North America Diabetes Drugs Market Outlook to 2030

Region:North America

Author(s):Meenakshi

Product Code:KROD4653

October 2024

93

About the Report

North America Diabetes Drugs Market Overview

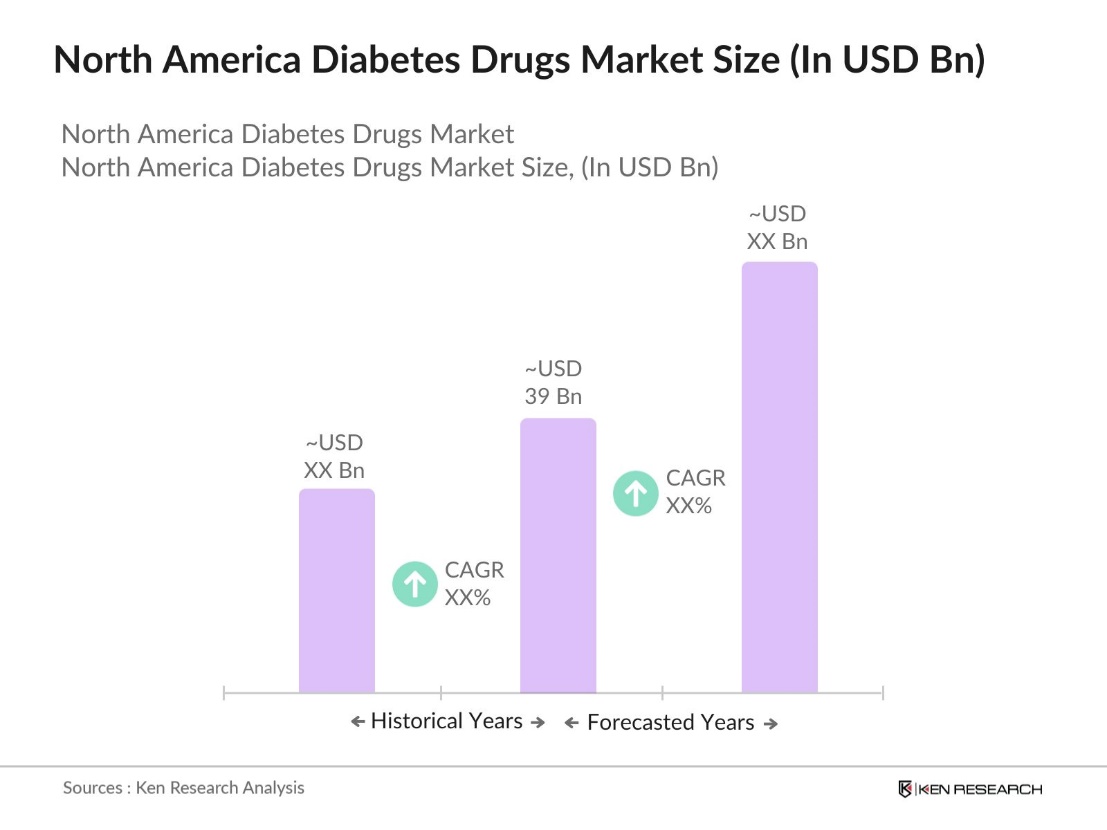

- The North America Diabetes Drugs Market is valued at USD 39 billion, is driven by the increasing prevalence of diabetes, rising obesity rates, and a growing aging population. The rise in the adoption of sedentary lifestyles has contributed significantly to the expansion of the diabetes drugs market. The availability of new drug classes, such as GLP-1 receptor agonists and SGLT-2 inhibitors, and advancements in insulin delivery technologies further drive market growth. Additionally, increasing awareness and government initiatives for diabetes management continue to enhance the market's expansion.

- The market is dominating due to its high diabetes prevalence and substantial healthcare expenditure. The robust healthcare infrastructure in the U.S., coupled with extensive research and development activities, ensures that pharmaceutical companies have the resources to launch innovative treatments. Canada and Mexico also play key roles in the market, with their healthcare systems prioritizing diabetes treatment, but their dominance is relatively limited compared to the U.S.

- In 2023, the FDA approved several innovative diabetes drugs under its novel drug approval program. This initiative aims to fast-track the approval of new treatments that significantly enhance patient care. For diabetes management, biosimilar drugs and advanced combination therapies were key approvals, offering better accessibility and affordability. These regulatory efforts help in reducing treatment gaps and ensuring timely access to cutting-edge diabetes medications, which are crucial for addressing the rising prevalence of diabetes across North America.

North America Diabetes Drugs Market Segmentation

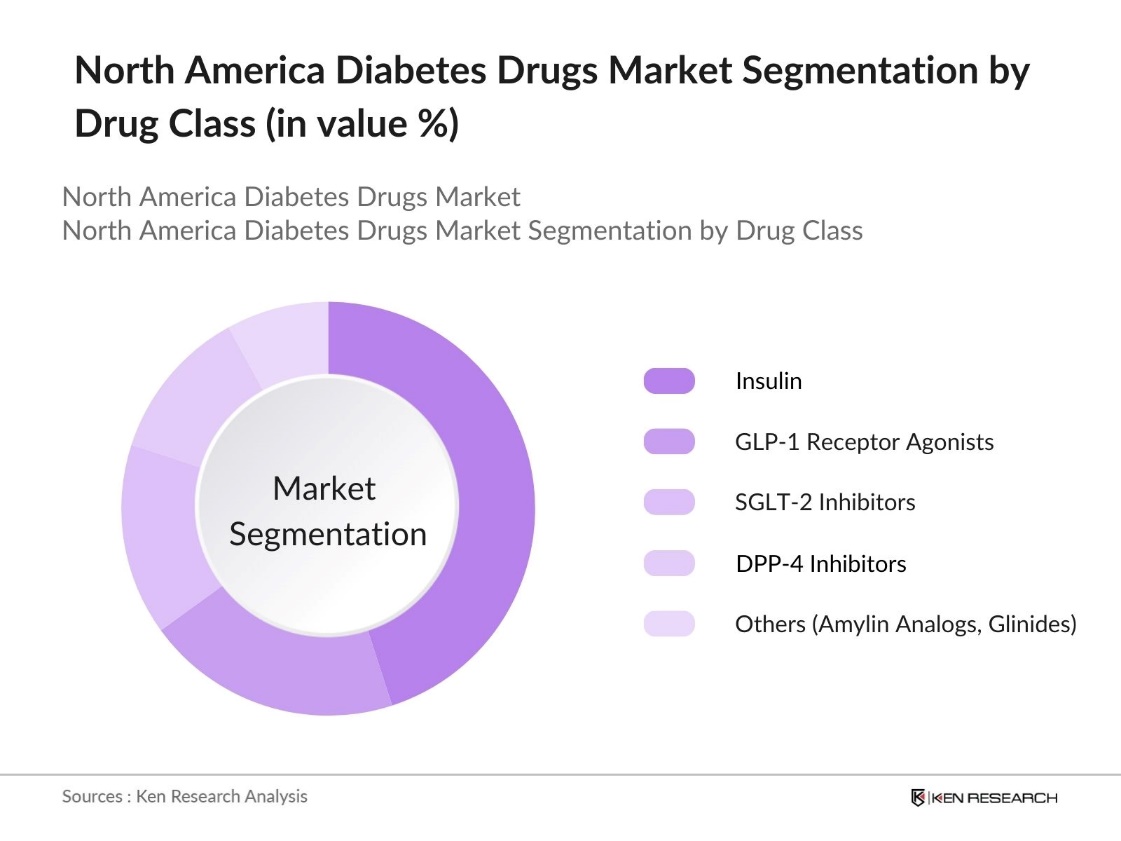

By Drug Class: North America Diabetes Drugs Market is segmented by drug class into insulin, GLP-1 receptor agonists, SGLT-2 inhibitors, DPP-4 inhibitors, and others (amylin analogs, glinides, etc.). Recently, insulin has retained a dominant market share in North America due to its crucial role in managing both Type 1 and advanced Type 2 diabetes. Its long-standing use as the first-line therapy for diabetes treatment, coupled with continuous innovations in delivery methods such as smart insulin pens and pumps, has maintained its dominance.

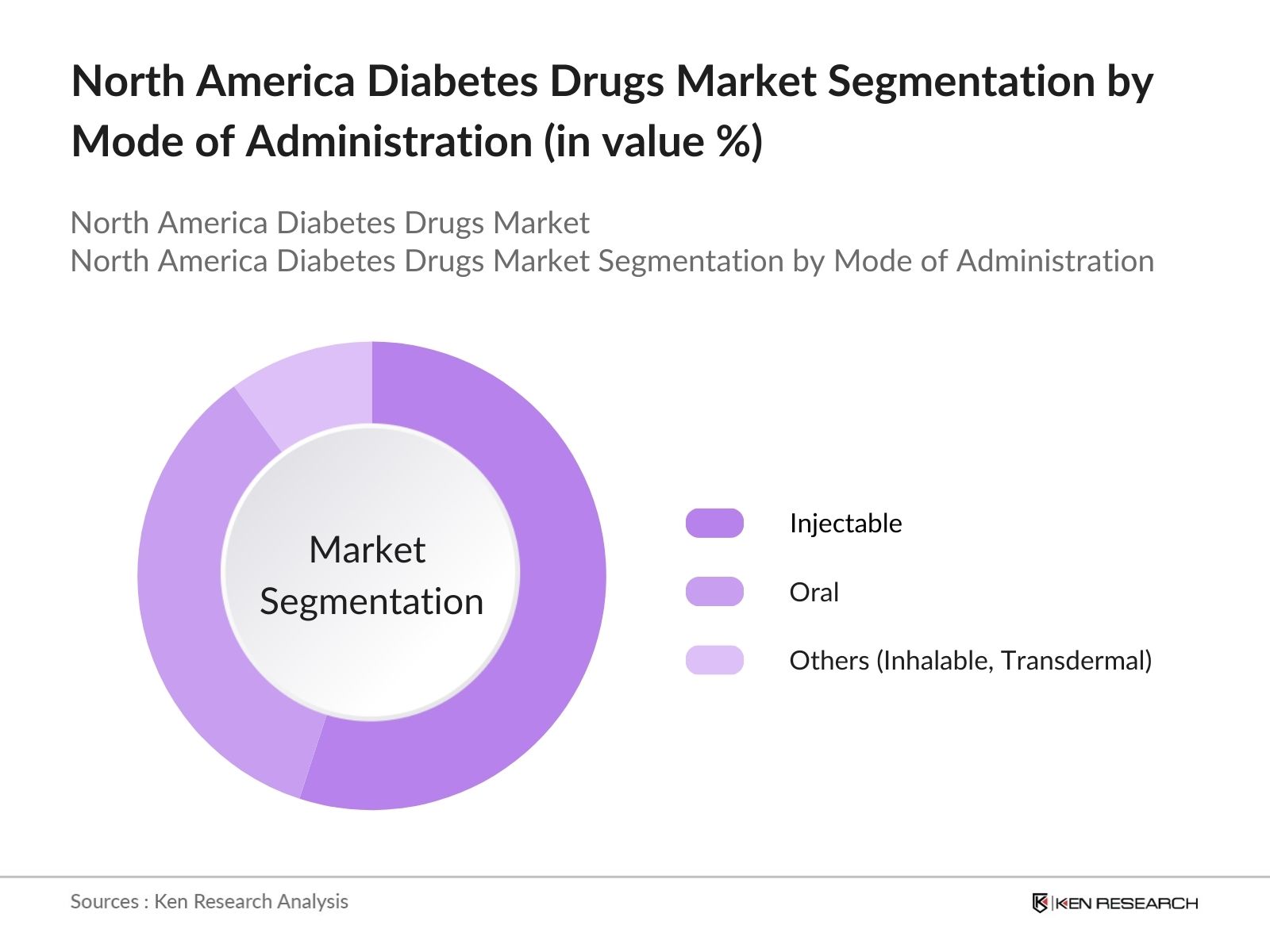

By Mode of Administration: North America Diabetes Drugs Market is segmented by mode of administration into oral, injectable, and others (inhalable, transdermal patches). Injectable drugs, particularly insulin, dominate the market due to the large number of diabetes patients requiring insulin therapy. The advancement of more patient-friendly injectable devices such as pre-filled syringes and pens has improved compliance, further strengthening this segment. While oral drugs, particularly SGLT-2 inhibitors and DPP-4 inhibitors, hold a significant market share, injectable treatments remain critical in severe cases where oral medications prove insufficient.

North America Diabetes Drugs Market Competitive Landscape

The market is led by global pharmaceutical giants known for their extensive research and development efforts in diabetes treatment. The competitive landscape in the diabetes drugs market showcases several key players dominating the market. Major companies like Novo Nordisk and Eli Lilly are industry leaders in insulin products, while newer entrants such as AstraZeneca have carved a niche in the oral diabetes drug market with their innovative SGLT-2 inhibitors.

|

Company Name |

Establishment Year |

Headquarters |

Key Products |

R&D Expenditure |

Revenue (USD Bn) |

Number of Patents |

Global Reach |

Regulatory Approvals |

Collaborations |

|

Novo Nordisk |

1923 |

Bagsvrd, Denmark |

|||||||

|

Eli Lilly and Company |

1876 |

Indianapolis, USA |

|||||||

|

Sanofi |

1973 |

Paris, France |

|||||||

|

AstraZeneca |

1999 |

Cambridge, UK |

|||||||

|

Merck & Co. |

1891 |

Kenilworth, USA |

North America Diabetes Drugs Industry Analysis

Growth Drivers

- Increasing Prevalence of Diabetes: As of 2024, the prevalence of diabetes in North America continues to rise, by the Centers for Disease Control and Prevention (CDC) in 2022, more than 130.0 million people in the U.S., were suffering from diabetes or prediabetes. This rise in diabetes cases is largely driven by lifestyle factors, such as unhealthy diets and sedentary lifestyles. This growing patient population directly fuels the demand for diabetes drugs, with insulin and non-insulin therapies being crucial in managing this chronic condition.

- Advancements in Drug Delivery Systems: In 2024, Medtronic received CE approval for its MiniMed 780G system with the Simplera Sync sensor, marking a significant advancement in insulin delivery technology. This all-in-one continuous glucose monitoring (CGM) system offers real-time glucose monitoring without fingersticks and features an automated insulin correction every 5 minutes, enhancing post-meal glucose control. The integration of this technology reduces the mental burden on patients managing diabetes, while the sensor's ease of use drives higher adoption rates, particularly in Europe.

- Rising Healthcare Expenditure: Healthcare spending in North America is steadily increasing, with diabetes treatment representing a considerable portion of the budget. The growing focus on managing chronic diseases, like diabetes, reflects the need for better treatment solutions, which in turn boosts the demand for diabetes drugs. The rise in healthcare funding highlights the prioritization of chronic disease management, leading to expanded access to diabetes medications. This continued allocation of resources for diabetes care plays a vital role in the growth of the diabetes drugs market.

Market Challenges

- High Cost of Insulin Therapy: The high cost of insulin continues to pose a significant challenge for many patients in North America. Despite advancements in diabetes treatments, many individuals struggle to afford this essential therapy, creating barriers to consistent disease management. High insulin prices also place strain on healthcare systems, limiting access to critical treatments for lower-income populations. This highlights the need for more affordable alternatives, such as biosimilars, which could alleviate financial pressures on both patients and healthcare providers.

- Regulatory Hurdles in Drug Approvals: The approval process for diabetes drugs in North America is stringent and lengthy, posing challenges for bringing new therapies to market. Stringent regulatory requirements, including clinical trials and safety reviews, contribute to extended timelines and higher costs for drug manufacturers. This often delays the introduction of innovative treatments, slowing down market growth and limiting patient access to newer, potentially more effective drugs. Regulatory complexities, therefore, remain a key challenge in this market.

North America Diabetes Drugs Market Future Outlook

Over the next five years, the North America Diabetes Drugs Market is expected to experience significant growth, driven by technological advancements in drug delivery systems, increasing government initiatives for diabetes management, and the rising adoption of biosimilar insulin. The demand for personalized medicine and patient-specific treatment plans will further fuel growth as pharmaceutical companies aim to develop more targeted therapies.

Market Opportunities

- Emerging Biosimilar Drugs: Biosimilars offer a growing opportunity in the diabetes drugs market, providing more affordable alternatives to branded insulin products. As cost-containment strategies become more prominent, biosimilar insulins are being increasingly adopted across North America. Their introduction helps alleviate financial pressures on both healthcare providers and patients, enhancing access to essential diabetes treatments.

- Personalized Medicine for Diabetes: Personalized medicine is transforming diabetes care by enabling treatments tailored to individual patient needs. Advances in genetic profiling and biomarker identification have allowed healthcare providers to develop more precise drug therapies that optimize glycemic control while minimizing side effects. Personalized treatment plans are particularly beneficial for patients with complex cases, including those with multiple comorbidities, improving outcomes and reducing complications.

Scope of the Report

|

Drug Class |

Insulin GLP-1 Receptor Agonists SGLT-2 Inhibitors DPP-4 Inhibitors Others |

|

Mode of Administration |

Oral Injectable Others (Inhalable, Transdermal Patches) |

|

Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

|

End-User |

Hospitals Clinics Homecare Settings |

|

Country |

United States Canada Mexico |

Products

Key Target Audience

Pharmaceutical Companies

Biotechnology Companies

Health Insurance Companies

Government and Regulatory Bodies (FDA, Health Canada)

Investment and Venture Capitalist Firms

Banks and Financial Institutions

Companies

Major Players

Novo Nordisk

Eli Lilly and Company

Sanofi

AstraZeneca

Merck & Co.

Boehringer Ingelheim

Johnson & Johnson

Pfizer Inc.

Novartis AG

GlaxoSmithKline

Takeda Pharmaceutical Company

Mylan N.V.

Biocon Ltd.

Teva Pharmaceuticals

Sun Pharmaceutical Industries

Table of Contents

1. North America Diabetes Drugs Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. North America Diabetes Drugs Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. North America Diabetes Drugs Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Prevalence of Diabetes

3.1.2 Growing Geriatric Population

3.1.3 Advancements in Drug Delivery Systems

3.1.4 Rising Healthcare Expenditure

3.2 Market Challenges

3.2.1 High Cost of Insulin Therapy

3.2.2 Regulatory Hurdles in Drug Approvals

3.2.3 Reimbursement Issues in the Healthcare System

3.3 Opportunities

3.3.1 Emerging Biosimilar Drugs

3.3.2 Personalized Medicine for Diabetes

3.3.3 Expansion of Digital Diabetes Management Tools

3.4 Trends

3.4.1 Shift Towards Oral Drugs (GLP-1 Receptor Agonists)

3.4.2 Development of Combination Therapies

3.4.3 Adoption of Wearable Glucose Monitors

3.5 Government Regulation

3.5.1 FDA Approval Procedures

3.5.2 Reimbursement Guidelines

3.5.3 Price Caps and Controls

3.5.4 Diabetes Treatment Standards (ADA Guidelines)

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. North America Diabetes Drugs Market Segmentation

4.1 By Drug Class (In Value %)

4.1.1 Insulin

4.1.2 GLP-1 Receptor Agonists

4.1.3 SGLT-2 Inhibitors

4.1.4 DPP-4 Inhibitors

4.1.5 Others (Amylin Analogs, Glinides, etc.)

4.2 By Mode of Administration (In Value %)

4.2.1 Oral

4.2.2 Injectable

4.2.3 Others (Inhalable, Transdermal Patches)

4.3 By Distribution Channel (In Value %)

4.3.1 Hospital Pharmacies

4.3.2 Retail Pharmacies

4.3.3 Online Pharmacies

4.4 By End-User (In Value %)

4.4.1 Hospitals

4.4.2 Clinics

4.4.3 Homecare Settings

4.5 By Country (In Value %)

4.5.1 United States

4.5.2 Canada

4.5.3 Mexico

5. North America Diabetes Drugs Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Novo Nordisk

5.1.2 Eli Lilly and Company

5.1.3 Sanofi

5.1.4 Merck & Co.

5.1.5 AstraZeneca

5.1.6 Boehringer Ingelheim

5.1.7 Johnson & Johnson

5.1.8 Pfizer Inc.

5.1.9 Novartis AG

5.1.10 GlaxoSmithKline

5.1.11 Takeda Pharmaceutical Company

5.1.12 Mylan N.V.

5.1.13 Biocon Ltd.

5.1.14 Teva Pharmaceuticals

5.1.15 Sun Pharmaceutical Industries

5.2 Cross Comparison Parameters (Market Share, Drug Portfolio, Revenue, R&D Expenditure, Geographical Presence, Regulatory Approvals, Collaborations, Mergers & Acquisitions)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. North America Diabetes Drugs Market Regulatory Framework

6.1 FDA Regulatory Standards for Diabetes Drugs

6.2 Health Canada Guidelines for Drug Approval

6.3 Compliance with American Diabetes Association (ADA) Treatment Standards

6.4 Patent Expirations and Generic Market Impact

7. North America Diabetes Drugs Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. North America Diabetes Drugs Future Market Segmentation

8.1 By Drug Class (In Value %)

8.2 By Mode of Administration (In Value %)

8.3 By Distribution Channel (In Value %)

8.4 By End-User (In Value %)

8.5 By Country (In Value %)

9. North America Diabetes Drugs Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map of all stakeholders within the North America Diabetes Drugs Market. This step utilizes extensive desk research from secondary and proprietary databases to identify the critical factors influencing the market. Key variables include diabetes prevalence, healthcare spending, and regulatory changes.

Step 2: Market Analysis and Construction

In this phase, historical data on diabetes drug adoption is compiled and analyzed. Metrics such as insulin usage and the penetration of oral diabetes medications are assessed to gauge the markets performance. Additional evaluation of treatment outcomes is conducted to ensure the accuracy of market forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through interviews with industry experts and diabetes care providers. These interviews provide insights into the operational challenges and emerging trends within the market, helping to refine the research findings.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with pharmaceutical companies and diabetes care professionals to verify the findings and ensure a comprehensive analysis. This process confirms market estimates and ensures that the report presents an accurate picture of the North America Diabetes Drugs Market.

Frequently Asked Questions

01. How big is the North America Diabetes Drugs Market?

The North America Diabetes Drugs Market is valued at USD 39 billion, with its growth driven by rising diabetes prevalence and advancements in drug delivery technologies.

02. What are the key challenges in the North America Diabetes Drugs Market?

Challenges in North America Diabetes Drugs Market include high drug costs, regulatory hurdles for new therapies, and increasing competition from biosimilar drugs, which place pressure on market pricing and profitability.

03. Who are the major players in the North America Diabetes Drugs Market?

Key players in North America Diabetes Drugs Market include Novo Nordisk, Eli Lilly, Sanofi, AstraZeneca, and Merck & Co., known for their innovations in insulin and oral diabetes medications.

04. What are the growth drivers of the North America Diabetes Drugs Market?

Growth drivers in North America Diabetes Drugs Market include the increasing prevalence of diabetes, the rise in obesity rates, government initiatives for diabetes management, and the growing adoption of innovative drug therapies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.