North America Radiation Detection Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD8442

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD8442

December 2024

85

The North America radiation detection market is highly competitive, with major players leading through innovations in technology, strategic collaborations, and extensive distribution networks. Notable companies such as Thermo Fisher Scientific, Mirion Technologies, and Ludlum Measurements are actively expanding their product portfolios to cater to diverse industrial and healthcare needs.

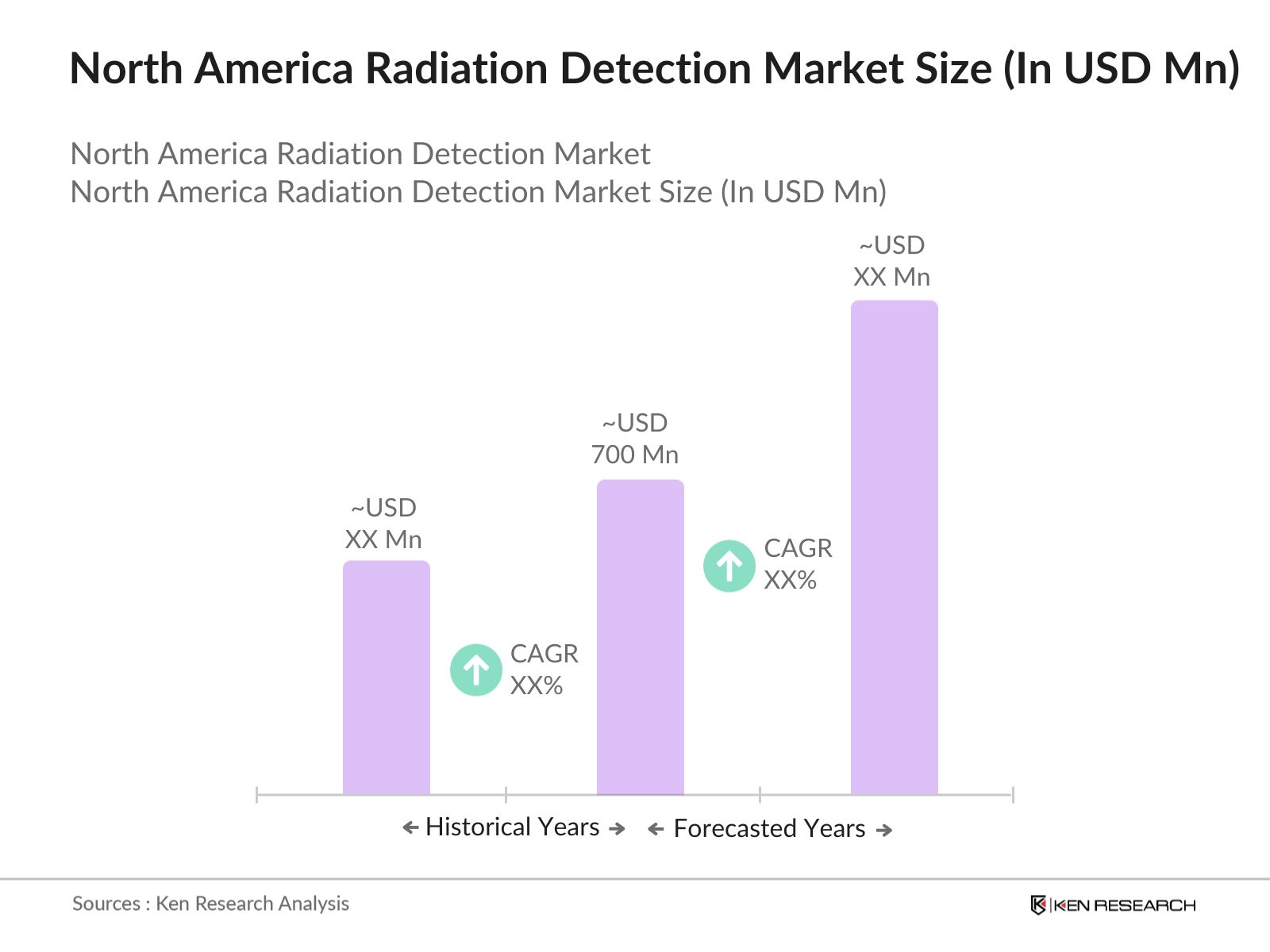

The North America radiation detection market is projected to grow substantially, supported by continued investments in nuclear energy, advancements in healthcare diagnostics, and heightened security concerns. Trends such as the integration of IoT-enabled radiation monitoring, compact portable devices, and AI-based detection systems are expected to drive the market forward. The increasing use of digital platforms for monitoring and regulatory compliance is also anticipated to create new opportunities for industry players, especially as the demand for mobile and cloud-based solutions rises.

|

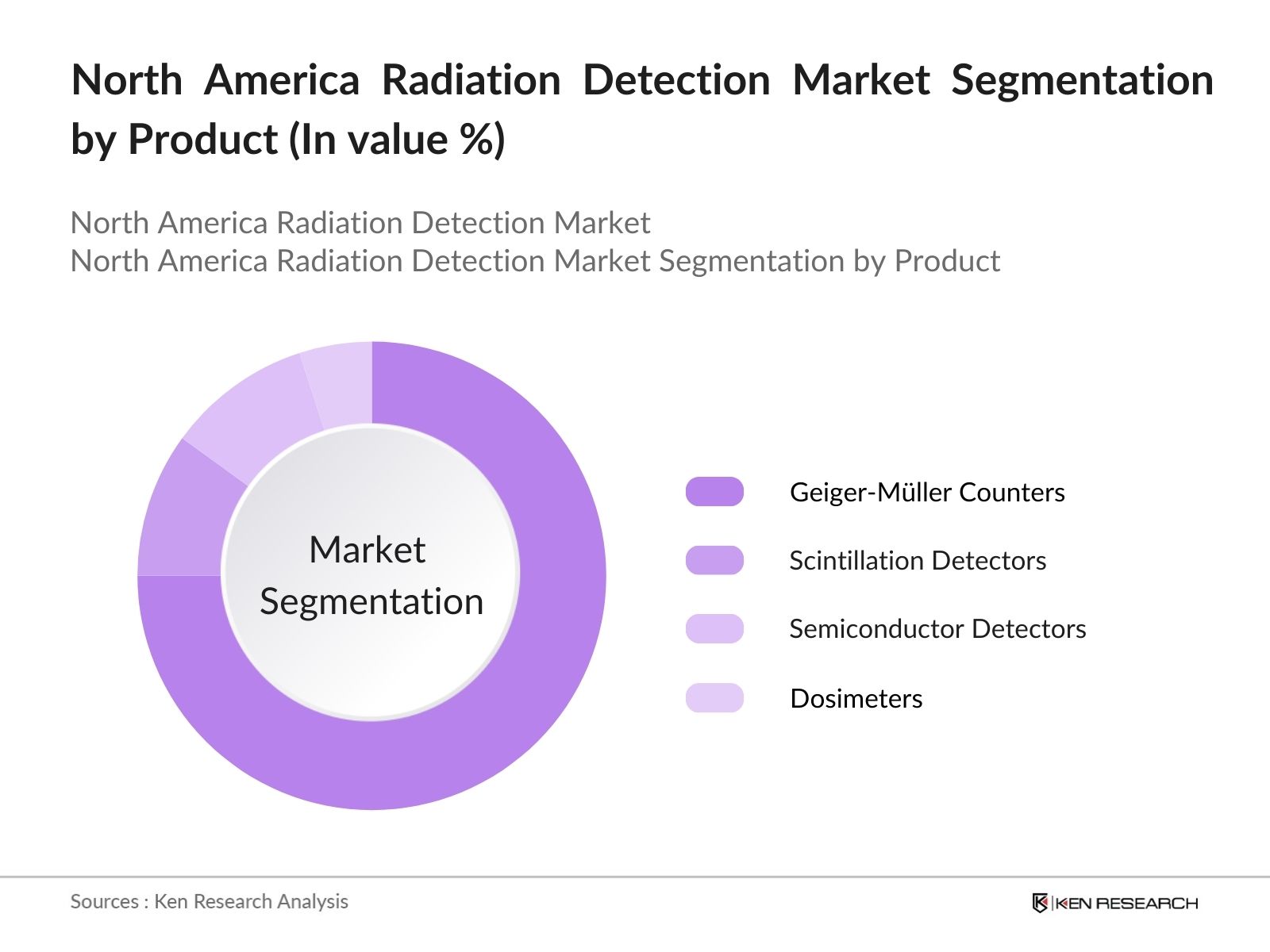

By Product Type |

Geiger-Mller Counters Scintillation Detectors Semiconductor Detectors Dosimeters |

|

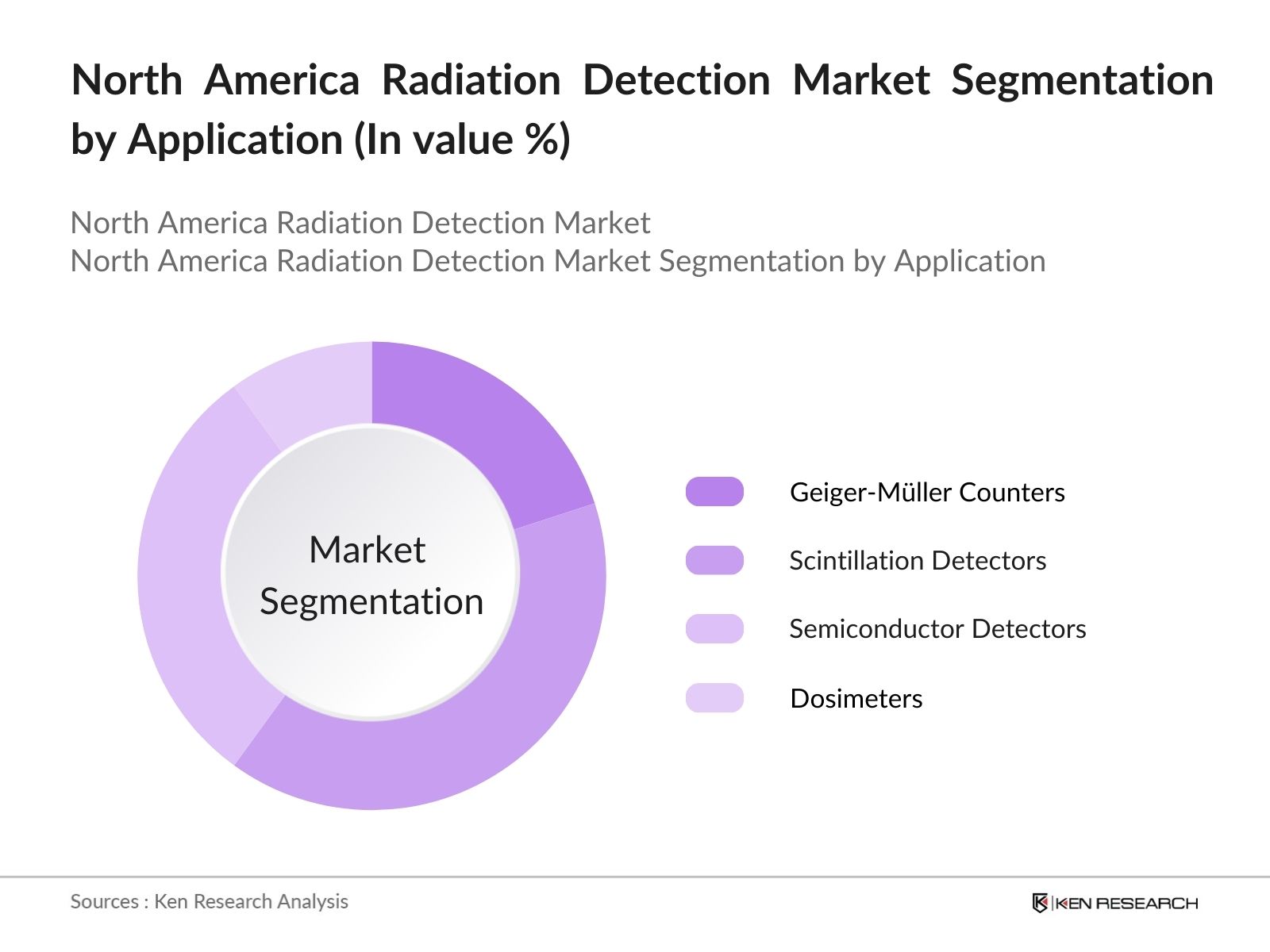

By Application |

Nuclear Power Plants Medical Imaging Industrial Monitoring Defense and Homeland Security |

|

By Detection Type |

Alpha Radiation Beta Radiation Gamma Radiation |

|

By End-User |

Hospitals and Clinics Research Institutes Industrial Facilities Government Agencies |

|

By Region |

USA Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Nuclear Power Generation (Units)

3.1.2. Rising Healthcare Imaging Procedures (No. of Procedures)

3.1.3. Government Safety Initiatives (Policies)

3.1.4. Industrial Radiation Usage (Applications)

3.2. Market Challenges

3.2.1. High Equipment Costs (USD)

3.2.2. Stringent Regulatory Requirements (Compliance)

3.2.3. Limited Skilled Workforce (No. of Professionals)

3.3. Opportunities

3.3.1. Technological Advancements in Detection Equipment (New Patents)

3.3.2. Expansion in Emerging Markets (Regions)

3.3.3. Increasing Demand in Homeland Security (Budget Allocations)

3.4. Trends

3.4.1. Adoption of Digital Radiation Detection (Technology)

3.4.2. Integration with IoT for Real-Time Monitoring (Connected Devices)

3.4.3. Miniaturization of Radiation Detectors (Size)

3.5. Government Regulation

3.5.1. Nuclear Regulatory Commission (NRC) Standards

3.5.2. Radiation Safety Certification Processes (Certification)

3.5.3. Environmental Protection Agency (EPA) Guidelines

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Geiger-Mller Counters

4.1.2. Scintillation Detectors

4.1.3. Semiconductor Detectors

4.1.4. Dosimeters

4.2. By Application (In Value %)

4.2.1. Nuclear Power Plants

4.2.2. Medical Imaging

4.2.3. Industrial Monitoring

4.2.4. Defense and Homeland Security

4.3. By Detection Type (In Value %)

4.3.1. Alpha Radiation

4.3.2. Beta Radiation

4.3.3. Gamma Radiation

4.4. By End-User (In Value %)

4.4.1. Hospitals and Clinics

4.4.2. Research Institutes

4.4.3. Industrial Facilities

4.4.4. Government Agencies

4.5. By Region (In Value %)

4.5.1. USA

4.5.2. Canada

4.5.3. Mexico

5.1. Detailed Profiles of Major Companies

5.1.1. Thermo Fisher Scientific Inc.

5.1.2. Mirion Technologies, Inc.

5.1.3. Ludlum Measurements Inc.

5.1.4. Landauer, Inc.

5.1.5. Ametek Inc.

5.1.6. Fluke Corporation

5.1.7. Canberra Industries, Inc.

5.1.8. GE Healthcare

5.1.9. Radiation Detection Technologies Inc.

5.1.10. Arrow-Tech Inc.

5.1.11. Sun Nuclear Corporation

5.1.12. Durridge Company Inc.

5.1.13. Infab Corporation

5.1.14. Fuji Electric Co., Ltd.

5.1.15. Bar-Ray Products Inc.

5.2. Cross Comparison Parameters (R&D Investments, Manufacturing Capacity, Distribution Network, Product Portfolio, Revenue, Market Share, Customer Base, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Funding

5.8. Private Equity Investments

6.1. Licensing and Compliance Requirements

6.2. Radiation Exposure Limits

6.3. Certification Processes for Safety Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Detection Type (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact Us

This phase involves mapping out the ecosystem of the North America Radiation Detection Market, including all major stakeholders. Extensive desk research is conducted using both proprietary and public databases to identify the core market dynamics and influential variables.

Historical data is analyzed to construct a comprehensive market profile, examining factors like product adoption rates, market demand by sector, and regional growth trends. This phase also involves a review of quality and accuracy statistics for reliable data synthesis.

Market hypotheses are developed based on initial findings and validated through consultations with industry experts via CATIs. These discussions provide insights into market operational challenges and opportunities directly from industry leaders.

The final phase integrates direct feedback from radiation detection device manufacturers and healthcare providers, corroborating data with real-world market observations. This ensures a well-rounded, accurate analysis ready for business strategy and decision-making.

The North America Radiation Detection Market is valued at USD 700 million, supported by growing healthcare diagnostic demands, nuclear power applications, and homeland security investments.

Key challenges in the North America Radiation Detection Market include stringent regulatory compliance requirements, high equipment costs, and a limited skilled workforce to operate complex radiation detection systems.

Major players in the North America Radiation Detection Market include Thermo Fisher Scientific, Mirion Technologies, and Ludlum Measurements, all of which have significant market presence due to their innovative technologies and reliable product portfolios.

Growth in this North America Radiation Detection Market is primarily driven by increased adoption in nuclear power plants, expansion of healthcare radiological applications, and the rising need for advanced safety protocols in defense and homeland security.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.