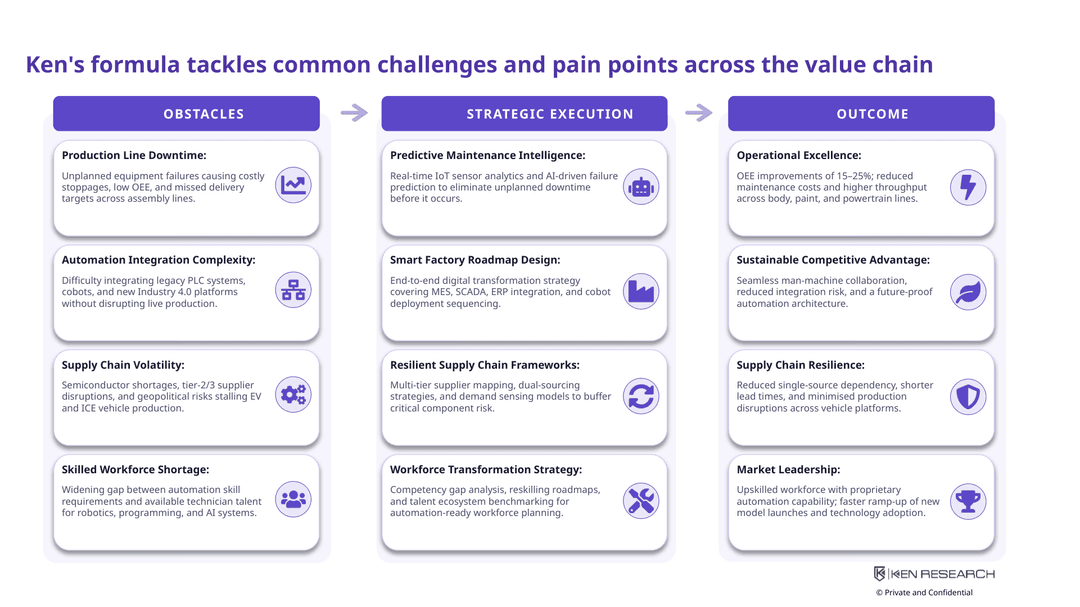

Why This POV Matters Now

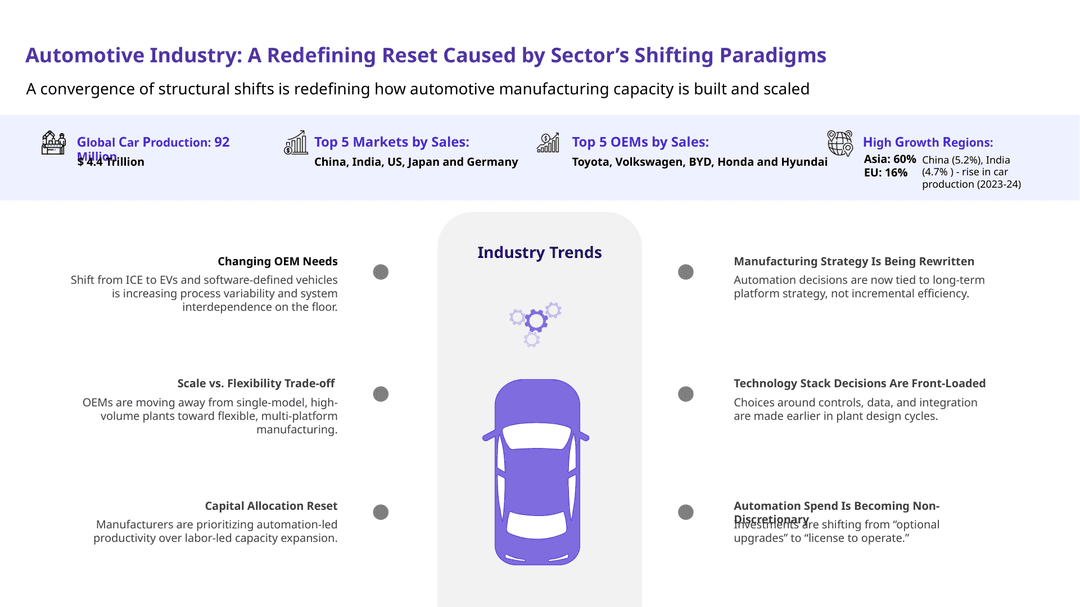

Theautomotive sectoris moving away from single-model, high-volume plants toward flexible, multi-platform manufacturing. As EV platforms, personalization, and software-led vehicle architectures increase production complexity, OEMs are being forced to rethink how they build capacity.

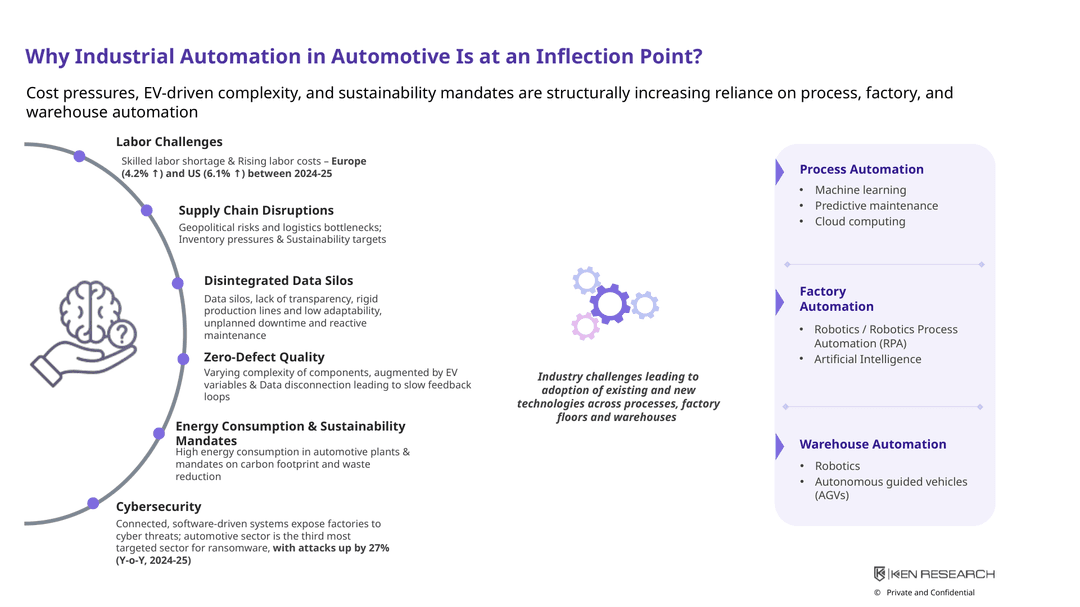

At the same time, cost pressures are rising. Skilled labor shortages, wage inflation, fragmented data systems, unplanned downtime, sustainability mandates, and cyber risks are increasing the urgency for automation-led manufacturing models.

Industrial automation is no longer a discretionary investment. For many OEMs, it is becoming a license to operate.

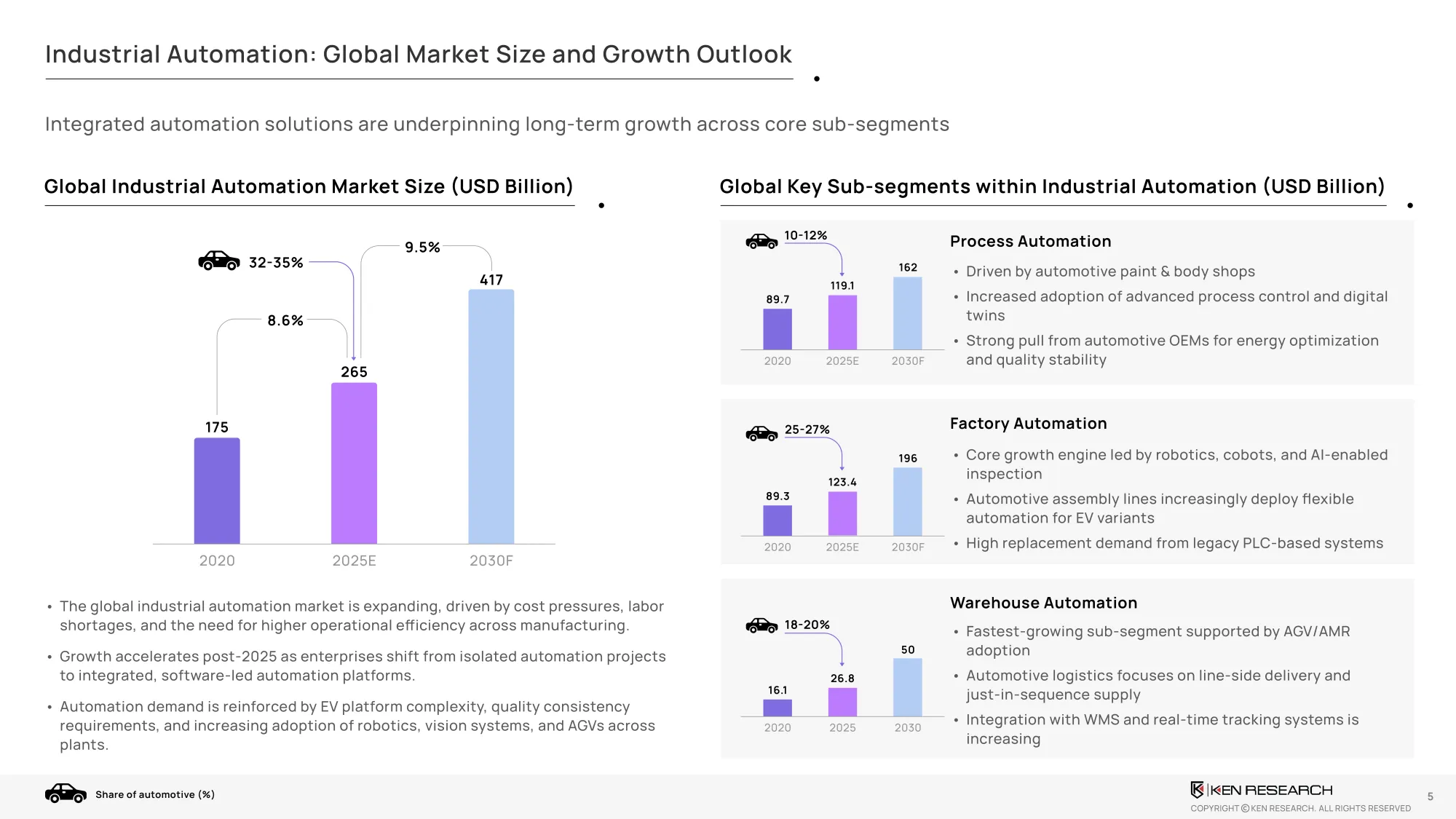

Market Context: The Automation Opportunity Is Scaling

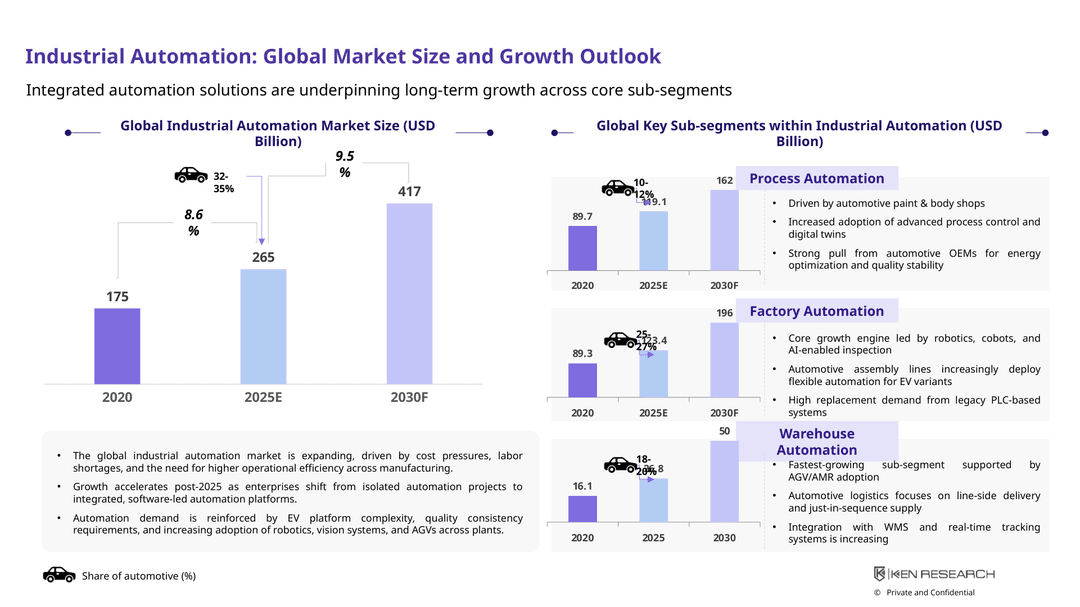

The global industrial automation market is expanding as manufacturing industries shift from isolated automation projects to integrated, software-led platforms. In automotive, this shift is especially visible across process automation, factory automation, and warehouse automation.

Industrial automationis being pulled deeper into automotive paint shops, body shops, assembly lines, EV production environments, logistics flows, and quality inspection systems. Robotics, cobots, machine vision, AGVs, AMRs, cloud platforms, predictive maintenance, AI, digital twins, and advanced control systems are becoming part of the new manufacturing stack.

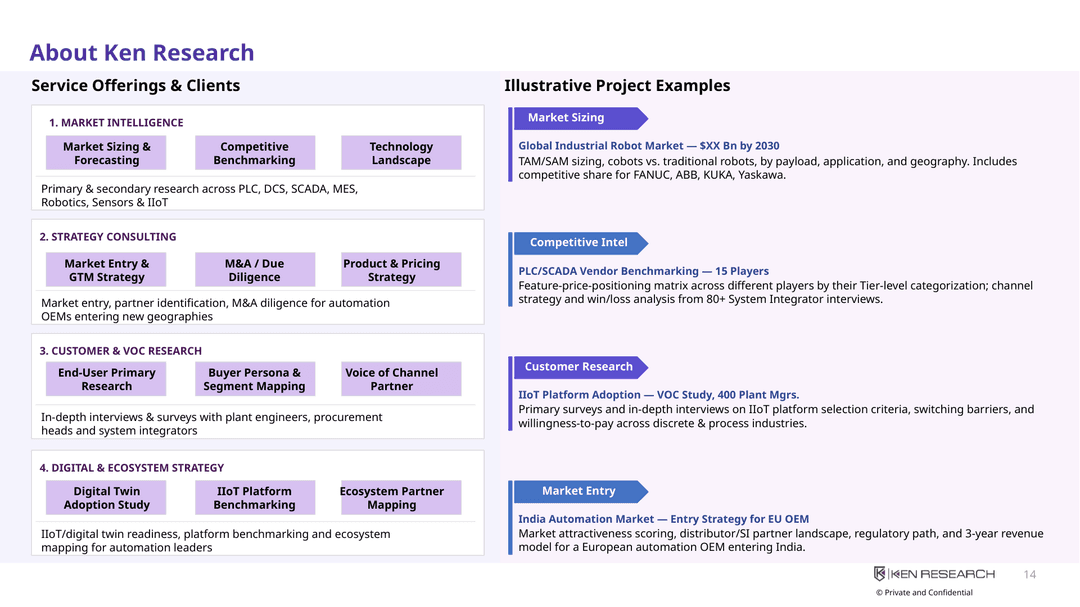

What the Full POV Helps You Decode

This POV helps automotive OEMs, automation providers, CTOs, IT leaders, and strategy teams understand where industrial automation is heading and why the next phase will be more integrated, data-led, and autonomous.

The full POV explores:

- Why automotive manufacturing is facing an automation reset

- How EV complexity and software-defined vehicles are reshaping factory requirements

- Why automation spend is shifting from optional capex to strategic necessity

- How process, factory, and warehouse automation are evolving across automotive plants

- Where robotics, cobots, AGVs, AMRs, AI, cloud, machine vision, and predictive maintenance are gaining relevance

- How the shift from Industry 4.0 to Industry 5.0 is changing the role of humans, machines, and data

- What OEMs and automation providers must prioritize to move from siloed automation to autonomous operating models

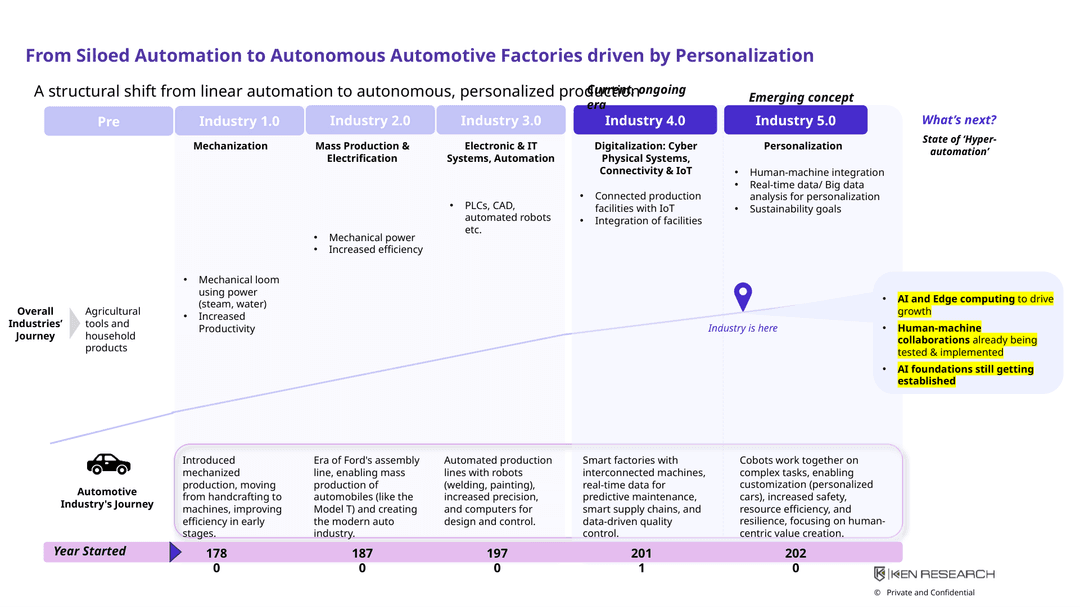

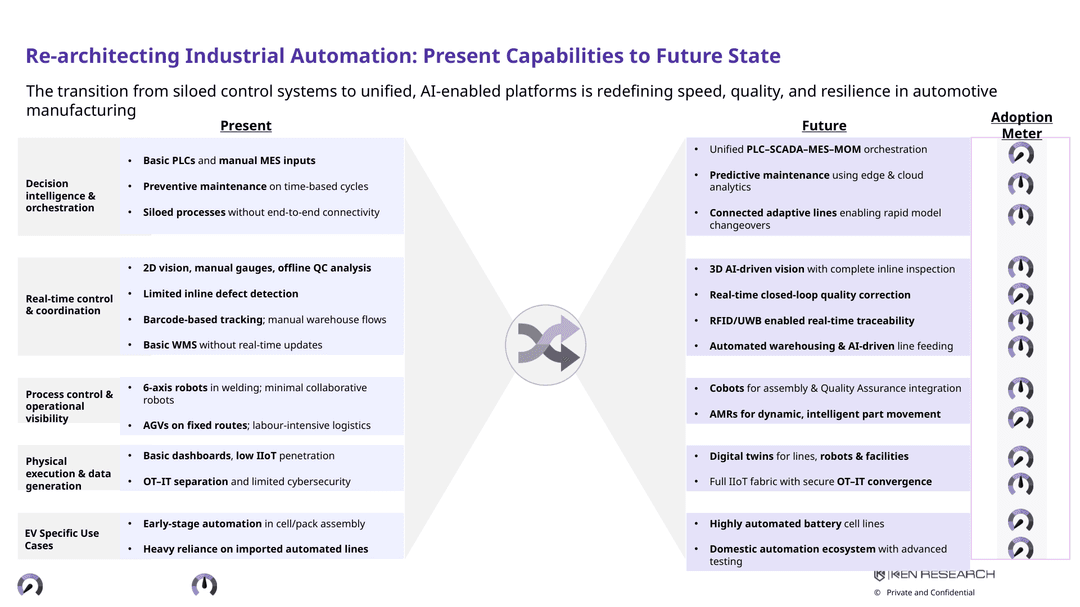

From Industry 4.0 to Industry 5.0: The New Manufacturing Logic

Automotive automation has moved through several phases, from mechanization and mass production to electronic systems, PLCs, robots, CAD, IoT, and connected factories. The current shift is more strategic.

Industry 4.0 focused on connectivity, cyber-physical systems, smart factories, predictive maintenance, and data-driven quality control. Industry 5.0 adds human-machine collaboration, personalization, sustainability, and resilience.

This means automotive manufacturing is moving beyond automation of individual tasks. The future factory must respond to model variation, EV assembly complexity, quality expectations, line-side logistics, energy optimization, and real-time decision-making.

The core challenge is not whether OEMs should automate. The challenge is how to build automation that is flexible, integrated, and future-ready.

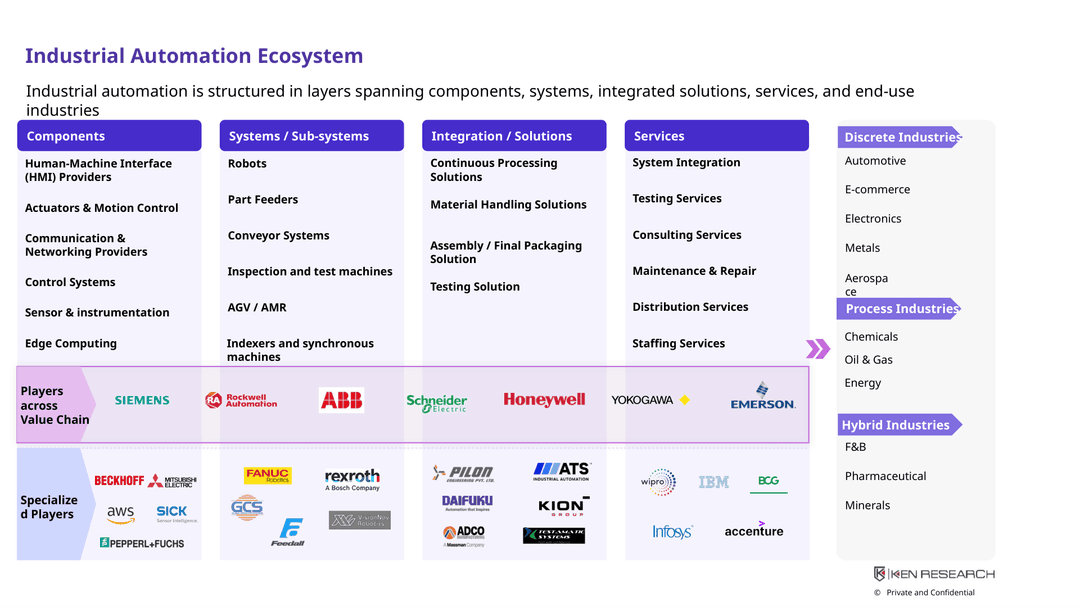

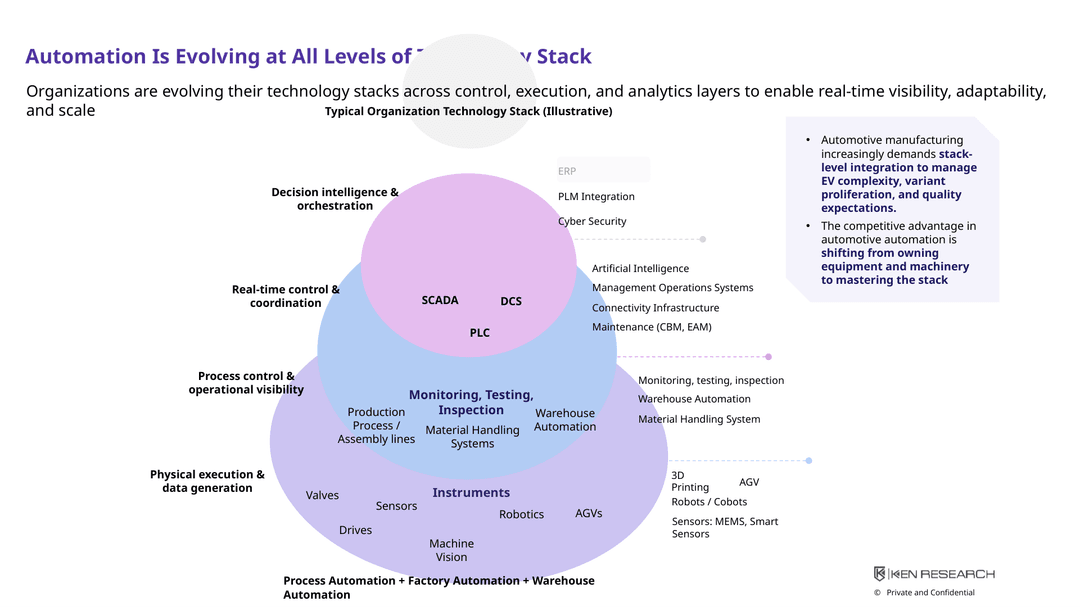

Technology Stack: Competitive Advantage Is Moving Beyond Equipment

Automotive plants are evolving across multiple layers of the technology stack. Sensors, drives, robotics, AGVs, machine vision, material handling systems, PLCs, SCADA, DCS, MES, MOM, ERP, PLM, cybersecurity, AI, cloud, and maintenance platforms are becoming interconnected.

This changes the source of competitive advantage.

Owning equipment or machinery alone is no longer enough. OEMs and automation providers must master stack-level integration across control, execution, analytics, and decision intelligence layers.

Factories that remain dependent on siloed systems may struggle with slow feedback loops, downtime, limited traceability, weak adaptability, and higher integration risk.

What This Means for OEMs and Automation Providers

For OEMs, the automation question is becoming board-level. Investment decisions need to align with EV roadmaps, model flexibility, supply chain resilience, product quality, energy efficiency, cybersecurity, and workforce readiness.

For automation providers, the opportunity is shifting from selling isolated systems to helping OEMs build integrated, scalable, and intelligent operating models. This creates demand for stronger solution design, system integration, digital twin readiness, IIoT platforms, predictive analytics, robotics deployment, and smart factory roadmaps.

The next three to five years will be critical. Human-machine collaboration, AI-enabled inspection, predictive maintenance, warehouse automation, and connected plant intelligence are likely to define how automotive factories improve productivity, quality, safety, and sustainability.

The key question is:

Can automotive manufacturers move from automation investments to autonomous manufacturing strategy before complexity overtakes capacity?

Download the Full Industrial Automation in Automotive POV