USA Automatic Weapons Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD8205

November 2024

90

About the Report

USA Automatic Weapons Market Overview

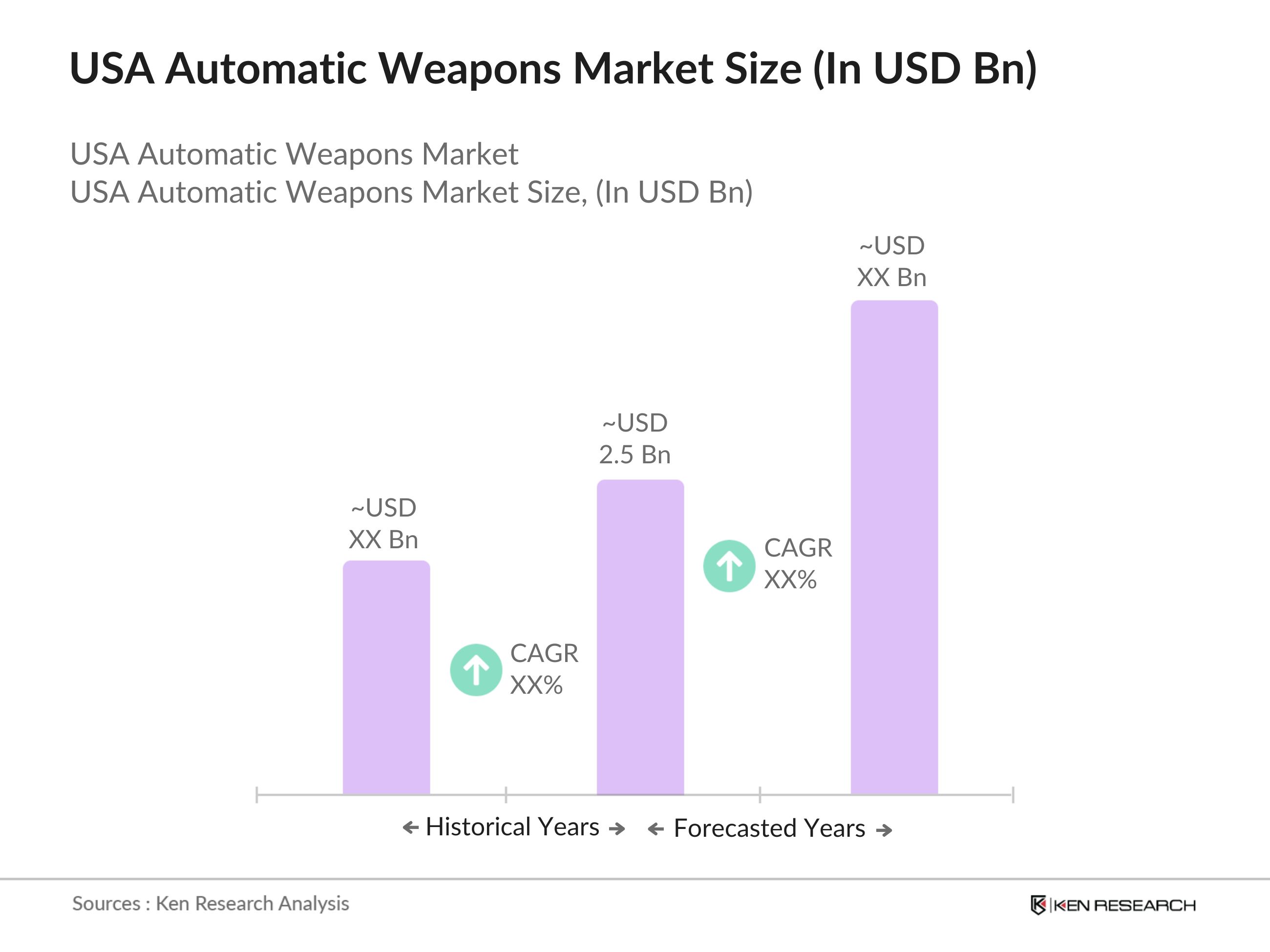

- The USA automatic weapons market is valued at USD 2.5 billion, based on a five-year historical analysis. The market has been driven by increasing defense spending, rising demand for advanced weapons technology, and the need for modernizing military capabilities. The demand for automatic weapons is primarily fueled by the governments focus on enhancing border security and defense readiness in light of global geopolitical tensions. Investments in research and development for next-generation weaponry also play a significant role in driving this market's expansion.

- In the USA, the market for automatic weapons is dominated by cities such as Washington D.C., New York, and Los Angeles, which serve as the central hubs for defense contractors and military procurement. The dominance of these cities is due to the presence of major defense companies, strong government support, and proximity to military bases and government agencies. Additionally, these regions host key defense contractors responsible for fulfilling military contracts for weapon development and supply.

- The Biden-Harris Administrationrecently announceda significantinitiative aimedat reforming theautomatic weaponsmarket in theUnited Statesthrough enhancedregulation andenforcement offirearm sales. On April 11, 2024, the administration unveiled a new Department of Justice final rule that expands firearm background checks as part of implementing theBipartisan Safer Communities Act. This act represents the most substantial expansion of background checks since the Brady Bill was enacted in 1993.

USA Automatic Weapons Market Segmentation

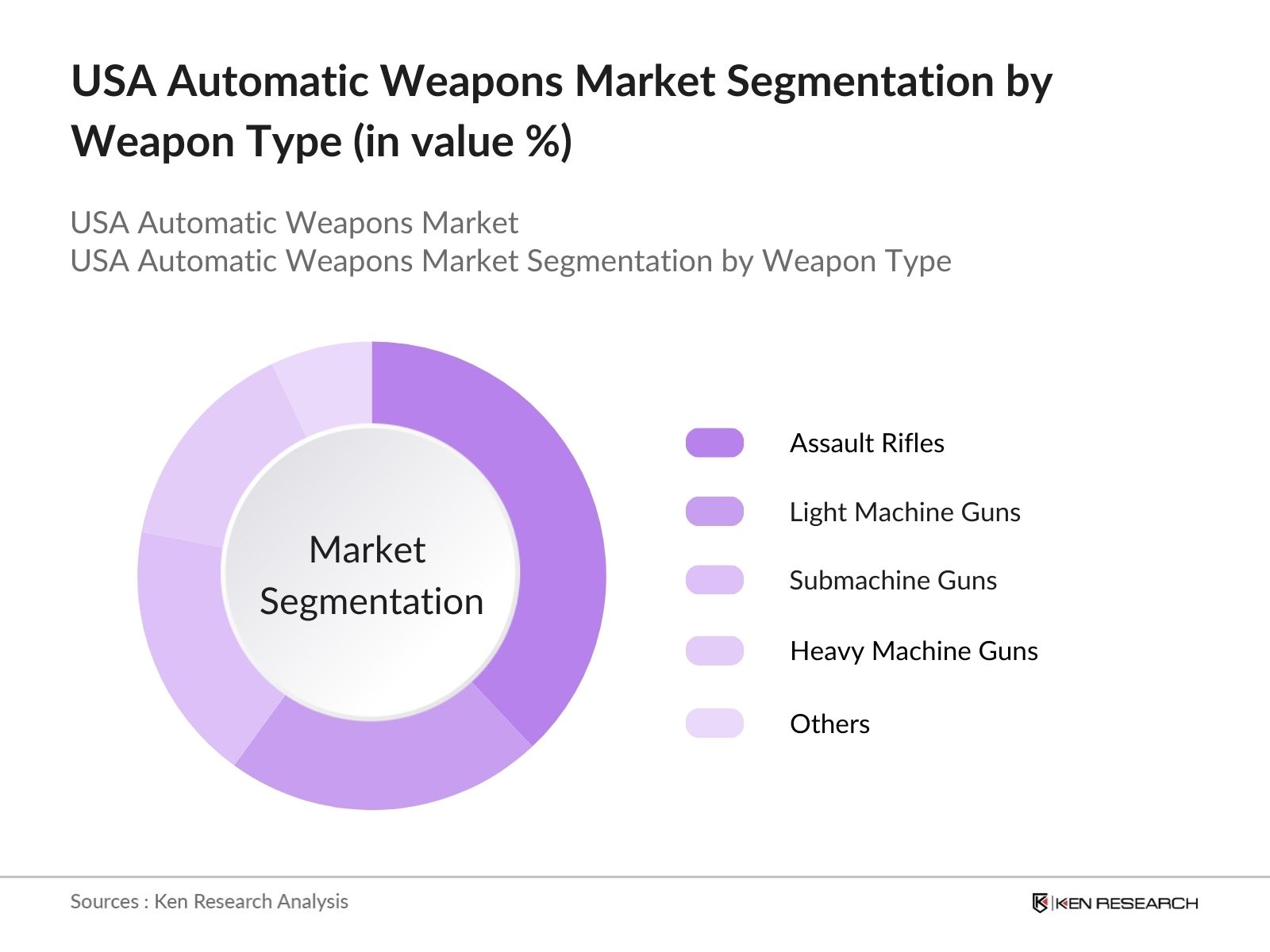

- By Weapon Type: The USA automatic weapons market is segmented by weapon type into light machine guns, heavy machine guns, submachine guns, assault rifles, and others. Recently, assault rifles have captured the dominant market share under this segment due to their widespread use by military personnel and special operations forces. The versatility and efficiency of assault rifles in various combat situations, along with continuous innovation in terms of design and firepower, have made them a preferred choice for defense organizations. Key contracts from the US Department of Defense for modernized assault rifles further drive this segments leadership.

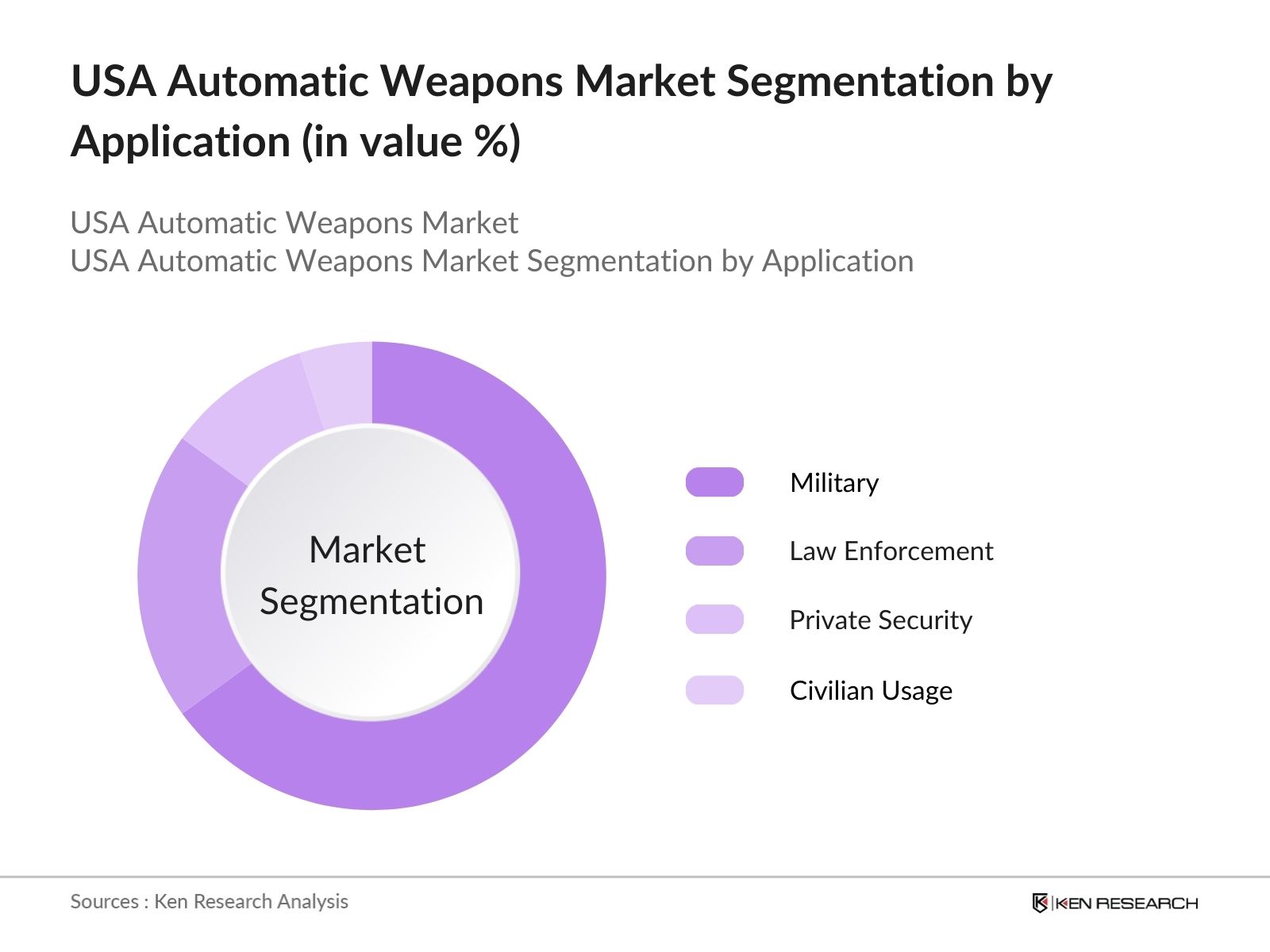

- By Application: The USA automatic weapons market is also segmented by application into military, law enforcement, private security, and civilian usage. The military segment dominates this category, accounting for the largest market share. The strong dominance of the military sector can be attributed to substantial defense budgets and a focus on modernizing military operations. The integration of advanced automatic weapons in training and combat readiness, coupled with ongoing procurement projects by the US Army and Marine Corps, makes this segment the largest revenue generator.

USA Automatic Weapons Market Competitive Landscape

The USA automatic weapons market is highly consolidated, with a few key players dominating the market due to their contracts with government agencies and technological expertise. Major defense contractors such as General Dynamics, Northrop Grumman, and Lockheed Martin have significant influence on the market. The consolidation of these companies highlights their key role in fulfilling defense contracts and supplying cutting-edge weaponry to the US military. These companies also benefit from their ability to integrate new technologies, such as AI, into weapon systems to maintain a competitive edge.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

No. of Employees |

Major Defense Contracts |

Technological Expertise |

Product Range |

Global Presence |

R&D Investments |

|

General Dynamics |

1952 |

Reston, VA |

- | - | - | - | - | - | - |

|

Lockheed Martin |

1995 |

Bethesda, MD |

- | - | - | - | - | - | - |

|

Northrop Grumman |

1939 |

Falls Church, VA |

- | - | - | - | - | - | - |

|

Colts Manufacturing Co. |

1855 |

West Hartford, CT |

- | - | - | - | - | - | - |

|

FN Herstal |

1889 |

Herstal, Belgium |

- | - | - | - | - | - | - |

USA Automatic Weapons Market Analysis

Market Growth Drivers

- Rising Defense Budgets and Military Modernization: The USA's defense budget, which surpassed $800 billion in 2023, is driving demand for advanced automatic weapons. Investments in modernizing military equipment, including automatic rifles and machine guns, are being prioritized to maintain global military dominance.

- Increased Law Enforcement Procurement: Automatic weapons are increasingly procured by law enforcement agencies to address emerging threats such as organized crime and terrorism. Agencies reported a 15% rise in procurement spending from 2022 to 2023, according to Department of Justice statistics.

- Technological Advancements in Weapon Systems: Innovations such as lightweight materials, improved accuracy, and integrated AI for targeting have boosted the appeal of automatic weapons. These advancements are driving adoption in specialized military units and private defense sectors.

Market Challenges

- Stringent Regulatory Frameworks: Federal and state-level restrictions, including the National Firearms Act (NFA) and licensing requirements, create significant hurdles for manufacturers and suppliers in the USA. Compliance costs have risen by 25% for manufacturers in the past two years.

- Public Backlash and Ethical Concerns: Increased public scrutiny and advocacy for stricter gun control laws pose challenges for the market. Rising incidents of gun violence have sparked debates, leading to potential policy shifts that could restrict market growth.

USA Automatic Weapons Market Future Outlook

Over the next five years, the USA automatic weapons market is expected to witness steady growth, driven by advancements in military technologies, increased government defense spending, and the need for enhanced security measures. Key trends such as the integration of artificial intelligence (AI) in weapon systems and the development of lightweight, portable weapon platforms will shape the future of this market. The governments focus on strengthening national defense capabilities and ongoing geopolitical tensions will also contribute to the consistent demand for automatic weapons.

Market Opportunities

- Increased Awareness Among Younger Demographics: Younger consumers in the U.S., particularly those aged 18-34, are showing an increasing interest in dietary supplements like NAC. In 2024, market research data shows that over 5 million younger consumers actively purchased NAC supplements, driven by social media campaigns highlighting its antioxidant and detoxifying benefits. This demographic is expected to be a key driver of market growth, particularly as younger individuals prioritize holistic health and wellness.

- Introduction of NAC in Novel Supplement Formats (Gummies, Liquids): The growing demand for easy-to-consume supplements has led to the development of new NAC formats such as gummies and liquids. In 2024, over 12 million units of gummy supplements were sold in the U.S., according to the U.S. Food and Drug Administrations market data. This trend is expected to grow further as manufacturers capitalize on the demand for innovative supplement forms, particularly in the expanding wellness market.

Scope of the Report

|

By Product Type |

Light Machine Guns Heavy Machine Guns Submachine Guns Assault Rifles Others |

|

By Application |

Military Law Enforcement Civilian (Hunting, Competitive Shooting) Private Security Others |

|

By Technology |

Gas-Operated Recoil-Operated Electrically Driven Advanced Propulsion Systems |

|

By Caliber |

5.56mm 7.62mm 12.7mm Others |

|

By Region |

Northeast Midwest South West |

Products

Key Target Audience

Defense Contractors

US Department of Defense

Law Enforcement Agencies

Private Security Firms

Military Training Institutions

Weapon Manufacturing Companies

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Bureau of Alcohol, Tobacco, Firearms, and Explosives (ATF), US Department of Homeland Security)

Companies

Players Mentioned in the Report:

General Dynamics

Northrop Grumman

Lockheed Martin

Colts Manufacturing Company

FN Herstal

Barrett Firearms Manufacturing

Beretta USA

Sig Sauer, Inc.

Ruger Firearms

Smith & Wesson

Table of Contents

1. USA Automatic Weapons Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Automatic Weapons Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Automatic Weapons Market Analysis

3.1. Growth Drivers (Military Procurement, Defense Budget, Technological Advancements, Border Security)

3.1.1. Increase in Government Defense Expenditure

3.1.2. Focus on Tactical Precision and Firepower

3.1.3. Rising Demand for Counter-Terrorism Operations

3.1.4. Advancements in Weapons Manufacturing Technology

3.2. Market Challenges (Regulatory Hurdles, Production Costs, Export Restrictions, Skilled Labor)

3.2.1. Stringent Export Control Regulations

3.2.2. Rising Manufacturing and R&D Costs

3.2.3. Compliance with International Arms Treaties

3.2.4. Limited Availability of Skilled Workforce

3.3. Opportunities (Expansion in Global Defense Markets, Defense Modernization Programs, Public-Private Partnerships, Customization of Weapon Systems)

3.3.1. Growth in Defense Contracts with NATO Allies

3.3.2. Opportunities in Emerging Defense Markets

3.3.3. Integration with AI and Automation in Weapon Systems

3.3.4. Collaborations with Private Sector in Weapon Development

3.4. Trends (Modular Weapon Systems, Lightweight Materials, Integration with Battlefield Management Systems, Autonomous Weapon Systems)

3.4.1. Adoption of Modular and Configurable Weapon Systems

3.4.2. Rising Popularity of Lightweight and Ergonomic Designs

3.4.3. Integration of Automatic Weapons with AI for Enhanced Battlefield Intelligence

3.4.4. Development of Semi-Autonomous and Autonomous Weapon Platforms

3.5. Government Regulation (Arms Export Control Act, International Traffic in Arms Regulations (ITAR), Firearms Regulation, Military Procurement Policies)

3.5.1. Overview of the USAs International Arms Trade Compliance

3.5.2. National Defense Authorization Act (NDAA) and its Impact

3.5.3. Key Reforms in USA Firearms and Ammunition Regulations

3.5.4. Defense Trade and Security Cooperation Initiatives

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA Automatic Weapons Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Light Machine Guns

4.1.2. Heavy Machine Guns

4.1.3. Submachine Guns

4.1.4. Assault Rifles

4.1.5. Others

4.2. By Application (In Value %)

4.2.1. Military

4.2.2. Law Enforcement

4.2.3. Civilian (Hunting, Competitive Shooting)

4.2.4. Private Security

4.2.5. Others

4.3. By Technology (In Value %)

4.3.1. Gas-Operated

4.3.2. Recoil-Operated

4.3.3. Electrically Driven

4.3.4. Advanced Propulsion Systems

4.4. By Caliber (In Value %)

4.4.1. 5.56mm

4.4.2. 7.62mm

4.4.3. 12.7mm

4.4.4. Others

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Automatic Weapons Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. General Dynamics

5.1.2. Lockheed Martin

5.1.3. Colt's Manufacturing Company

5.1.4. Heckler & Koch GmbH

5.1.5. FN Herstal

5.1.6. Kalashnikov Concern

5.1.7. Beretta Holding

5.1.8. Rheinmetall AG

5.1.9. Northrop Grumman Corporation

5.1.10. Barrett Firearms Manufacturing

5.1.11. Thales Group

5.1.12. Sig Sauer, Inc.

5.1.13. Remington Arms

5.1.14. Bushmaster Firearms International

5.1.15. Daniel Defense

5.2. Cross Comparison Parameters (Revenue, Weapon Types, Global Presence, Defense Contracts, Technological Advancements, R&D Investments, Caliber Range, Market Penetration)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Automatic Weapons Market Regulatory Framework

6.1. Arms Export Control and Compliance Regulations

6.2. Certification and Standardization Processes

6.3. Import/Export Policies and Trade Barriers

6.4. Weapon Testing and Certification Guidelines

7. USA Automatic Weapons Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Automatic Weapons Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Caliber (In Value %)

8.5. By Region (In Value %)

9. USA Automatic Weapons Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Strategic Product Positioning

9.3. Competitive Benchmarking

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Automatic Weapons Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the USA Automatic Weapons Market. This includes assessing market penetration, the ratio of military to private-sector contracts, and the resultant revenue generation. Furthermore, an evaluation of defense-related statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews (CATIs) with industry experts representing defense contractors and law enforcement officials. These consultations provide valuable operational and financial insights, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple weapon manufacturers to acquire detailed insights into product segments, sales performance, government contracts, and technological advancements. This interaction ensures a comprehensive, accurate, and validated analysis of the USA Automatic Weapons Market.

Frequently Asked Questions

1. How big is the USA Automatic Weapons Market?

The USA automatic weapons market is valued at USD 2.5 billion, driven by increasing defense expenditure and a rising focus on modernizing military equipment. The growing adoption of automatic weapons by law enforcement agencies and private security firms also adds to the markets growth.

2. What are the challenges in the USA Automatic Weapons Market?

Challenges in the USA automatic weapons market include stringent export regulations, high production and R&D costs, and increasing scrutiny over arms distribution. Compliance with international arms treaties also poses a challenge for manufacturers looking to expand into global markets.

3. Who are the major players in the USA Automatic Weapons Market?

Key players in the USA automatic weapons market include General Dynamics, Northrop Grumman, Lockheed Martin, Colts Manufacturing Company, and FN Herstal. These companies dominate the market due to their strong government contracts and technological advancements in automatic weapon systems.

4. What are the growth drivers of the USA Automatic Weapons Market?

The USA automatic weapons market is propelled by increased government defense spending, advancements in weapons technology, and the growing need for border security. The rising demand for sophisticated and automated weaponry in military operations is another significant growth driver.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.