Saudi Arabia Aerospace Plastics Market Outlook 2030

Region:Middle East

Author(s):Shivani Mehra

Product Code:KROD7846

November 2024

82

About the Report

Saudi Arabia Aerospace Plastics Market Overview

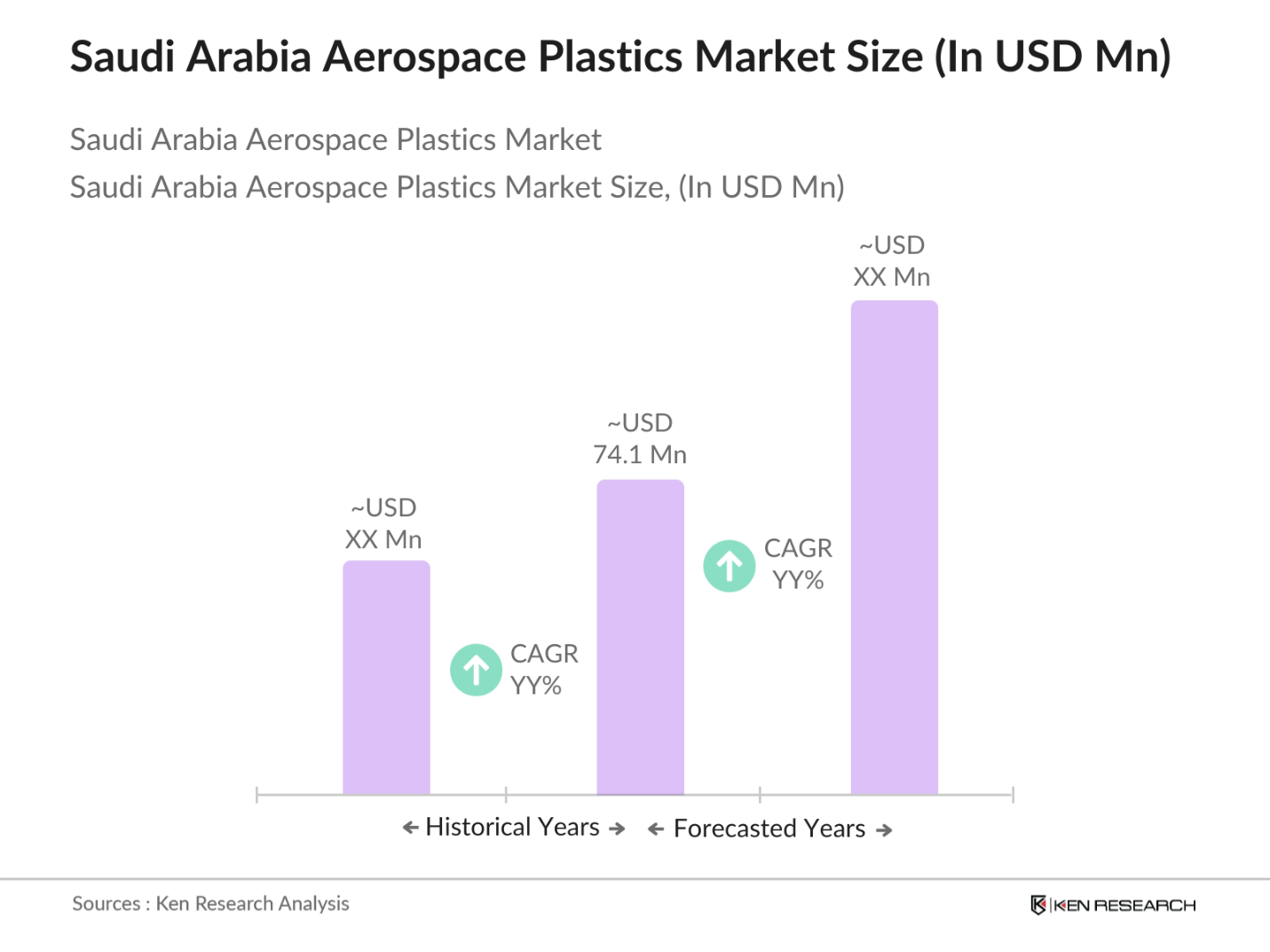

- The aerospace plastics market in Saudi Arabia is valued at USD 74.1 million, driven by increasing demand for lightweight and high-performance materials in aviation and defense sectors. The surge in aircraft production, coupled with advancements in aerospace components, contributes to this valuation. Factors like enhanced fuel efficiency and reduced carbon emissions further bolster demand for aerospace plastics. These materials offer superior durability, corrosion resistance, and ease of processing, positioning them as a preferred choice in the aerospace industry.

- Key cities such as Riyadh and Jeddah dominate the aerospace plastics market in Saudi Arabia. Riyadh, as the capital, hosts major aerospace manufacturing plants and defense contractors, making it a hub for aerospace plastic consumption. Jeddah, with its strategic location and bustling aviation industry, plays a significant role in driving demand. These cities benefit from government-backed investments in aviation infrastructure, including expansions at key airports and aviation research facilities.

- In 2023, the Saudi government allocated $20 billion for the development of aviation infrastructure, which includes the modernization of airports, aircraft maintenance facilities, and local manufacturing units. This investment aims to improve the country's aviation ecosystem and expand aviation infrastructure, creating significant opportunities for aerospace plastic manufacturers to provide advanced materials for both aircraft construction and maintenance. This investment is critical in supporting the growth of the aviation sector and enhancing the demand for aerospace plastics.

Saudi Arabia Aerospace Plastics Market Segmentation

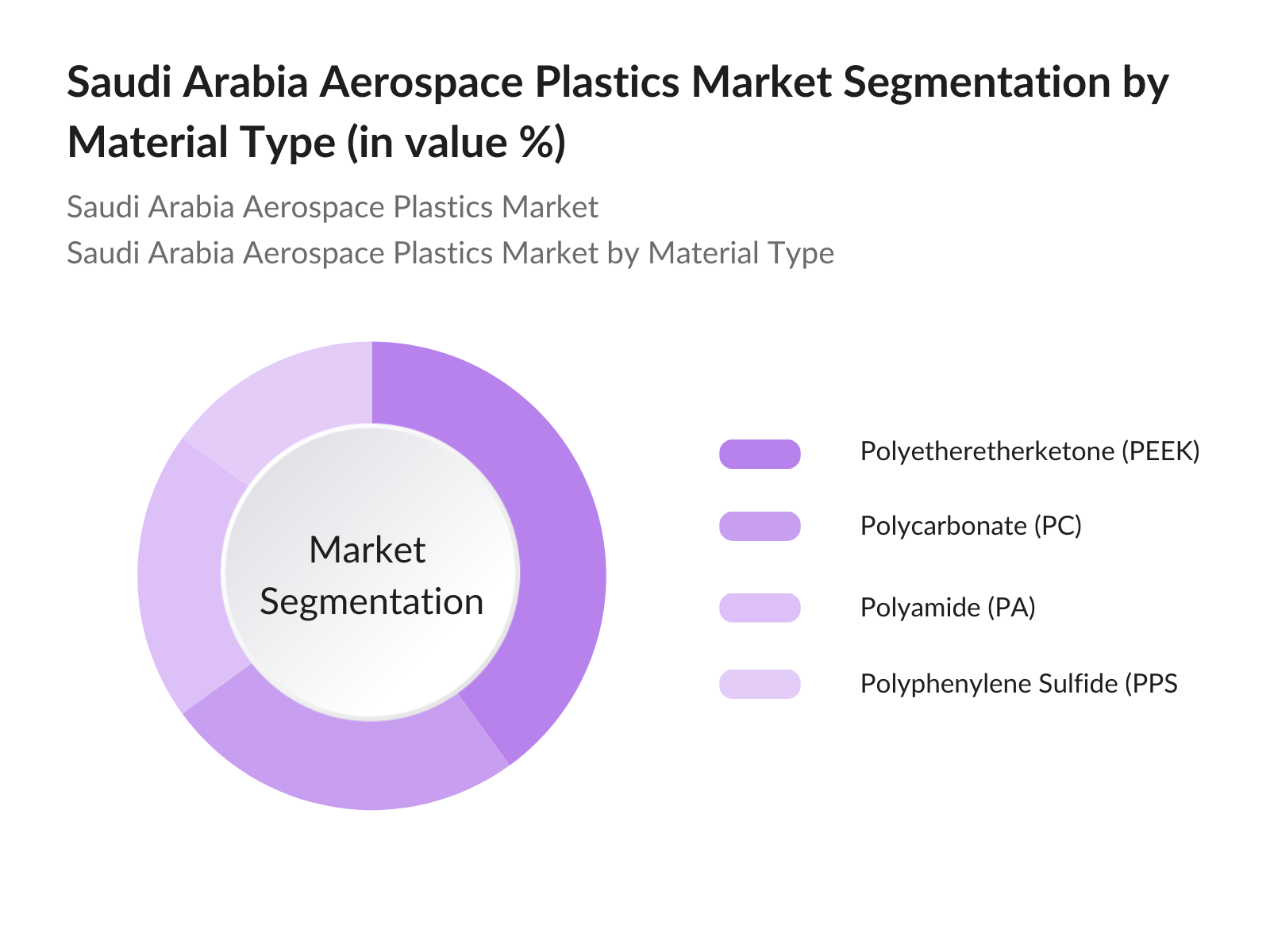

- By Material Type: The Saudi Arabia aerospace plastics market is segmented by material type into Polyetheretherketone (PEEK), Polycarbonate (PC), Polyamide (PA), and Polyphenylene Sulfide (PPS). Polyetheretherketone (PEEK) dominates the market under the material type segment, primarily due to its superior strength-to-weight ratio and resistance to high temperatures, making it ideal for critical aerospace applications like engine components and airframes. Additionally, its usage in military aircraft production is also a key driver of its dominance.

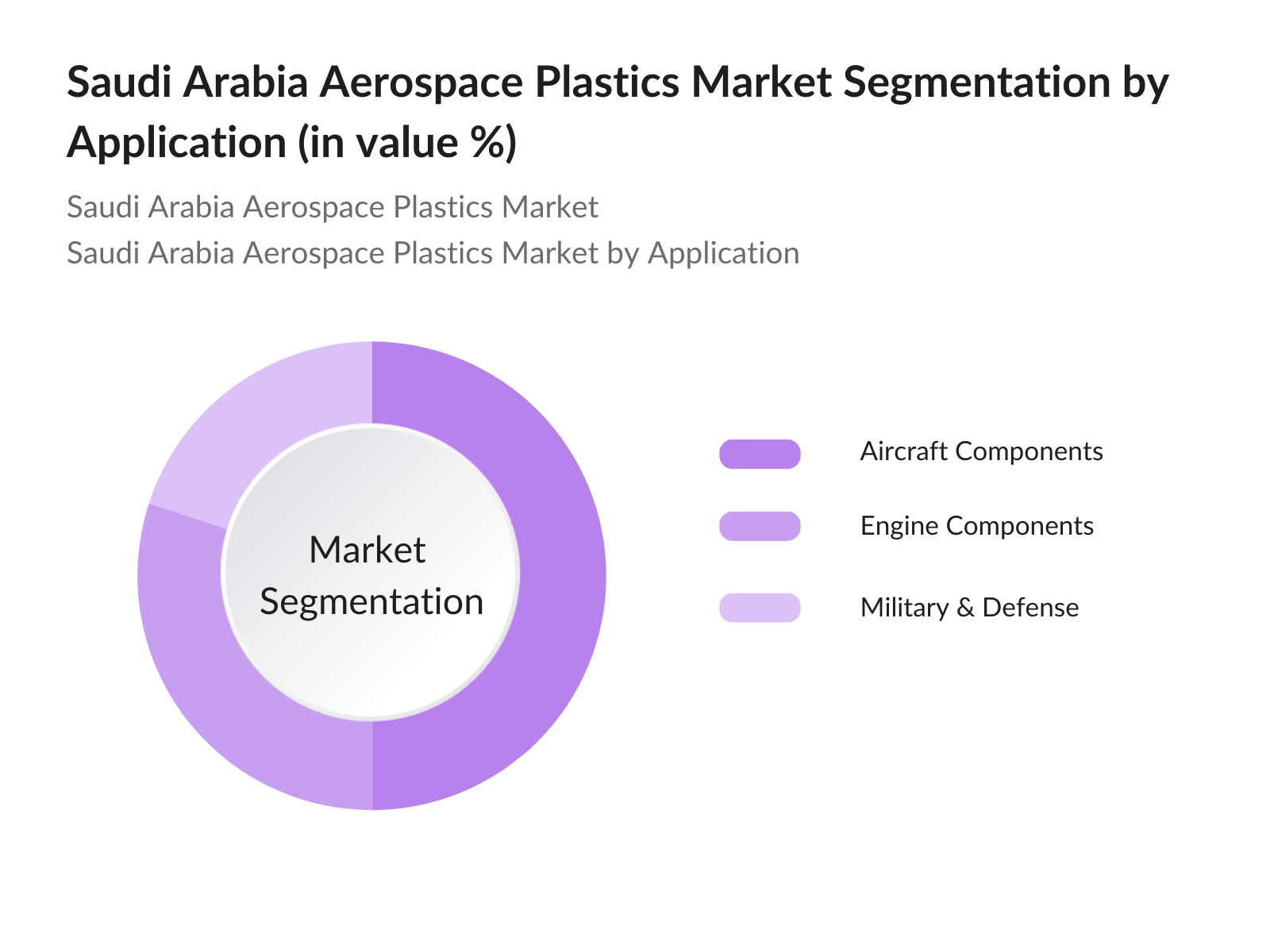

- By Application: The Saudi Arabia aerospace plastics market is segmented by application into Aircraft Components, Engine Components, and Military & Defense. Aircraft Components, such as fuselage parts, wings, and interior cabin elements, represent the largest application segment, driven by the demand for lightweight and fuel-efficient materials in civil aviation. Engine Components come next, with high-temperature resistant plastics like PEEK playing a key role in aerospace engine manufacturing due to their durability and ability to withstand extreme heat.

Saudi Arabia Aerospace Plastics Market Competitive Landscape

The Saudi Arabia aerospace plastics market is dominated by both local and global players who have invested significantly in research and development to enhance the properties of aerospace plastics. Major players are focusing on collaborations with aerospace OEMs, expanding their product portfolios to cater to advanced aerospace applications.

|

Company |

Establishment Year |

Headquarters |

Key Parameters |

|

Solvay S.A. |

1863 |

Brussels, Belgium |

- |

|

SABIC |

1976 |

Riyadh, Saudi Arabia |

- |

|

Victrex Plc |

1993 |

Lancashire, UK |

- |

|

BASF SE |

1865 |

Ludwigshafen, Germany |

- |

|

DuPont de Nemours, Inc. |

1802 |

Wilmington, USA |

- |

Saudi Arabia Aerospace Plastics Industry Analysis

Market Growth Drivers

- Adoption of Lightweight Materials in Aircraft Manufacturing: The use of lightweight aerospace plastics in aircraft manufacturing has increased significantly in Saudi Arabia, primarily to enhance fuel efficiency and performance. For example, replacing metal components with plastic composites leads to notable weight reduction, which directly translates into fuel savings. In 2023, the Saudi aviation sector saw an increase in aircraft production, driven by both civilian and military demand. Lightweight plastics, such as carbon-fiber-reinforced polymers, are increasingly being used in structural components, reducing fuel consumption and carbon emissions in the aviation sector by 2-3 metric tons per aircraft annually.

- Increased Demand for Fuel-Efficient Aircraft: With rising fuel costs and environmental regulations, fuel efficiency has become a top priority for Saudi Arabia's aviation industry. Lightweight plastics play a critical role in reducing fuel consumption. According to the International Air Transport Association (IATA), global airlines spend a significant portion of their operating costs on fuel, and reducing aircraft weight directly impacts fuel efficiency. This has driven the increased adoption of aerospace plastics in Saudi aircraft production. In 2024, the introduction of advanced plastic materials into the local aerospace industry contributed to notable fuel efficiency gains across the fleet.

- Government Support and Manufacturing Initiatives: Saudi Arabia is focusing on diversifying the economy and building a robust manufacturing sector, including aerospace. The government has invested in the aviation industry to modernize the fleet and build local aircraft manufacturing capabilities. These initiatives encourage local production and innovation, allowing Saudi manufacturers to integrate advanced plastic materials that improve fuel efficiency and reduce the environmental footprint of the aviation industry.

Market Challenges:

- High Material Costs: The cost of aerospace-grade plastics remains a significant challenge for manufacturers in Saudi Arabia. Global fluctuations in the prices of raw materials, especially those derived from petroleum, have directly impacted the costs of producing high-performance plastics. In 2023, polymer import prices into Saudi Arabia increased due to disruptions in the global supply chain, putting additional financial pressure on local manufacturers. The reliance on imports for critical materials further exacerbates the cost issues, making it challenging for Saudi-based companies to remain competitive in the global aerospace market.

- Stringent Regulatory Barriers: Aerospace plastic manufacturers in Saudi Arabia must comply with stringent safety and quality standards imposed by the General Authority of Civil Aviation (GACA) and international bodies like the International Civil Aviation Organization (ICAO). The need to meet these rigorous aviation standards requires costly testing and certification procedures, which add to production expenses. Furthermore, frequent updates to international safety standards necessitate constant adaptation, posing a challenge for manufacturers to keep up with both regulatory compliance and innovation simultaneously.

Saudi Arabia Aerospace Plastics Market Future Outlook

Over the next five years, the Saudi Arabia aerospace plastics market is expected to grow significantly, driven by ongoing advancements in aerospace materials and increasing demand for lightweight, fuel-efficient components. Government investments in the aerospace sector, along with the rising demand for commercial and military aircraft, will continue to fuel market growth. Additionally, innovations in 3D printing and advanced composite materials will further enhance the usage of aerospace plastics.

Market Opportunities:

- Increase in Domestic Aircraft Production: The Saudi aerospace industry has witnessed an increase in domestic aircraft production, providing significant opportunities for the aerospace plastics market. In 2023, the General Authority for Military Industries (GAMI) reported the production of 25 new aircraft units, which included both military and civilian aircraft. This trend is set to continue as part of Saudi Arabias broader industrial strategy to localize aircraft manufacturing. The growing focus on producing aircraft domestically increases the demand for high-performance, lightweight plastics used in structural components, enhancing fuel efficiency and reducing operating costs for local manufacturers.

- Rising Demand for UAVs (Unmanned Aerial Vehicles): The increasing use of Unmanned Aerial Vehicles (UAVs) in both civilian and defense applications in Saudi Arabia presents a substantial growth opportunity for aerospace plastics. In 2023, the Saudi government announced plans to enhance the production of UAVs as part of its broader technological innovation strategy. Lightweight aerospace plastics are critical in UAV manufacturing due to their ability to reduce weight while maintaining structural integrity. This rise in UAV demand is expected to boost the use of advanced plastic composites, offering long-term growth prospects for the aerospace plastics market.

Scope of the Report

|

By Material Type |

Polyetheretherketone (PEEK) Polycarbonate (PC) Polyamide (PA) Polyphenylene Sulfide (PPS) Others |

|

By Application |

Aircraft Interiors Airframe Structures Engine Components Electrical Components Others |

|

By End-Use Industry |

Commercial Aviation Defense Space Industry |

|

By Manufacturing Process |

Injection Molding Thermoforming Additive Manufacturing Extrusion Others |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Aerospace Manufacturers

Defense Contractors

Government and Regulatory Bodies (General Authority of Civil Aviation GACA)

Aviation Infrastructure Companies

Material Suppliers and Distributors

Investments and Venture Capitalist Firms

R&D Institutes in Aerospace Materials

Aviation Engineering Companies

Companies

Players mentioned in the report

Solvay S.A.

SABIC (Saudi Basic Industries Corporation)

Victrex Plc

BASF SE

DuPont de Nemours, Inc.

Evonik Industries AG

Mitsubishi Chemical Corporation

Hexcel Corporation

Teijin Limited

Toray Industries, Inc.

Arkema S.A.

Gurit Holding AG

Owens Corning

Celanese Corporation

RTP Company

Table of Contents

1. Saudi Arabia Aerospace Plastics Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Saudi Arabia Aerospace Plastics Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Saudi Arabia Aerospace Plastics Market Analysis

3.1 Growth Drivers (Lightweight Materials, Fuel Efficiency)

3.2 Market Challenges (High Material Costs, Regulatory Barriers)

3.3 Opportunities (Increase in Aircraft Production, Emerging Defense Sector)

3.4 Trends (3D Printing, Advanced Composites in Plastics)

3.5 Government Regulations (Aviation Standards, Import Tariffs)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Suppliers, Manufacturers, Government Entities)

3.8 Porters Five Forces (Bargaining Power of Suppliers, Threat of Substitutes)

3.9 Competition Ecosystem

4. Saudi Arabia Aerospace Plastics Market Segmentation

4.1 By Material Type (In Value %)

4.1.1 Polyetheretherketone (PEEK)

4.1.2 Polycarbonate (PC)

4.1.3 Polyamide (PA)

4.1.4 Polyphenylene Sulfide (PPS)

4.1.5 Others

4.2 By Application (In Value %)

4.2.1 Aircraft Interiors

4.2.2 Airframe Structures

4.2.3 Engine Components

4.2.4 Electrical Components

4.2.5 Others

4.3 By End-Use Industry (In Value %)

4.3.1 Commercial Aviation

4.3.2 Defense

4.3.3 Space Industry

4.4 By Manufacturing Process (In Value %)

4.4.1 Injection Molding

4.4.2 Thermoforming

4.4.3 Additive Manufacturing

4.4.4 Extrusion

4.4.5 Others

4.5 By Region (In Value %)

4.5.1 Central Region

4.5.2 Western Region

4.5.3 Eastern Region

4.5.4 Northern Region

4.5.5 Southern Region

5. Saudi Arabia Aerospace Plastics Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Solvay S.A.

5.1.2 SABIC (Saudi Basic Industries Corporation)

5.1.3 Victrex Plc

5.1.4 BASF SE

5.1.5 DuPont de Nemours, Inc.

5.1.6 Evonik Industries AG

5.1.7 Mitsubishi Chemical Corporation

5.1.8 Hexcel Corporation

5.1.9 Teijin Limited

5.1.10 Toray Industries, Inc.

5.1.11 Arkema S.A.

5.1.12 Gurit Holding AG

5.1.13 Owens Corning

5.1.14 Celanese Corporation

5.1.15 RTP Company

5.2 Cross Comparison Parameters (Material Innovation, Market Share, Sustainability Initiatives, Geographic Presence, R&D Expenditure, Strategic Partnerships, Revenue, Manufacturing Capacity)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Venture Capital, Government Funding)

5.7 Private Equity Investments

6. Saudi Arabia Aerospace Plastics Market Regulatory Framework

6.1 Environmental Standards

6.2 Compliance Requirements (Saudi Standards, Metrology, and Quality Organization SASO)

6.3 Certification Processes (Aerospace Material Standards, International Aviation Regulations)

7. Saudi Arabia Aerospace Plastics Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Saudi Arabia Aerospace Plastics Future Market Segmentation

8.1 By Material Type (In Value %)

8.2 By Application (In Value %)

8.3 By End-Use Industry (In Value %)

8.4 By Manufacturing Process (In Value %)

8.5 By Region (In Value %)

9. Saudi Arabia Aerospace Plastics Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Marketing Initiatives (Target Customer Segments, Region-Specific Marketing)

9.3 White Space Opportunity Analysis

9.4 Customer Cohort Analysis (Commercial, Defense, Space Sector Analysis)

Research Methodology

Step 1: Identification of Key Variables

In this phase, we identified the key variables driving the Saudi Arabia Aerospace Plastics Market through extensive desk research. Using proprietary databases and government reports, we gathered data on production levels, consumption trends, and regulatory frameworks. The focus was to understand the interplay between market drivers and the influence of lightweight material advancements.

Step 2: Market Analysis and Construction

We compiled and analyzed historical market data related to the aerospace plastics industry in Saudi Arabia. This included evaluating the adoption of high-performance polymers in aircraft components and estimating the market penetration across both commercial and defense aviation. The analysis aimed to construct a detailed market size and growth pattern, backed by verified data.

Step 3: Hypothesis Validation and Expert Consultation

We developed market hypotheses based on the data collected, which were then validated through expert consultations. Interviews were conducted with aerospace engineers, material suppliers, and defense contractors to gain practical insights into market dynamics and validate growth drivers identified earlier.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing the research findings to produce a comprehensive report. This phase included verifying the data through bottom-up approaches, including direct engagement with Saudi-based aerospace manufacturers and suppliers. This ensured the accuracy and validity of market projections.

Frequently Asked Questions

01. How big is the Saudi Arabia Aerospace Plastics Market?

The Saudi Arabia aerospace plastics market is valued at USD 74.1 million, driven by increasing demand for lightweight materials in aviation and defense sectors. Government initiatives to expand the aerospace industry further support this growth.

02. What are the challenges in the Saudi Arabia Aerospace Plastics Market?

The primary challenges include high raw material costs and stringent aviation regulations. Additionally, the reliance on imported raw materials increases production costs, limiting local manufacturers' competitiveness.

03. Who are the major players in the Saudi Arabia Aerospace Plastics Market?

Key players include Solvay S.A., SABIC, Victrex Plc, BASF SE, and DuPont. These companies lead the market due to their advanced materials technology, strong partnerships with aerospace OEMs, and high R&D investment.

04. What are the growth drivers of the Saudi Arabia Aerospace Plastics Market?

Growth is driven by the increasing demand for fuel-efficient aircraft, government investments in expanding the aerospace sector, and technological advancements in lightweight materials like PEEK and PPS. The defense sector also contributes significantly to demand.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.