Why This POV Matters Now

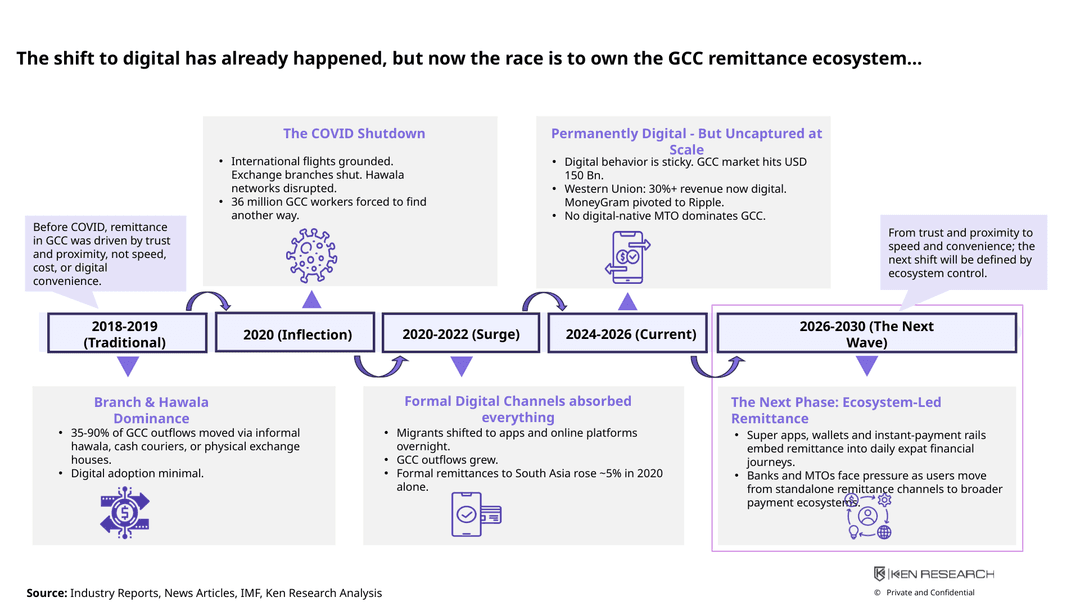

For years, GCC remittance was shaped by trust, proximity, branch access, and informal networks. COVID accelerated formal digital adoption, but the market still remains fragmented. No digital-native MTO has fully captured theGCC remittance ecosystemat scale.

That gap is important.

Banks and MTOs still hold strong payout networks and compliance capabilities, but fintechs, wallets, neobanks, and super apps are moving closer to the customer. As users shift from standalone remittance channels to everyday financial platforms, the competitive battleground is moving from transaction access to ecosystem ownership.

What the Full POV Helps You Decode

This POV helps decision-makers understand where GCC remittance value is shifting and what must be prioritized before the market becomes more consolidated.

The full POV explores:

- How GCC remittance moved from branch-led transfers to digital-first and ecosystem-led models

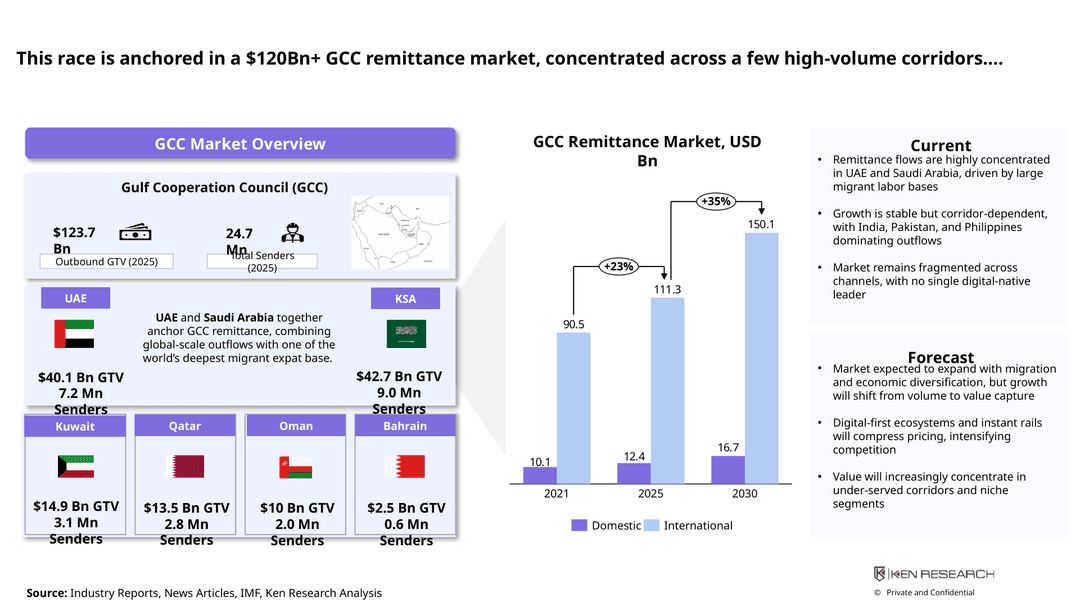

- Why UAE and Saudi Arabia continue to anchor regional outflows

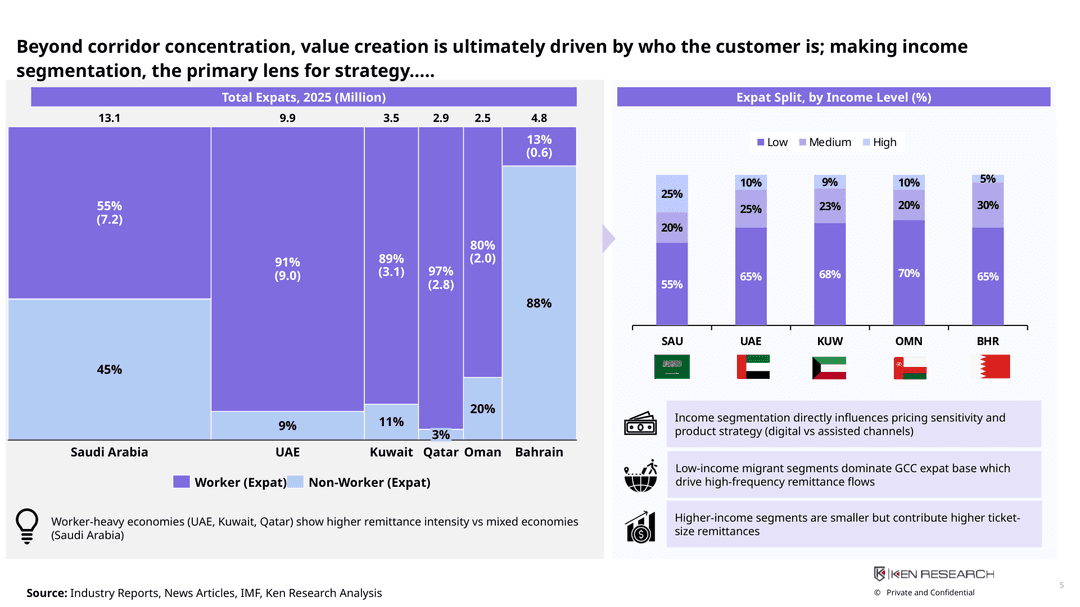

- How sender segments differ by income level, ticket size, frequency, and channel preference

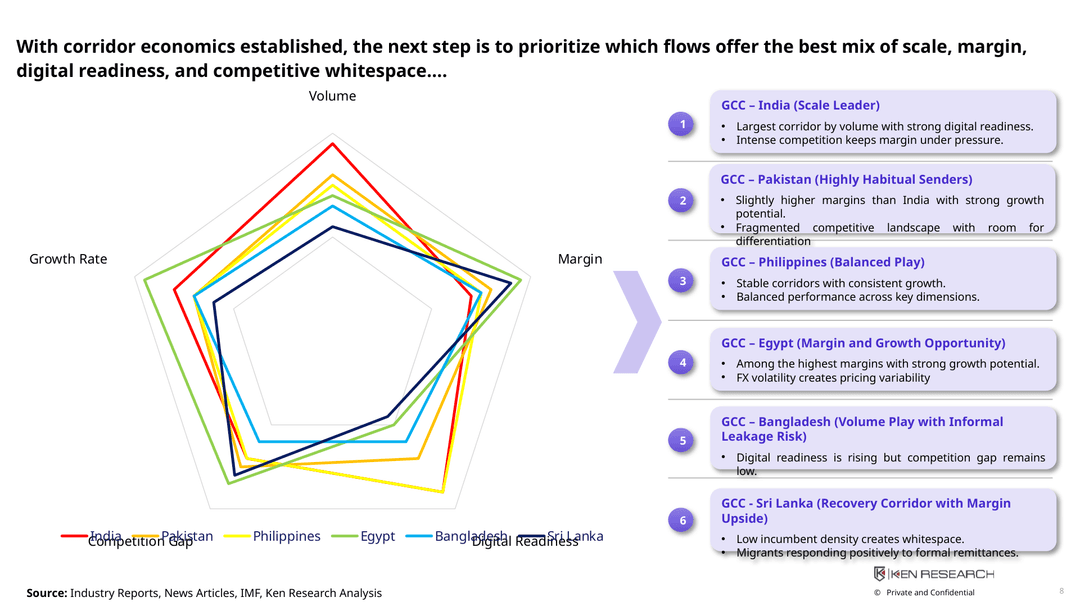

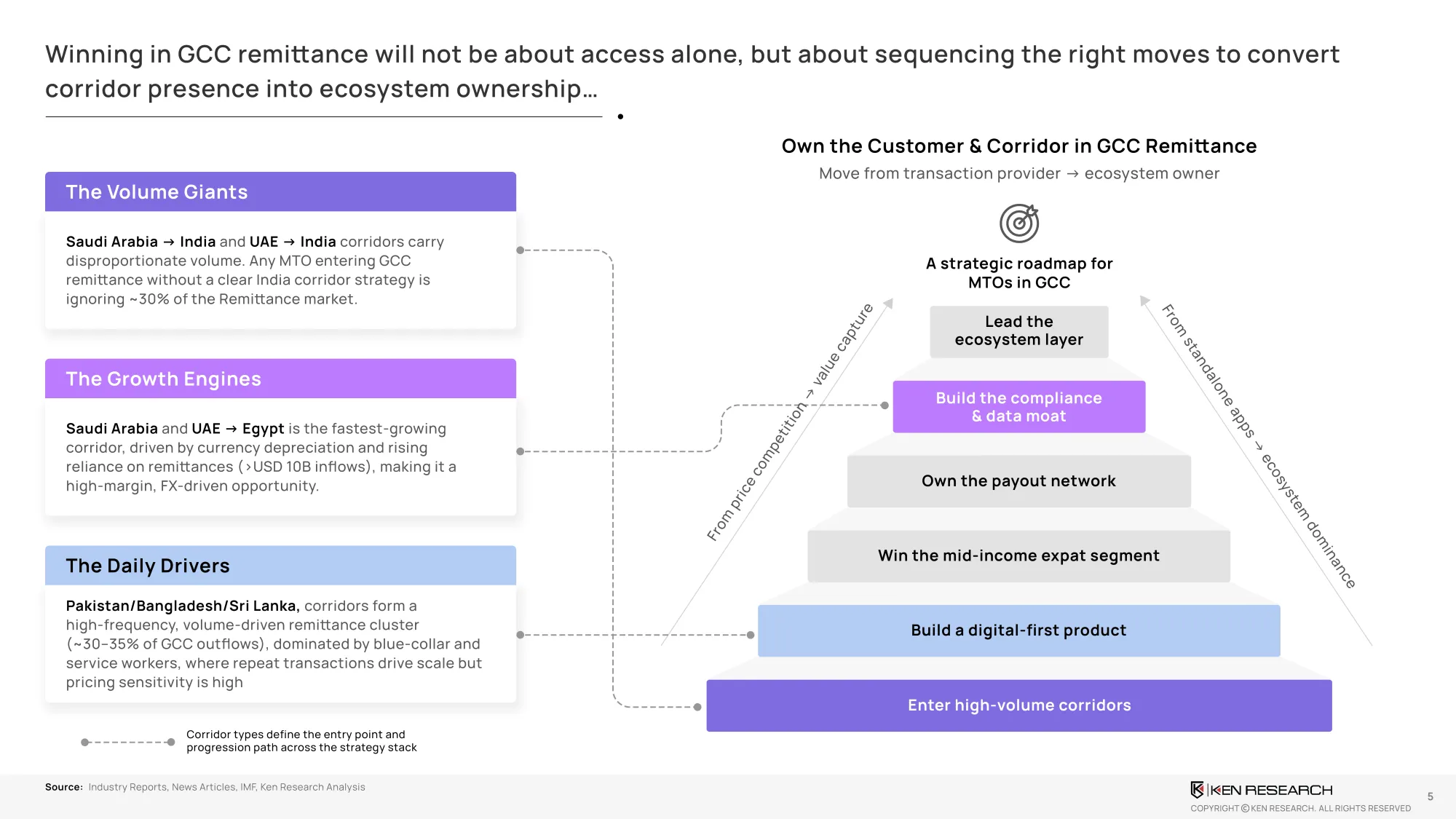

- Which corridors offer scale, margin, digital readiness, and competitive whitespace

- Why India, Pakistan, Philippines, Egypt, Bangladesh, and Sri Lanka corridors require different strategies

- How super apps, wallets, neobanks, banks, and MTOs are competing for control

- What strategic moves can help players move from transaction provider to ecosystem owner

The Real Growth Question

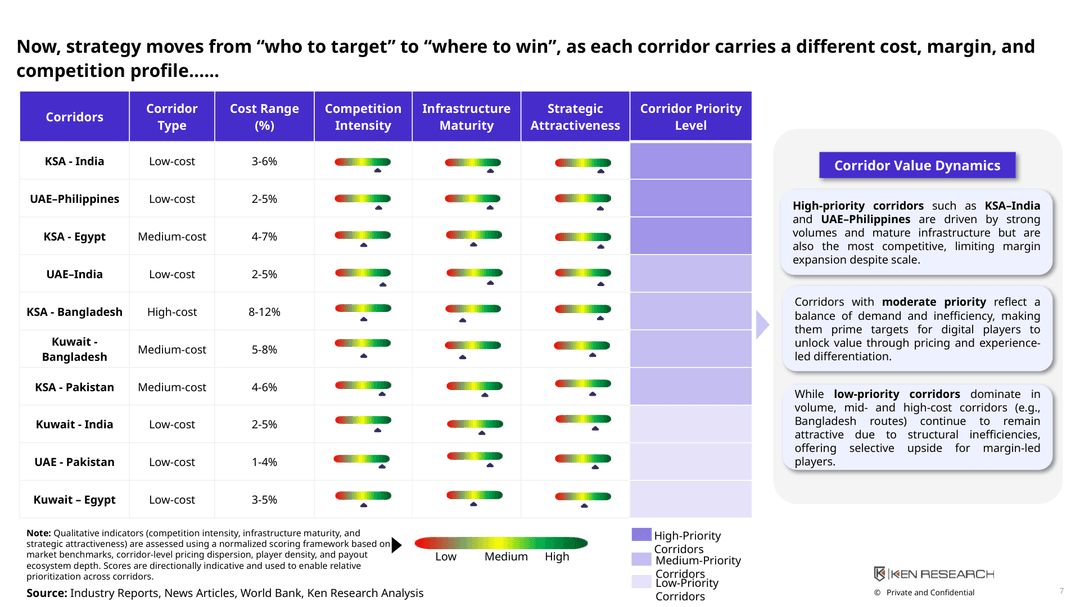

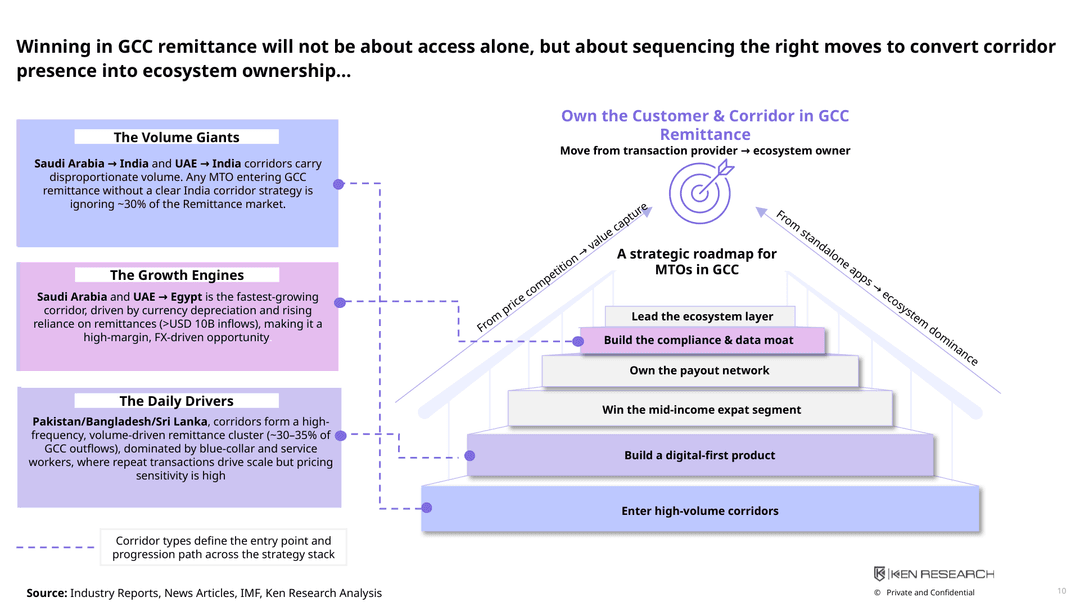

The biggest mistake in GCC remittance strategy is treating all corridors equally. A high-volume corridor is not always a high-margin opportunity. Some corridors have mature infrastructure and heavy competition, while others carry pricing inefficiencies, lower digital maturity, or underserved sender groups.

The full POV compares corridors using cost range, competitive intensity, infrastructure maturity, and strategic attractiveness. This helps identify where players should defend scale, where they should chase margin, and where digital-led differentiation can unlock new growth.

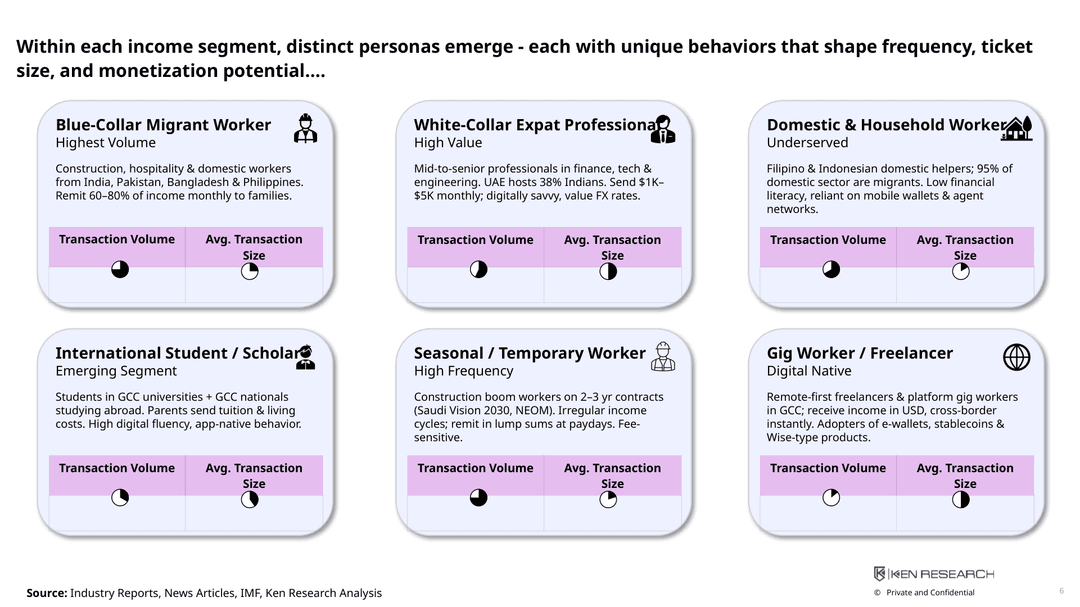

The corridor lens is especially important because remittance behavior is highly habitual. Blue-collar workers may prioritize cost and payout reliability, while white-collar expats may focus on FX transparency and app experience. Domestic workers, seasonal workers, students, and gig workers each add another layer of product complexity.

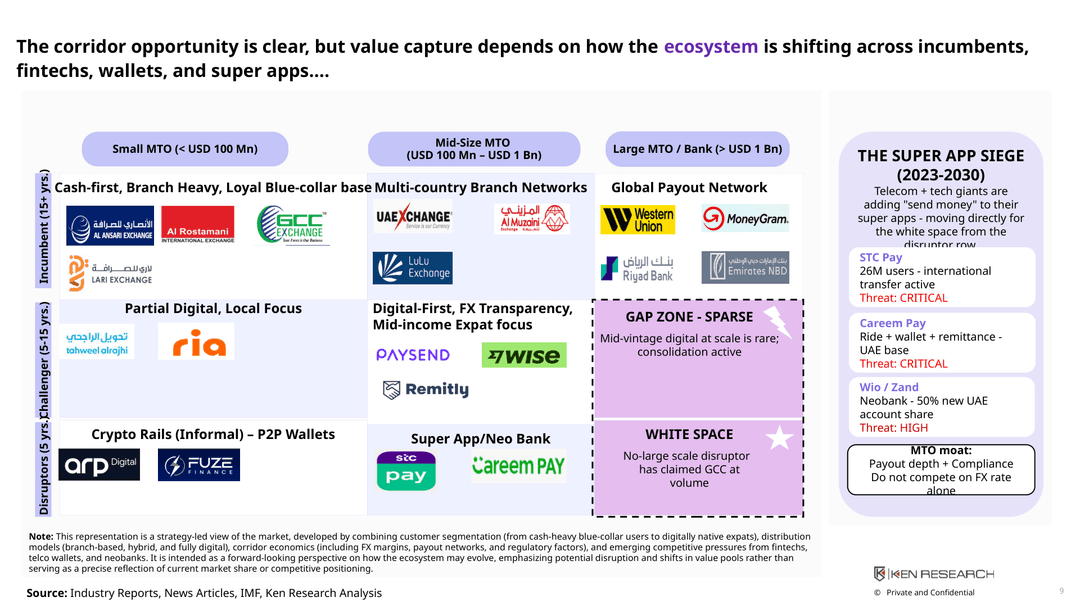

The Competitive Shift: Super Apps Are Closing In

The next disruption in GCC remittance may not come only from traditional money transfer companies. It may come from platforms that already own daily customer engagement.

Telecom wallets, super apps, and neobanks are embedding “send money” into broader financial journeys. This changes the competitive equation for banks and MTOs. If remittance becomes part of salary access, mobile wallets, ride-hailing apps, digital banking, or merchant ecosystems, standalone transaction providers could lose direct control of the sender relationship.

This is why the moat can no longer be built on FX rates alone. The stronger advantage will come from payout depth, compliance strength, data ownership, corridor intelligence, and ecosystem partnerships.

The Strategic Question for Banks, MTOs, Fintechs, and Investors

TheGCC remittance marketis mature in size but not yet mature in ownership.

For banks and MTOs, the priority is to defend trust while becoming more digitally relevant. For fintechs and wallets, the opportunity is to target underserved corridors and customer segments with better pricing, experience, and speed. For investors, the key is to identify platforms that can move beyond transaction volume and build corridor-led, compliance-backed, ecosystem-scale models.

The full POV gives a structured view of where to play, how to price, which corridors to prioritize, and how the competitive landscape may evolve as ecosystem players move deeper into cross-border transfers.

Download the Full GCC Remittance Market POV