USA Polyethylene Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD4027

December 2024

90

About the Report

USA Polyethylene Market Overview

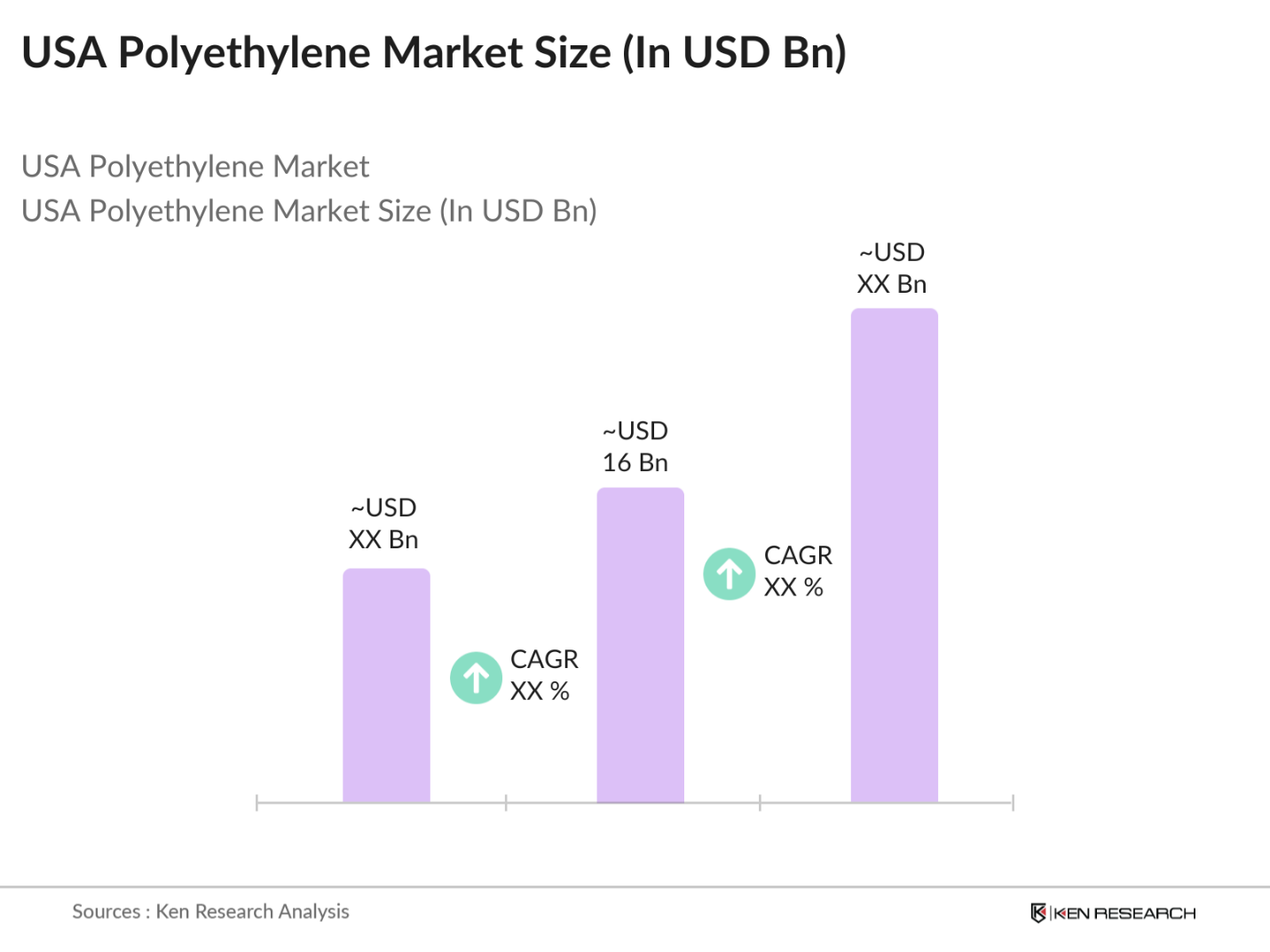

- The USA Polyethylene market is valued at USD 16 billion, based on a five-year historical analysis. This valuation is primarily driven by the extensive demand for polyethylene in packaging and construction applications. The abundant availability of shale gas in the USA has given polyethylene manufacturers a cost advantage, leading to expanded production capacities and higher output. Furthermore, innovations in manufacturing techniques, such as smart packaging integration and the adoption of bio-based alternatives, have supported consistent growth in the market.

- The market is predominantly influenced by key regions such as Texas, Louisiana, and Pennsylvania, where the availability of low-cost feedstock derived from shale gas is abundant. These states have seen major investments in polyethylene production facilities, making them hubs for the industry. The proximity to vast petrochemical resources, coupled with established infrastructure, gives these regions a strategic advantage in serving both domestic and international markets.

- The U.S. Department of the Interiors ban on single-use plastics across national parks and federal facilities, implemented in 2023, has led to a substantial decrease in single-use polyethylene production. This policy is part of broader federal efforts to reduce plastic pollution, affecting an estimated 4 million pounds of polyethylene usage annually.

USA Polyethylene Market Segmentation

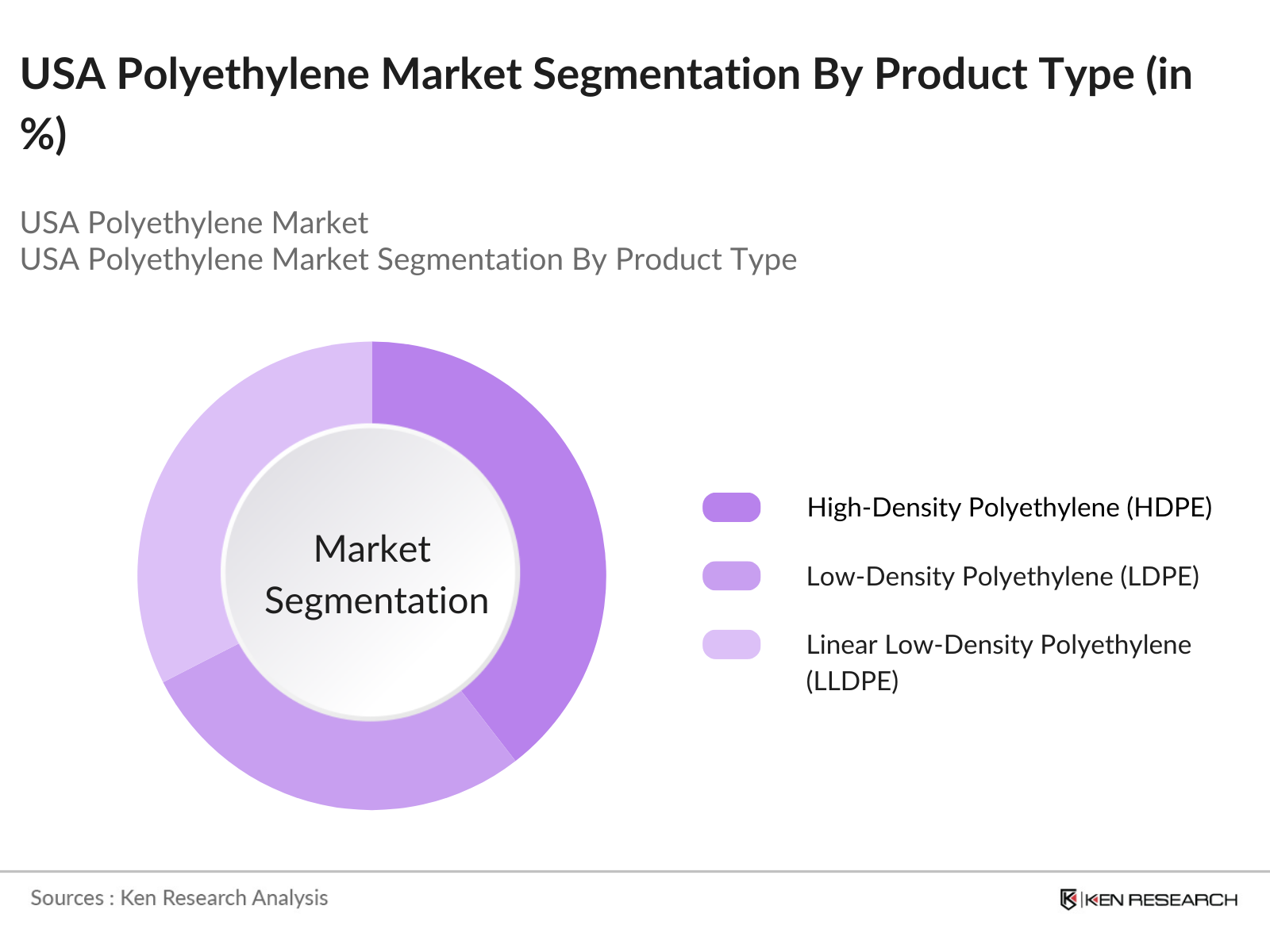

By Product Type: The USA Polyethylene market is segmented by product type into High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), and Linear Low-Density Polyethylene (LLDPE). Recently, HDPE has dominated the market share due to its extensive use in construction, packaging, and automotive sectors. Its high resistance to impact and temperature variations makes it a preferred material in industrial applications. LDPE, on the other hand, is widely used in film and packaging applications, offering flexibility and clarity that other polyethylene grades cannot match.

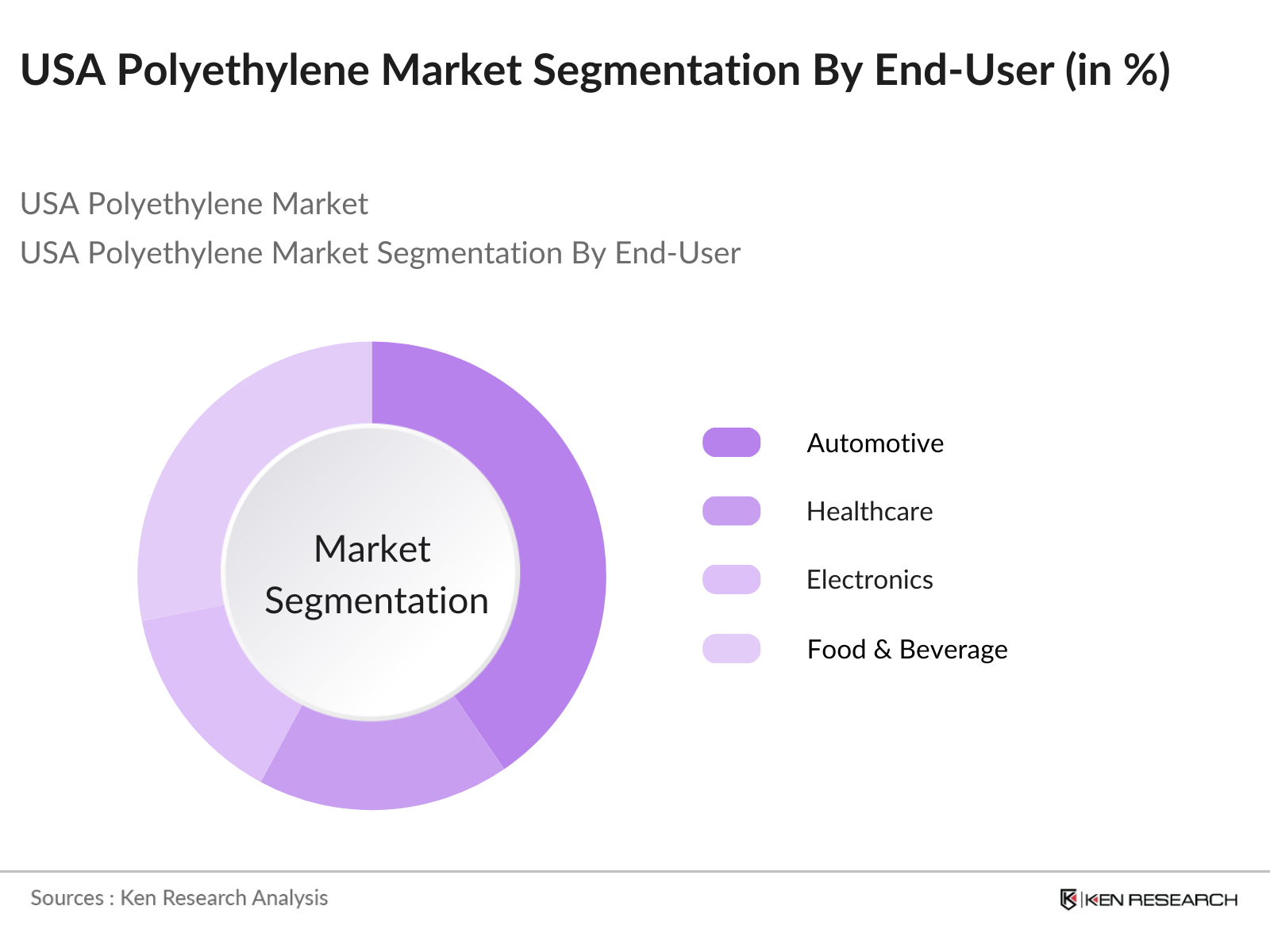

By End-Use Industry: The market is segmented by end-use industry into Automotive, Healthcare, Electronics, Food & Beverage, and Construction. The food and beverage sector remains the dominant player due to the widespread use of polyethylene for packaging solutions. The increasing demand for packaged food and the growth of e-commerce have propelled this segments dominance. The healthcare segment is also emerging as a significant market, driven by the need for sterile and durable packaging for medical devices and pharmaceutical products.

USA Polyethylene Market Competitive Landscape

The USA Polyethylene market is competitive and features a mix of major multinational corporations and regional players. The market is dominated by companies that have integrated operations from raw material extraction to polyethylene production. These companies have established a significant presence due to their vast production capacities and extensive distribution networks. The competitive landscape in the USA Polyethylene market shows a clear preference for strategic partnerships, technological advancements, and a commitment to sustainability.

USA Polyethylene Industry Analysis

Growth Drivers

- Increased Demand in Packaging (Segmentation: Bottles & Containers, Films & Sheets): The demand for polyethylene in the U.S. packaging industry has increased significantly, driven by the growth in bottled water consumption and food storage solutions. According to U.S. Census data, over 48 billion units of bottled water were produced in the U.S. in 2023, reflecting a substantial need for polyethylene-based bottles and containers. Moreover, the flexible packaging segment, including films and sheets, has grown in tandem with the rise of e-commerce, which now constitutes over 15% of total retail sales in the country.

- Shale Gas Boom Impact on Cost Competitiveness (Regional Dynamics): The shale gas boom has substantially reduced the cost of ethylene production in the U.S., making it one of the most cost-competitive regions for polyethylene production globally. The Energy Information Administration (EIA) estimates that U.S. natural gas production reached 117.5 billion cubic feet per day in 2024, supporting lower feedstock prices and enhancing the cost advantages of domestic polyethylene manufacturers.

- Expansion of Construction Industry Applications (Geomembranes, Geotextiles): The construction sector's demand for high-density polyethylene (HDPE) has risen sharply, particularly for geomembranes and geotextiles used in infrastructure projects. The American Society of Civil Engineers reported that U.S. infrastructure spending increased by $1.2 trillion in 2023. This expansion is driven by increased federal investment in public works and urban development projects, leading to higher consumption of construction-related polyethylene products.

Market Challenges

- Stringent Regulations on Single-Use Plastics (Government Policies): The U.S. government has implemented stricter regulations on single-use plastics, significantly impacting polyethylene consumption patterns. The U.S. Department of the Interior announced a ban on the sale and distribution of single-use plastic products across national parks by 2023, affecting over 400 locations and reducing demand for single-use polyethylene items.

- Environmental Concerns Associated with Production and Disposal: Environmental issues related to polyethylene production and disposal are intensifying, with polyethylene waste constituting over 30 million tons of the U.S. plastic waste stream in 2023. The Environmental Protection Agency (EPA) has introduced new recycling mandates and waste management policies to tackle the challenges associated with polyethylenes environmental impact.

USA Polyethylene Market Future Outlook

Over the next few years, the USA Polyethylene market is expected to see significant growth driven by increased demand in key end-use industries such as construction, packaging, and healthcare. The ongoing developments in shale gas extraction and the expanding polyethylene production capacities are poised to bolster the market further. The growth is also likely to be influenced by a rise in the adoption of sustainable practices and bio-based polyethylene materials, aligning with the global push for environmentally friendly products.

Market Opportunities

- Bio-Based Polymers as Sustainable Alternatives: The development and commercialization of bio-based polyethylene as a sustainable alternative are creating new market opportunities. The USDA reports that bio-based product manufacturing contributed $459 billion to the U.S. economy in 2023, highlighting the shift toward bio-based solutions. The demand for bio-based polyethylene is expected to rise as companies aim to meet the sustainability goals set by federal and state governments.

- Adoption in Advanced Manufacturing Technologies (CNC Machines, 3D Printing): Polyethylene's versatility in advanced manufacturing technologies, such as CNC machining and 3D printing, is increasing its applications in automotive and consumer goods. The U.S. additive manufacturing sector, valued at $12.7 billion in 2023, has shown increased integration of polyethylene due to its favorable mechanical properties and ease of fabrication.

Scope of the Report

|

By Product Type |

High-Density Polyethylene (HDPE) Low-Density Polyethylene (LDPE) Linear Low-Density Polyethylene (LLDPE) |

|

By Application |

Packaging Construction Agriculture Industrial Machinery |

|

By End-Use |

Automotive Healthcare Electronics Food and Beverage Others |

|

Region |

North-East USA South-East USA Mid-West USA West Coast USA |

Products

Key Target Audience

Automotive Manufacturers

Packaging Industry Players

Healthcare Product Manufacturers

Construction and Infrastructure Companies

Government and Regulatory Bodies (U.S. Environmental Protection Agency, U.S. Department of the Interior)

Investments and Venture Capitalist Firms

Electronics and Consumer Goods Manufacturers

Petrochemical Feedstock Suppliers

Companies

Players Mentioned in the Report

ExxonMobil Chemical

Dow, Inc.

Chevron Phillips Chemical Co.

Westlake Chemical

LyondellBasell Industries

Huntsman International LLC

SABIC

Borealis AG

INEOS

Formosa Plastics Corporation

Table of Contents

1. USA Polyethylene Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. USA Polyethylene Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. USA Polyethylene Market Analysis

3.1 Growth Drivers

3.1.1 Increased Demand in Packaging (Segmentation: Bottles & Containers, Films & Sheets)

3.1.2 Shale Gas Boom Impact on Cost Competitiveness (Regional Dynamics)

3.1.3 Expansion of Construction Industry Applications (Geomembranes, Geotextiles)

3.1.4 Rising Adoption of Smart Packaging Solutions (Integration of RFID, QR Codes)

3.2 Market Challenges

3.2.1 Stringent Regulations on Single-Use Plastics (Government Policies)

3.2.2 Environmental Concerns Associated with Production and Disposal

3.3 Opportunities

3.3.1 Bio-Based Polymers as Sustainable Alternatives

3.3.2 Adoption in Advanced Manufacturing Technologies (CNC Machines, 3D Printing)

3.4 Trends

3.4.1 Growth in Use of High-Density Polyethylene (HDPE) in Construction

3.4.2 Increase in E-Commerce and Demand for Flexible Packaging

3.5 Government Regulation

3.5.1 Reduction in Single-Use Plastic (U.S. Department of Interior Policies)

3.5.2 Compliance and Certification Requirements for Recyclability

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. USA Polyethylene Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 High-Density Polyethylene (HDPE)

4.1.2 Low-Density Polyethylene (LDPE)

4.1.3 Linear Low-Density Polyethylene (LLDPE)

4.2 By Application (In Value %)

4.2.1 Packaging

4.2.2 Construction

4.2.3 Agriculture

4.2.4 Industrial Machinery

4.3 By End-Use (In Value %)

4.3.1 Automotive

4.3.2 Healthcare

4.3.3 Electronics

4.3.4 Food and Beverage

4.3.5 Others

4.4 By Region (In Value %)

4.4.1 North-East USA

4.4.2 South-East USA

4.4.3 Mid-West USA

4.4.4 West Coast USA

5. USA Polyethylene Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 ExxonMobil Chemical

5.1.2 Dow, Inc.

5.1.3 Chevron Phillips Chemical Co.

5.1.4 Westlake Chemical

5.1.5 DuPont

5.1.6 Celanese Corporation

5.1.7 Eastman Chemical Company

5.1.8 Huntsman International LLC

5.1.9 RTP Company

5.1.10 SABIC

5.1.11 LyondellBasell Industries Holdings BV

5.1.12 INEOS

5.1.13 Formosa Plastics Corporation

5.1.14 Borealis AG

5.1.15 Braskem

5.2 Cross Comparison Parameters (Market Share, Revenue, Production Capacities, Geographical Presence, Investment in R&D, Sustainability Initiatives, Strategic Partnerships, New Product Developments)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. USA Polyethylene Market Regulatory Framework

6.1 Environmental Standards

6.2 Compliance Requirements

6.3 Certification Processes

7. USA Polyethylene Market Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. USA Polyethylene Market Future Segmentation

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By End-Use (In Value %)

8.4 By Region (In Value %)

9. USA Polyethylene Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Polyethylene Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data related to the USA Polyethylene Market is compiled and analyzed. This includes assessing market penetration, the ratio of polyethylene production to consumption, and the resultant revenue generation. Further, an evaluation of key market trends and regulatory impacts is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through consultations with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple polyethylene manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the USA Polyethylene Market.

Frequently Asked Questions

1. How big is the USA Polyethylene Market?

The USA Polyethylene market is valued at USD 16 billion, based on a five-year historical analysis. This valuation is primarily driven by the extensive demand for polyethylene in packaging and construction applications.

2. What are the challenges in the USA Polyethylene Market?

Challenges include stringent government regulations concerning single-use plastics and environmental concerns regarding production and waste management. The competition from bio-based polymers also poses a significant threat to conventional polyethylene products.

3. Who are the major players in the USA Polyethylene Market?

Key players include ExxonMobil Chemical, Dow, Chevron Phillips Chemical Co., LyondellBasell Industries, and Westlake Chemical. These companies dominate due to their extensive production capacities, strategic partnerships, and sustainability initiatives.

4. What are the growth drivers of the USA Polyethylene Market?

The growth drivers include increased demand from packaging and construction industries, cost advantages of production due to shale gas availability, and rising adoption of smart, packaging, and technological advancements such as smart packaging solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.