North America Automated Guided Vehicle Market Outlook to 2030

Region:North America

Author(s):Mukul

Product Code:KROD3088

Region:North America

Author(s):Mukul

Product Code:KROD3088

October 2024

87

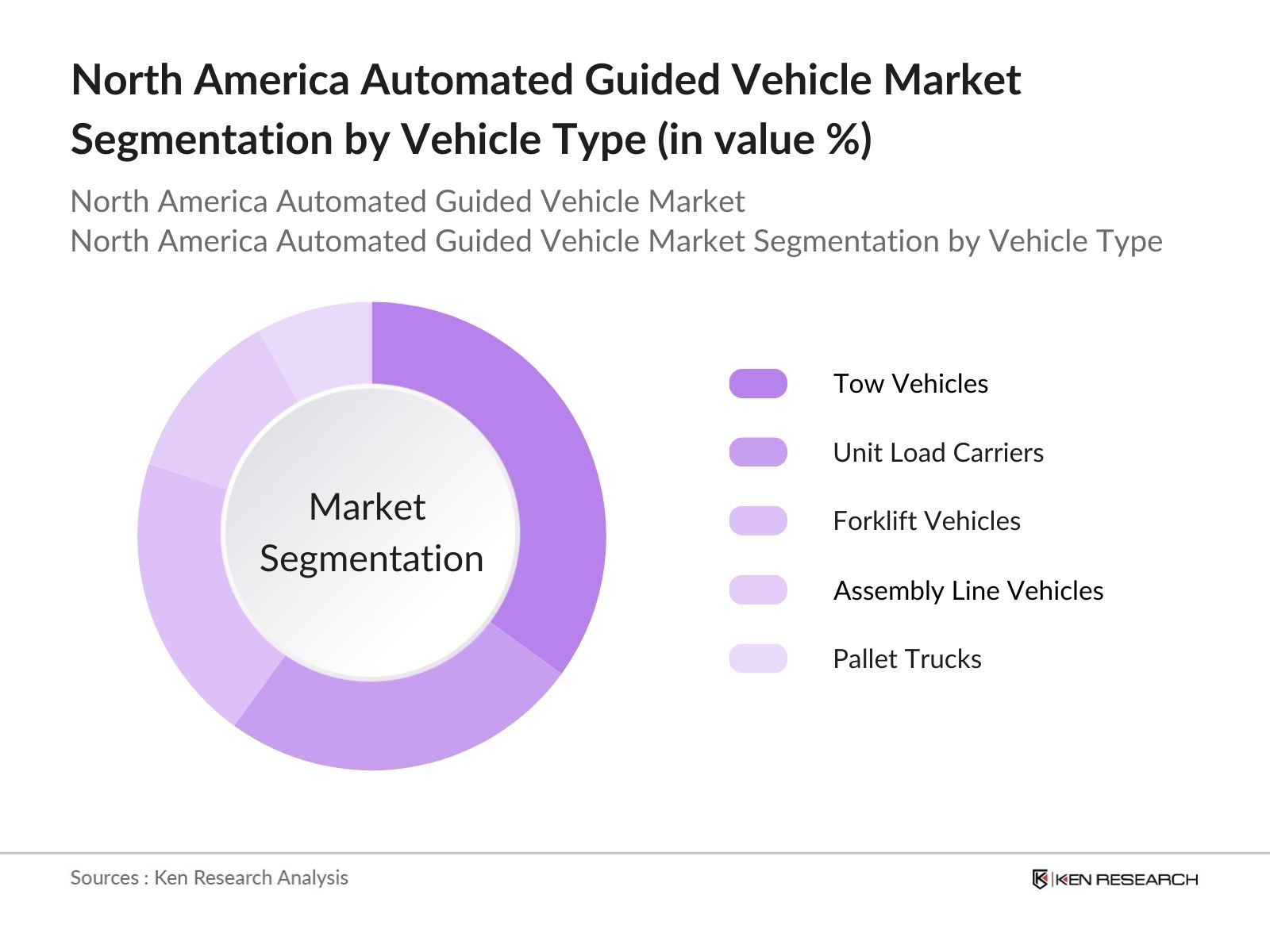

By Vehicle Type: North Americas AGV market is segmented by vehicle type into tow vehicles, unit load carriers, forklift vehicles, assembly line vehicles, and pallet trucks. Tow vehicles dominate the market, as they are widely used in warehouses for material handling, offering flexibility and high load capacities. The high demand for tow vehicles can be attributed to their ability to handle multiple load types, making them essential for industries such as automotive and logistics.

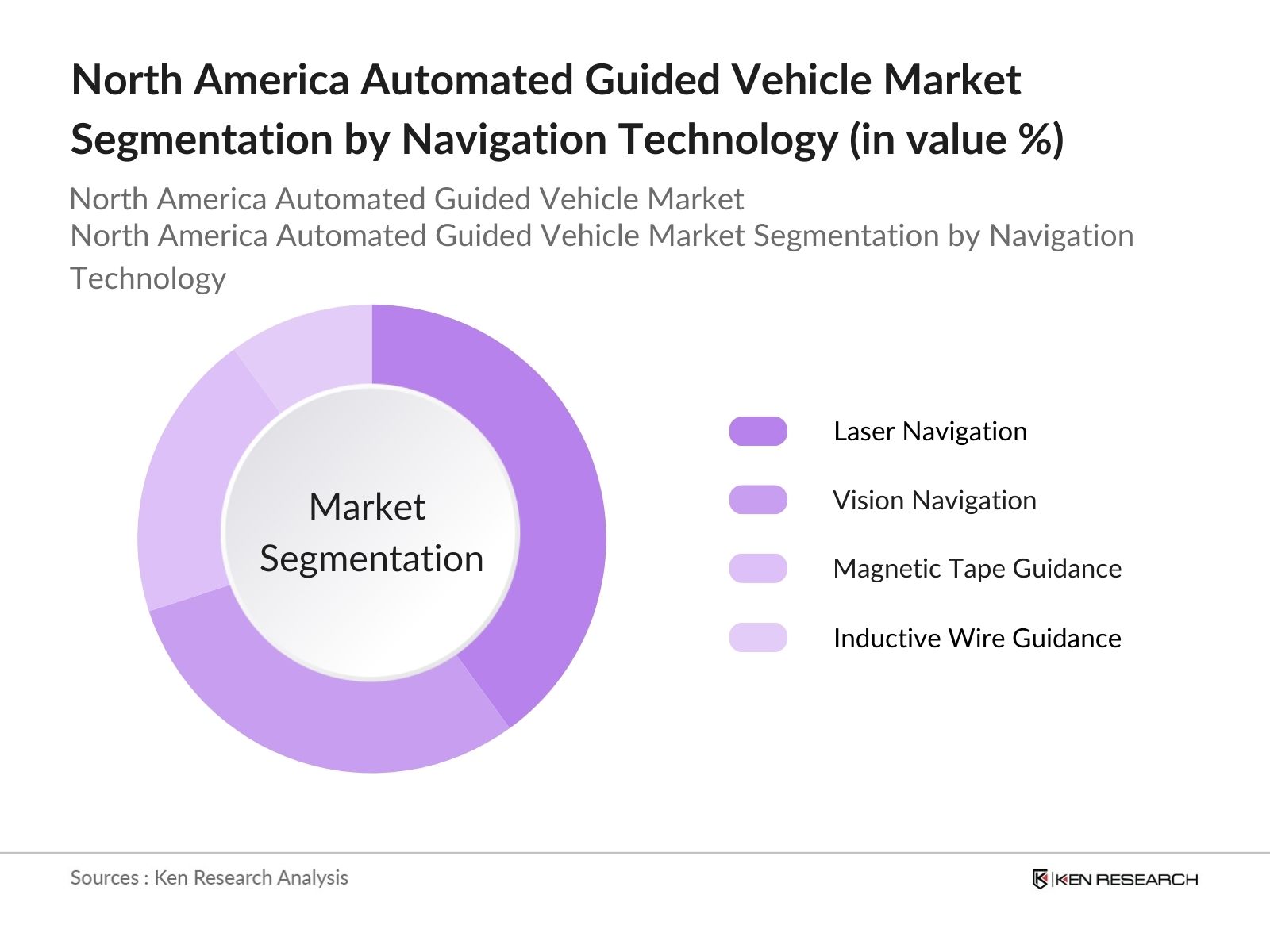

By Navigation Technology: In terms of navigation technology, the AGV market is divided into laser navigation, vision navigation, magnetic tape guidance, and inductive wire guidance. Laser navigation technology dominate the market, due to its superior precision and adaptability in complex environments. The rise in smart factories and the need for high-accuracy AGVs to operate in dynamic conditions have propelled the adoption of laser navigation systems in North America.

The North American AGV market is dominated by a combination of global and regional players who control significant portions of the market. These companies offer a broad range of automated guided vehicle solutions, capitalizing on innovations such as AI-driven navigation systems and collaborative AGVs. The competitive landscape in North America reflects the importance of strong R&D investments and strategic partnerships in driving growth. Additionally, companies are focusing on expanding their customer base across industries such as automotive, logistics, and e-commerce.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD Mn) |

Market Share (%) |

R&D Investments (USD Mn) |

Number of AGV Models |

Technological Focus |

Recent Acquisitions |

|

Toyota Industries Corp |

1926 |

Japan (North America HQ: USA) |

||||||

|

Daifuku Co. Ltd. |

1937 |

Japan (North America HQ: USA) |

||||||

|

Swisslog Holding AG |

1900 |

Switzerland (North America HQ: USA) |

||||||

|

JBT Corporation |

1884 |

USA |

||||||

|

KION Group AG |

1904 |

Germany (North America HQ: USA) |

Over the next five years, the North America Automated Guided Vehicle market is expected to experience significant growth, driven by increased automation in manufacturing and logistics. Government initiatives to promote smart manufacturing and industrial automation, coupled with advancements in AGV technologies such as AI and machine learning, are expected to propel market growth. Furthermore, the ongoing labor shortage in key industries will continue to push businesses towards automated solutions.

|

By Vehicle Type |

Tow Vehicles |

|

By Navigation Technology |

Laser Navigation |

|

By Application |

Manufacturing |

|

By End-User Industry |

Automotive Industry |

|

By Region |

United States |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increase in E-Commerce Warehousing (Impact on Material Handling Systems)

3.1.2. Rising Adoption of Industry 4.0 (Automated Systems for Process Efficiency)

3.1.3. Labor Shortages in Manufacturing and Warehousing (Demand for Automation)

3.2. Market Challenges

3.2.1. High Initial Cost of AGV Deployment

3.2.2. Technical Integration Challenges (Interoperability with Existing Systems)

3.2.3. Limited Availability of Skilled Operators

3.3. Opportunities

3.3.1. Growth in 3PL (Third-Party Logistics) Industry

3.3.2. Expansion in Cold Chain Storage Facilities

3.3.3. Adoption of Collaborative Mobile Robots (Integration with AGVs)

3.4. Trends

3.4.1. Shift Towards AGVs with Advanced AI Capabilities

3.4.2. Integration of AGVs in Smart Factories and Smart Warehousing

3.4.3. Increased Utilization of AGVs in Automated Material Handling

3.5. Regulatory Landscape

3.5.1. Safety Standards (OSHA, ANSI/ITSDF B56.5)

3.5.2. Data and Cybersecurity Regulations for Automated Systems

3.5.3. U.S. and Canada Regulatory Environment for AGVs

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (AGV Manufacturers, Integrators, End-users)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Vehicle Type (In Value %)

4.1.1. Tow Vehicles

4.1.2. Unit Load Carriers

4.1.3. Forklift Vehicles

4.1.4. Assembly Line Vehicles

4.1.5. Pallet Trucks

4.2. By Navigation Technology (In Value %)

4.2.1. Laser Navigation

4.2.2. Vision Navigation

4.2.3. Magnetic Tape Guidance

4.2.4. Inductive Wire Guidance

4.3. By Application (In Value %)

4.3.1. Manufacturing (Automotive, Electronics, Aerospace)

4.3.2. Logistics and Warehousing (Distribution Centers, Retail Warehousing)

4.3.3. Healthcare (Hospitals, Pharmaceutical)

4.3.4. Food and Beverage Industry

4.3.5. E-Commerce and Retail

4.4. By End-User Industry (In Value %)

4.4.1. Automotive Industry

4.4.2. Logistics and Distribution

4.4.3. Healthcare

4.4.4. Food and Beverage

4.4.5. Retail and E-Commerce

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5.1. Detailed Profiles of Major Companies

5.1.1. Toyota Industries Corporation

5.1.2. Daifuku Co. Ltd.

5.1.3. Swisslog Holding AG

5.1.4. KION Group AG

5.1.5. JBT Corporation

5.1.6. Seegrid Corporation

5.1.7. Hyster-Yale Materials Handling, Inc.

5.1.8. E&K Automation GmbH

5.1.9. Balyo Inc.

5.1.10. Bastian Solutions, Inc.

5.1.11. Murata Machinery, Ltd.

5.1.12. Kollmorgen Corporation

5.1.13. KUKA AG

5.1.14. SSI Schaefer Group

5.1.15. Oceaneering International, Inc.

5.2. Cross Comparison Parameters (Revenue, Headquarters, Market Share, Fleet Size, Innovation Rate, Customer Base, Technology Adoption, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Initiatives

5.9. Private Equity Investments

6.1. Industry Standards and Certifications (ISO 3691-4, ISO 10218)

6.2. Compliance Requirements for Autonomous Systems

6.3. Certification Processes for Safety and Security

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vehicle Type (In Value %)

8.2. By Navigation Technology (In Value %)

8.3. By Application (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves constructing an ecosystem map that includes all key stakeholders in the North American AGV market. Extensive desk research is conducted using secondary and proprietary databases to gather industry-level information. The main aim of this step is to identify critical variables affecting market dynamics, such as automation trends and technological advancements.

In this phase, historical data on the North American AGV market is compiled and analyzed. Key metrics include the number of AGV installations, their usage in different industries, and revenue generation. Additionally, AGV penetration rates and service provider data are evaluated to ensure accuracy in revenue estimates.

The developed market hypotheses are validated through consultations with industry experts via CATI (Computer-Assisted Telephone Interviews). These interviews provide direct insights from professionals in the AGV industry, which are crucial for refining market data and understanding operational trends.

The final step involves engaging directly with AGV manufacturers and distributors to obtain detailed information on product segments, sales performance, and customer preferences. This engagement complements the statistical findings from the bottom-up analysis, ensuring an accurate and validated market outlook.

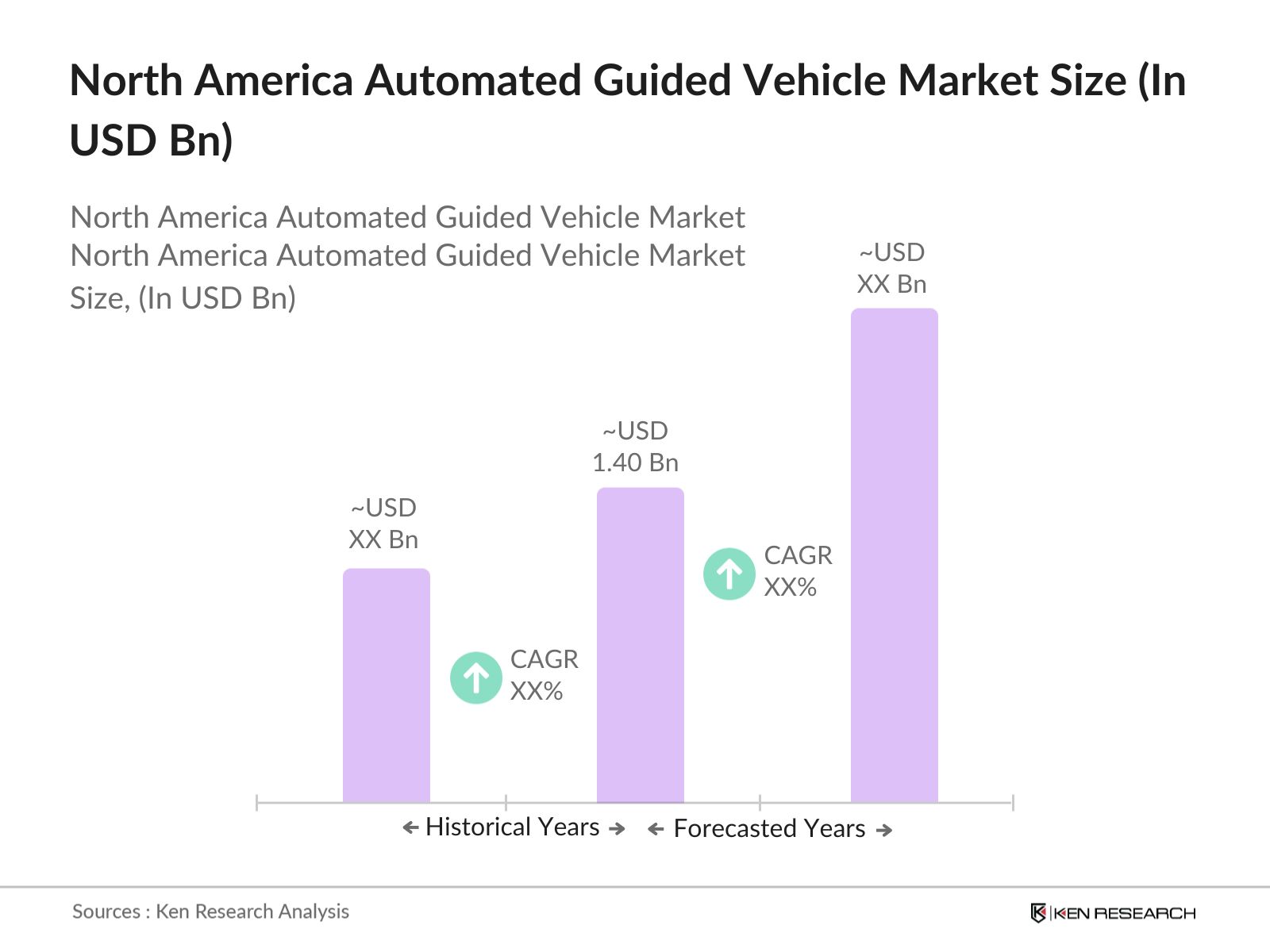

The North America Automated Guided Vehicle market is valued at USD 1.40 billion, driven by the increasing demand for automation in warehousing and manufacturing sectors.

Challenges in the North America Automated Guided Vehicle market include high initial investment costs for AGV systems, technical challenges related to system integration, and the need for skilled operators for smooth operations.

Major players in the North America Automated Guided Vehicle market include Toyota Industries Corporation, Daifuku Co. Ltd., Swisslog Holding AG, JBT Corporation, and KION Group AG.

The North America Automated Guided Vehicle market is propelled by the rise in e-commerce, the expansion of automated warehouses, and labor shortages that drive the demand for AGV systems in various industries.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.