US Optic Fiber Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD7393

November 2024

97

About the Report

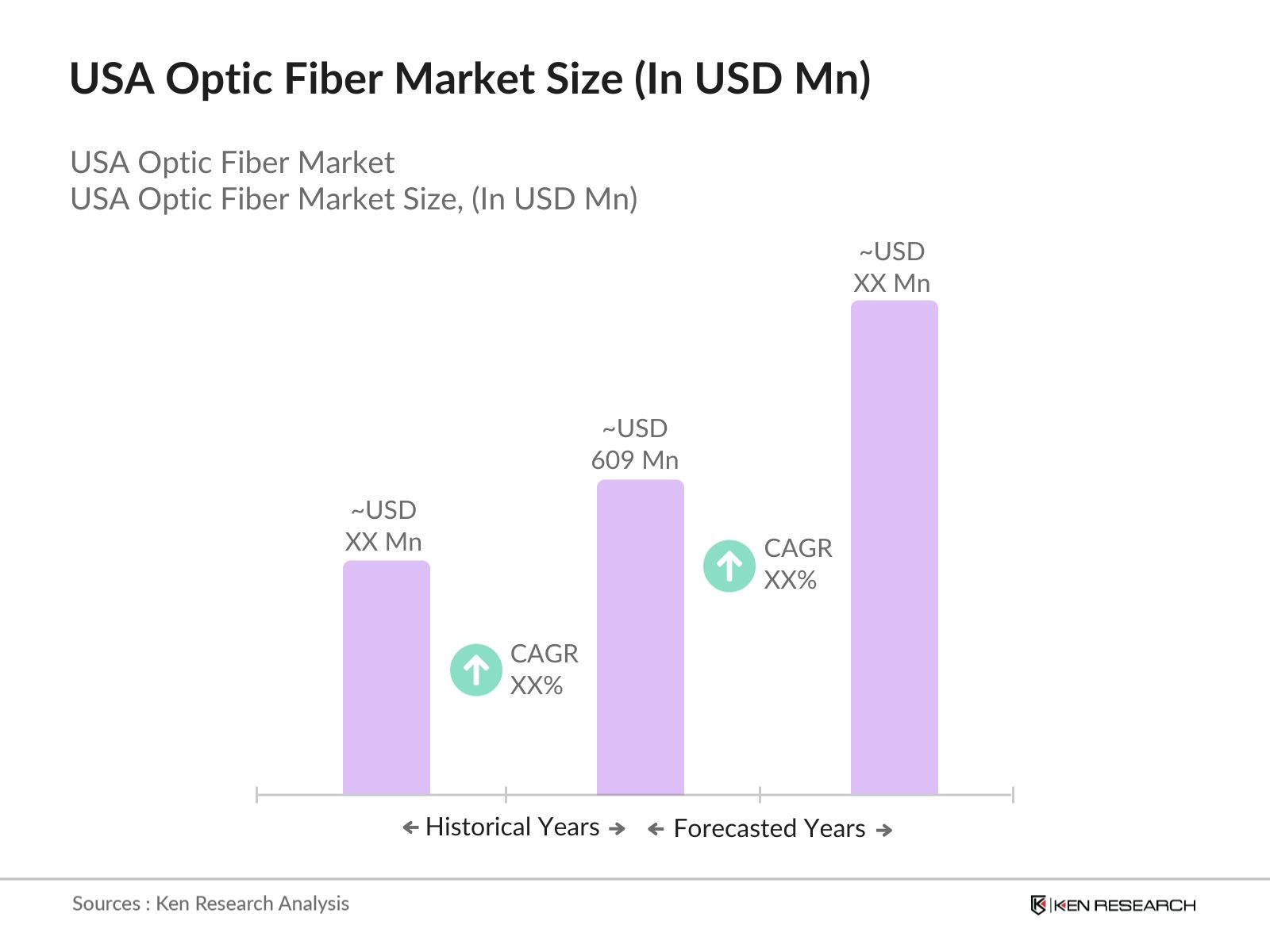

USA Optic Fiber Market Overview

- The USA optic fiber market is valued at USD 609 Million, driven by surging demand for high-speed internet and the expansion of 5G networks across the country. Over the past five years, investments in fiber infrastructure have significantly increased, supported by government incentives aimed at improving broadband access in rural areas. The growth is also driven by the increasing adoption of cloud-based services and Internet of Things (IoT) technologies, which require faster and more reliable data transmission.

- Major cities such as New York, San Francisco, and Washington D.C. are key contributors to the optic fiber market, largely due to their advanced technological infrastructure and high demand for 5G deployment. These cities are home to large data centers and corporate headquarters of tech giants, which create a constant demand for reliable, high-speed connectivity. The West Coast, in particular, benefits from the presence of Silicon Valley and the tech industry, which drives a substantial portion of optic fiber demand in the region.

- he U.S. governments Infrastructure Investment and Jobs Act, passed in 2021, continues to have a significant impact on the optic fiber market. By 2024, over $65 billion had been allocated to expand broadband access, with a large portion dedicated to fiber optic installations. This funding supports both urban and rural broadband projects, providing a substantial boost to fiber optic infrastructure development.

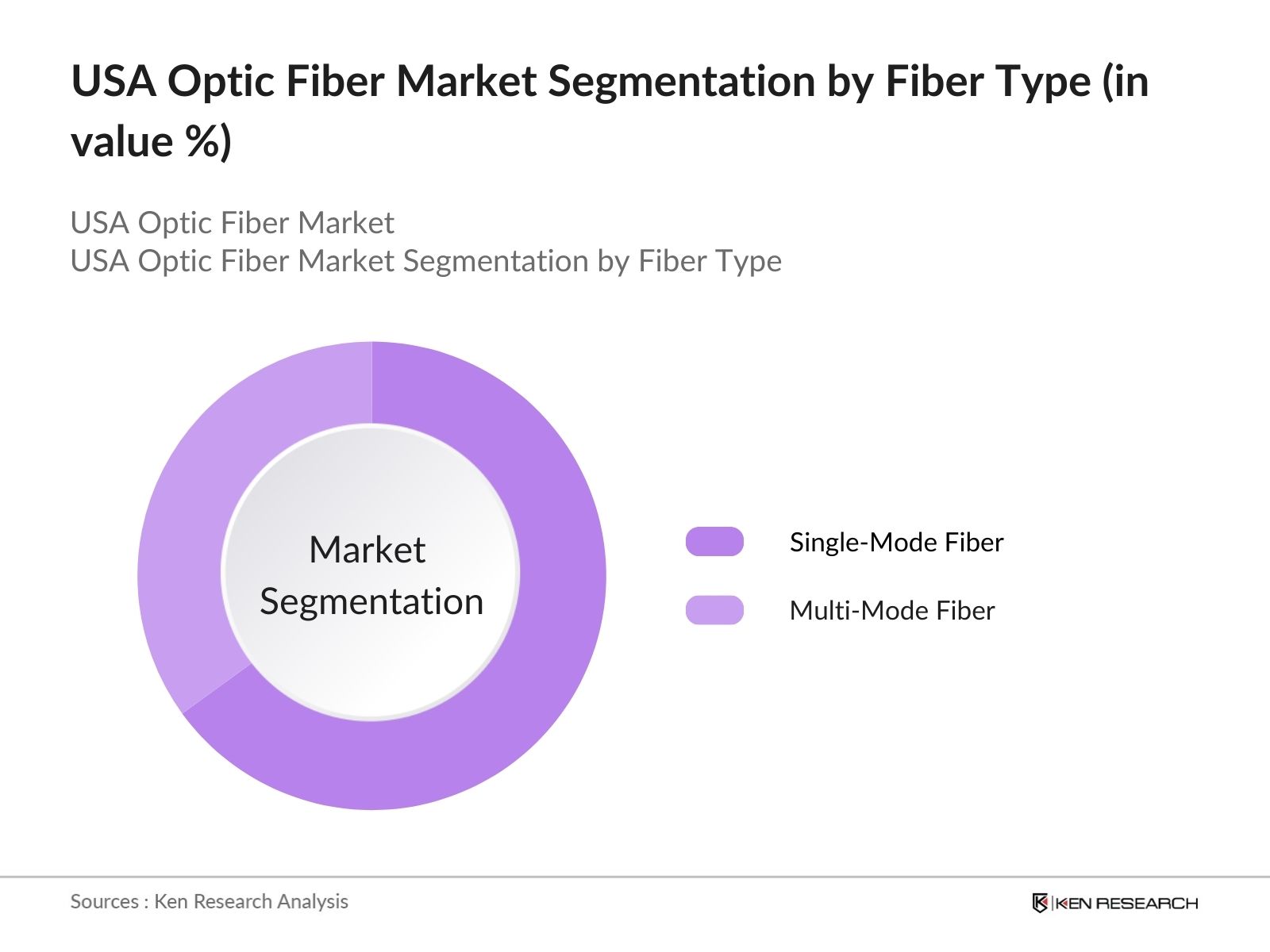

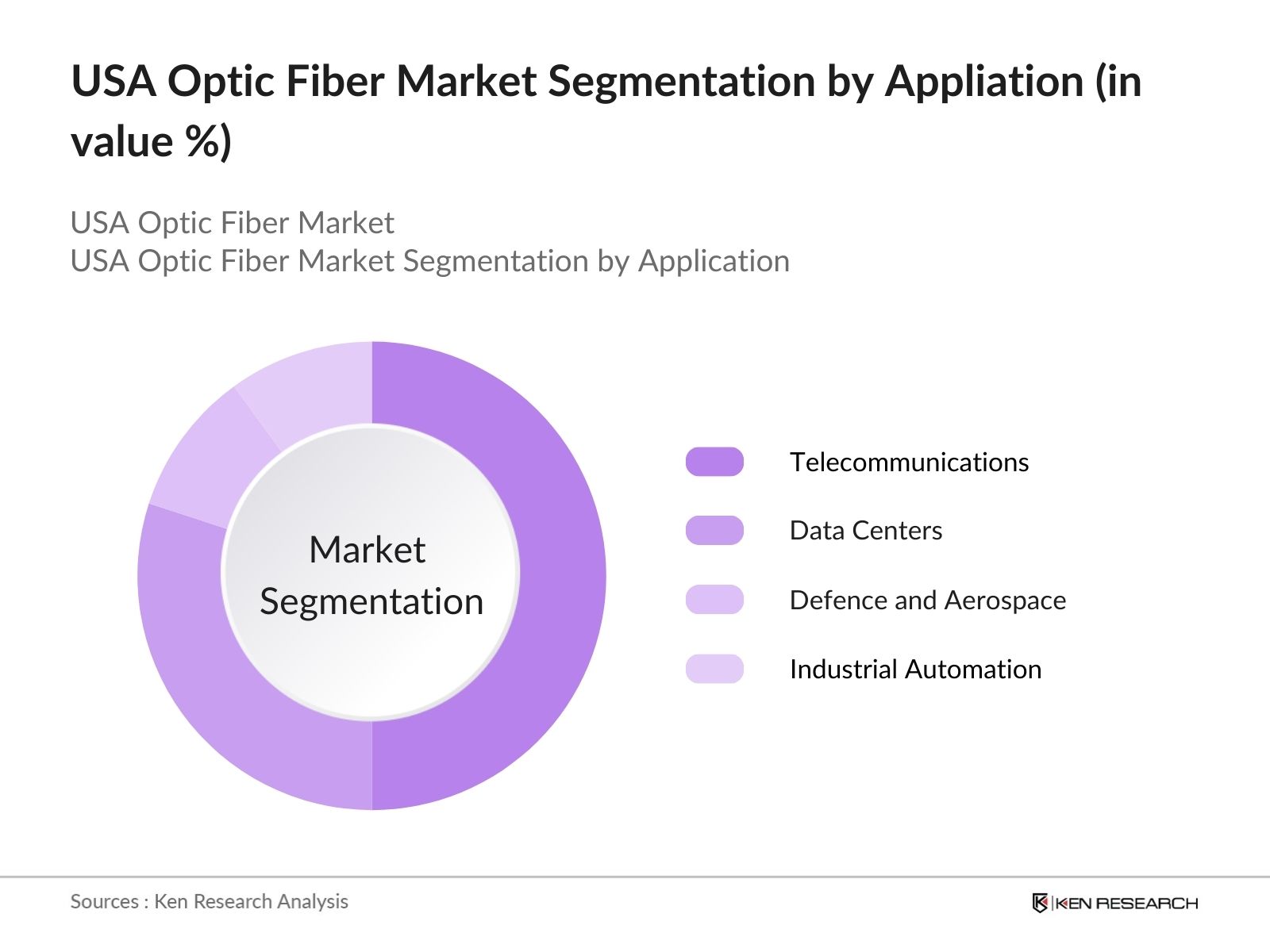

USA Optic Fiber Market Segmentation

- By Fiber Type: The market is segmented by fiber type into single-mode fiber and multi-mode fiber. Single-mode fiber dominates the market due to its extensive use in long-distance telecommunication and high-speed data transmission applications. With its ability to support higher bandwidth over longer distances, it is favored in telecom, data centers, and large-scale enterprise applications. Single-mode fiber is also critical for the deployment of 5G networks, which are being rolled out across urban and rural areas.

- By Application: The market is segmented by application into telecommunications, data centers, defense and aerospace, and industrial automation. Telecommunications is the dominant sub-segment, as it accounts for the largest share of optic fiber deployments across the nation. With the growing demand for high-speed internet services and the expansion of 5G networks, telecom companies are investing heavily in upgrading their fiber infrastructure to meet consumer and business needs.

USA Optic Fiber Market Competitive Landscape

The USA optic fiber market is dominated by several key players, both domestic and international, who lead the market in terms of product offerings, technological innovation, and customer reach. The competitive landscape is characterized by strong partnerships with telecommunications companies and infrastructure development programs driven by government initiatives. The market is led by companies like Corning Inc., Prysmian Group, and CommScope, who have established a strong presence in the USA through their advanced fiber technologies. These companies benefit from significant investments in R&D and long-term contracts with telecom providers.

|

Company |

Establishment Year |

Headquarters |

Fiber Type Offered |

No. of Employees |

Revenue (USD Bn) |

Product Innovations |

R&D Investments |

Strategic Partnerships |

Geographic Reach |

|

Corning Inc. |

1851 |

Corning, NY |

|||||||

|

Prysmian Group |

1879 |

Milan, Italy |

|||||||

|

CommScope |

1976 |

Hickory, NC |

|||||||

|

Sterlite Technologies |

2000 |

Pune, India |

|||||||

|

OFS Fitel, LLC |

2001 |

Norcross, GA |

USA Optic Fiber Market Analysis

Market Growth Drivers

- Rising Demand for High-Speed Data Transmission The USA has witnessed exponential growth in data consumption, driven by both individual consumers and enterprises. In 2024, the total data traffic in the country is estimated to reach around 300 exabytes per month, largely fueled by video streaming, online gaming, and other data-heavy applications. This surging demand for high-speed data transmission has increased the deployment of optic fiber infrastructure, which provides unmatched speed and reliability compared to traditional broadband systems.

- Government Initiatives for 5G Deployment The U.S. government, through initiatives like the Federal Communications Commissions (FCC) efforts, has been actively supporting the rollout of 5G networks. By 2024, the government allocated over $65 billion through programs like the Infrastructure Investment and Jobs Act, which includes funding for broadband and 5G infrastructure expansion. Optic fiber plays a crucial role in 5G deployment as it serves as the backbone for high-speed, low-latency data transmission required for 5G technologies, significantly boosting fiber demand.

- Expansion of Cloud-Based Services The rapid growth of cloud computing services in the U.S. is directly contributing to the increasing adoption of optic fiber. By the end of 2024, major cloud service providers like AWS, Google Cloud, and Microsoft Azure are expanding data centers across the country, with projected investments exceeding $20 billion for infrastructure. These cloud data centers heavily rely on optic fiber for seamless connectivity, low latency, and reliable bandwidth to meet the growing demand for cloud-based services.

Market Challenges

- High Initial Installation Costs The high initial costs associated with optic fiber installation present a significant barrier to market expansion. By 2024, average installation costs per mile of optic fiber ranged from $15,000 to $30,000, depending on the geographic region and complexity of the installation. These costs include expenses for trenching, labor, and the fiber itself, making it challenging for smaller players to enter the market or expand operations.

- Skilled Workforce Shortage The U.S. faces a skilled workforce shortage in the telecom industry, particularly in roles that involve the installation and maintenance of fiber optic networks. By 2024, the U.S. labor market reported a shortage of around 50,000 skilled fiber technicians, which could slow down the pace of fiber deployment projects. This shortage has led to increased labor costs, further elevating the overall cost of installation for telecom companies.

USA Optic Fiber Market Future Outlook

Over the next five years, the USA optic fiber market is expected to experience continuous growth, fueled by government initiatives to improve broadband infrastructure, particularly in underserved rural areas. The expansion of 5G networks and smart city projects will further boost demand for high-quality fiber optic cables. Additionally, advancements in fiber optic technologies, such as bend-insensitive fiber and increased deployment of fiber-to-the-home (FTTH), will contribute to the market's evolution. These factors position the optic fiber market for sustained expansion, driven by both public and private investments.

Market Opportunities

- Increasing Demand from Data Centers Data centers are experiencing growing demand for optic fiber solutions to handle massive data flows. In 2024, U.S.-based data centers accounted for nearly 40% of the world's data processing capacity, requiring an extensive optic fiber network to meet bandwidth and connectivity needs. This presents a lucrative opportunity for optic fiber manufacturers and installers, especially as new data center construction projects are planned across key U.S. regions.

- Integration of Optic Fiber in Smart City Projects Smart city initiatives across U.S. metropolitan areas have integrated optic fiber as the backbone for efficient communication systems, public safety networks, and intelligent traffic management systems. In 2024, cities like New York, Los Angeles, and Chicago have invested over $5 billion collectively in upgrading infrastructure to incorporate smart technologies. The fiber optic networks supporting these smart city projects present long-term growth opportunities for market players involved in optic fiber deployment.

Scope of the Report

|

Fiber Type |

Single-Mode Fiber Multi-Mode Fiber |

|

Cable Type |

Loose Tube Cable Tight-Buffered Cable |

|

Application |

Telecommunications Data Centers Defense and Aerospace Industrial Automation |

|

End-User |

Enterprises Government and Public Sector IT and Telecom Providers, Healthcare |

|

Region |

Northeast USA Midwest USA West USA South USA |

Products

Key Target Audience

Telecommunications Providers (e.g., Verizon, AT&T)

Data Center Operators

Fiber Optic Cable Manufacturers

Government and Regulatory Bodies (e.g., Federal Communications Commission - FCC)

Defense and Aerospace Contractors

Industrial Automation Companies

IT and Telecom Equipment Suppliers

Investors and Venture Capitalist Firms

Companies

Major Players

Corning Inc.

Prysmian Group

CommScope

Sterlite Technologies

OFS Fitel, LLC

General Cable Technologies Corporation

Fujikura Ltd.

Sumitomo Electric Industries

Nexans S.A.

LS Cable & System

Table of Contents

USA Optic Fiber Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

USA Optic Fiber Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

USA Optic Fiber Market Analysis

3.1. Growth Drivers

3.1.1. Rising Demand for High-Speed Data Transmission

3.1.2. Government Initiatives for 5G Deployment

3.1.3. Expansion of Cloud-Based Services

3.1.4. Adoption of Internet of Things (IoT)

3.2. Market Challenges

3.2.1. High Initial Installation Costs

3.2.2. Skilled Workforce Shortage

3.2.3. Complex Installation Processes

3.2.4. Impact of Regulatory Compliance

3.3. Opportunities

3.3.1. Increasing Demand from Data Centers

3.3.2. Integration of Optic Fiber in Smart City Projects

3.3.3. Expansion into Underserved Rural Areas

3.3.4. Collaboration with Telecom Providers for 5G Networks

3.4. Trends

3.4.1. Emergence of Multi-Fiber Technology

3.4.2. Growth of FTTH (Fiber-to-the-Home) Networks

3.4.3. Increased Use of Wavelength Division Multiplexing (WDM)

3.4.4. Advancements in Fiber Optic Sensors

3.5. Government Regulation

3.5.1. Federal Communications Commission (FCC) Policies on Broadband Expansion

3.5.2. Tax Incentives for Infrastructure Development

3.5.3. Cybersecurity Standards for Optic Fiber Networks

3.5.4. Regulatory Support for 5G Rollout

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape

USA Optic Fiber Market Segmentation

4.1. By Fiber Type (In Value %)

4.1.1. Single-Mode Fiber

4.1.2. Multi-Mode Fiber

4.2. By Cable Type (In Value %)

4.2.1. Loose Tube Cable

4.2.2. Tight-Buffered Cable

4.3. By Application (In Value %)

4.3.1. Telecommunications

4.3.2. Data Centers

4.3.3. Defense and Aerospace

4.3.4. Industrial Automation

4.4. By End-User (In Value %)

4.4.1. Enterprises

4.4.2. Government and Public Sector

4.4.3. IT and Telecom Providers

4.4.4. Healthcare

4.5. By Region (In Value %)

4.5.1. Northeast USA

4.5.2. Midwest USA

4.5.3. West USA

4.5.4. South USA

USA Optic Fiber Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Corning Inc.

5.1.2. CommScope

5.1.3. Prysmian Group

5.1.4. OFS Fitel, LLC

5.1.5. Sterlite Technologies Ltd

5.1.6. AFL Global

5.1.7. Yangtze Optical Fibre and Cable Joint Stock Ltd Co (YOFC)

5.1.8. Fujikura Ltd

5.1.9. Sumitomo Electric Industries

5.1.10. General Cable Technologies Corporation

5.1.11. LS Cable & System

5.1.12. Nexans S.A.

5.1.13. ZTT International

5.1.14. Leoni AG

5.1.15. Belden Inc.

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Fiber Type Offering, Customer Base, Geographic Reach, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

USA Optic Fiber Market Regulatory Framework

6.1. Federal Communications Commission (FCC) Regulations

6.2. Compliance Requirements for Broadband and 5G Networks

6.3. Cybersecurity Standards for Fiber Infrastructure

6.4. Certification and Licensing Processes

USA Optic Fiber Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

USA Optic Fiber Future Market Segmentation

8.1. By Fiber Type (In Value %)

8.2. By Cable Type (In Value %)

8.3. By Application (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

USA Optic Fiber Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The research begins with mapping the USA optic fiber ecosystem, identifying all significant stakeholders including fiber optic manufacturers, service providers, and regulatory bodies. The process utilizes secondary research from proprietary databases and government resources to understand key market dynamics such as demand drivers, product innovations, and market constraints.

Step 2: Market Analysis and Construction

This step involves an in-depth analysis of historical market data related to optic fiber deployment, including penetration rates in telecommunications, data centers, and government infrastructure. Market trends are analyzed to assess product performance, network expansion, and investment patterns.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses derived from data analysis are validated through consultations with industry experts. These consultations are conducted via interviews and focus groups with senior executives from optic fiber manufacturing companies, ensuring that data accuracy is maintained throughout the research.

Step 4: Research Synthesis and Final Output

In the final step, detailed reports are generated, which include insights into fiber optic products, competitive analysis, market trends, and consumer preferences. The report also cross-references the bottom-up approach used in data collection to ensure the comprehensiveness of the USA optic fiber market analysis.

Frequently Asked Questions

01. How big is the USA Optic Fiber Market?

The USA optic fiber market is valued at USD 609 Million, driven by increasing demand for high-speed internet and the deployment of 5G networks across the country. Continuous investment in fiber infrastructure has helped the market achieve this size.

02. What are the challenges in the USA Optic Fiber Market?

Challenges in the USA optic fiber market include high installation costs, shortage of skilled workforce, and complex regulatory compliance for network deployment, which can hinder widespread adoption.

03. Who are the major players in the USA Optic Fiber Market?

Key players in the USA optic fiber market include Corning Inc., Prysmian Group, CommScope, Sterlite Technologies, and OFS Fitel, LLC, who dominate the market through technological innovations and strategic partnerships with telecom providers.

04. What are the growth drivers of the USA Optic Fiber Market?

The growth of the USA optic fiber market is driven by the demand for high-speed data transmission, expansion of 5G networks, and the adoption of cloud-based services, along with government initiatives to improve broadband access in rural areas.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.