USA Cell Culture Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD3568

October 2024

95

About the Report

USA Cell Culture Market Overview

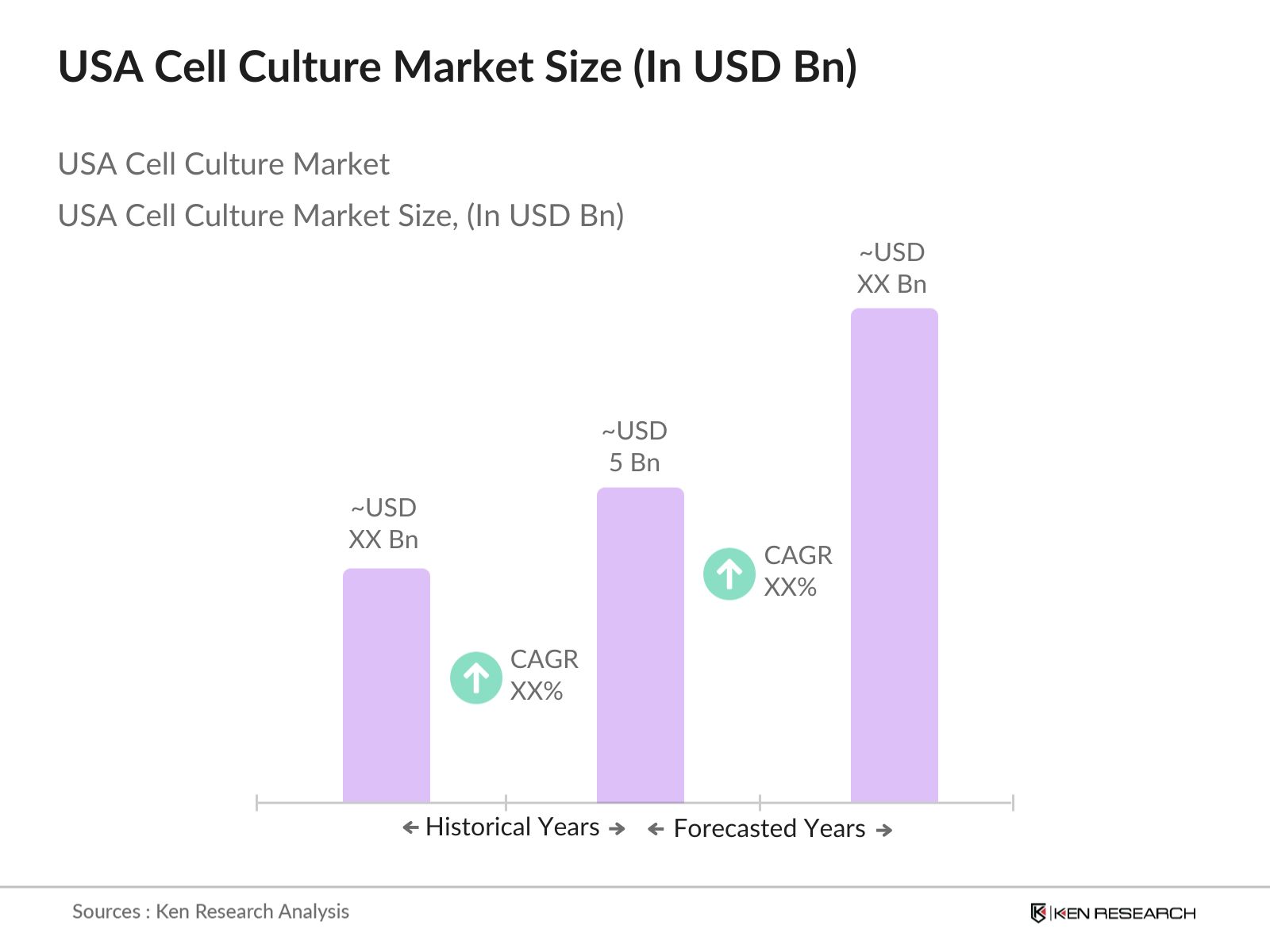

- The USA cell culture market was valued at USD 5 billion based on a five-year historical analysis., driven by robust demand in biopharmaceutical production and continuous innovation in biotechnology. The market has been catalyzed by an increase in biologics and biosimilars production, as well as significant investments in regenerative medicine and stem cell research. The rising adoption of single-use technologies and automation for cell culture production has further enhanced market growth. The expansion in healthcare infrastructure, coupled with strong R&D initiatives from government and private organizations, also contributes to this growth.

- The USA dominates the global cell culture market due to its highly advanced research infrastructure, presence of leading pharmaceutical and biotechnology companies, and a strong network of research institutes. Cities like Boston, San Francisco, and San Diego are leading hubs for biotech and life sciences, with a concentration of laboratories, research facilities, and a skilled workforce. This dominance is primarily driven by the availability of high funding for research, early adoption of new technologies, and collaborations with universities and private players.

- The FDA maintains rigorous guidelines for cell-based products, including requirements for clinical trials and product safety. These guidelines ensure that only products meeting high standards of quality and safety reach the market, although they do extend the time required for product development and approval.

USA Cell Culture Market Segmentation

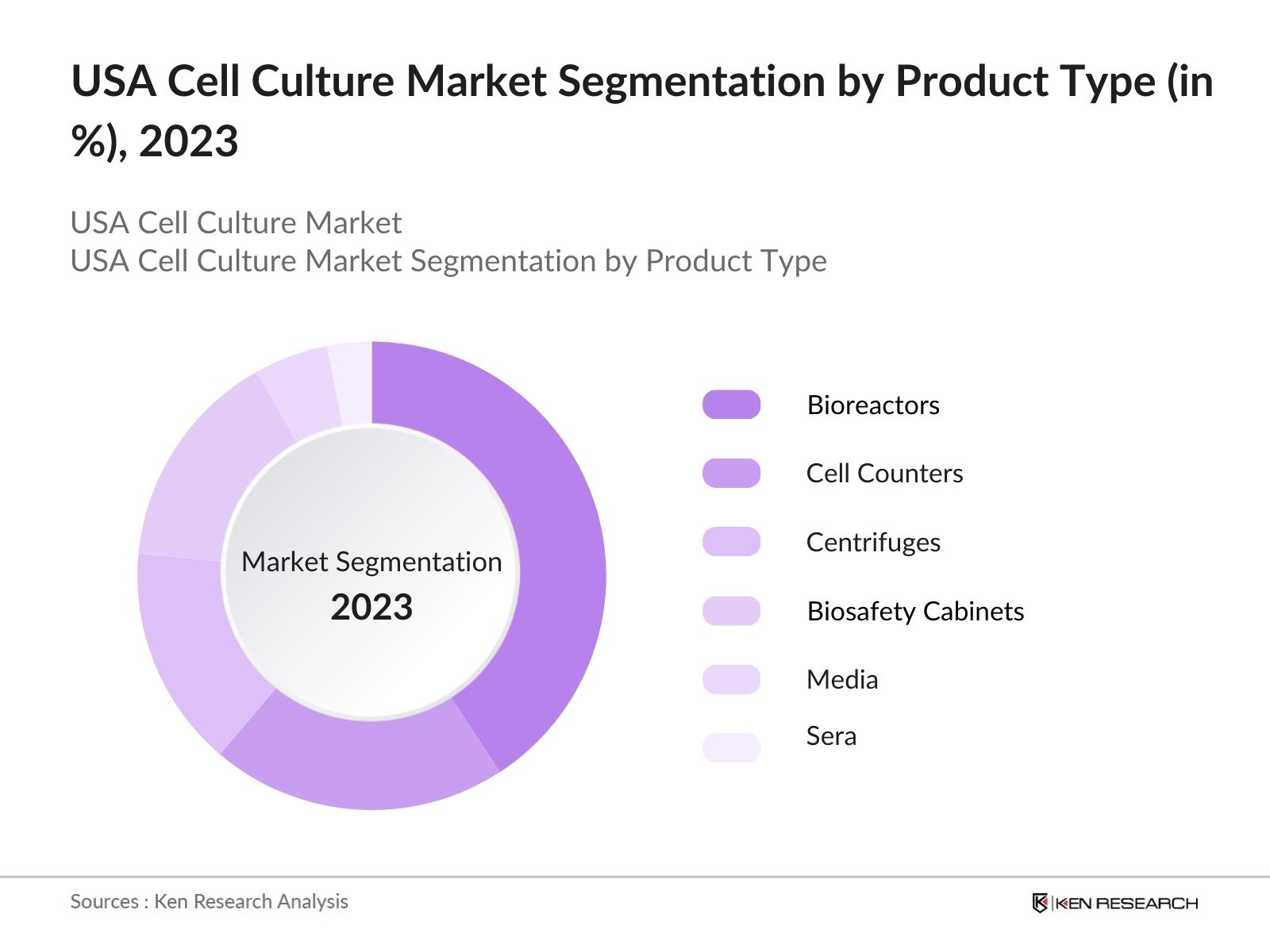

By Product Type: The USA cell culture market is segmented by product type into cell culture equipment and cell culture consumables. Cell culture equipment includes bioreactors, cell counters, centrifuges, and biosafety cabinets, while consumables consist of media, sera, and reagents. Cell culture equipment has been a dominant segment due to the increasing adoption of advanced bioreactors and automation technologies that improve productivity and efficiency in large-scale biopharmaceutical production.

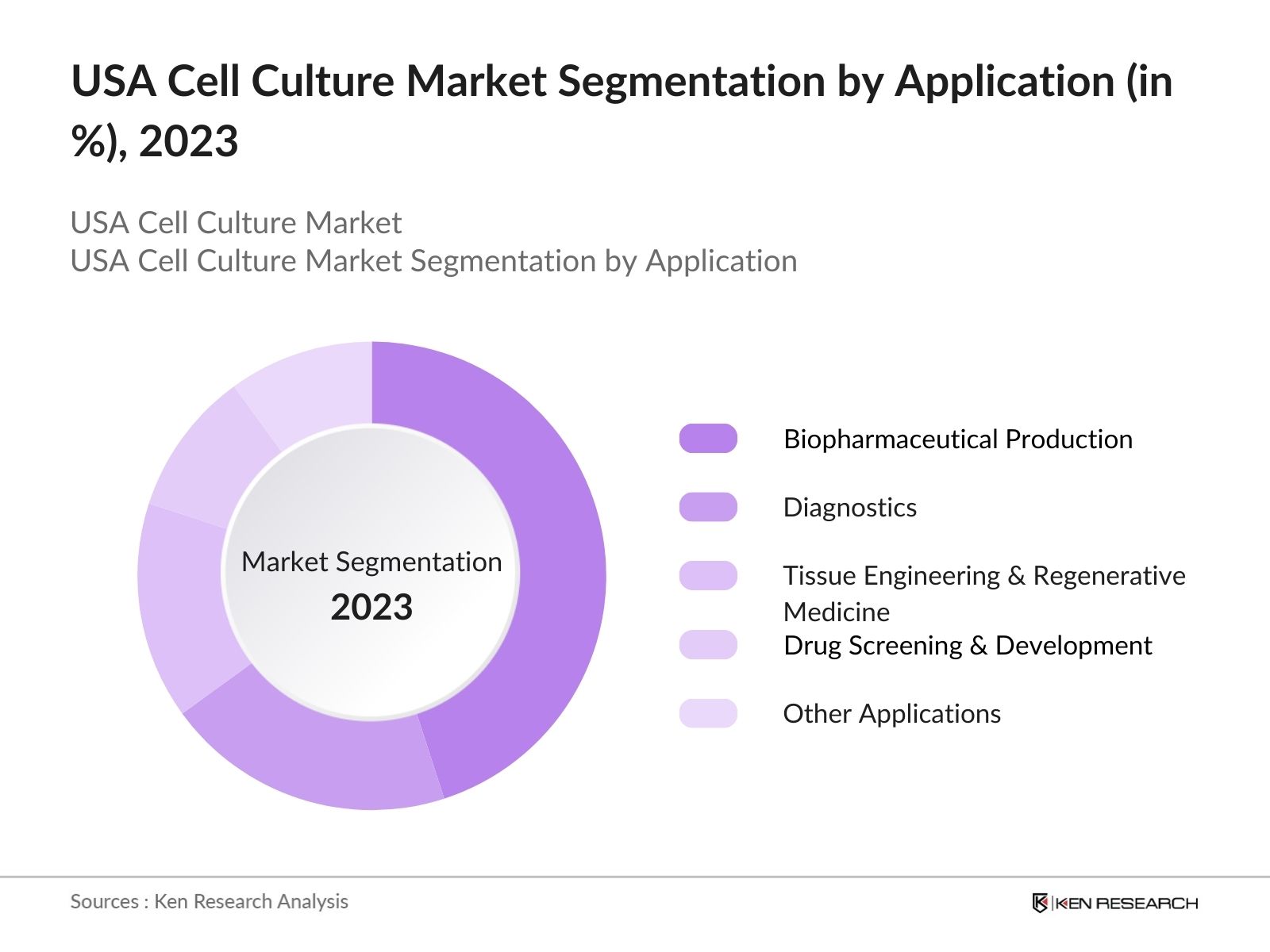

By Application: The USA cell culture market is segmented by application into biopharmaceutical production, diagnostics, tissue engineering and regenerative medicine, drug screening and development, and other applications. Biopharmaceutical production leads this segment, driven by the increased focus on monoclonal antibody production, vaccine development, and gene therapy applications. The expansion of biologics and biosimilars manufacturing facilities, coupled with high demand for personalized medicine, underpins the dominance of biopharmaceutical applications.

USA Cell Culture Market Competitive Landscape

The USA cell culture market is characterized by the presence of established players and frequent mergers and acquisitions aimed at expanding product portfolios and technological capabilities. Major players include Thermo Fisher Scientific, Danaher Corporation, Merck KGaA, Lonza Group, and Becton, Dickinson and Company. These companies dominate due to their comprehensive product offerings, strong market presence, and continuous focus on R&D and innovation.

USA Cell Culture Industry Analysis

Growth Drivers

- Increasing Demand for Biopharmaceuticals and Biosimilars: The demand for biopharmaceuticals and biosimilars in the USA has been steadily growing due to advancements in healthcare and an aging population. As of 2024, the United States spends over $4 trillion on healthcare annually, with biopharmaceuticals accounting for a significant portion. The markets expansion is driven by the increasing prevalence of chronic diseases, such as cancer and diabetes, which have risen to impact over 60 million people.

- Adoption of Single-Use Technologies: The adoption of single-use technologies (SUT) in cell culture processes has significantly accelerated the efficiency of manufacturing biopharmaceuticals. This technology minimizes contamination risk and improves operational efficiency, supporting rapid scale-up and cost management. The U.S. biopharmaceutical sector's capital investment in these technologies has increased by over $500 million in recent years, highlighting the growing preference for single-use systems in research and production.

- Technological Advancements in Cell Culture Systems: The integration of automated systems and AI in cell culture processes has resulted in significant efficiency gains. As a result, the U.S. pharmaceutical industrys labor productivity has seen an improvement of nearly 3% per year over the past five years. These advancements reduce manual intervention, lowering the risk of human error and improving the reproducibility of results.

Market Challenges

- High Cost of Cell Biology Research: The cost of cell biology research is a significant barrier to market expansion. The average cost for R&D in cell culture and related technologies is estimated to be between $1 million and $2 million per study. These high expenses are often a limiting factor for smaller research institutions and startups.

- Limitations in Producing High-Density Cell Cultures: Producing high-density cell cultures remains a challenge due to issues with nutrient availability, oxygen supply, and waste product removal. These constraints limit the scalability and cost-effectiveness of manufacturing processes. Addressing these limitations requires ongoing research and development efforts, which are capital-intensive.

USA Cell Culture Market Future Outlook

Over the next five years, the USA cell culture market is expected to experience significant growth driven by ongoing investments in biopharmaceutical production, advancements in stem cell research, and increasing adoption of 3D cell culture technologies. The market will benefit from the growing focus on precision medicine and the development of innovative therapeutic products such as CAR-T therapies and gene therapies. Additionally, the market is expected to see a rise in demand for automated and single-use technologies that support efficient and scalable cell culture processes.

Market Opportunities

- Expansion in Regenerative Medicine and Cell-Based Therapies: Regenerative medicine, including stem cell therapy, represents a significant growth opportunity. The U.S. governments investment in regenerative medicine research exceeds $1 billion annually, supporting the development of novel treatments for conditions like spinal cord injuries and organ damage.

- Shift Towards 3D Cell Culture Technologies: The market is seeing a shift from traditional 2D to 3D cell culture technologies, which more accurately mimic in vivo conditions. This shift has driven research in oncology and regenerative medicine, with over 50% of ongoing clinical trials now involving 3D culture models.

Scope of the Report

|

By Product Type |

Cell Culture Equipment Cell Culture Consumables Bioreactors Cell Counters Centrifuges Media Sera Reagents |

|

By Application |

Biopharmaceutical Production Diagnostics Tissue Engineering and Regenerative Medicine Drug Screening and Development Other Applications |

|

By End User |

Pharmaceutical and Biotechnology Companies Research and Academic Institutes Hospitals and Diagnostic Laboratories Other End Users |

|

By Region |

North America Europe Asia Pacific Latin America Middle East and Africa |

Products

Key Target Audience

Pharmaceutical and Biotechnology Companies

Biopharmaceutical Manufacturers

Research and Academic Institutes

Contract Manufacturing Organizations (CMOs)

Contract Research Organizations (CROs)

Government and Regulatory Bodies (e.g., FDA, NIH)

Investments and Venture Capitalist Firms

Healthcare Providers and Diagnostics Centers

Companies

Players Mentioned in the Report

Thermo Fisher Scientific

Danaher Corporation

Merck KGaA

Lonza Group AG

Becton, Dickinson and Company

Corning Incorporated

Sartorius AG

FUJIFILM Irvine Scientific

HiMedia Laboratories

Eppendorf AG

Table of Contents

1. USA Cell Culture Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. USA Cell Culture Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. USA Cell Culture Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Demand for Biopharmaceuticals and Biosimilars

3.1.2 Adoption of Single-Use Technologies

3.1.3 Government and Private Funding in Cell-Based Research

3.1.4 Technological Advancements in Cell Culture Systems

3.1.5 Rising Prevalence of Chronic Diseases

3.2 Market Challenges

3.2.1 High Cost of Cell Biology Research

3.2.2 Limitations in Producing High-Density Cell Cultures

3.2.3 Stringent Regulatory Frameworks

3.3 Opportunities

3.3.1 Expansion in Regenerative Medicine and Cell-Based Therapies

3.3.2 Increasing Investments in R&D Activities

3.3.3 Advancements in Stem Cell Research

3.4 Trends

3.4.1 Integration of AI and Automation in Cell Culture

3.4.2 Shift Towards 3D Cell Culture Technologies

3.4.3 Use of Microfluidic Systems and Lab-on-a-Chip Models

3.5 Government Regulation

3.5.1 FDA Regulatory Guidelines for Cell-Based Products

3.5.2 Compliance with cGMP Standards

3.5.3 National Institutes of Health (NIH) Funding Policies

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

4. USA Cell Culture Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Cell Culture Equipment

Bioreactors

Cell Counters

Centrifuges

Biosafety Cabinets

Microscopes

4.1.2 Cell Culture Consumables

Media

Sera

Reagents

4.2 By Application (In Value %)

4.2.1 Biopharmaceutical Production

Monoclonal Antibody Production

Vaccine Production

4.2.2 Diagnostics

4.2.3 Tissue Engineering and Regenerative Medicine

4.2.4 Drug Screening and Development

4.2.5 Other Applications

4.3 By End User (In Value %)

4.3.1 Pharmaceutical and Biotechnology Companies

4.3.2 Research and Academic Institutes

4.3.3 Hospitals and Diagnostic Laboratories

4.3.4 Other End Users

4.4 By Region (In Value %)

4.4.1 North America (USA and Canada)

4.4.2 Europe

4.4.3 Asia Pacific

4.4.4 Latin America

4.4.5 Middle East and Africa

5. USA Cell Culture Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Thermo Fisher Scientific

5.1.2 Danaher Corporation

5.1.3 Merck KGaA

5.1.4 Becton, Dickinson and Company

5.1.5 Lonza Group AG

5.1.6 Sartorius AG

5.1.7 Corning Incorporated

5.1.8 Eppendorf AG

5.1.9 HiMedia Laboratories

5.1.10 FUJIFILM Irvine Scientific

5.1.11 GE Healthcare

5.1.12 PromoCell GmbH

5.1.13 Bio-Rad Laboratories, Inc.

5.1.14 Agilent Technologies, Inc.

5.1.15 Miltenyi Biotec

5.2 Cross Comparison Parameters

Revenue

Market Share

Product Portfolio

Strategic Initiatives

Mergers & Acquisitions

Collaborations and Partnerships

Recent Product Launches

Innovation Focus

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. USA Cell Culture Market Regulatory Framework

6.1 FDA Guidelines for Cell-Based Products

6.2 cGMP Compliance Requirements

6.3 Patent Analysis

6.4 Intellectual Property Trends

7. USA Cell Culture Market Future Projections

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. USA Cell Culture Market Segmentation - Future Outlook

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By End User (In Value %)

8.4 By Region (In Value %)

9. USA Cell Culture Market Analyst Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first step involves constructing an ecosystem map that covers all major stakeholders within the USA Cell Culture Market. This step includes extensive desk research, leveraging secondary and proprietary databases to gather comprehensive industry-level information. The aim is to identify critical variables influencing the market, such as regulatory policies, technological trends, and market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data regarding market penetration, service provider ratios, and revenue generation are compiled and analyzed. The data is verified for accuracy through comparison with multiple data sources. Service quality statistics and market developments are also assessed to ensure reliable revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through structured interviews with industry experts representing a diverse array of companies. These consultations provide operational and financial insights directly from industry practitioners, which are instrumental in refining and validating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple stakeholders to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This ensures a comprehensive, accurate, and validated analysis of the USA cell culture market.

Frequently Asked Questions

01. How big is the USA Cell Culture Market?

The USA cell culture market was valued at USD 5 billion based on a five-year historical analysis., driven by robust demand in biopharmaceutical production and continuous innovation in biotechnology.

02. What are the challenges in the USA Cell Culture Market?

The USA cell culture market challenges include high costs associated with cell biology research, stringent regulatory requirements, and limitations in producing high-density cell cultures.

03. Who are the major players in the USA Cell Culture Market?

Key players in the USA cell culture market include Thermo Fisher Scientific, Danaher Corporation, Merck KGaA, Lonza Group, and Becton, Dickinson and Company. These companies dominate due to their extensive product offerings and strong market presence.

04. What are the growth drivers of the USA Cell Culture Market?

The USA cell culture market is propelled by the increasing adoption of single-use technologies, advancements in regenerative medicine, and growing biopharmaceutical production.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.