Can a 33-Kilometer Strait Decide the Future of Food Security?

The fertilizer industry has become one of the most exposed links in the global food security chain. The Middle East conflict has not only disrupted energy and shipping routes. It has also placed fertilizer supply, crop economics, planting cycles, and import-dependent food systems under immediate pressure.

Why This POV Matters Now

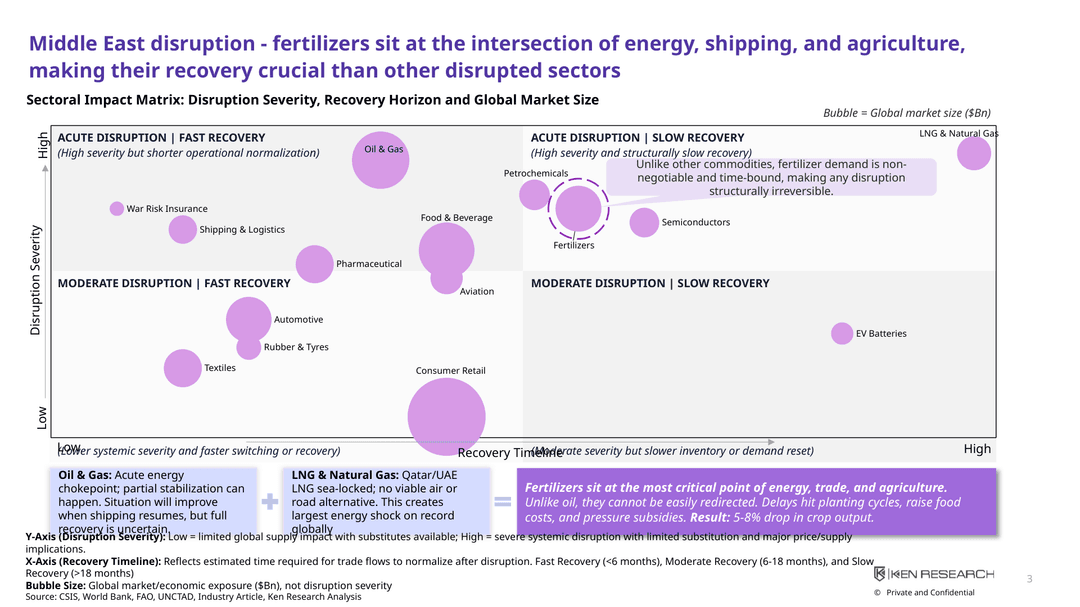

Fertilizer demand is different from most commodities. It is non-negotiable, seasonal, and directly tied to planting windows. A delayed shipment cannot always be recovered later, because the crop cycle does not wait for trade routes to normalize.

This is what makes the current disruption more serious.

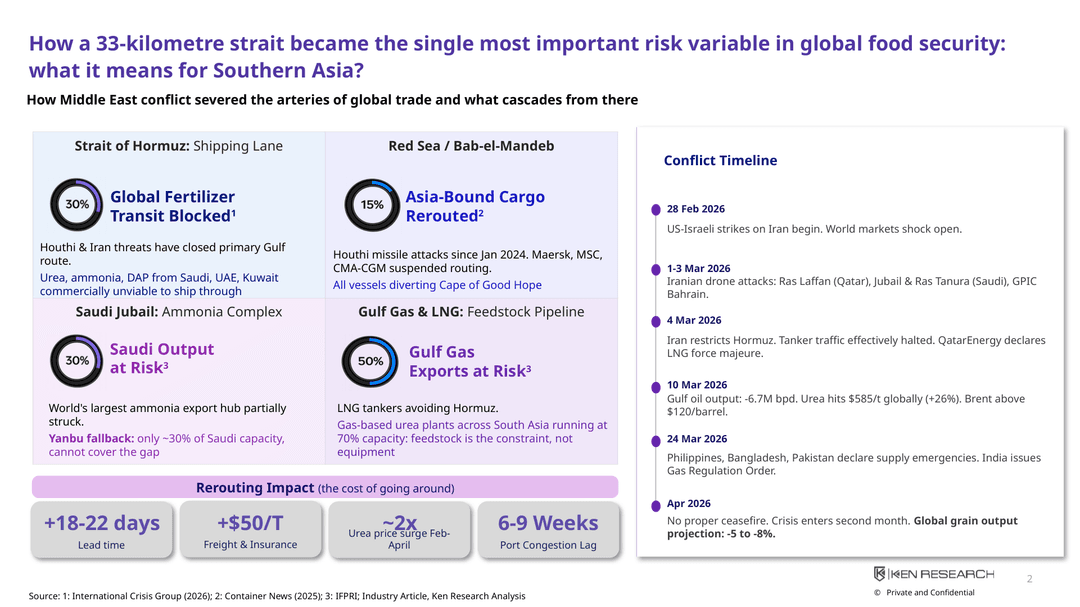

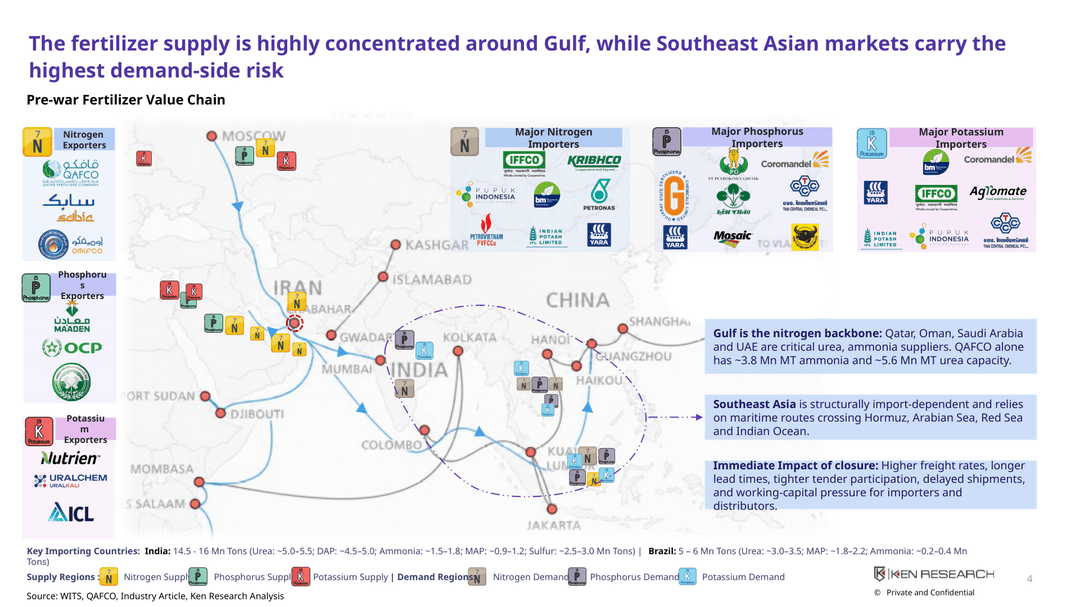

The Gulf region is deeply embedded in nitrogen fertilizer supply through urea and ammonia, while import-dependent markets across Asia face rising costs, longer lead times, tighter tender participation, and working-capital pressure. If disruption continues, the impact can move beyond price inflation into yield losses and food security risk.

Unlike oil or some industrial commodities, fertilizers cannot be easily substituted or delayed without downstream consequences.

Market Context: Fertilizer Is an Energy-Linked Food System

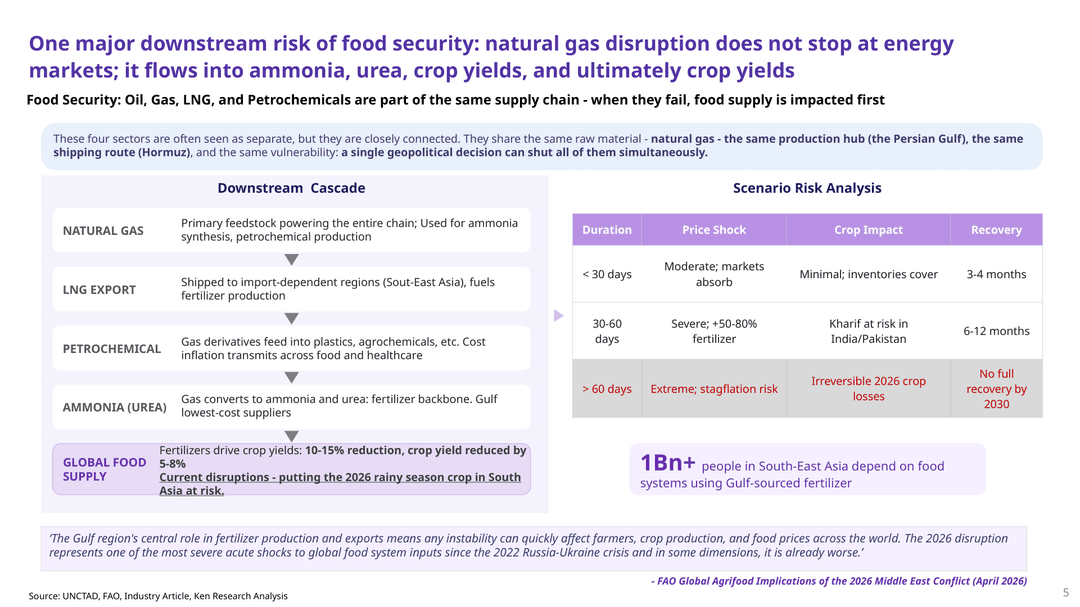

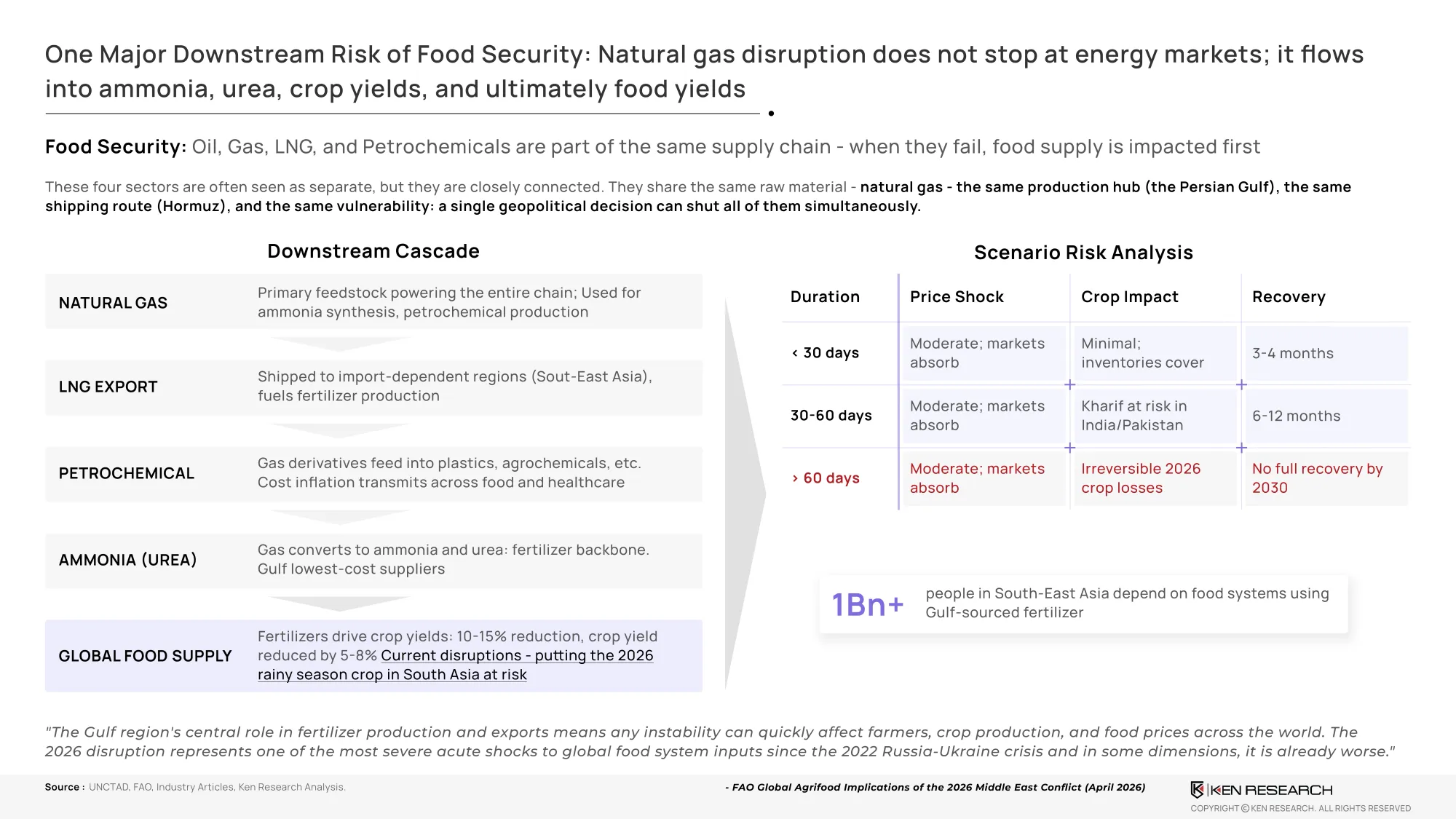

The fertilizer supply chain is closely connected to natural gas. Gas supports ammonia production, theglobal ammonia marketfeeds urea, and urea supports crop yields. When gas exports, LNG flows, ammonia production, and fertilizer shipping face disruption at the same time, the downstream impact reaches agriculture faster than many other sectors.

This POV explains why fertilizers sit at the intersection of energy, trade, agriculture, and public policy.

The disruption has created multiple stress points:

- Higher fertilizer prices and import costs

- Longer lead times due to rerouting

- Freight and insurance cost escalation

- Feedstock pressure for gas-based urea plants

- Reduced tender participation and shipment delays

- Higher subsidy burden for import-dependent governments

- Risk to planting-season availability across South Asia

What the Full POV Helps You Decode

This POV helps governments, fertilizer companies, traders, agri-input distributors, investors, and food-security stakeholders understand how geopolitical disruption moves across the fertilizer value chain.

The full POV explores:

- How the Middle East conflict disrupted key energy and fertilizer trade routes

- Why Hormuz and Red Sea exposure matters for global fertilizer movement

- How Gulf-linked urea, ammonia, sulfur, and LNG flows affect import-dependent markets

- Why India, Indonesia, Malaysia, Bangladesh, and Pakistan face different levels of exposure

- How fertilizer price shocks can move into food inflation, subsidy pressure, and crop losses

- Which alternative routes and supply sources can reduce pressure, and where they fall short

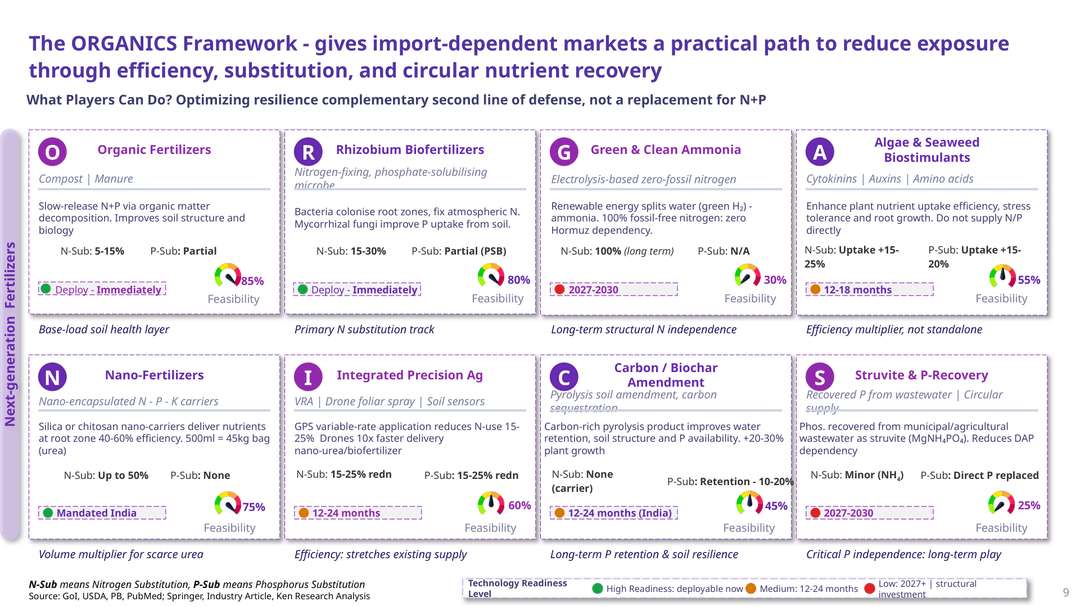

- How organic, bio, nano, green ammonia, precision agriculture, and circular nutrient recovery can support long-term resilience

The Food Security Link: From Gas Shock to Crop Risk

The crisis shows that food security is not only an agricultural issue. It is also an energy, logistics, trade, and procurement issue.

Natural gas disruption affects ammonia and urea production. Shipping disruptions delay fertilizer availability. Higher freight and insurance costs raise landed prices. Importers face tighter procurement windows. Farmers face uncertainty around input availability and affordability in thecrop protection market.

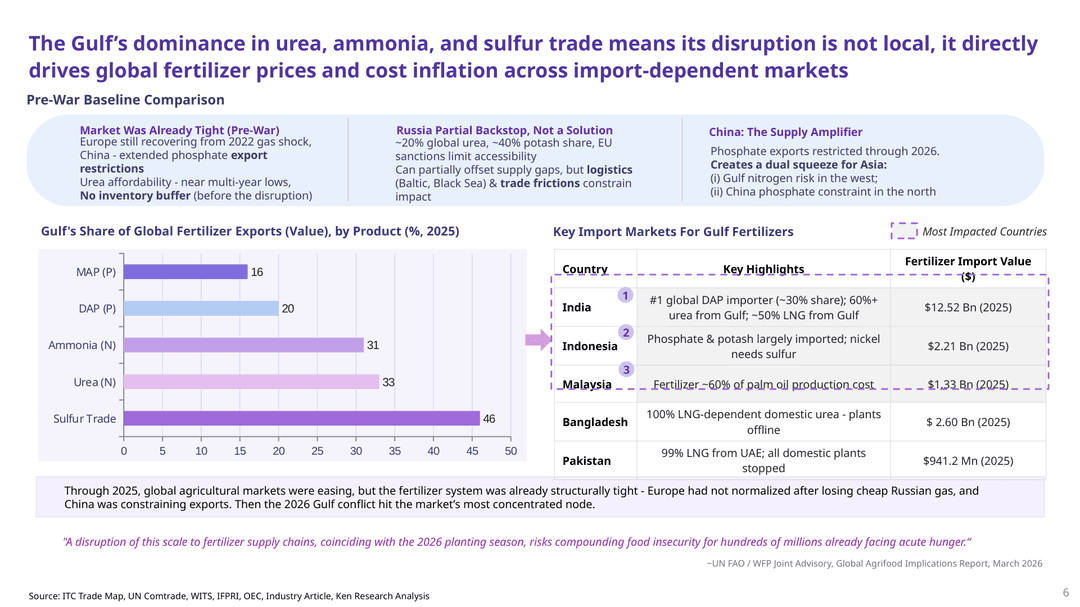

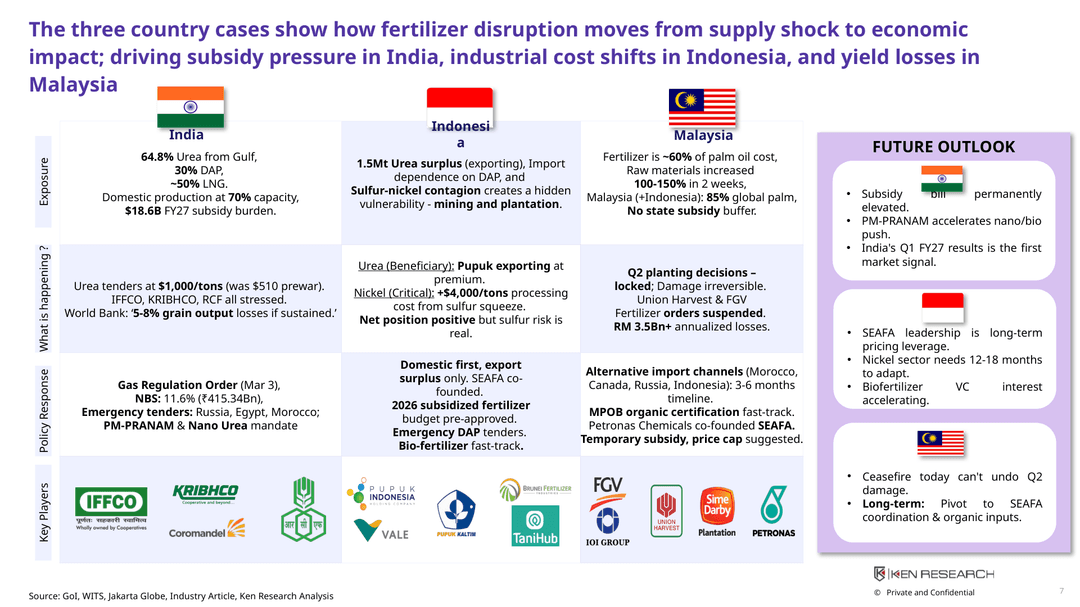

Most Exposed Markets: Import Dependence Is the Real Vulnerability

The disruption does not affect every country equally.

India faces exposure through urea, DAP, ammonia, sulfur, and LNG dependence. Bangladesh and Pakistan are vulnerable due to LNG-linked urea production and import reliance. Malaysia faces pressure because fertilizer forms a large share of palm oil production cost. Indonesia has a more mixed position, with urea surplus potential but sulfur-linked industrial risk.

The full POV compares country-level exposure, import values, policy responses, emergency procurement measures, and future outlook across key markets.

This makes the analysis useful not only for fertilizer suppliers, but also for food-security planners, agri-input companies, procurement teams, logistics providers, investors, and policymakers.

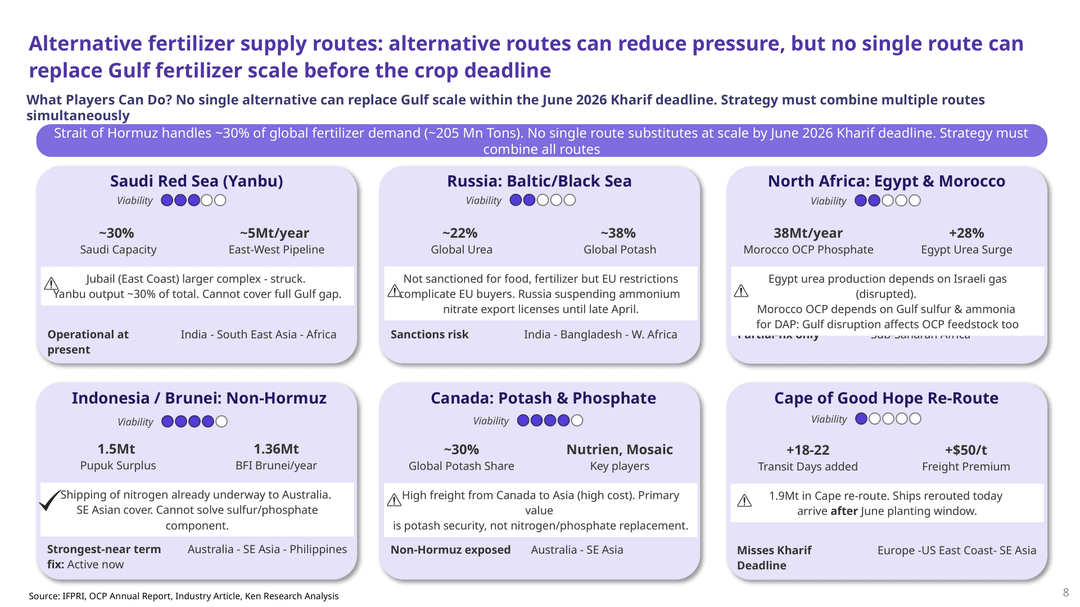

Alternative Routes Are Not Enough Without Resilience Strategy

Alternative supply routes exist, but no single route can replace Gulf fertilizer scale within urgent planting deadlines.

Saudi Red Sea capacity,Saudi Arabia green ammonia market, Russia, North Africa, Indonesia, Brunei, Canada, and Cape of Good Hope rerouting can each reduce pressure in specific ways. However, each option carries limitations linked to scale, cost, sanctions risk, timing, freight economics, feedstock exposure, or nutrient coverage.

This means the response cannot rely on one replacement route.

The full POV outlines why import-dependent markets need a combined strategy involving diversified sourcing, split shipments, strategic inventory buffers, bilateral agreements, alternative nutrient sources, and smarter fertilizer efficiency solutions.

The Strategic Question for Decision-Makers

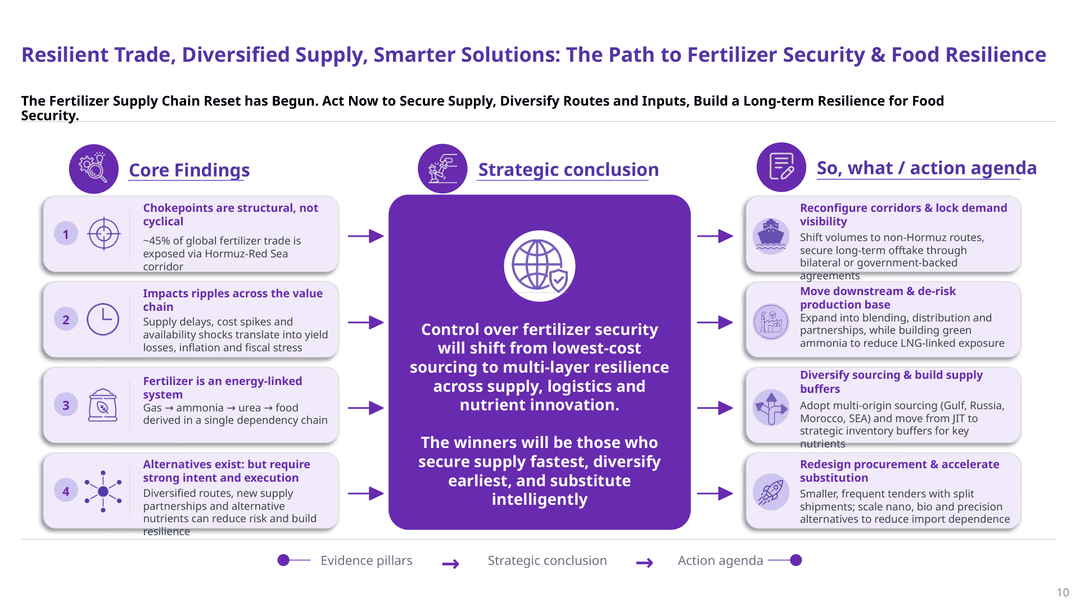

Thefertilizer supply chainreset has already begun.

The question is no longer whether geopolitical risk can disrupt fertilizer markets. It already has. The sharper question is how quickly governments, importers, traders, distributors, producers, and investors can build resilience before the next disruption hits planting cycles again.

The winners will be those who secure supply fastest, diversify earliest, and substitute intelligently.

Control over fertilizer security is shifting from lowest-cost sourcing to multi-layer resilience across supply, logistics, procurement, and nutrient innovation.