Middle East & Africa Corrosion Protection Coatings Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD6808

December 2024

85

About the Report

Middle East & Africa Corrosion Protection Coatings Market Overview

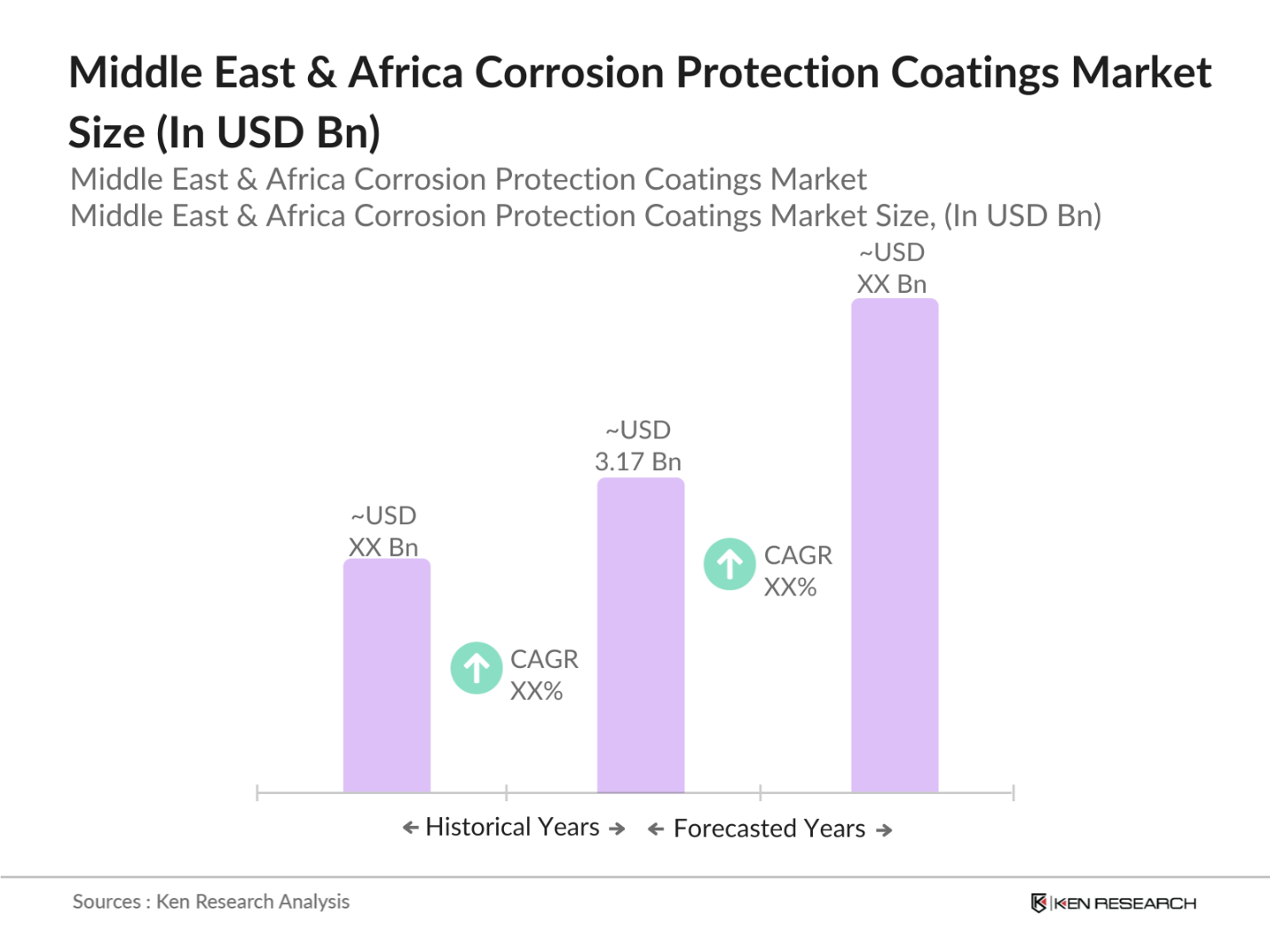

- The Middle East & Africa corrosion protection coatings market is valued at USD 3.17 billion. This market is primarily driven by the growth of the oil & gas sector, which requires extensive corrosion protection for pipelines, refineries, and offshore platforms. Additionally, infrastructure development, including airports, bridges, and roadways, is also contributing to the increased demand for corrosion protection solutions. The rise of industrialization and urbanization further bolsters this market, driving demand for coatings that enhance the lifespan of structures and equipment.

- Key countries such as Saudi Arabia, UAE, and South Africa dominate the market due to their booming oil & gas and infrastructure sectors. Saudi Arabia, for instance, invests heavily in oil exploration and refinery maintenance, which requires corrosion-resistant solutions. The UAE's fast-paced urbanization and South Africa's industrial growth, particularly in manufacturing and mining, make them leading markets for corrosion protection coatings. These nations also benefit from government initiatives aimed at maintaining the integrity of critical infrastructure.

- In response to tightening environmental regulations, the use of low VOC and waterborne coatings is rising. The GCC countries aim to reduce their VOC emissions by 10% by 2025 . Waterborne coatings are becoming increasingly popular in the region, offering a more sustainable option compared to solvent-borne coatings. These coatings are now widely used in infrastructure and automotive applications.

Middle East & Africa Corrosion Protection Coatings Market Segmentation

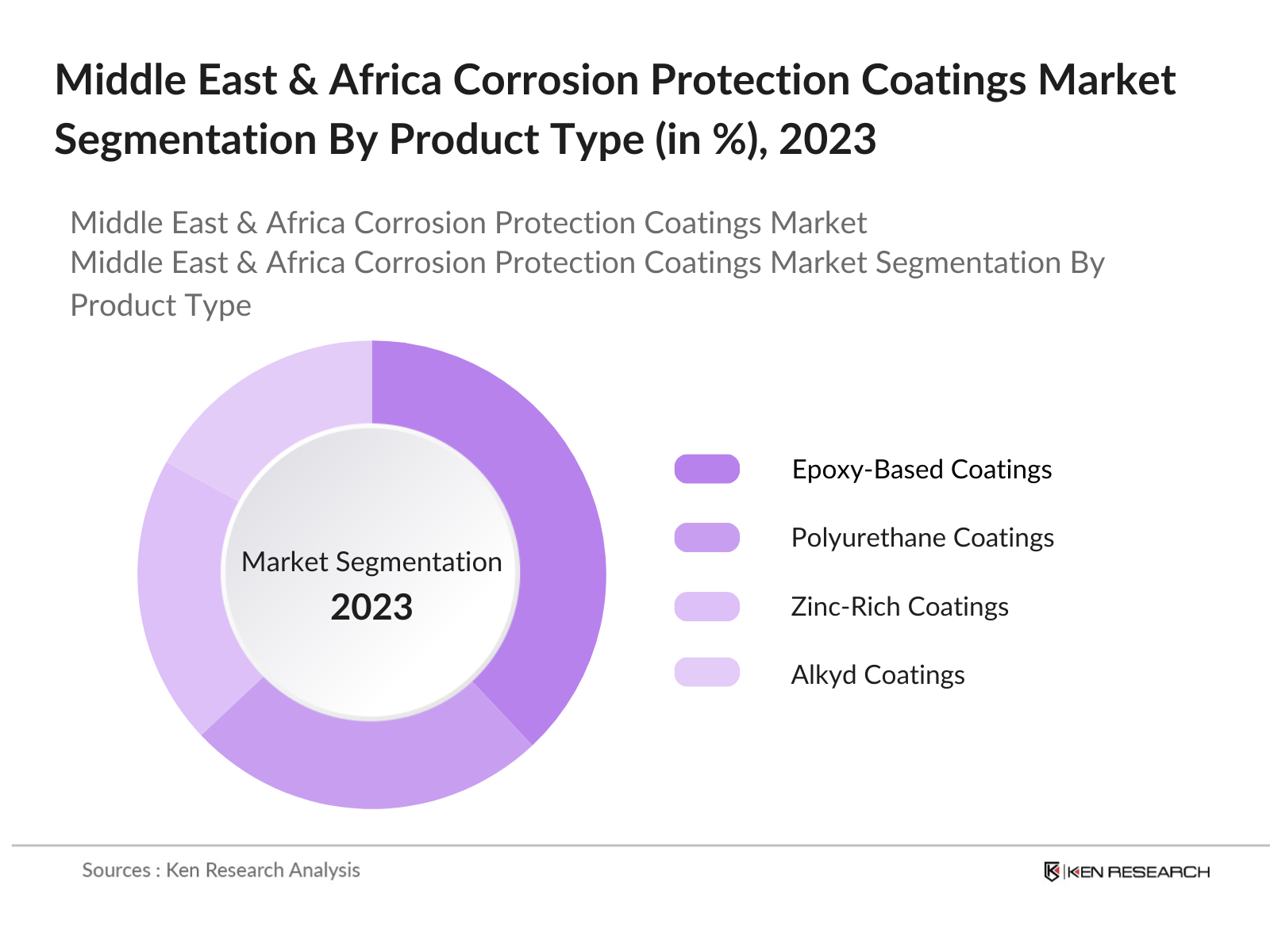

By Product Type: The Middle East & Africa corrosion protection coatings market is segmented by product type into epoxy-based coatings, polyurethane coatings, zinc-rich coatings, alkyd coatings, and others (including ceramic and fluoropolymer coatings). Epoxy-based coatings currently hold the dominant market share due to their excellent corrosion resistance, adhesion, and durability. These coatings are widely used in industries such as oil & gas, marine, and construction, where protection from harsh environmental conditions is paramount. Furthermore, their cost-effectiveness makes them a preferred choice for large-scale infrastructure projects.

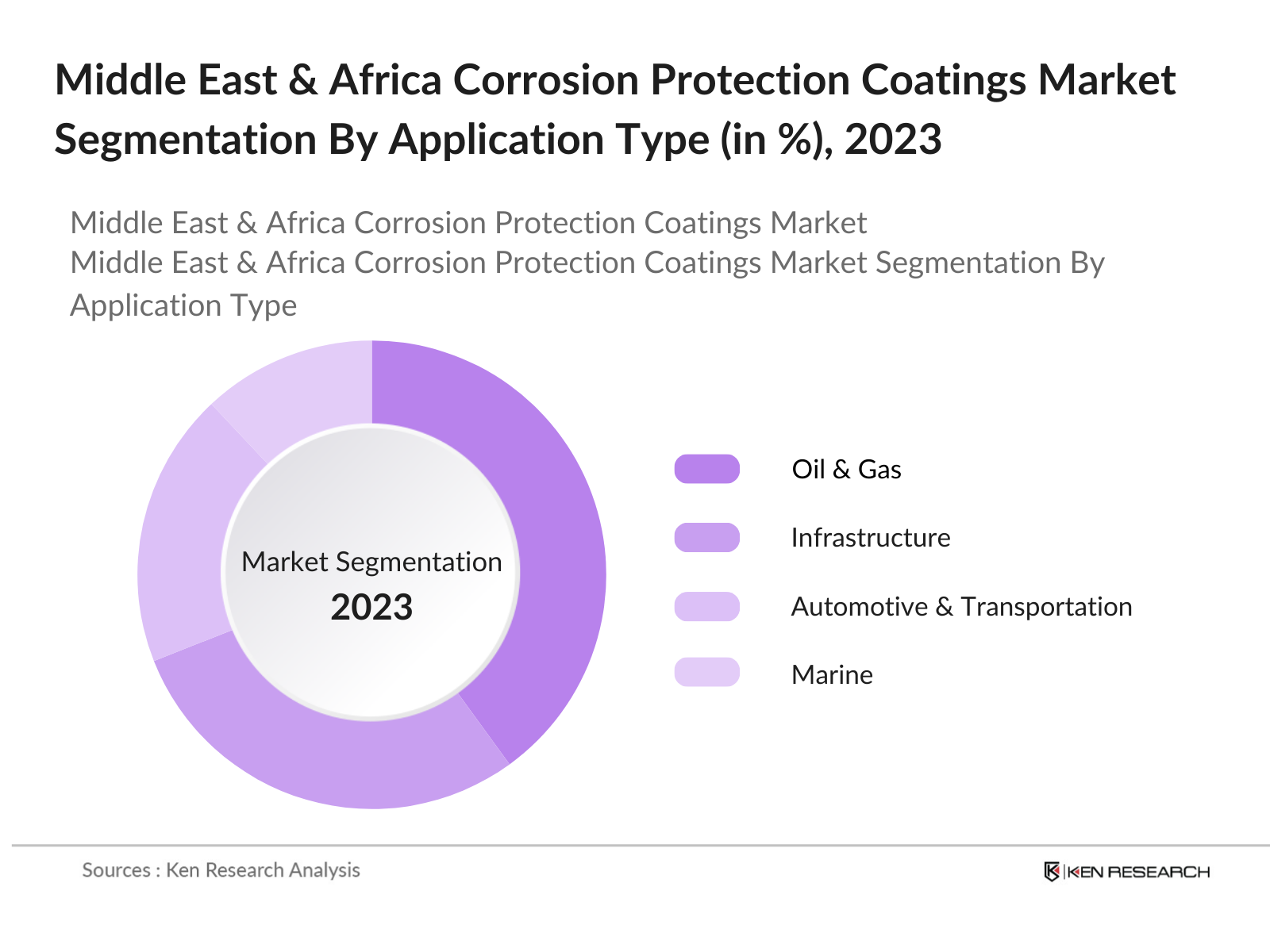

By Application: The corrosion protection coatings market is also segmented by application into oil & gas, infrastructure, automotive & transportation, marine, and power generation. The oil & gas sector dominates the market, owing to the extensive need for corrosion protection in pipelines, storage tanks, and offshore drilling rigs. These coatings prevent equipment degradation caused by exposure to saline environments, harsh chemicals, and fluctuating temperatures, all common in oil & gas operations. The sector's rapid growth in the Middle East, particularly in Saudi Arabia and the UAE, drives demand for high-performance corrosion protection coatings.

Middle East & Africa Corrosion Protection Coatings Market Competitive Landscape

The Middle East & Africa corrosion protection coatings market is characterized by the presence of a few key players that dominate the competitive landscape. The market is largely consolidated, with leading companies focusing on product innovation, strategic partnerships, and geographical expansion to maintain their competitive edge. The oil & gas and infrastructure sectors provide substantial opportunities for these firms, leading to an intense rivalry to capture market share.

|

Company |

Year of Establishment |

Headquarters |

Product Portfolio |

Revenue (USD Bn) |

Number of Employees |

Regional Presence |

Market Strategy |

|

PPG Industries, Inc. |

1883 |

Pittsburgh, USA |

_ |

_ |

_ |

_ |

_ |

|

Akzo Nobel N.V. |

1792 |

Amsterdam, Netherlands |

_ |

_ |

_ |

_ |

_ |

|

Jotun A/S |

1926 |

Sandefjord, Norway |

_ |

_ |

_ |

_ |

_ |

|

Hempel A/S |

1915 |

Lyngby, Denmark |

_ |

_ |

_ |

_ |

_ |

|

The Sherwin-Williams Company |

1866 |

Cleveland, USA |

_ |

_ |

_ |

_ |

_ |

Middle East & Africa Corrosion Protection Coatings Industry Analysis

Growth Drivers

- Increasing Infrastructure Development: The MEA region is undergoing extensive infrastructure development. In 2023, regional governments allocated USD 400 billion for construction projects, including oil pipelines and smart cities . These projects require robust corrosion protection solutions, especially in the pipeline sector, where corrosion can cause operational disruptions and financial losses. With a focus on infrastructure modernization, the demand for advanced coatings is expected to rise.

- Oil & Gas Industry Expansion: The oil & gas sector remains a cornerstone of the regions economy. In 2023, the GCC nations produced 24 million barrels of oil per day , a significant portion of which is transported through pipelines that are prone to corrosion. To mitigate risks, oil companies are investing heavily in corrosion protection systems. The demand for advanced coatings, such as those used for underwater pipelines, has increased

- Government Initiatives for Industrial Development: Governments in the Middle East and Africa are actively supporting industrial development through various initiatives. The Saudi Vision 2030 and Egypts Sustainable Development Strategy are key policies that have allocated USD 200 billion to industrial infrastructure . These initiatives, which emphasize the modernization of industrial facilities, require advanced corrosion protection systems to ensure the longevity of equipment and structures.

Market Challenges

- High Cost of Advanced Coatings: Advanced coatings, such as those employing nanotechnology, tend to be expensive due to high production costs. The average cost of nanotech-based coatings is 20-30% higher than traditional options . While these coatings offer superior performance, the high initial costs deter some industries from widespread adoption. Small and medium enterprises (SMEs) in particular find these costs prohibitive, slowing market penetration.

- Availability of Cheaper Alternatives: Cheaper alternatives, such as alkyd-based coatings, remain a challenge for the market. In 2023, alkyd coatings accounted for approximately 15% of the coatings market due to their lower costs. However, they offer limited corrosion resistance, especially in high-salinity environments prevalent in the Middle East. Industries that prioritize cost over performance often opt for these alternatives, which slows the adoption of more advanced solutions.

Middle East & Africa Corrosion Protection Coatings Future Outlook

Over the next few years, the Middle East & Africa corrosion protection coatings market is expected to experience significant growth driven by infrastructure development, increasing oil & gas exploration activities, and the need for corrosion prevention in harsh climates. The market will also see a growing demand for environmentally friendly and sustainable coatings, as regional governments enforce stricter environmental regulations and promote the use of eco-friendly materials. This shift towards sustainable solutions will drive innovation and new product developments in the market.

Opportunities

- Growth in Renewable Energy Projects: The renewable energy sector is expanding rapidly in the MEA region. In 2023, the region had 37 GW of installed renewable energy capacity . Offshore wind farms and solar installations, particularly in Egypt and Morocco, are driving the demand for advanced corrosion protection. Offshore wind turbines, exposed to saltwater, require durable coatings to prevent corrosion and ensure operational efficiency.

- Increasing Demand for Advanced Coatings in the Marine Sector: The marine sector plays a crucial role in the region's economy, particularly with the Suez Canal handling over 1.2 billion tons of cargo annually . To maintain the integrity of ships and port infrastructure, the use of advanced corrosion-resistant coatings is essential. The increasing use of epoxy and polyurethane coatings in marine applications is a significant growth opportunity for the market.

Scope of the Report

|

Product Type |

Epoxy-Based Coatings Polyurethane Coatings Zinc-Rich Coatings Alkyd Coatings |

|

Application |

Oil & Gas Infrastructure Automotive & Transportation Marine |

|

Technology |

Solvent-Borne Water-Borne Powder Coating UV-Cured Coatings |

|

Substrate Type |

Metal Concrete Composites Others |

|

Region |

Middle East North Africa Sub-Saharan Africa |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Oil & Gas Companies

Infrastructure Development Companies

Marine and Shipping Companies

Automotive & Transportation Industries

Power Generation Firms

Corrosion Protection Coating Companies

Government and Regulatory Bodies (e.g., Saudi Standards, Metrology and Quality Organization (SASO), UAE Ministry of Infrastructure Development)

Investments and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

PPG Industries, Inc.

Akzo Nobel N.V.

The Sherwin-Williams Company

Hempel A/S

Jotun A/S

RPM International Inc.

Kansai Paint Co., Ltd.

Nippon Paint Holdings Co., Ltd.

Axalta Coating Systems

BASF SE

Tnemec Company, Inc.

Carboline Company

H.B. Fuller

Wacker Chemie AG

DuluxGroup Ltd

Table of Contents

1. Middle East & Africa Corrosion Protection Coatings Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Middle East & Africa Corrosion Protection Coatings Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Middle East & Africa Corrosion Protection Coatings Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Infrastructure Development (Construction, Pipelines)

3.1.2. Oil & Gas Industry Expansion

3.1.3. Government Initiatives for Industrial Development

3.1.4. Stringent Environmental Regulations on Corrosion Prevention

3.2. Market Challenges

3.2.1. High Cost of Advanced Coatings

3.2.2. Availability of Cheaper Alternatives

3.2.3. Complex Application and Maintenance Processes

3.3. Opportunities

3.3.1. Growth in Renewable Energy Projects (Offshore Wind, Solar Farms)

3.3.2. Increasing Demand for Advanced Coatings in the Marine Sector

3.3.3. Technological Innovations in Coatings (Smart Coatings, Self-Healing Coatings)

3.4. Trends

3.4.1. Adoption of Environmentally Friendly Coatings (Low VOC, Waterborne Coatings)

3.4.2. Use of Nanotechnology in Corrosion Protection

3.4.3. Rising Demand for Polyurethane and Epoxy-Based Coatings

3.5. Government Regulations

3.5.1. Environmental Protection Standards in Corrosion Prevention

3.5.2. Industrial Safety Regulations

3.5.3. Certifications for Corrosion Resistance Coatings

3.5.4. Public-Private Partnerships for Infrastructure Development

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Middle East & Africa Corrosion Protection Coatings Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Epoxy-Based Coatings

4.1.2. Polyurethane Coatings

4.1.3. Zinc-Rich Coatings

4.1.4. Alkyd Coatings

4.1.5. Others (Fluoropolymer, Ceramic Coatings)

4.2. By Application (In Value %) 4.2.1. Oil & Gas

4.2.2. Infrastructure

4.2.3. Automotive & Transportation

4.2.4. Marine

4.2.5. Power Generation

4.3. By Technology (In Value %) 4.3.1. Solvent-Borne

4.3.2. Water-Borne

4.3.3. Powder Coating

4.3.4. UV-Cured Coatings

4.4. By Substrate Type (In Value %) 4.4.1. Metal

4.4.2. Concrete

4.4.3. Composites

4.4.4. Others

4.5. By Region (In Value %) 4.5.1. Middle East

4.5.2. North Africa

4.5.3. Sub-Saharan Africa

5. Middle East & Africa Corrosion Protection Coatings Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. PPG Industries, Inc.

5.1.2. Akzo Nobel N.V.

5.1.3. The Sherwin-Williams Company

5.1.4. Hempel A/S

5.1.5. Jotun A/S

5.1.6. RPM International Inc.

5.1.7. Kansai Paint Co., Ltd.

5.1.8. Nippon Paint Holdings Co., Ltd.

5.1.9. Axalta Coating Systems

5.1.10. BASF SE

5.1.11. Tnemec Company, Inc.

5.1.12. Carboline Company

5.1.13. H.B. Fuller

5.1.14. Wacker Chemie AG

5.1.15. DuluxGroup Ltd

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters Location

5.2.3. Year of Inception

5.2.4. Product Portfolio

5.2.5. Revenue (USD Bn)

5.2.6. Regional Presence

5.2.7. Strategic Initiatives

5.2.8. Customer Base

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Middle East & Africa Corrosion Protection Coatings Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. Middle East & Africa Corrosion Protection Coatings Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Middle East & Africa Corrosion Protection Coatings Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Substrate Type (In Value %)

8.5. By Region (In Value %)

9. Middle East & Africa Corrosion Protection Coatings Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The research process began with identifying key variables, such as product type, application, and geographical scope, influencing the Middle East & Africa corrosion protection coatings market. This involved extensive secondary research and analysis of industry reports, government publications, and company press releases.

Step 2: Market Analysis and Construction

In this phase, historical data on the market size, growth drivers, and challenges were collected and analyzed to understand the market's evolution. This included studying regional trends, demand patterns, and technological advancements in corrosion protection coatings.

Step 3: Hypothesis Validation and Expert Consultation

To validate the market hypotheses, consultations were conducted with industry experts, including product managers, engineers, and executives from leading companies. These interviews provided insights into emerging trends, competitive dynamics, and product performance across different applications.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing the data and insights collected from secondary and primary research. A bottom-up approach was employed to estimate market size and growth rates, ensuring accurate and reliable results. This synthesis formed the basis of the report's key findings and recommendations.

Frequently Asked Questions

01. How big is the Middle East & Africa Corrosion Protection Coatings Market?

The Middle East & Africa corrosion protection coatings market is valued at USD 3.17 billion, driven by the demand from oil & gas, infrastructure, and marine industries.

02. What are the challenges in the Middle East & Africa Corrosion Protection Coatings Market?

Key challenges include the high cost of advanced coatings, complex application processes, and competition from cheaper alternatives, which can limit market growth in price-sensitive regions.

03. Who are the major players in the Middle East & Africa Corrosion Protection Coatings Market?

The major players include PPG Industries, Akzo Nobel, The Sherwin-Williams Company, Hempel A/S, and Jotun A/S, dominating due to their established presence, product innovations, and strategic partnerships.

04. What are the growth drivers of the Middle East & Africa Corrosion Protection Coatings Market?

Growth is primarily driven by the expansion of the oil & gas sector, rapid infrastructure development, and increasing demand for durable and corrosion-resistant coatings in harsh climates.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.