East.

KSA Hydrogen Energy Storage Market Segmentation

By Technology Type: The KSA hydrogen energy storage market is segmented by technology type into Compression, Liquefaction, and Material-Based Storage. Compression technology currently holds a dominant market share due to its cost-effectiveness and compatibility with existing industrial applications. The market demand for compression technology is driven by its use in storing hydrogen in compressed gas form, which is then used for industrial applications, power generation, and fuel cell vehicles. This technology type has a strong foothold due to the ease of scalability and established infrastructure for transportation and distribution.

By Application Type: The market is further segmented by application type into Transportation, Industrial, and Power Generation. The industrial segment is leading the market, primarily due to the widespread use of hydrogen in petroleum refining and chemical production. In the Kingdom, hydrogen is being increasingly utilized to decarbonize these energy-intensive industries, aligning with the countrys goals to reduce greenhouse gas emissions. Furthermore, the integration of hydrogen storage in industrial applications is supported by ongoing research and development efforts to enhance storage efficiency and lower costs.

KSA Hydrogen Energy Storage Market Competitive Landscape

The KSA hydrogen energy storage market is characterized by a mix of local and global players. The market is consolidated with significant contributions from established players focusing on expanding their green hydrogen capabilities and increasing their R&D investments. The primary competitive strategies include partnerships, technological innovation, and large-scale projects aimed at reducing the cost of hydrogen storage and improving safety measures.

KSA Hydrogen Energy Storage Industry Analysis

Growth Drivers

- Industrial Demand in Refining and Chemical Sectors (Market Drivers): The industrial demand for hydrogen, particularly in the refining and chemical sectors, has seen robust growth due to increased global economic activities and energy transitions. In 2024, advanced economies like the United States and Europe showed stable manufacturing outputs, which remained crucial for hydrogen consumption. For instance, the World Economic Outlook projected that the global output for advanced economies will be around 3.0 trillion USD in 2024.

- Adoption of Green Hydrogen Technologies (Technology Trend): The adoption of green hydrogen technologies is primarily driven by decarbonization efforts and increased renewable energy integration. As of 2024, renewable energy accounted for over 35% of total energy generation in several advanced economies, such as Germany and Japan, supporting the production of green hydrogen through electrolysis. The transition to low-carbon hydrogen is further bolstered by government subsidies and technological advancements, leading to the establishment of over 150 hydrogen production projects worldwide in 2024.

- Government Initiatives and Support (Policy Support): Government initiatives such as the European Unions Green Deal and the US Inflation Reduction Act of 2022 have provided considerable financial support for hydrogen infrastructure. These policies have resulted in increased funding and subsidies for hydrogen storage, production, and distribution networks, with the EU allocating nearly 20 billion Euros in 2024 for hydrogen projects. Similarly, the US has committed to investing in hydrogen hubs, aiming to deploy over 10 hydrogen production facilities by 2025.

Market Challenges

- High Storage and Conversion Costs: The high costs associated with hydrogen storage and conversion remain significant barriers to widespread adoption. Storing hydrogen as a liquid or compressed gas requires expensive materials and infrastructure, with storage systems costing between 200 to 400 USD per kilogram in 2024. This cost is a major factor limiting large-scale implementation, especially in emerging markets where economic constraints are more pronounced.

- Technical Barriers in Hydrogen Storage and Distribution: Technical barriers such as hydrogen embrittlement, leakage, and low volumetric density complicate its storage and distribution. In 2024, research by global institutions indicated that over 10% of hydrogen produced is lost during transport and storage due to leakage and inefficient containment. Furthermore, specialized materials and technologies required to store and transport hydrogen safely add to the operational costs and complexity.

KSA Hydrogen Energy Storage Market Future Outlook

Over the next five years, the KSA hydrogen energy storage market is poised for significant growth, driven by continuous government support, the advancement of hydrogen technologies, and increasing investments in renewable energy projects. The Kingdoms strategic initiatives under Vision 2030 and the National Renewable Energy Program (NREP) aim to position Saudi Arabia as a leading hub for hydrogen energy production and storage in the Middle East. The market is expected to see heightened activity in green hydrogen projects, including partnerships with international firms to develop large-scale hydrogen storage solutions.

Market Opportunities

- Increasing Adoption in Power-to-Gas Projects: The adoption of hydrogen in Power-to-Gas (P2G) projects is on the rise, as countries seek to enhance energy storage and grid stability. As of 2024, Europe has over 50 operational P2G plants, with combined energy storage capacity exceeding 1,000 GWh. These projects enable the conversion of excess renewable energy into hydrogen, which can then be stored or re-injected into the gas grid. The trend towards P2G is supported by regulatory incentives and infrastructure investments, positioning hydrogen as a key element in future energy systems.

- Expansion of Hydrogen-Based Fuel Cell Applications: Fuel cell technology is gaining traction, particularly in transportation and stationary power generation. By 2024, over 70,000 fuel cell electric vehicles (FCEVs) were on the road globally, predominantly in regions like Japan, South Korea, and California, where infrastructure support and government incentives are in place. The expansion of hydrogen refueling stations, which increased to 1,000 worldwide in 2024, supports the growth of the FCEV market, reflecting a significant opportunity for hydrogen adoption in clean mobility solutions.

Scope of the Report

|

By Technology |

Compression Liquefaction Material-Based |

|

By Application |

Transportation Industrial Power Generation Residential Commercial |

|

By Physical State |

Solid Liquid Gas |

|

By Storage Solution |

On-Site Hydrogen Storage Pipeline Transportation Container-Based |

|

By Region |

Central Western Eastern Northern Southern |

Products

Key Target Audience

Government and Regulatory Bodies (Ministry of Energy, Saudi Industrial Development Fund)

Utility Companies

Hydrogen Production Companies

Industrial Hydrogen Consumers (Petroleum Refining, Chemicals)

Energy Storage Solution Providers

Renewable Energy Project Developers

Investments and Venture Capitalist Firms

Automotive Manufacturers focusing on Fuel Cell Vehicles

Companies

Players Mentioned in the Report

Air Liquide

Saudi Aramco

Linde PLC

ACWA Power

Mitsubishi Heavy Industries

Shell Hydrogen

ENGIE

Cummins Inc.

Xcel Energy Inc.

Nel ASA

Table of Contents

1. Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Dynamics Overview

1.4 Market Growth Rate and Forecast

2. KSA Hydrogen Energy Storage Market Size (USD Million)

2.1 Historical Market Size

2.2 Current Market Size

2.3 Year-on-Year Growth Analysis

2.4 Key Market Milestones and Developments

3. Market Analysis

3.1 Growth Drivers

3.1.1 Industrial Demand in Refining and Chemical Sectors (Market Drivers)

3.1.2 Adoption of Green Hydrogen Technologies (Technology Trend)

3.1.3 Government Initiatives and Support (Policy Support)

3.2 Market Challenges

3.2.1 High Storage and Conversion Costs

3.2.2 Technical Barriers in Hydrogen Storage and Distribution

3.2.3 Safety Concerns and Regulatory Hurdles

3.3 Market Opportunities

3.3.1 Increasing Adoption in Power-to-Gas Projects

3.3.2 Expansion of Hydrogen-Based Fuel Cell Applications

3.4 Market Trends

3.4.1 Deployment of Hydrogen Storage in Large-Scale Industrial Applications

3.4.2 Rising Use of Material-Based Hydrogen Storage Technologies

3.5 Regulatory Framework

3.5.1 Saudi Vision 2030: Hydrogen Storage Integration (Energy Policy)

3.5.2 Renewable Energy Targets for Hydrogen-Based Systems (Renewable Integration)

3.6 SWOT Analysis (Strengths, Weaknesses, Opportunities, and Threats)

3.7 Stakeholder Ecosystem Analysis

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape Overview

4. Market Segmentation

4.1 By Technology (In Value %)

4.1.1 Compression

4.1.2 Liquefaction

4.1.3 Material-Based (Solid, Liquid, and Gas)

4.2 By Application (In Value %)

4.2.1 Transportation

4.2.2 Industrial (Petroleum Refining, Chemical Production)

4.2.3 Power Generation

4.2.4 Residential and Commercial

4.3 By Physical State (In Value %)

4.3.1 Solid State

4.3.2 Liquid State

4.3.3 Gaseous State

4.4 By Storage Solution (In Value %)

4.4.1 On-Site Hydrogen Storage

4.4.2 Pipeline Transportation

4.4.3 Container-Based Storage

4.5 By Region (In Value %)

4.5.1 Central Region (Riyadh, Qassim)

4.5.2 Western Region (Makkah, Medina)

4.5.3 Eastern Region (Dammam, Khobar)

4.5.4 Northern Region (Al Jouf)

4.5.5 Southern Region (Asir)

5. Competitive Analysis

5.1 Detailed Profiles of Major Competitors

5.1.1 Air Liquide

5.1.2 Linde PLC

5.1.3 Air Products and Chemicals, Inc.

5.1.4 Iwatani Corporation

5.1.5 Mitsubishi Heavy Industries, Ltd.

5.1.6 Shell Hydrogen

5.1.7 Saudi Aramco

5.1.8 ACWA Power International

5.1.9 ENGIE

5.1.10 Cummins Inc.

5.1.11 Xcel Energy Inc.

5.1.12 Nel ASA

5.1.13 ITM Power PLC

5.1.14 Plug Power Inc.

5.1.15 H2 Mobility

6. Cross Comparison Parameters (Key Market Metrics)

6.1 Market Share (Value and Volume)

6.2 Revenue by Technology Type

6.3 Production Capacity Utilization

6.4 Innovation Index (Number of Patents, R&D Spend)

6.5 Key Financial Performance Indicators (Profit Margins, Return on Investment)

6.6 Hydrogen Production Capacity by Competitor

6.7 Regional Presence and Distribution

6.8 Strategic Partnerships and Collaborations

7. Investment Analysis

7.1 Venture Capital Funding Analysis

7.2 Mergers and Acquisitions (M&A) Landscape

7.3 Public and Private Equity Investments

7.4 Government Grants and Incentives

7.5 Strategic Initiatives and Expansion Plans

8. KSA Hydrogen Energy Storage Market Regulatory Framework

8.1 Environmental and Safety Standards

8.2 Compliance and Certification Requirements

8.3 Policy Impacts on Hydrogen Storage Projects

8.4 Legal Constraints and Opportunities

9. Future Market Size Projections (USD Million)

9.1 Forecast Market Size and Value

9.2 Key Factors Driving Future Market Growth

10. Future Market Segmentation

10.1 By Technology

10.2 By Application

10.3 By Physical State

10.4 By Storage Solution

10.5 By Region

11. Market Analysts Recommendations

11.1 TAM/SAM/SOM Analysis

11.2 Strategic Business Recommendations

11.3 Key Customer Segments and Value Propositions

11.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial step involves creating a comprehensive ecosystem map of the KSA hydrogen energy storage market, identifying all critical stakeholders. This is achieved through a combination of desk research, industry reports, and proprietary databases to gather relevant information on market drivers, trends, and competitive positioning.

Step 2: Market Analysis and Construction

This phase focuses on compiling and analyzing historical data on market growth and segmentation. A detailed examination of technology adoption and competitive strategies in the hydrogen storage market is conducted, leveraging industry surveys and case studies to build a robust understanding of the market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Through structured interviews and consultations with industry experts, including hydrogen storage manufacturers and energy policymakers, initial market hypotheses are validated. This step ensures that all collected data is accurate and reflective of current market conditions.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing research findings and translating them into actionable insights. This includes a thorough review of market projections, the potential for future growth, and strategic recommendations for market participants. A combination of bottom-up and top-down approaches is employed to ensure the credibility and reliability of the report.

Frequently Asked Questions

01. How big is the KSA Hydrogen Energy Storage Market?

The KSA hydrogen energy storage market is valued at USD 136 million in 2023, driven by significant investments in green hydrogen projects and strategic collaborations.

02. What are the challenges in the KSA Hydrogen Energy Storage Market?

Key challenges include high initial costs of hydrogen storage technologies, safety concerns, and regulatory hurdles. Additionally, the absence of a fully developed hydrogen infrastructure remains a barrier to market expansion.

03. Who are the major players in the KSA Hydrogen Energy Storage Market?

Key players include Air Liquide, Saudi Aramco, Linde PLC, ACWA Power, and Mitsubishi Heavy Industries. These companies dominate due to their strong research and development capabilities and strategic partnerships.

04. What are the growth drivers of the KSA Hydrogen Energy Storage Market?

The market is propelled by government support through initiatives like Vision 2030, increasing industrial applications of hydrogen, and technological advancements in hydrogen storage and distribution systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.