MEA Veterinary Healthcare Market Outlook to 2030

Region:Middle East

Author(s):Vijay Kumar

Product Code:KROD4954

November 2024

95

About the Report

MEA Veterinary Healthcare Market Overview

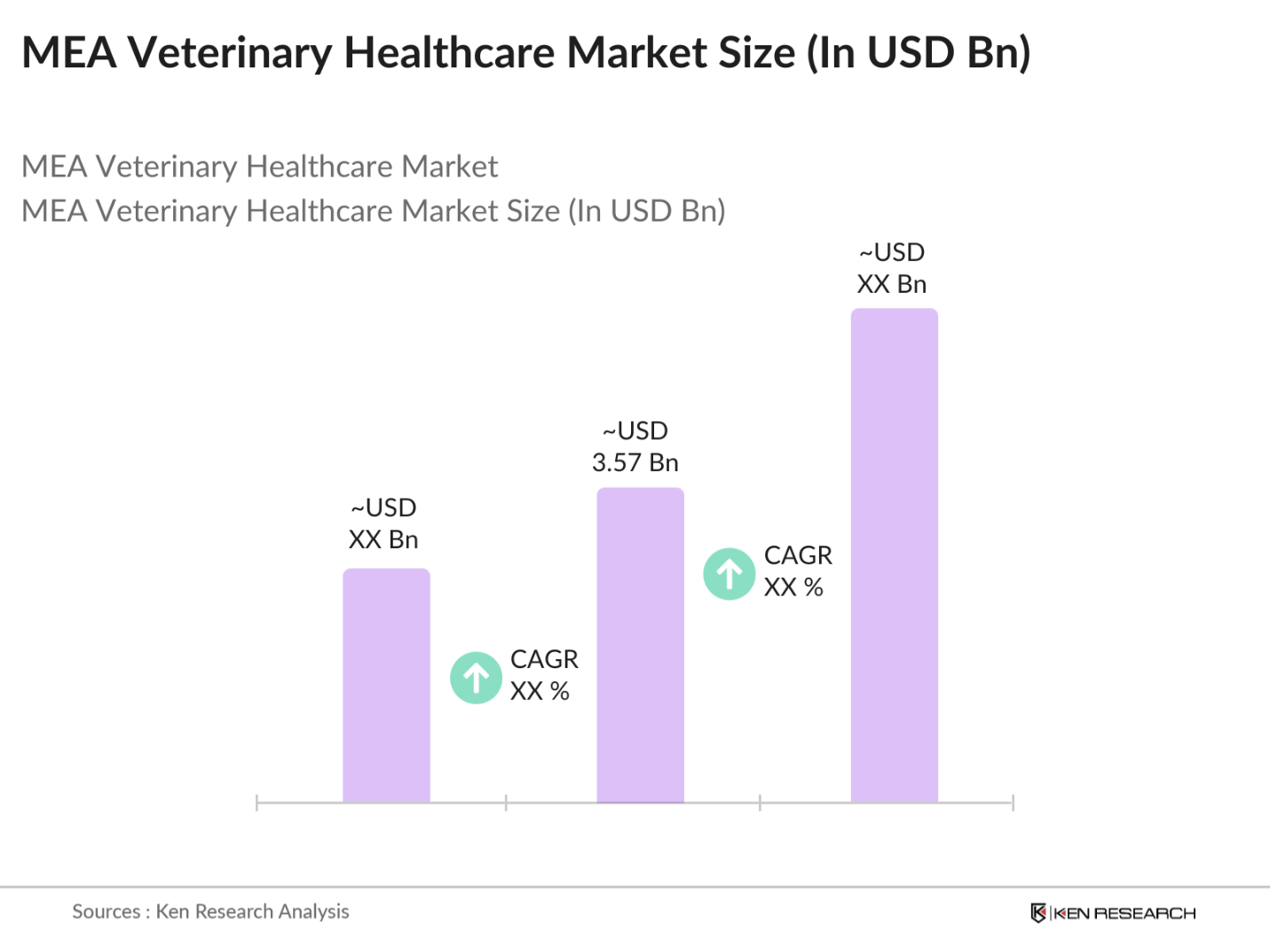

- The Middle East and Africa (MEA) veterinary healthcare market is valued at USD 3.57 billion, based on a five-year historical analysis. This valuation is driven by the increasing demand for animal-derived food products, rising pet ownership, and advancements in veterinary services and pharmaceuticals. The region's growing awareness of animal health and welfare has further propelled market growth.

- Within the MEA region, countries such as the United Arab Emirates (UAE), Saudi Arabia, and South Africa dominate the veterinary healthcare market. This dominance is attributed to their well-established veterinary infrastructure, higher disposable incomes, and a significant population of companion animals. Additionally, these nations have proactive government policies supporting animal health, contributing to their leading positions in the market.

- Governments in the Middle East and Africa (MEA) region are establishing and enforcing veterinary service standards to ensure the quality and safety of animal healthcare. In 2023, the South African Veterinary Council (SAVC) mandated that all veterinary practices adhere to specific operational guidelines, including facility hygiene, equipment maintenance, and staff qualifications, to maintain accreditation. Similarly, the United Arab Emirates' Ministry of Climate Change and Environment (MOCCAE) implemented regulations requiring veterinary clinics to obtain licenses and comply with standardized protocols for animal treatment and welfare.

MEA Veterinary Healthcare Market Segmentation

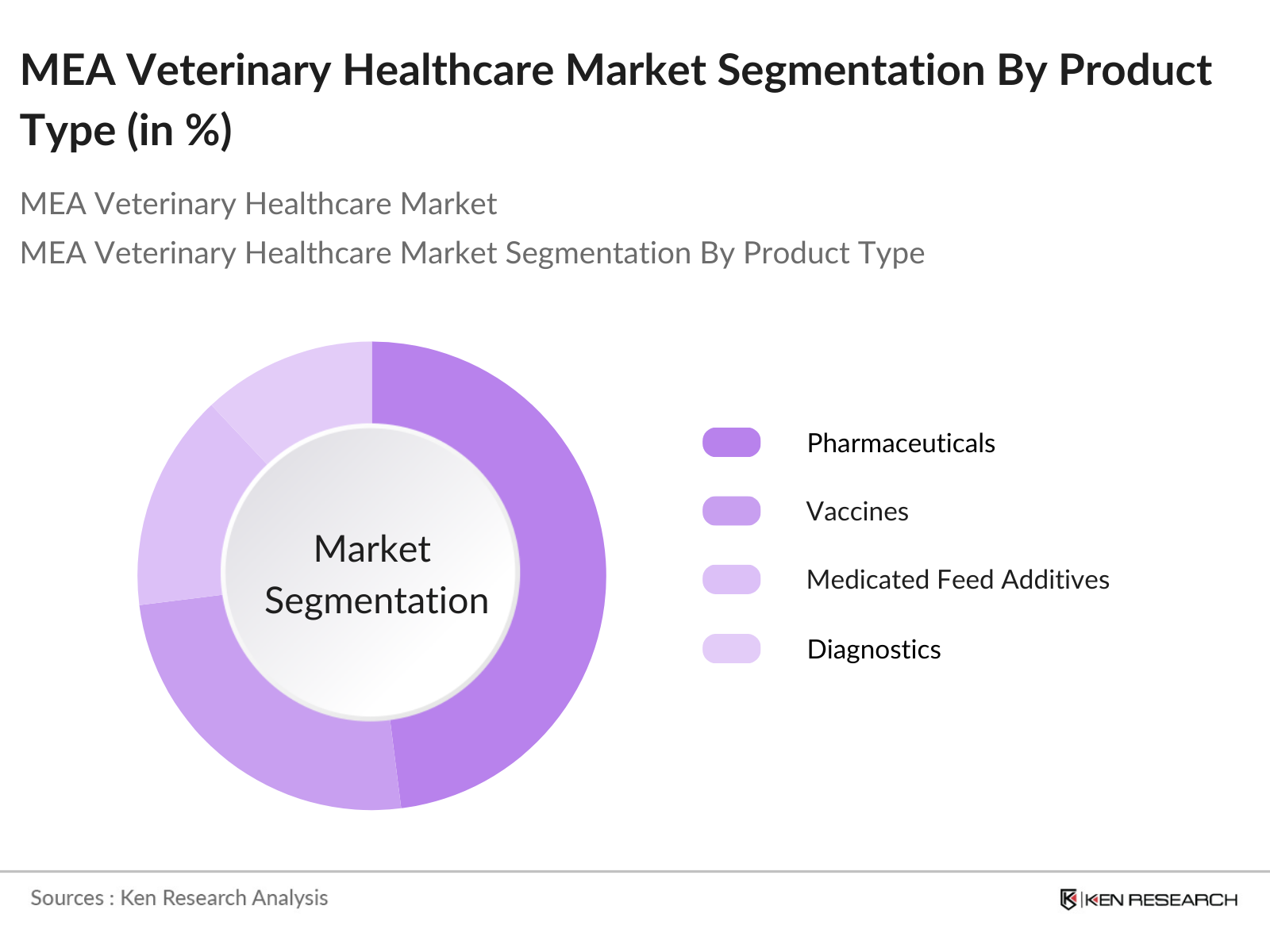

By Product Type: The market is segmented by product type into pharmaceuticals, vaccines, medicated feed additives, diagnostics, and veterinary services. Pharmaceuticals hold a dominant market share in this segmentation, primarily due to the continuous need for therapeutic treatments for various animal diseases. The prevalence of infectious diseases among livestock and companion animals necessitates a steady demand for veterinary drugs, thereby sustaining the prominence of the pharmaceuticals segment.

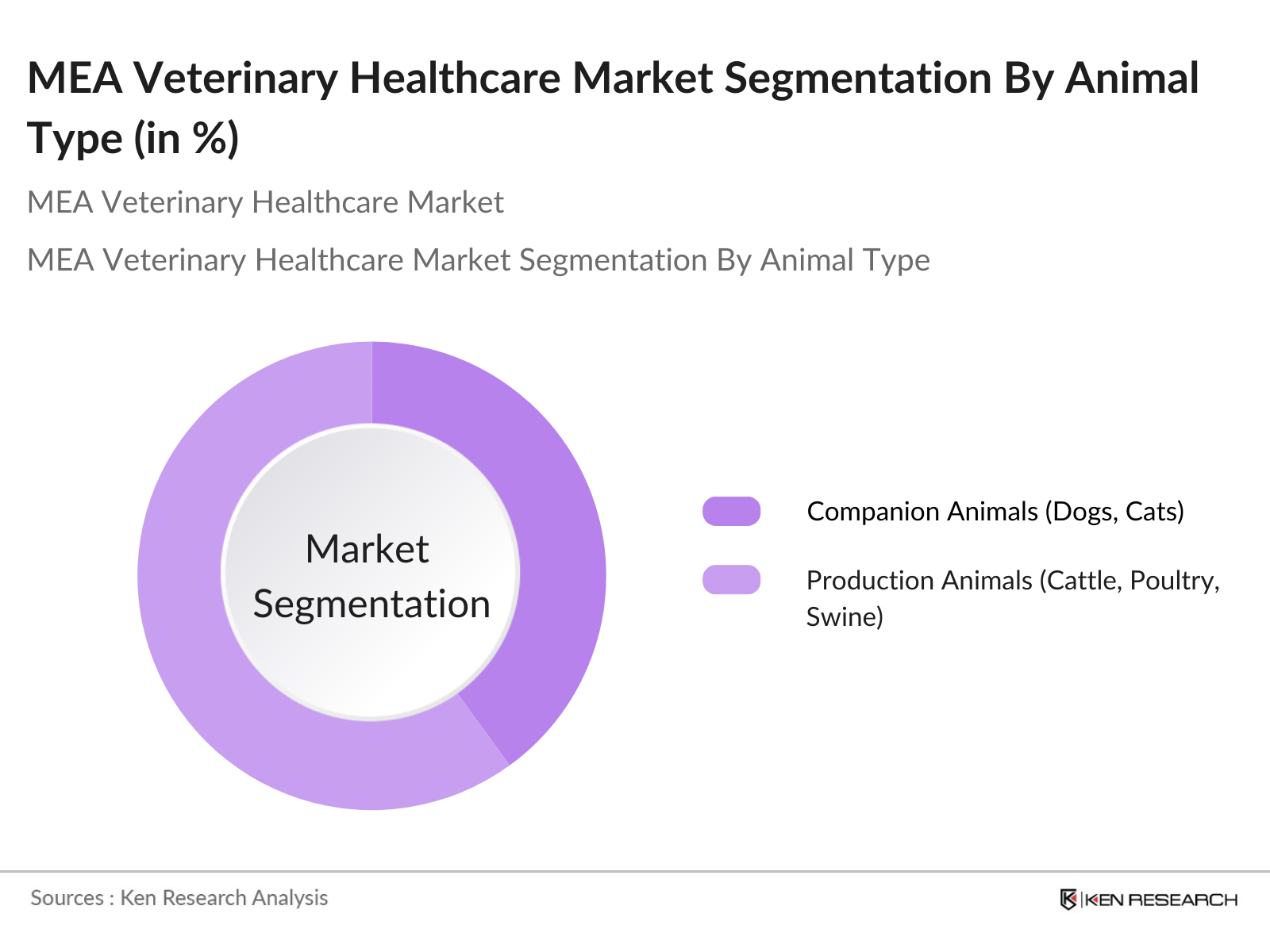

By Animal Type: The market is also segmented by animal type into companion animals (dogs, cats, horses) and production animals (cattle, poultry, swine, sheep, and goats). Production animals account for a larger market share within this segmentation. This is largely due to the region's reliance on livestock for food production, making the health and productivity of these animals crucial. Consequently, there is a substantial investment in veterinary healthcare for production animals to ensure food security and economic stability.

MEA Veterinary Healthcare Market Competitive Landscape

The MEA veterinary healthcare market is characterized by the presence of both multinational corporations and regional players, contributing to a competitive environment. These companies maintain their market positions through extensive product portfolios, significant R&D investments, and strong regional presence.

MEA Veterinary Healthcare Industry Analysis

Growth Drivers

- Increasing Demand for Veterinary Services: The Middle East and Africa (MEA) region has witnessed a significant rise in the demand for veterinary services, driven by the growing awareness of animal health and welfare. In 2023, the MEA veterinary services market generated a revenue of USD 4,785.1 million, reflecting the increasing investment in animal healthcare. This surge is attributed to the expanding livestock sector and the rising number of companion animals, necessitating enhanced veterinary care.

- Expansion in Livestock Production: Livestock production in the MEA region has been on an upward trajectory, with countries like Ethiopia and Nigeria leading in cattle and poultry farming. According to the Food and Agriculture Organization (FAO), Ethiopia's cattle population reached approximately 60 million heads in 2022, underscoring the region's emphasis on livestock farming. This expansion necessitates improved veterinary healthcare services to ensure animal health and productivity.

- Rising Pet Adoption Rates: Urbanization and changing lifestyles have led to an increase in pet ownership across the MEA region. In South Africa, for instance, the pet population was estimated at over 9 million dogs and 2.4 million cats in 2022, indicating a growing trend in pet adoption. This rise in companion animals has escalated the demand for veterinary services, including preventive care and treatment.

Market Challenges

- High Cost of Veterinary Services: The cost of veterinary services in the MEA region remains a significant challenge. In countries like South Africa, veterinary consultation fees can range from USD 20 to USD 50 per visit, making it less accessible for low-income households. This financial barrier limits the ability of many pet owners and livestock farmers to seek necessary veterinary care.

- Limited Access in Rural Areas: Rural areas in the MEA region often face limited access to veterinary services. In Ethiopia, for example, there is approximately one veterinarian per 100,000 livestock units, indicating a significant gap in veterinary care availability. This disparity affects animal health and productivity in these regions.

MEA Veterinary Healthcare Market Future Outlook

Over the next five years, the MEA veterinary healthcare market is expected to experience significant growth. This expansion will be driven by increasing investments in animal health infrastructure, rising awareness of zoonotic diseases, and the adoption of advanced veterinary technologies. Additionally, government initiatives aimed at improving animal health and productivity are anticipated to further propel market growth.

Market Opportunities

- Growth of Veterinary Telemedicine: The adoption of veterinary telemedicine is gaining momentum in the MEA region. In 2023, several countries, including the UAE and South Africa, reported an increase in telemedicine platforms offering veterinary consultations, providing remote access to veterinary care. This development enhances accessibility, especially in remote areas.

- Expansion into Emerging Markets: Emerging markets in the MEA region, such as Kenya and Ghana, present significant opportunities for veterinary healthcare expansion. Kenya's livestock sector contributes approximately 12% to the national GDP, indicating a substantial market for veterinary services. Investing in these markets can drive growth in the veterinary healthcare sector.

Scope of the Report

|

Product Type |

Pharmaceuticals |

|

Animal Type |

Companion Animals (Dogs, Cats, Horses) |

|

Route of Administration |

Oral |

|

End-User |

Veterinary Clinics |

|

Country |

UAE |

Products

Key Target Audience

Veterinary Clinics and Hospitals

Livestock Farmers and Producers

Pet Owners and Associations

Veterinary Pharmaceutical Manufacturers

Animal Health Research Institutes

Government and Regulatory Bodies (e.g., Ministry of Agriculture and Fisheries)

Investments and Venture Capitalist Firms

Veterinary Equipment Suppliers

Companies

Players Mentioned in the Report

Zoetis Inc.

Merck Animal Health

Ceva Sant Animale

Elanco Animal Health

Boehringer Ingelheim

Vetoquinol

IDEXX Laboratories

Virbac SA

Heska Corporation

Hester Biosciences

Table of Contents

1. Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Market Size (In USD Billion)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Demand for Veterinary Services

3.1.2 Expansion in Livestock Production

3.1.3 Rising Pet Adoption Rates

3.1.4 Advancements in Animal Health Products

3.2 Market Challenges

3.2.1 High Cost of Veterinary Services

3.2.2 Limited Access in Rural Areas

3.2.3 Shortage of Skilled Veterinary Professionals

3.3 Opportunities

3.3.1 Growth of Veterinary Telemedicine

3.3.2 Expansion into Emerging Markets

3.3.3 Increase in Government Initiatives for Animal Health

3.4 Trends

3.4.1 Digital Health Integration in Veterinary Care

3.4.2 Preventive Health Focus

3.4.3 Growing Demand for Veterinary Vaccines

3.5 Government Regulations

3.5.1 Animal Health Policies

3.5.2 Veterinary Service Standards

3.5.3 Import and Export Controls

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4. Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Pharmaceuticals

4.1.2 Vaccines

4.1.3 Medicated Feed Additives

4.1.4 Diagnostics

4.1.5 Veterinary Services

4.2 By Animal Type (In Value %)

4.2.1 Companion Animals (Dogs, Cats, Horses)

4.2.2 Production Animals (Cattle, Poultry, Swine, Sheep and Goats)

4.3 By Route of Administration (In Value %)

4.3.1 Oral

4.3.2 Injectable

4.3.3 Topical

4.3.4 Others

4.4 By End-User (In Value %)

4.4.1 Veterinary Clinics

4.4.2 Animal Farms

4.4.3 Research Institutes

4.4.4 Retail Pharmacies

4.5 By Country (In Value %)

4.5.1 UAE

4.5.2 Saudi Arabia

4.5.3 South Africa

4.5.4 Egypt

4.5.5 Rest of MEA

5. Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Zoetis Inc.

5.1.2 Merck Animal Health

5.1.3 Ceva Sant Animale

5.1.4 Elanco Animal Health

5.1.5 Boehringer Ingelheim

5.1.6 Vetoquinol

5.1.7 IDEXX Laboratories

5.1.8 Virbac SA

5.1.9 Heska Corporation

5.1.10 Hester Biosciences

5.1.11 Phibro Animal Health

5.1.12 Neogen Corporation

5.1.13 Biogenesis Bago

5.1.14 Biochek BV

5.1.15 ImmuCell Corporation

5.2 Cross Comparison Parameters (Headquarters, Inception Year, Revenue, Product Portfolio, Market Share, Number of Employees, Regional Presence, R&D Investment)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Regulatory Framework

6.1 Animal Health Compliance Standards

6.2 Veterinary Product Registration and Licensing

6.3 Import and Export Regulations

7. Future Market Size (In USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Animal Type (In Value %)

8.3 By Route of Administration (In Value %)

8.4 By End-User (In Value %)

8.5 By Country (In Value %)

9. Market Analysts Recommendations

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the MEA Veterinary Healthcare Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the MEA Veterinary Healthcare Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple veterinary healthcare providers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the MEA Veterinary Healthcare market.

Frequently Asked Questions

01. How big is the MEA Veterinary Healthcare Market?

The Middle East and Africa (MEA) veterinary healthcare market is valued at USD 3.57 billion, based on a five-year historical analysis.

02. What are the main challenges in the MEA Veterinary Healthcare Market?

The primary challenges include limited access to veterinary services in rural areas, high costs of veterinary care, and a shortage of trained veterinary professionals. These factors hinder the widespread adoption of veterinary healthcare services across the region.

03. Who are the major players in the MEA Veterinary Healthcare Market?

Key players in the market include Zoetis Inc., Merck Animal Health, Ceva Sant Animale, Elanco Animal Health, and Boehringer Ingelheim. These companies have established a strong presence due to their extensive product offerings, R&D investments, and regional networks.

04. What are the growth drivers of the MEA Veterinary Healthcare Market?

The market is propelled by rising awareness of animal health, increasing demand for livestock-derived food products, and government initiatives supporting veterinary care. Furthermore, the growing pet ownership trend in urban areas contributes to market expansion.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.