Digital Payments in Saudi Arabia: From National Infrastructure to Scalable Value Creation

Download the Full Consulting POV Now

Executive Summary

Saudi Arabia’s payments ecosystem is undergoing a structural transformation, driven byVision 2030, state-led infrastructure modernization, and rapid digital adoption across consumers and businesses. The Kingdom has moved decisively from cash and basic card payments toinstant payments, wallets, and integrated national rails, positioning payments as a core pillar of economic digitization.

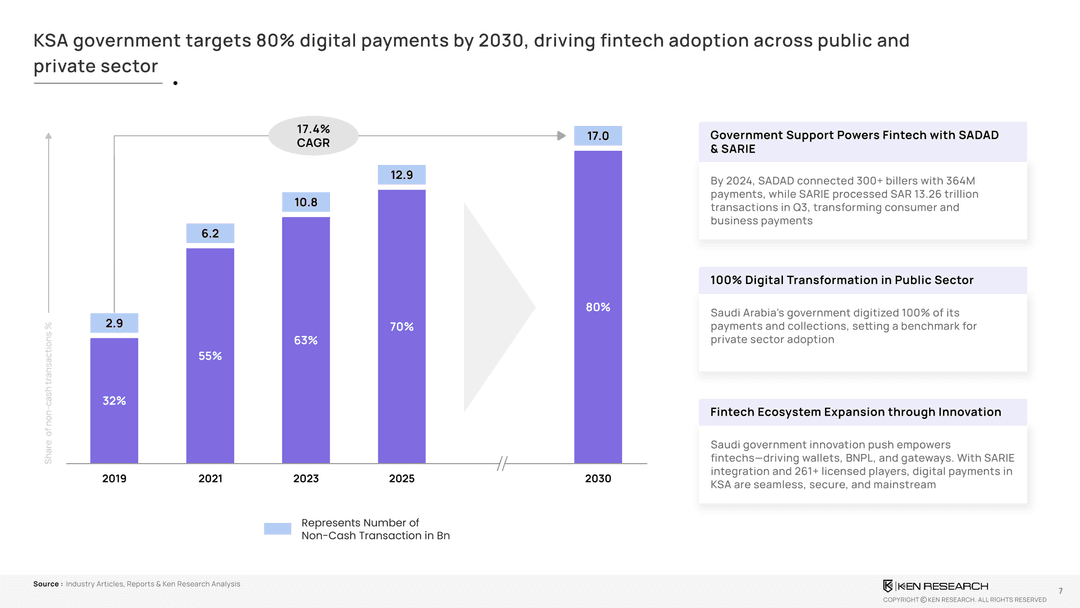

Non-cash transactions have risen from32% to 70%, with the government targeting80% cashless transactions by 2030. Total non-cash transaction volumes have expanded from2.9 billion to 17.0 billion, growing at a~17.4% CAGR, supported by POS expansion, SARIE instant payments, and wallet adoption. This POV examineswhere scale is emerging, which layers generate the most attractive economics, and how stakeholders can position themselves to capture long-term valueinSaudi Arabia digital payments economy.

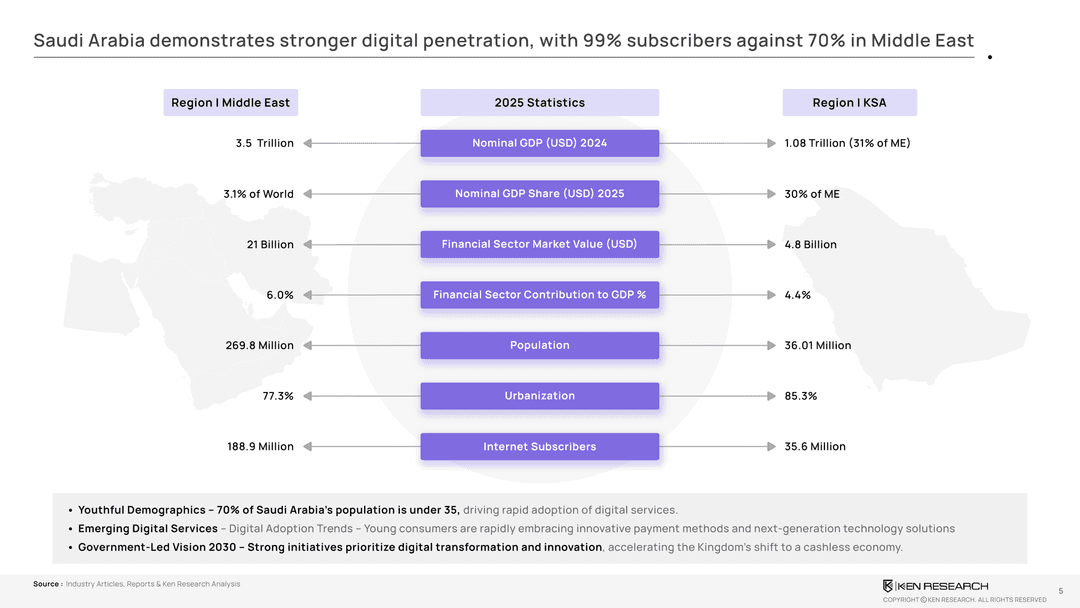

Why Saudi Arabia Is Structurally Positioned for Payment Digitization

Saudi Arabia combines demographic, digital, and policy advantages that accelerate payment adoption:

- ~70% of the population is under 35, driving rapid uptake of digital services

- Internet penetration stands at~99%, significantly higher than the Middle East average

- The financial sector contributes meaningfully to GDP, supported by strong regulatory backing

- Vision 2030 places digital payments at the center of financial inclusion and economic modernization

Compared to the broader Middle East, Saudi Arabia demonstrateshigher digital penetration, stronger policy alignment, and faster conversion from cash to digital instruments, making it one of the most attractive payment markets in the region.

Evolution of Saudi Arabia’s Payment Rails: From Cards to Real-Time Infrastructure

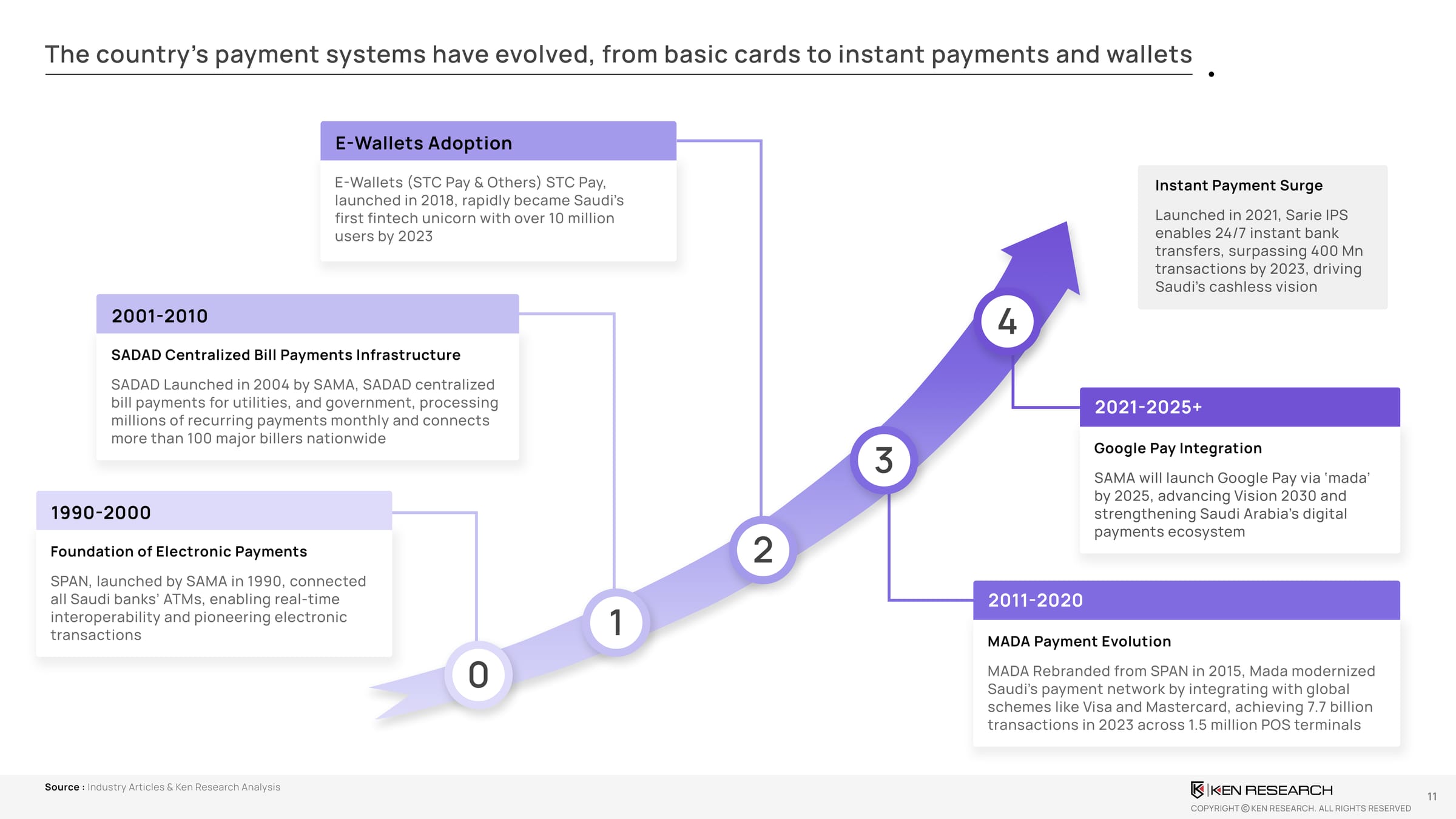

Saudi Arabia’s payment journey has beenstate-orchestrated and sequential, creating trust and scale:

- SPAN (1990):Enabled real-time ATM interoperability

- SADAD (2004):Centralized bill payments across utilities and government

- MADA (2015):Modernized card infrastructure, processing7.7 billion transactions in 2023across1.5 million POS terminals

- E-wallets (2018 onwards):STC Pay surpassed10 million users, becoming Saudi Arabia’s first fintech unicorn

- SARIE IPS (2021):Enabled 24/7 instant transfers, exceeding400 million transactions by 2023

- Google Pay via mada (by 2025):Strengthening global integration and contactless adoption

This evolution reflectspayments as national digital infrastructure, not fragmented fintech experimentation.

Adoption Momentum: Non-Cash Payments Are Becoming the Default

Saudi Arabia’s shift to digital payments is visible in bothshare and volume:

- Non-cash transactions increased from32% → 55% → 63% → 70%, with a2030 target of 80%

- Total non-cash transactions rose from2.9 billion to 17.0 billion, growing at~17.4% CAGR

- POS and card transactions dominate volumes, while SARIE drives rapid real-time payment adoption

This momentum is reinforced by government payments, consumer convenience, and merchant acceptance, making cash increasingly residual.

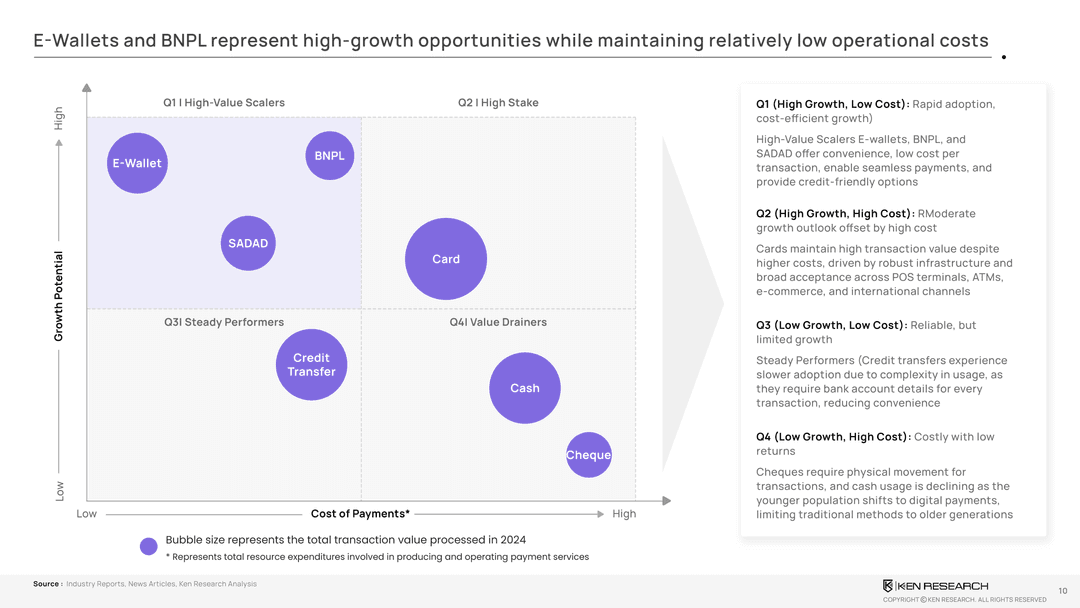

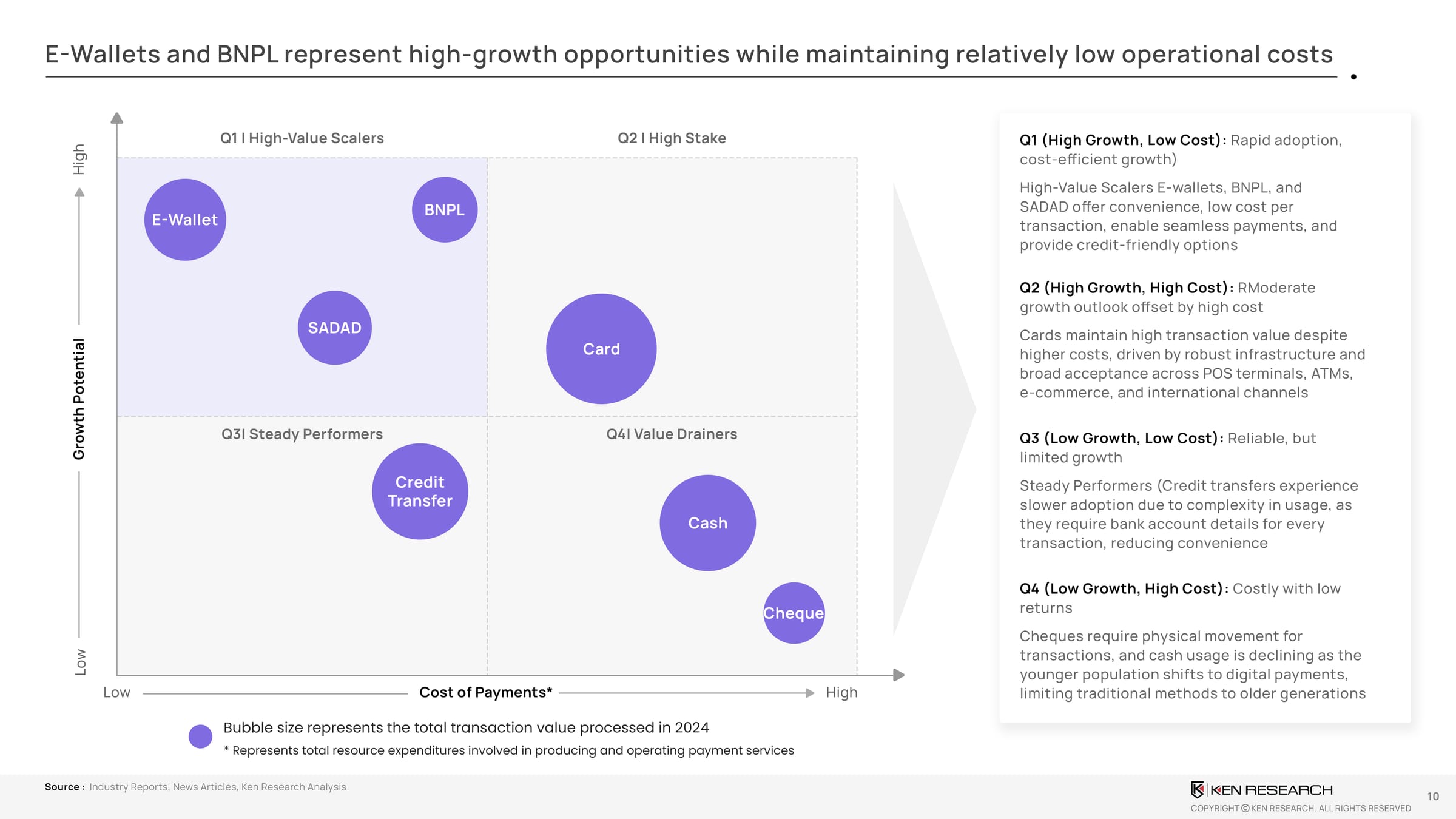

Payment Mode Economics: Growth Alone Does Not Equal Value

Different payment instruments exhibitdistinct growth–cost dynamics:

- High Growth, Low Cost (Q1):E-wallets, BNPL, and SADAD offer rapid adoption, low per-transaction costs, and scalable economics

- High Growth, High Cost (Q2):Cards maintain high transaction value but incur higher infrastructure and interchange costs

- Low Growth, Low Cost (Q3):Credit transfers remain steady but less convenient for consumers

- Low Growth, High Cost (Q4):Cheques and cash continue to decline, constrained to legacy use cases

The most attractive opportunities lie wheregrowth, cost efficiency, and user engagement intersect.

Where Value Is Being Created Across the Payment Stack

Value creation in Saudi Arabia is increasingly concentrated across specific layers:

- Government rails:Core trust and scale enablers (e.g., SADAD, SARIE)

- Consumer interaction layer:E-wallets and BNPL driving engagement and frequency

- Transaction processing:High-volume backend infrastructure

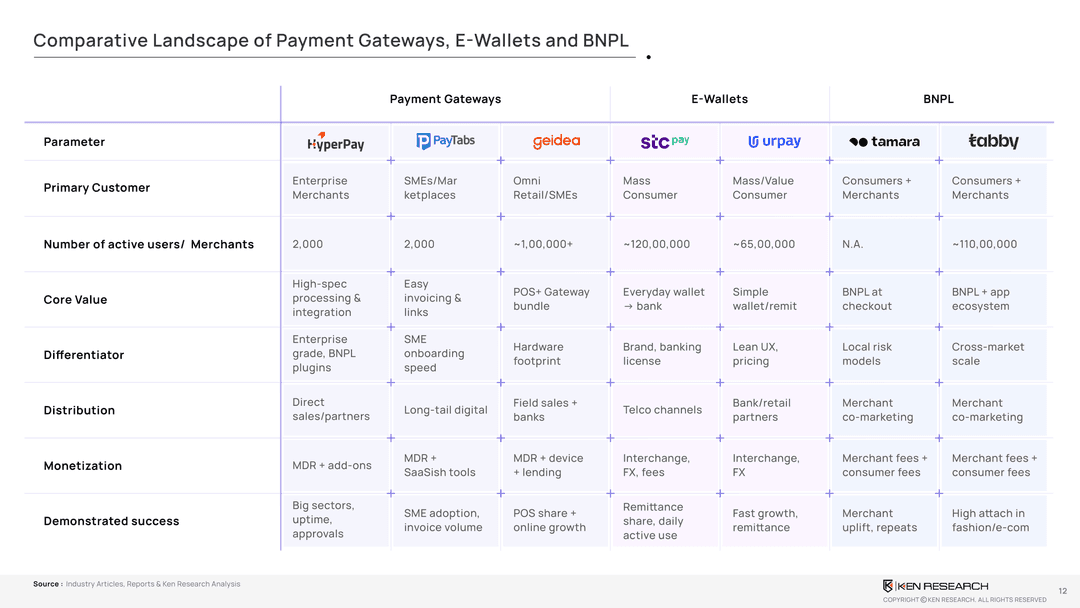

- Payment gateways:Enabling e-commerce, platforms, and SMEs

While government rails anchor the ecosystem,wallets, BNPL, and gateways represent the primary monetization layers, especially for PSPs and fintech's targeting merchants and consumers.

Forward Outlook: Payments as an Engine of Vision 2030

Saudi Arabia’s payments opportunity is expected to scale toward~SAR 25 trillion, driven by:

- Remittances and cross-border flows

- E-commerce, ride-hailing, and food delivery growth

- Open banking and real-time payments

- Expansion of wallets, BNPL, QR, and contactless solutions

Emerging fintech's such asJeelPay, Moyasar, and Arabian Payillustrate how niche, localized solutions can unlock high-growth segments within the broader ecosystem.

Strategic Imperatives for Payment Stakeholders

To capture long-term value, stakeholders must:

- Innovate beyond cards toward wallets, BNPL, and real-time use cases

- Target SMEs with cost-efficient, scalable infrastructure

- Build alliances across banks, merchants, and platforms

- Strengthen compliance, trust, and localization

- Align offerings tightly with Vision 2030 priorities

Execution discipline—not just transaction growth—will define winners in Saudi Arabia’s next phase of payment evolution.

Payments Are Becoming the Operating System of Saudi Arabia’s Digital Economy

Saudi Arabia’s digital payments journey is no longer about replacing cash—it is aboutbuilding a scalable, interoperable, and monetizable transaction backbonefor the Kingdom’s economy. As Vision 2030 accelerates adoption, stakeholders that align with national rails, optimize cost structures, and innovate at the interaction layer will shape the future of payments in Saudi Arabia.

Download the Full POV:Digital Payments in Saudi Arabia – Strategic Outlook and Opportunity Assessment