Middle East & Africa Bread Market Outlook to 2030

Region:Middle East

Author(s):Sanjna

Product Code:KROD9747

November 2024

91

About the Report

Middle East & Africa Bread Market Overview

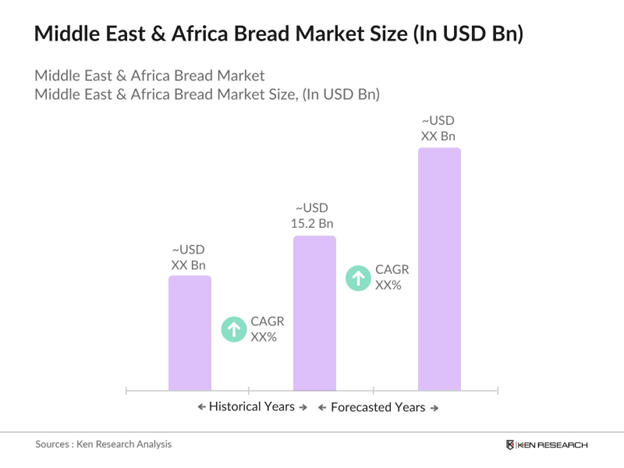

- The Middle East & Africa Bread Market is valued at USD 15.2 billion, with significant growth driven by urbanization and changing consumer lifestyles. The increasing demand for convenience foods and the adoption of healthier bread options, such as gluten-free and organic varieties, have further bolstered the market. Expansion in retail distribution networks, including supermarkets and online platforms, has made bread more accessible, accelerating its consumption across the region.

- Key countries dominating the market include Saudi Arabia, South Africa, and Egypt. Saudi Arabia leads due to its high urbanization rate and substantial investments in modern retail infrastructure. South Africa's dominance is attributed to its well-established bakery chains and rising consumer demand for artisanal bread. Meanwhile, Egypt, with its large population and cultural reliance on bread, maintains significant market demand supported by government subsidies on basic bread products.

- Subsidy programs in many MENA countries, such as those in Egypt and Algeria, reduce the cost of bread production and ensure affordability for low-income populations. The Egyptian government allocated over $3 billion in 2023 for wheat and bread subsidies. Such policies not only support consumer affordability but also sustain production volumes, creating a stable environment for market growth.

Middle East & Africa Bread Market Segmentation

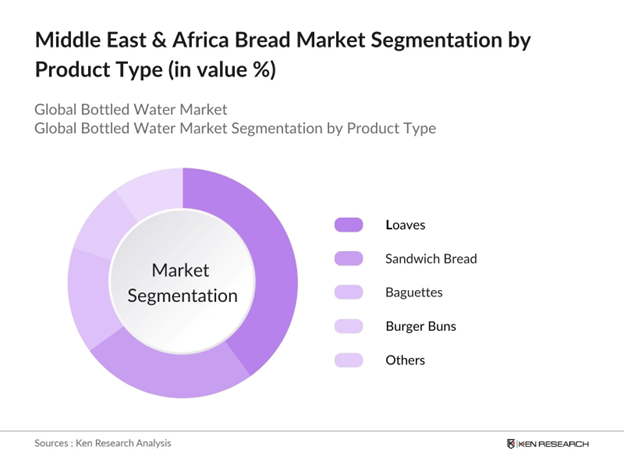

By Product Type: The Middle East & Africa Bread Market is segmented by product type into loaves, sandwich bread, baguettes, burger buns, and others. Recently, loaves have dominated the market share due to their versatility and cultural acceptance across various demographics in the region. Loaves are a staple for household consumption and are widely distributed through retail stores, making them a preferred choice for consumers. Additionally, the affordability and convenience of loaves contribute to their leading position in the product type segmentation.

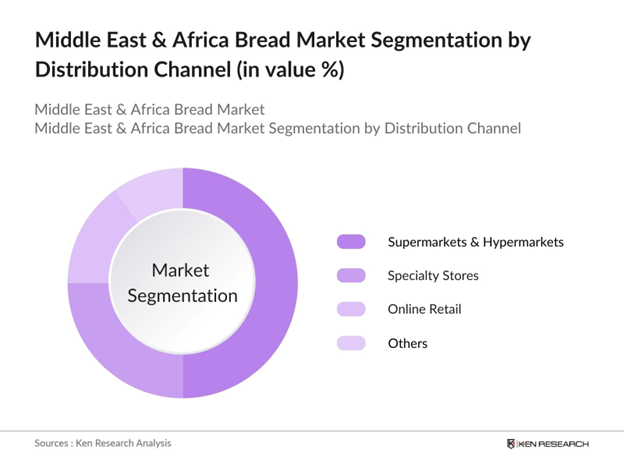

By Distribution Channel: The market is also segmented by distribution channels into supermarkets and hypermarkets, specialty stores, online retail, and others. Supermarkets and hypermarkets dominate due to their widespread presence and ability to offer a variety of bread products at competitive prices. These outlets cater to a large customer base and provide convenience through bulk purchasing options and regular promotions, ensuring high customer footfall.

Middle East & Africa Bread Market Competitive Landscape

The Middle East & Africa Bread Market is characterized by a mix of local and international players, creating a competitive environment. Prominent companies leverage their robust distribution networks, innovation in bread types, and focus on branding to maintain dominance. The market is dominated by companies like Grupo Bimbo SAB de CV and Almarai Co SJSC, supported by their strong product portfolios and extensive regional presence.

Middle East & Africa Bread Market Analysis

Growth Drivers

-

Urbanization and Changing Lifestyles: The Middle East and North Africa (MENA) region has experienced significant urbanization, with urban populations reaching approximately 300 million in 2023. This shift has led to changing dietary habits, increasing the demand for convenient food options like bread. In Egypt, for instance, urbanization has contributed to a higher consumption of bread products, aligning with the global trend of urban dwellers favoring ready-to-eat foods.

- Rising Demand for Convenience Foods: The fast-paced lifestyles in urban centers have escalated the demand for convenience foods, including bread. Saudi Arabia has one of the highest per capita bread consumption rates in the world. Reports indicate that the average Saudi consumes approximately 130 kg of bread annually, making them the largest consumers globally. In Saudi Arabia, the bakery sector has expanded to meet this demand, with bread being a staple in daily diets. The proliferation of quick-service restaurants and cafes in cities like Riyadh and Jeddah has further boosted bread consumption.

- Expansion of Retail Chains: The growth of modern retail chains in the MENA region has enhanced the availability and variety of bread products. Countries like the United Arab Emirates have seen a surge in hypermarkets and supermarkets, providing consumers with diverse bread options. This retail expansion has facilitated easier access to both local and international bread varieties, catering to a broad spectrum of consumer preferences.

Challenges

- Fluctuating Raw Material Prices: The bread industry in the MENA region faces challenges due to the volatility of raw material prices, particularly wheat. For example, Egypt, a major wheat importer, has been affected by global price fluctuations, impacting bread production costs. In 2023, Egypt's wheat imports rose to approximately10.88 million tons, a14.7% increasefrom the previous year, largely attributed to a dip in global wheat prices following the peaks caused by the Russia-Ukraine conflict. Such volatility poses risks to the stability of bread prices and the profitability of producers.

- Health Concerns Related to Bread Consumption: Increasing awareness of health issues, such as obesity and diabetes, has led to a decline in bread consumption in some MENA countries. In Kuwait, health campaigns have highlighted the risks associated with high carbohydrate intake, influencing consumer choices towards healthier alternatives. This shift presents a challenge for traditional bread producers to adapt to changing consumer preferences.

Middle East & Africa Bread Market Future Outlook

Over the next five years, the Middle East & Africa Bread Market is expected to witness significant growth driven by increasing consumer inclination towards healthier bread options and technological advancements in baking processes. Expansion in online retail channels and a growing preference for artisanal and specialty bread will further drive market development. Additionally, rising disposable incomes and urbanization will enhance market penetration in untapped regions.

Market Opportunities

-

Growth in Gluten-Free and Organic Bread Segments: The MENA region is witnessing a growing demand for gluten-free and organic bread products. Recent product launches include gluten-free cereals by Nestl and expanded selections of gluten-free items in major supermarkets like Carrefour, indicating that producers are actively diversifying their offerings to meet evolving consumer preferences. In the United Arab Emirates, health-conscious consumers are increasingly opting for these alternatives, leading to a rise in specialty bakeries catering to this niche market.

- Technological Advancements in Baking Processes: Adoption of advanced baking technologies in the MENA region has improved production efficiency and product quality. Bakeries in Saudi Arabia are increasingly investing in automated systems to enhance production efficiency and maintain product consistency. This shift is driven by the need to meet growing consumer demand for high-quality bread products. In Saudi Arabia, bakeries are investing in automated systems to enhance output and maintain consistency, meeting the growing consumer demand for high-quality bread products.

Scope of the Report

|

Segment |

Sub-Segments |

|

By Product Type |

Loaves |

|

Sandwich Bread |

|

|

Baguettes |

|

|

Burger Buns |

|

|

Others |

|

|

By Category |

Organic |

|

Conventional |

|

|

By Distribution Channel |

Supermarkets and Hypermarkets |

|

Specialty Stores |

|

|

Online Retail |

|

|

Others |

|

|

By Specialty Type |

Gluten-Free |

|

Fortified |

|

|

Organic |

|

|

Low-Calorie |

|

|

Sugar-Free |

|

|

By Country |

Saudi Arabia |

|

Turkey |

|

|

Nigeria |

|

|

UAE |

|

|

Egypt |

|

|

South Africa |

|

|

Rest of Middle East & Africa |

Products

Key Target Audience

Food and Beverage Companies

Retail Chains and Supermarkets

Online Retail Platforms

Bakery Equipment Manufacturers

Ingredient Suppliers (e.g., flour and yeast manufacturers)

Health and Wellness Organizations

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Ministry of Industry and Mineral Resources, Saudi Food and Drug Authority)

Companies

Players Mentioned in the Report

Grupo Bimbo SAB de CV

Almarai Co SJSC

Modern Bakery LLC

Aryzta AG

Sunbulah Group

Wonder Bakery LLC

Agthia Group

Al Rashed Food Co Ltd

Dr. Schr AG

Bakemart Middle East

Table of Contents

1. Middle East & Africa Bread Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Middle East & Africa Bread Market Size (USD Million)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Middle East & Africa Bread Market Analysis

3.1. Growth Drivers

3.1.1. Urbanization and Changing Lifestyles

3.1.2. Rising Demand for Convenience Foods

3.1.3. Expansion of Retail Chains

3.1.4. Increasing Disposable Income

3.2. Market Challenges

3.2.1. Fluctuating Raw Material Prices

3.2.2. Health Concerns Related to Bread Consumption

3.2.3. Supply Chain Disruptions

3.3. Opportunities

3.3.1. Growth in Gluten-Free and Organic Bread Segments

3.3.2. Technological Advancements in Baking Processes

3.3.3. Expansion into Untapped Markets

3.4. Trends

3.4.1. Adoption of Artisanal and Specialty Breads

3.4.2. Integration of Healthier Ingredients

3.4.3. Rise of Online Retail Channels

3.5. Government Regulations

3.5.1. Food Safety Standards

3.5.2. Import and Export Policies

3.5.3. Subsidies and Taxation Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. Middle East & Africa Bread Market Segmentation

4.1. By Product Type (Value %)

4.1.1. Loaves

4.1.2. Sandwich Bread

4.1.3. Baguettes

4.1.4. Burger Buns

4.1.5. Others

4.2. By Category (Value %)

4.2.1. Organic

4.2.2. Conventional

4.3. By Distribution Channel (Value %)

4.3.1. Supermarkets and Hypermarkets

4.3.2. Specialty Stores

4.3.3. Online Retail

4.3.4. Others

4.4. By Specialty Type (Value %)

4.4.1. Gluten-Free

4.4.2. Fortified

4.4.3. Organic

4.4.4. Low-Calorie

4.4.5. Sugar-Free

4.5. By Country (Value %)

4.5.1. Saudi Arabia

4.5.2. Turkey

4.5.3. Nigeria

4.5.4. UAE

4.5.5. Egypt

4.5.6. South Africa

4.5.7. Rest of Middle East & Africa

5. Middle East & Africa Bread Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Grupo Bimbo SAB de CV

5.1.2. Almarai Co SJSC

5.1.3. Agthia Group

5.1.4. Modern Bakery LLC

5.1.5. Aryzta AG

5.1.6. Sunbulah Group

5.1.7. Wonder Bakery LLC

5.1.8. Agthia Group

5.1.9. Al Rashed Food Co Ltd

5.1.10. Dr. Schr AG

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Share, Regional Presence, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6. Middle East & Africa Bread Market Regulatory Framework

6.1. Food Safety Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. Middle East & Africa Bread Future Market Size (USD Million)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Middle East & Africa Bread Future Market Segmentation

8.1. By Product Type (Value %)

8.2. By Category (Value %)

8.3. By Distribution Channel (Value %)

8.4. By Specialty Type (Value %)

8.5. By Country (Value %)

9. Middle East & Africa Bread Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

10. Disclaimer

11. Contact Us

Research Methodology

Step 1: Identification of Key Variables

This phase involves mapping the market ecosystem, identifying all major stakeholders in the Middle East & Africa Bread Market. Desk research and proprietary databases are utilized to gather comprehensive industry data, focusing on the critical variables influencing market dynamics.

Step 2: Market Analysis and Construction

Historical market data is compiled to assess revenue generation, product penetration, and market trends. Analysis of distribution channels and consumer preferences ensures accurate market size estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through interviews with industry experts, including manufacturers, retailers, and distributors. This provides operational insights that enhance the reliability of the data.

Step 4: Research Synthesis and Final Output

Data synthesis from primary and secondary sources is finalized, followed by detailed market segmentation and competitive analysis. Insights are validated with industry stakeholders to ensure accuracy and comprehensiveness.

Frequently Asked Questions

01. How big is the Middle East & Africa Bread Market?

The Middle East & Africa Bread Market is valued at USD 15.2 billion, driven by growing consumer demand for convenience foods and expansion in retail networks.

02. What are the challenges in the Middle East & Africa Bread Market?

Challenges in Middle East & Africa Bread Market include fluctuating raw material prices, increasing health awareness impacting bread consumption, and supply chain disruptions affecting the timely delivery of products.

03. Who are the major players in the Middle East & Africa Bread Market?

Key players in Middle East & Africa Bread Market include Grupo Bimbo SAB de CV, Almarai Co SJSC, Modern Bakery LLC, Aryzta AG, and Sunbulah Group. These companies lead through extensive regional presence and product innovation.

04. What are the growth drivers of the Middle East & Africa Bread Market?

Middle East & Africa Bread Market is propelled by urbanization, rising disposable incomes, and growing demand for healthier bread options, such as gluten-free and organic varieties.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.