USA Carbon Capture, Utilization, and Storage (CCUS) Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD4922

December 2024

90

About the Report

USA Carbon Capture, Utilization, and Storage (CCUS) Market Overview

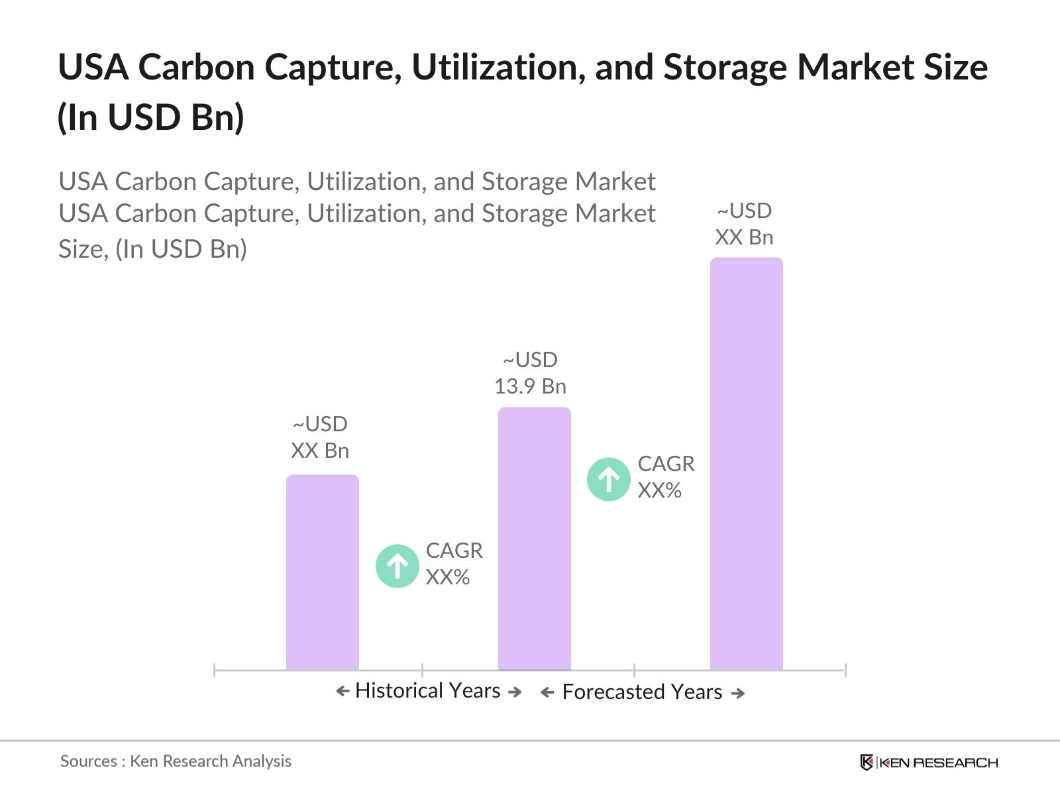

- The USA CCUS Market is valued at USD 13.9 billion, driven by a combination of government initiatives and private sector investments aimed at achieving decarbonization goals. The strong demand for carbon capture technologies stems from the need to reduce industrial CO2 emissions and meet climate targets, which are being reinforced by tax incentives like the 45Q Tax Credit and federal funding programs through the Department of Energy (DOE). These factors have accelerated the adoption of CCUS across power generation and heavy industries, which are significant contributors to carbon emissions.

- Dominant cities and regions within the USA CCUS market include the Gulf Coast (Texas and Louisiana) and the Midwest (Illinois Basin). The Gulf Coast dominates due to its dense industrial clusters and proximity to viable geological storage sites for CO2, which are essential for carbon sequestration. Additionally, Texas's well-established infrastructure for Enhanced Oil Recovery (EOR) has made it a hub for integrating CCUS technologies. The Midwest, with its industrial base and geological features, is also emerging as a key region for CCUS activities.

- In 2022, the 45Q tax credit include significant increases to incentivize carbon capture and storage projects. As part of the 2022 Inflation Reduction Act, credits for carbon capture rose to $85 per ton for geologically sequestered CO2 and $60 per ton for CO2 utilized, including enhanced oil recovery. Direct Air Capture facilities now qualify for up to $180 per ton for sequestration. Additionally, the construction eligibility window was extended to 2033, expanding the scope and long-term support for CCUS initiatives.

USA Carbon Capture, Utilization, and Storage (CCUS) Market Segmentation

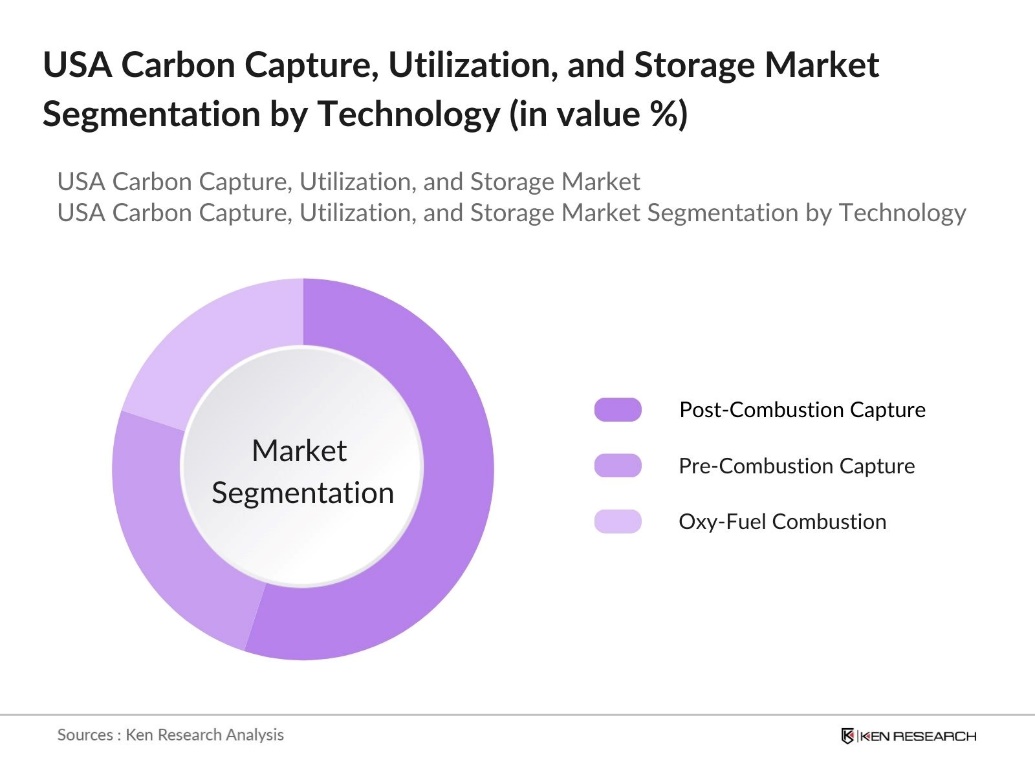

By Technology: The USA CCUS market is segmented by technology into pre-combustion capture, post-combustion capture, and oxy-fuel combustion. Recently, post-combustion capture has held a dominant market share due to its suitability for retrofitting existing power plants and industrial facilities. The ability to install carbon capture units on pre-existing infrastructure without significant modifications gives post-combustion capture a competitive edge. This technology is particularly favored in power generation and industrial processes where minimizing operational disruptions is crucial.

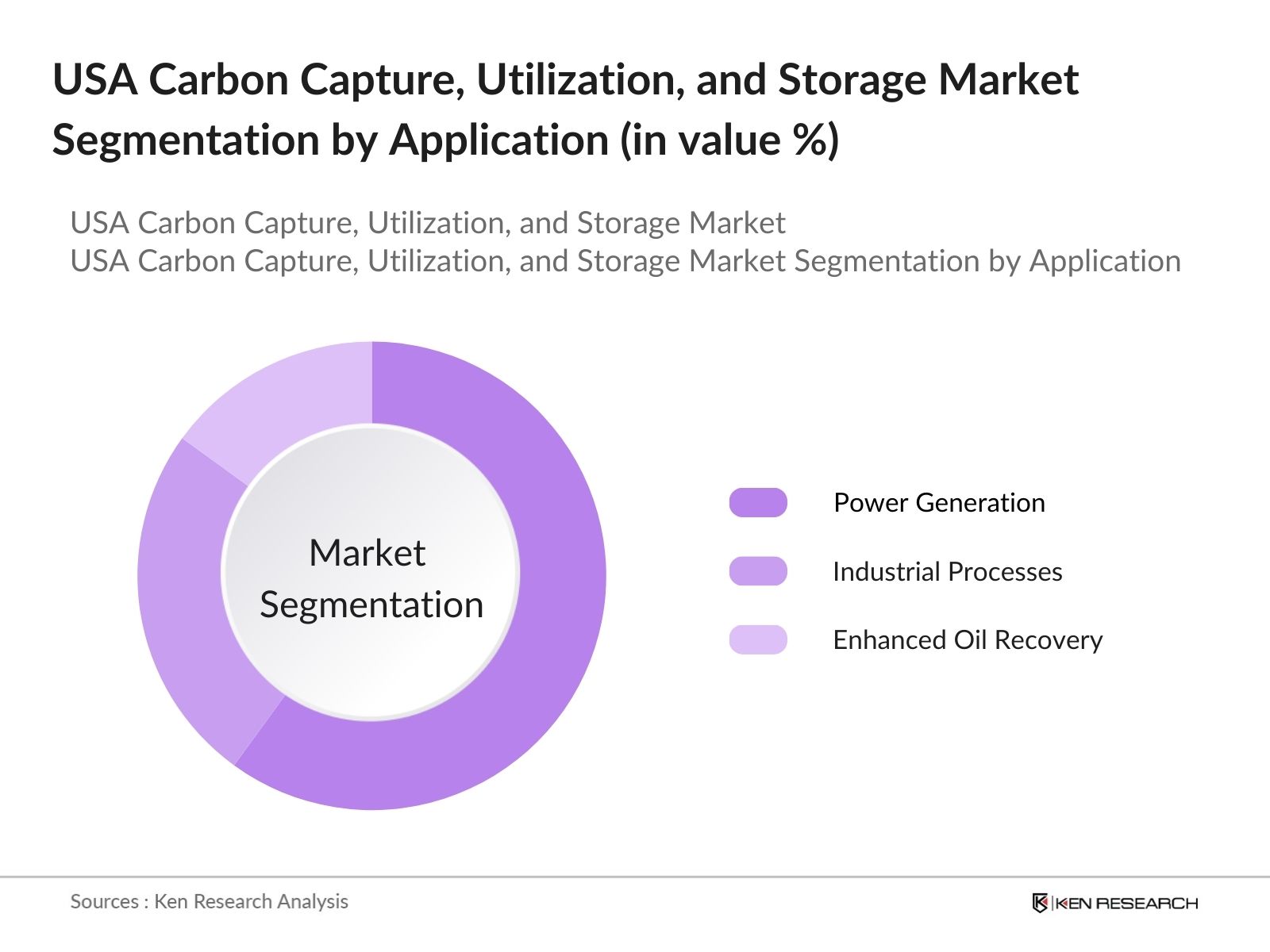

By Application: The CCUS market is segmented by application into power generation, industrial processes, and Enhanced Oil Recovery (EOR). Power generation is the dominant segment, primarily driven by the increasing demand for cleaner energy production. This segment benefits from significant government support and regulatory pressure to decarbonize electricity production. Utilities are rapidly adopting CCUS technologies to reduce their carbon footprint while maintaining energy output, making power generation the key application driving CCUS market adoption.

USA Carbon Capture, Utilization, and Storage (CCUS) Market Competitive Landscape

The market is dominated by a few key players, including both energy giants and innovative startups. Companies like ExxonMobil and Chevron are leveraging their extensive experience in the oil and gas industry to integrate CCUS into their operations, particularly in the context of Enhanced Oil Recovery (EOR). These firms, along with innovators such as Carbon Clean and Global Thermostat, are at the forefront of technological advancements in carbon capture and storage.

|

Company Name |

Establishment Year |

Headquarters |

CO2 Sequestration Capacity |

Key Projects |

Geographical Reach |

CCUS Investment |

CO2 Utilization |

R&D Focus |

|

ExxonMobil |

1870 |

Texas, USA |

||||||

|

Chevron |

1879 |

California, USA |

||||||

|

Carbon Clean |

2009 |

London, UK |

||||||

|

Global Thermostat |

2010 |

New York, USA |

||||||

|

Occidental Petroleum |

1920 |

Texas, USA |

USA Carbon Capture, Utilization, and Storage (CCUS) Industry Analysis

Growth Drivers

- Energy Transition and Net-Zero Targets: The push for net-zero emissions by 2050 is accelerating CCUS adoption in the USA. The Bipartisan Infrastructure Law (BIL), signed in November 2021, allocates over $1 trillion in public investment, with a significant portion directed towards carbon capture and storage initiatives, supporting large-scale deployment of CCUS technologies across various industries to reduce carbon emissions.

- Industrial Decarbonization Initiatives: Industrial sectors like cement, steel, and chemicals contribute to the U.S. emissions. CCUS is a central component in their decarbonization strategy. For instance, in the cement industry alone, the deployment of CCUS could reduce emissions by 400,000 metric tons annually by 2025. The Concrete Zero initiative, are coordinating a business commitment to use 100% net-zero concrete by 2050.

- Advances in Carbon Utilization Technologies: Advances in carbon utilization technologies are transforming captured CO2 into valuable products like synthetic fuels and building materials. These innovations offer new opportunities for industries to convert emissions into useful resources, driving growth in sectors such as construction and energy. Government-supported programs are actively investing in projects that aim to enhance the conversion of CO2 into concrete, chemicals, and other materials, further encouraging the adoption of these advanced technologies.

Market Challenges

- High Costs of Infrastructure and Storage: Implementing CCUS technologies involves significant financial challenges, particularly in the development of infrastructure. The construction of pipelines and storage facilities for large-scale CO2 sequestration requires substantial investment, which can create financial strain for industries looking to adopt CCUS. These high costs are a major barrier to widespread implementation, making it difficult for companies to justify the expense without sufficient financial support or incentives.

- Uncertainty in Policy Support: Despite federal initiatives like the 45Q tax credit and funding programs, there remains uncertainty around long-term policy support for CCUS. Shifts in political priorities or leadership can affect the consistency of incentives and funding, which creates hesitation for industries considering CCUS adoption. Additionally, many states lack clear policy frameworks to support the development of CCUS infrastructure, leading to concerns about future regulatory stability.

USA Carbon Capture, Utilization, and Storage (CCUS) Market Future Outlook

The USA CCUS market is expected to witness substantial growth over the next five years, driven by continuous government support, advancements in carbon capture technologies, and increasing private sector investments. The implementation of federal policies such as the 45Q Tax Credit and various DOE funding initiatives is expected to further accelerate the development of new CCUS projects. Additionally, emerging innovations in CO2 utilization and the scaling up of Direct Air Capture (DAC) technology will play a critical role in driving the future market trajectory.

Market Opportunities

- Technological Innovations in CO2 Utilization: Advancements in CO2 utilization technologies are creating new opportunities for growth by transforming captured carbon into valuable products such as concrete, biofuels, and polymers. These innovations turn CO2 from a waste product into a resource, offering industries the potential for new revenue streams. Continued research and development in this area is driving further advancements, enabling broader adoption of these technologies across various sectors.

- Public-Private Partnerships: Public-private partnerships are playing a crucial role in expanding CCUS projects. Collaborations between the government and major corporations are driving the development of large-scale carbon capture initiatives. These partnerships combine private sector innovation and resources with government support, accelerating the implementation of CCUS facilities and contributing to the broader adoption of carbon capture technologies across industries.

Scope of the Report

|

Technology |

Pre-Combustion Capture Post-Combustion Capture Oxy-Fuel Combustion |

|

Application |

Power Generation Industrial Processes Enhanced Oil Recovery (EOR) |

|

End-Use Industry |

Energy Sector Heavy Industries Waste Management |

|

CO2 Utilization Method |

Chemical Conversion Building Materials Production Algae Biofixation |

|

Region |

Gulf Coast (Texas, Louisiana) Midwest (Illinois Basin) Western USA (California) |

Products

Key Target Audience

Energy Companies

Heavy Industries

Enhanced Oil Recovery (EOR) Companies

Heavy Industries

Carbon Offsetting Companies

Government and Regulatory Bodies (e.g., Environmental Protection Agency, Department of Energy)

Investors and VC Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

ExxonMobil

Chevron

Occidental Petroleum

Carbon Clean

Global Thermostat

Air Liquide

Shell

BP

Linde

Aker Solutions

Schlumberger

Climeworks

Carbon Engineering

NET Power

TotalEnergies

Table of Contents

1. USA CCUS Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. USA CCUS Market Size (In USD Billion)

2.1 Historical Market Size (Cost of CO2 Sequestration, CCUS Project Investment)

2.2 Year-On-Year Growth Analysis (CO2 Captured Volume, Utilization and Storage Capacity)

2.3 Key Market Developments and Milestones (Number of Operational Facilities, Pipeline Projects)

3. USA CCUS Market Analysis

3.1 Growth Drivers

3.1.1 Energy Transition and Net-Zero Targets

3.1.2 Government Incentives (Tax Credits, Funding Programs)

3.1.3 Industrial Decarbonization Initiatives

3.1.4 Advances in Carbon Utilization Technologies

3.2 Market Challenges

3.2.1 High Costs of Infrastructure and Storage

3.2.2 Uncertainty in Policy Support

3.2.3 Limited Pipeline and Storage Capacity

3.3 Opportunities

3.3.1 Technological Innovations in CO2 Utilization

3.3.2 Public-Private Partnerships

3.3.3 Cross-Sector Collaboration (Energy, Cement, Chemical Industries)

3.4 Trends

3.4.1 Rise in Blue Hydrogen Production (with CCUS)

3.4.2 Use of CCUS in Industrial Clusters

3.4.3 Adoption of Direct Air Capture (DAC) Technologies

3.5 Government Regulations

3.5.1 45Q Tax Credit Implementation

3.5.2 Environmental Protection Agency (EPA) Guidelines on CO2 Sequestration

3.5.3 State-Level CCUS Policies (California, Texas)

3.5.4 Federal Funding Programs for CCUS Projects (DOE, ARPA-E)

3.6. SWOT Analysis

3.7. Stake Ecosystem Analysis (OEMs, Suppliers, Regulatory Bodies)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA CCUS Market Segmentation

4.1 By Technology (In Value %)

4.1.1 Pre-Combustion Capture

4.1.2 Post-Combustion Capture

4.1.3 Oxy-Fuel Combustion

4.2 By Application (In Value %)

4.2.1 Power Generation

4.2.2 Industrial Processes (Steel, Cement, Chemicals)

4.2.3 Enhanced Oil Recovery (EOR)

4.3 By End-Use Industry (In Value %)

4.3.1 Energy Sector

4.3.2 Heavy Industries

4.3.3 Waste Management

4.4 By CO2 Utilization Method (In Value %)

4.4.1 Chemical Conversion

4.4.2 Building Materials Production

4.4.3 Algae Biofixation

4.5 By Region (In Value %)

4.5.1 Gulf Coast (Texas, Louisiana)

4.5.2 Midwest (Illinois Basin)

4.5.3 Western USA (California)

5. USA CCUS Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 ExxonMobil

5.1.2 Chevron

5.1.3 Shell

5.1.4 Occidental Petroleum

5.1.5 BP

5.1.6 Air Liquide

5.1.7 Linde

5.1.8 Aker Solutions

5.1.9 Schlumberger

5.1.10 Carbon Clean

5.1.11 Global Thermostat

5.1.12 Climeworks

5.1.13 Carbon Engineering

5.1.14 NET Power

5.1.15 TotalEnergies

5.2 Cross Comparison Parameters (Revenue, No. of Employees, Key Projects, CO2 Sequestration Capacity, Headquarters, Inception Year, CCUS R&D Investment, Geographical Footprint)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Joint Ventures, Technology Collaboration, New Project Launches)

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Grants and Subsidies

5.8 Venture Capital Funding

5.9 Private Equity Investments

6. USA CCUS Market Regulatory Framework

6.1 Federal Regulations (EPA, DOE, BLM)

6.2 State-Level Regulations (California, Texas)

6.3 Compliance Requirements for CO2 Storage

6.4 Certification Processes (Class VI Permits, Geologic Storage Approvals)

7. USA CCUS Future Market Size (In USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (Increasing Regulatory Stringency, Decarbonization Goals)

8. USA CCUS Future Market Segmentation

8.1 By Technology (In Value %)

8.2 By Application (In Value %)

8.3 By End-Use Industry (In Value %)

8.4 By CO2 Utilization Method (In Value %)

8.5 By Region (In Value %)

9. USA CCUS Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Strategic Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research began with identifying key variables impacting the USA CCUS market, such as technological advancements, policy incentives, and industrial decarbonization targets. This phase involved extensive desk research, relying on proprietary databases and government resources to define the critical drivers and barriers.

Step 2: Market Analysis and Construction

Next, historical data was analyzed to assess the development of the CCUS market in terms of technology adoption, number of operational projects, and CO2 storage capacity. This analysis was crucial for projecting the future market trajectory and identifying key opportunities in the value chain.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from key CCUS firms were consulted to validate market hypotheses. Through interviews and discussions, insights were gained regarding operational challenges, technology trends, and future market expectations, ensuring that the research was grounded in practical market realities.

Step 4: Research Synthesis and Final Output

In the final phase, data from both primary and secondary research were synthesized to produce a comprehensive analysis of the CCUS market. Key insights were drawn to inform strategic recommendations for market stakeholders, ensuring a reliable and validated market report.

Frequently Asked Questions

01. How big is the USA CCUS Market?

The USA CCUS Market, valued at USD 13.9 billion, is driven by increased demand for carbon capture technologies and government incentives aimed at reducing industrial CO2 emissions.

02. What are the challenges in the USA CCUS Market?

Key challenges in USA CCUS Market include the high costs associated with CCUS infrastructure development, regulatory uncertainties, and the limited availability of pipelines and storage sites for CO2.

03. Who are the major players in the USA CCUS Market?

Major players in USA CCUS Market include ExxonMobil, Chevron, Carbon Clean, Global Thermostat, and Occidental Petroleum, each contributing significantly to the adoption and innovation of CCUS technologies.

04. What are the growth drivers of the USA CCUS Market?

The USA CCUS Market growth is driven by government support through tax credits (e.g., 45Q Tax Credit), private sector investment, and the urgent need to meet decarbonization targets across industries.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.