USA Soy Protein Market Outlook to 2030

Region:North America

Author(s):Samanyu

Product Code:KROD4203

November 2024

98

About the Report

USA Soy Protein Market Overview

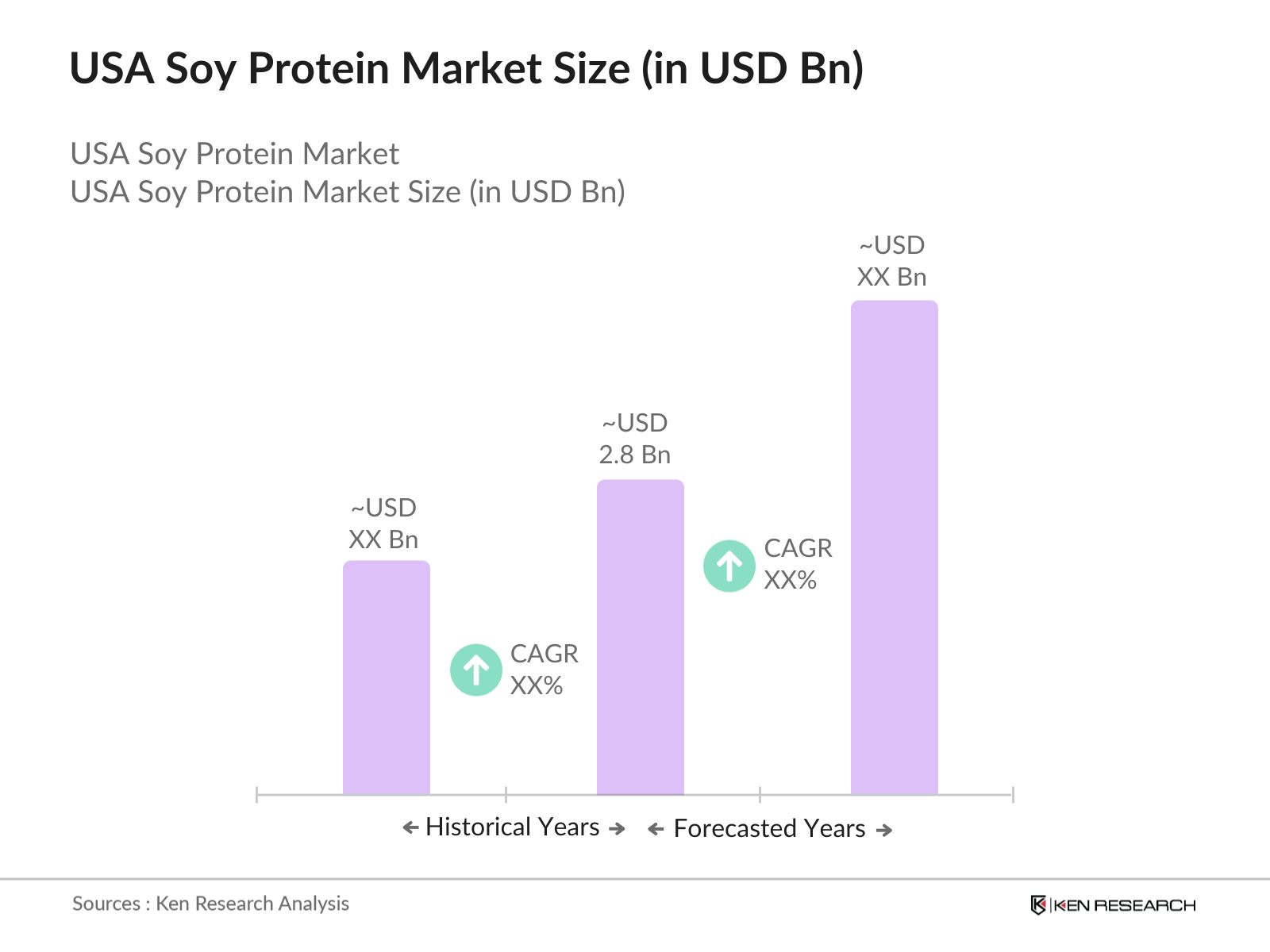

- The USA soy protein market is valued at USD 2.8 Bn, based on a five-year historical analysis. The market has expanded as consumers seek sustainable, non-animal protein sources, particularly in the food and beverage industry. The increasing awareness of the health benefits associated with soy protein, such as cardiovascular and metabolic health, has further fueled demand. Companies are also investing heavily in product innovation to cater to the growing vegan and vegetarian populations.

- The USA remains the dominant player in the global soy protein market, primarily due to its large agricultural base and advanced food processing infrastructure. Major cities such as Chicago, New York, and Los Angeles are hubs for food innovation, including the development of soy-based products. Additionally, these regions have a higher concentration of consumers interested in plant-based diets and sustainability, further contributing to the market's dominance.

- Soy protein is becoming a preferred ingredient in functional foods and beverages due to its versatility and health benefits. According to the USDA, soy protein is increasingly incorporated into products such as protein bars, shakes, and supplements. The growing demand for functional beverages in the U.S., driven by health-conscious consumers, has propelled soy proteins usage. In 2023, the National Institutes of Health (NIH) indicated that soy protein-based beverages are frequently chosen for their heart health and cholesterol-lowering benefits, aligning with consumer interest in health and wellness.

USA Soy Protein Market Segmentation

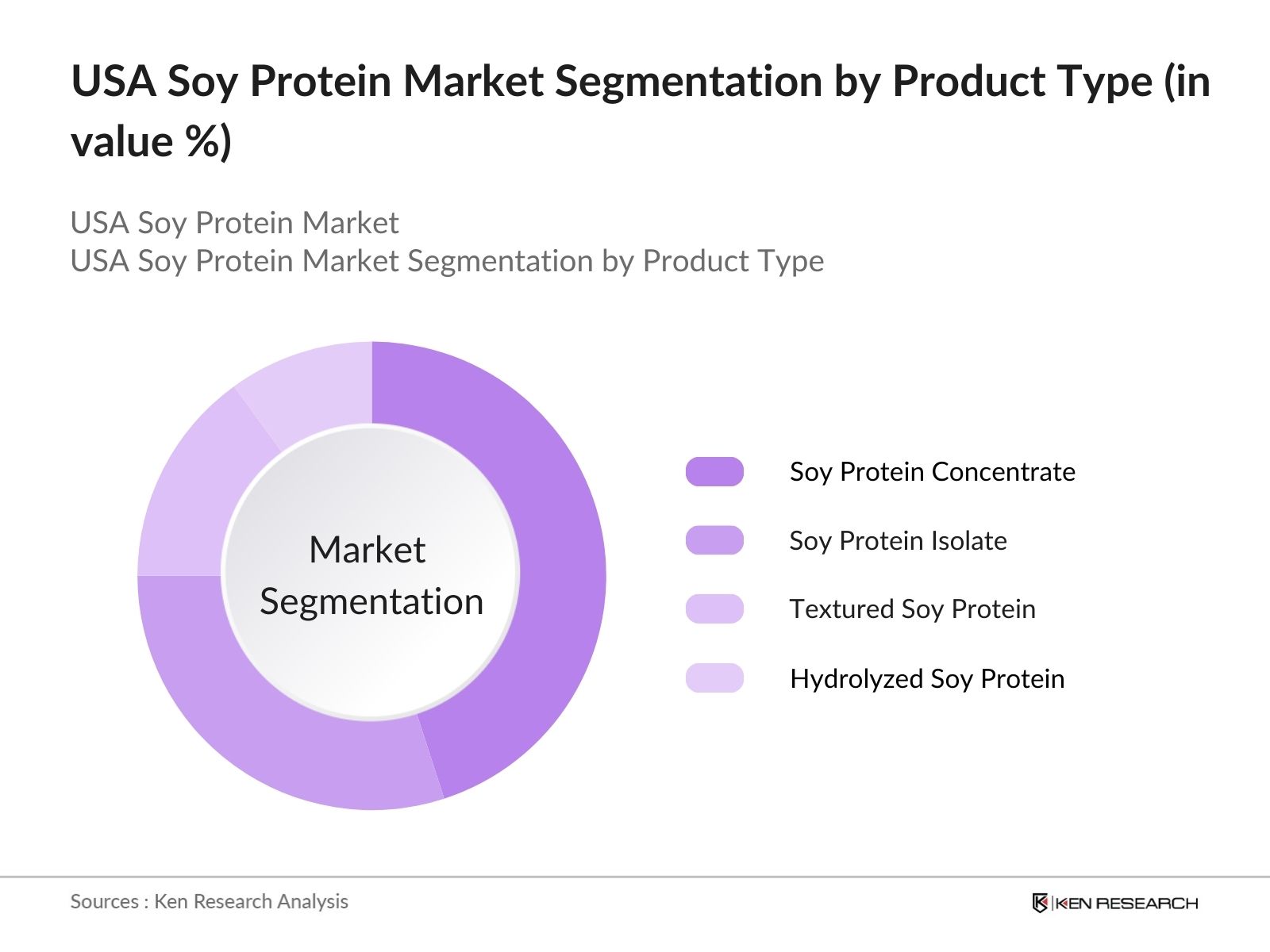

By Product Type: The market is segmented by product type into soy protein concentrate, soy protein isolate, textured soy protein, and hydrolyzed soy protein. Soy protein concentrate dominates the product type segmentation due to its widespread use in food and beverage applications, particularly in meat substitutes and dairy alternatives. The concentrate's ability to retain most of soys natural fiber and protein content makes it highly desirable for health-conscious consumers, driving its dominant market share.

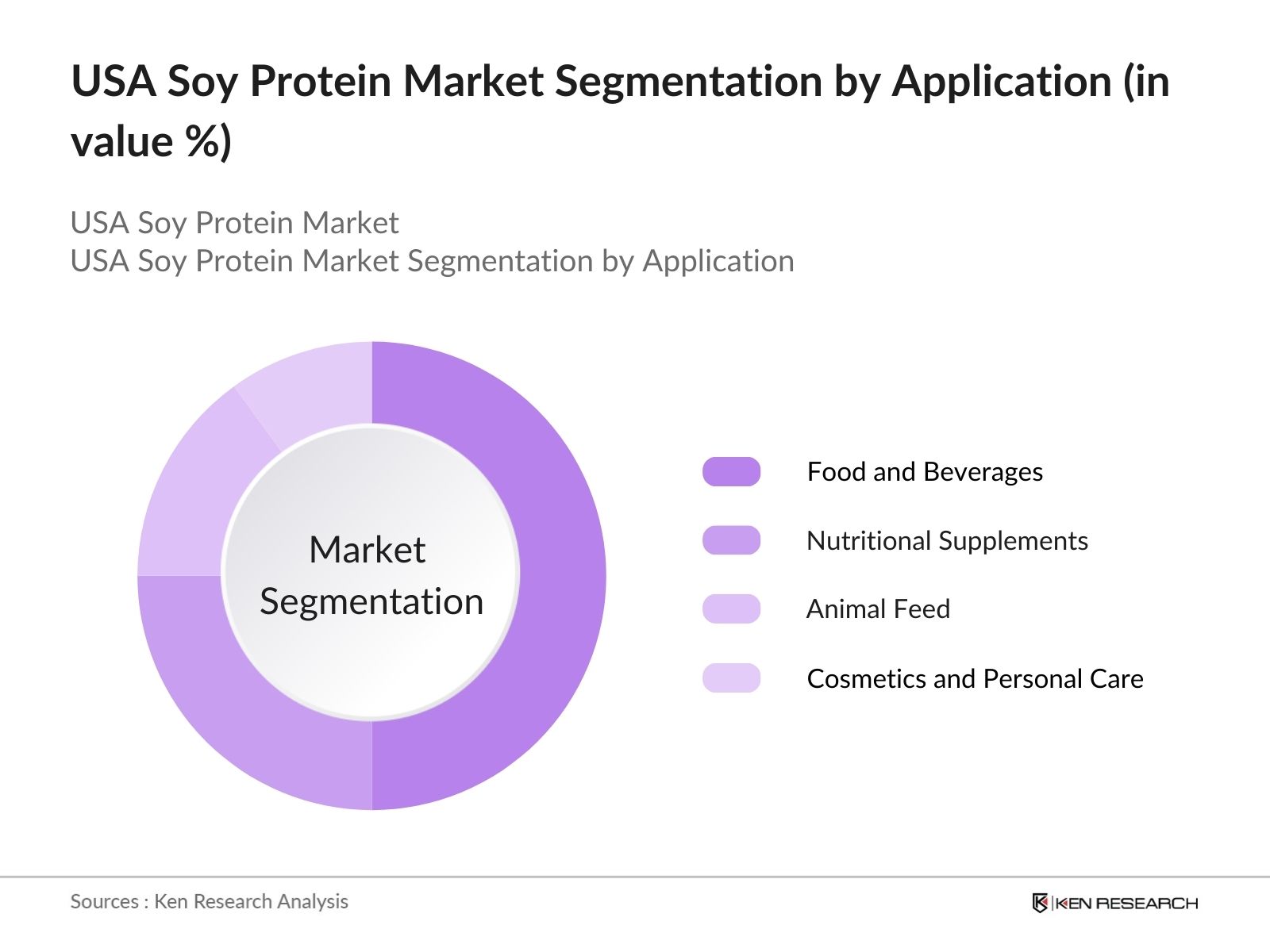

By Application: The market is segmented by application into food and beverages, nutritional supplements, animal feed, and cosmetics. The food and beverage segment leads the market, particularly in applications like meat substitutes and dairy-free products. This dominance is largely attributed to the increasing demand for plant-based products among health-conscious consumers and the rise of veganism. Companies are continuously introducing innovative food products such as soy protein-based burgers, shakes, and dairy alternatives, pushing this sub-segment to the forefront.

USA Soy Protein Market Competitive Landscape

The USA soy protein market is dominated by several key players, each contributing significantly to the industry through product innovation and extensive distribution networks.

The competitive landscape is characterized by both domestic and international players, including Archer Daniels Midland (ADM), Cargill, DuPont, and Bunge. These companies have strong supply chain networks and have established long-term relationships with food manufacturers. ADM, in particular, has gained prominence due to its significant investments in soy protein research and development, contributing to its leadership in the global market. Smaller players and startups focusing on organic and non-GMO soy protein products are also emerging, driven by consumer demand for clean-label foods.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

Key Product |

R&D Investment |

Global Presence |

Recent Innovations |

|

Archer Daniels Midland (ADM) |

1902 |

Chicago, USA |

||||||

|

Cargill Inc. |

1865 |

Minneapolis, USA |

||||||

|

DuPont Nutrition & Biosciences |

1802 |

Wilmington, USA |

||||||

|

Bunge Limited |

1818 |

St. Louis, USA |

||||||

|

Kerry Group |

1972 |

Tralee, Ireland |

USA Soy Protein Industry Analysis

Growth Drivers

- Growing Demand for Plant-Based Proteins: The shift towards plant-based diets has gained substantial momentum globally. In the USA, the growing awareness of the environmental and health benefits of plant-based diets has led to a marked increase in demand for soy protein products. According to the United Nations, global food demand is expected to increase by 60% by 2050, driving innovation in plant-based protein sources like soy. Additionally, data from the World Bank indicates that soybeans remain one of the most important crops in the United States, accounting for over 34.4 million hectares of cultivation in 2023, signaling strong growth potential in the soy protein sector.

- Increasing Vegan & Vegetarian Population: The U.S. Census Bureau data shows a growing trend towards veganism and vegetarianism. In 2023, approximately 10 million Americans identified as vegan, a number that has been increasing steadily. Soy protein is a key alternative for plant-based diets, fulfilling nutritional needs where traditional animal proteins are avoided. The nutritional profile of soy, containing all nine essential amino acids, positions it as a high-quality protein option. Furthermore, the USDA reports that 95% of soybean oil produced in the U.S. is used in food applications, reinforcing the central role soy plays in plant-based diets.

- Sustainability Concerns Driving Plant-Based Alternatives: Soy protein's appeal is amplified by environmental sustainability concerns. According to the Environmental Protection Agency (EPA), agricultural production contributes 10% to greenhouse gas emissions in the USA, with livestock accounting for the largest share. Soy protein offers a significantly lower environmental impact compared to animal proteins, as soybeans require 40% less land and emit 50% less CO. Furthermore, data from the U.S. Department of Agriculture (USDA) indicates that soy cultivation is increasingly integrated into sustainable farming practices, such as crop rotation, which helps preserve soil health and reduce reliance on chemical inputs.

Market Challenges

- Allergenicity Concerns: Soy protein is classified as one of the top eight food allergens in the United States, as per the Food Allergen Labeling and Consumer Protection Act (FALCPA). The prevalence of soy allergies impacts around 0.4% of the U.S. population, particularly affecting children. This allergenicity concern limits the consumption of soy protein products, despite the growing demand for plant-based alternatives. According to the National Institute of Allergy and Infectious Diseases (NIAID), soy allergies tend to persist into adulthood, reducing the consumer base and making product labeling a critical concern for manufacturers.

- Competitive Pressure from Other Plant-Based Proteins: Soy protein faces competitive pressure from other emerging plant-based proteins such as pea and rice proteins. According to the Food and Agriculture Organization (FAO), global pea protein production has been rising, particularly due to its non-allergenic properties. In the U.S., companies are increasingly incorporating pea protein into alternative meat products. The U.S. Department of Agriculture (USDA) reports that while soy remains dominant in the plant protein sector, the market share for pea protein has risen sharply in recent years due to its ability to mimic the texture and taste of meat more effectively in food applications.

USA Soy Protein Market Future Outlook

Over the next five years, the USA soy protein market is expected to see significant growth driven by innovations in plant-based food products, increasing consumer awareness about health benefits, and the rising demand for sustainable protein sources. Technological advancements in soy protein production and the development of new formulations will also enhance the market's appeal to a broader consumer base. The market is likely to benefit from the increasing number of consumers adopting vegan and vegetarian diets and the government's emphasis on promoting sustainable agricultural practices.

Future Market Opportunities

- Innovations in Soy Protein Derivatives: Technological advancements in enzyme-treated soy protein and the development of non-GMO variants present opportunities for growth. The U.S. Patent and Trademark Office (USPTO) has seen a surge in patents filed for novel soy protein derivatives, reflecting industry interest in new product formulations. Non-GMO soy protein products are gaining traction, particularly as consumers grow more health-conscious. According to the USDA, nearly 94% of soybeans in the U.S. are genetically modified, but the demand for non-GMO soybeans is rising, driving innovation in alternative soy protein formulations.

- Expansion into Non-traditional Markets: Soy protein is expanding beyond food applications into areas like pet food and sports nutrition. According to the American Pet Products Association (APPA), the U.S. pet food industry was valued at over USD 42 billion in 2023, with a growing emphasis on plant-based ingredients in premium pet food offerings. Soy protein is increasingly being incorporated into these products for its nutritional benefits. Furthermore, the National Collegiate Athletic Association (NCAA) highlights the growing interest in soy protein among athletes, who use it for muscle recovery and endurance, further broadening the market's scope.

Scope of the Report

|

By Product Type |

Soy Protein Concentrate Soy Protein Isolate Textured Soy Protein Hydrolyzed Soy Protein |

|

By Application |

Food & Beverage Nutritional Supplements Animal Feed Cosmetics and Personal Care |

|

By Distribution Channel |

B2B Sales Retail Stores E-commerce |

|

By End-User |

Commercial Food Manufacturers Dietary Supplement Manufacturers Animal Feed Producers |

|

By Region |

Northeast Midwest South West |

Products

Key Target Audience

Food and Beverage Manufacturers

Nutritional Supplement Producers

Animal Feed Manufacturers

Cosmetics and Personal Care Manufacturers

Banks and Financial Institutes

Investments and Venture Capitalist Firms

Organic and Non-GMO Certification Bodies

Government and Regulatory Bodies (FDA, USDA)

Retail and E-commerce Platforms

Companies

Major Players

Archer Daniels Midland (ADM)

Cargill Inc.

DuPont Nutrition & Biosciences

Bunge Limited

Kerry Group

CHS Inc.

Roquette Frres

Wilmar International Limited

Fuji Oil Holdings Inc.

Gushen Group Co., Ltd.

Shandong Yuwang Ecological Food Industry Co., Ltd.

Crown Soya Protein Group

Devansoy Inc.

Ingredion Incorporated

Farbest Brands

Table of Contents

1. USA Soy Protein Market Overview

1.1. Definition and Scope (Soy Protein Product Categories, Key Ingredients, and Sources)

1.2. Market Taxonomy (Soy Protein Concentrates, Isolates, Textured, Hydrolyzed)

1.3. Market Growth Rate (CAGR, Regional Growth, Adoption in Food & Beverage)

1.4. Market Segmentation Overview (Product Type, Application, Distribution Channel, End-Use, Region)

2. USA Soy Protein Market Size (In USD Bn)

2.1. Historical Market Size (Past Demand & Consumption Trends)

2.2. Year-On-Year Growth Analysis (Annual Growth, Emerging Trends)

2.3. Key Market Developments and Milestones (Innovations, Regulatory Changes, Market Entry of New Competitors)

3. USA Soy Protein Market Analysis

3.1. Growth Drivers

3.1.1. Growing Demand for Plant-Based Proteins

3.1.2. Increasing Vegan & Vegetarian Population

3.1.3. Sustainability Concerns Driving Plant-Based Alternatives

3.1.4. Health Benefits and Nutritional Value

3.2. Restraints

3.2.1. Allergenicity Concerns

3.2.2. Competitive Pressure from Other Plant-Based Proteins (Pea, Rice, etc.)

3.2.3. Price Volatility of Raw Materials

3.3. Opportunities

3.3.1. Innovations in Soy Protein Derivatives (Enzyme-treated, Non-GMO)

3.3.2. Expansion into Non-traditional Markets (Pet Food, Sports Nutrition)

3.3.3. Partnership with Food Giants for Product Launches

3.4. Trends

3.4.1. Growth in Clean Label Soy Protein Products

3.4.2. Increased Usage in Functional Foods & Beverages

3.4.3. Shift Towards Organic and Non-GMO Soy Protein

3.5. Government Regulation

3.5.1. FDA Guidelines on Soy Protein Labeling

3.5.2. Organic and Non-GMO Certification

3.5.3. Tariffs and Trade Policies Affecting Soy Supply Chain

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Farmers, Processors, Retailers, Consumers)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Competitive Rivalry, Threat of Substitution, Threat of New Entrants)

3.9. Competition Ecosystem (Key Players, Market Strategies, Collaborations)

4. USA Soy Protein Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Soy Protein Concentrate

4.1.2. Soy Protein Isolate

4.1.3. Textured Soy Protein

4.1.4. Hydrolyzed Soy Protein

4.2. By Application (In Value %)

4.2.1. Food & Beverage (Meat Alternatives, Dairy Alternatives, Protein Bars)

4.2.2. Nutritional Supplements (Sports Nutrition, Weight Management)

4.2.3. Animal Feed

4.2.4. Cosmetics and Personal Care

4.3. By Distribution Channel (In Value %)

4.3.1. B2B Sales

4.3.2. Retail Stores (Supermarkets, Specialty Stores)

4.3.3. E-commerce

4.4. By End-Use (In Value %)

4.4.1. Commercial Food Manufacturers

4.4.2. Dietary Supplement Manufacturers

4.4.3. Animal Feed Producers

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Soy Protein Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Archer Daniels Midland Company

5.1.2. Cargill Inc.

5.1.3. DuPont Nutrition & Biosciences

5.1.4. Kerry Group

5.1.5. Bunge Limited

5.1.6. CHS Inc.

5.1.7. Roquette Frres

5.1.8. Wilmar International Limited

5.1.9. Fuji Oil Holdings Inc.

5.1.10. Gushen Group Co., Ltd.

5.1.11. Shandong Yuwang Ecological Food Industry Co., Ltd.

5.1.12. Crown Soya Protein Group

5.1.13. Devansoy Inc.

5.1.14. Ingredion Incorporated

5.1.15. Farbest Brands

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, Product Portfolio, R&D Investment)

5.3. Market Share Analysis (Key Players' Market Share %)

5.4. Strategic Initiatives (New Product Development, Sustainability Initiatives, Strategic Partnerships)

5.5. Mergers and Acquisitions (Recent Acquisitions, Impact on Market Position)

5.6. Investment Analysis (CapEx Trends, Facility Expansions)

5.7. Venture Capital Funding (Key Startups, Funding Trends)

5.8. Government Grants (Support for Innovation, Sustainable Practices)

5.9. Private Equity Investments (Recent PE Activity, Impact on Market Consolidation)

6. USA Soy Protein Market Regulatory Framework

6.1. Food Safety Standards (FDA, USDA, Non-GMO Project)

6.2. Compliance Requirements (Nutritional Labeling, Claims)

6.3. Certification Processes (Organic, Halal, Kosher)

7. USA Soy Protein Market Future Size (In USD Bn)

7.1. Future Market Size Projections (Forecasted Demand, Growth Potential)

7.2. Key Factors Driving Future Market Growth (Technological Advancements, Consumer Preferences)

8. USA Soy Protein Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-Use (In Value %)

8.5. By Region (In Value %)

9. USA Soy Protein Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Market, Share of Market)

9.2. Customer Cohort Analysis (Market Segments, Preferences, Behavior)

9.3. Marketing Initiatives (Targeted Campaigns, Branding Strategies)

9.4. White Space Opportunity Analysis (Untapped Segments, Product Innovation)

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial step involved constructing an ecosystem map to identify the major stakeholders in the USA Soy Protein Market. This phase was supported by comprehensive desk research and data collection from secondary and proprietary databases to gather critical market information.

Step 2: Market Analysis and Construction

In this phase, historical data on the USA Soy Protein Market was compiled and analyzed. This included assessing market penetration and revenue generation trends, ensuring the accuracy of historical and current data.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through direct consultation with industry experts via interviews and surveys. These consultations provided operational insights that enriched our analysis and supported the reports findings.

Step 4: Research Synthesis and Final Output

In the final stage, a synthesis of all the research was conducted, drawing from industry interactions and quantitative analysis. This step ensured a comprehensive, accurate report reflecting current market conditions.

Frequently Asked Questions

01. How big is the USA Soy Protein Market?

The USA Soy Protein Market is valued at USD 2.8 billion in 2023, driven by the increasing demand for plant-based protein sources and innovations in the food and beverage industry.

02. What are the challenges in the USA Soy Protein Market?

Challenges in USA Soy Protein Market include the fluctuating prices of raw materials, competition from other plant-based proteins, and concerns related to soy allergenicity among consumers.

03. Who are the major players in the USA Soy Protein Market?

Key players in USA Soy Protein Market include Archer Daniels Midland (ADM), Cargill Inc., DuPont Nutrition & Biosciences, Bunge Limited, and Kerry Group. These companies dominate due to their established distribution networks, product portfolios, and significant R&D investments.

04. What are the growth drivers of the USA Soy Protein Market?

The USA Soy Protein Market is propelled by the growing demand for plant-based proteins, increasing awareness of health benefits, and advancements in soy protein formulations for food and beverage applications.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.