Global Capability Centres in India: From Offshore Scale to Global Command Centres

Download the Full Consulting POV NowExecutive Summary

India has emerged as theundisputed global hub for Global Capability Centres (GCCs). The country hosts1,900+ GCCs, accounting for~59% of the world’s total GCC base, supported by atalent pool of ~2 million professionals. This scale positions India not merely as an offshore delivery location, but as acore operating backbone for global enterprises.

Over the last decade, India’s GCC ecosystem has transitioned fromcost-focused shared servicestostrategic, transformation-led global hubs. GCC revenues expanded fromUSD 11.5 billion in FY’10 to USD 46.1 billion in FY’23, while installed GCC talent grew from~4 lakh to ~17 lakh professionals. With accelerating new setups, rising global leadership roles, and proactive state-level policy initiatives, India is entering the next phase of GCC evolution—from scale-driven expansion to strategic control and global accountability.

The Structural Shift: From Cost Arbitrage to Capability Leadership

India’s GCC journey has evolved through four clearly defined phases:

- GCC 1.0 (till 2010):Cost-driven IT support and back-office operations

- GCC 2.0 (2011–2015):Expansion of shared services and operational efficiency

- GCC 3.0 (2015–2023):Value-driven portfolio hubs focused on digital, analytics, and engineering

- GCC 4.0 (2023 onwards):Transformation-led centres anchored inAI, cybersecurity, cloud platforms, product engineering, and multifunctional global mandates

This evolution is reflected in outcomes:

- GCC headcount expanded~5x between 2010 and 2025

- GCC revenues increased~6x over the same period

- India is now entrusted withcore enterprise functions, not peripheral support roles

GCCs are increasingly structured asintegrated global organizations, functioning assecond headquartersrather than offshore delivery arms.

Download the GCC Evolution Timeline & Capability Shift Framework

Why the Last Three Years Mark a Clear Inflection Point

Recent growth reflects aquality-led shift, not just volume expansion:

- New GCC setupsdoubled in three years, increasing from65 in 2022 to 136 in 2024

- InCY’24,28% of new GCC entrantswere backed by parent firms with revenues exceedingINR 2.1 trillion

- These entrants are increasingly focused on:

This trend signals thatlarge global enterprises are relocating innovation ownership and strategic control to India, rather than merely scaling delivery capacity.

India Is No Longer Just Executing—It Is Leading

Leadership roles anchored in India have expanded rapidly:

- Global roles based out of India have grown at a~35.6% CAGR over the last six years

- India-based leaders now occupy positions such as:

Beyond IT and engineering, critical functions now anchored from India include:

- Product management

- Shared services and operations

- Finance, HR, and enterprise-wide support functions

Inclusivity has also improved meaningfully, withwomen accounting for 29.0% of global roles in FY’25, up from16.9% in FY’24. This reflects India’s growing contribution not just in scale, but also ininclusive global leadership.

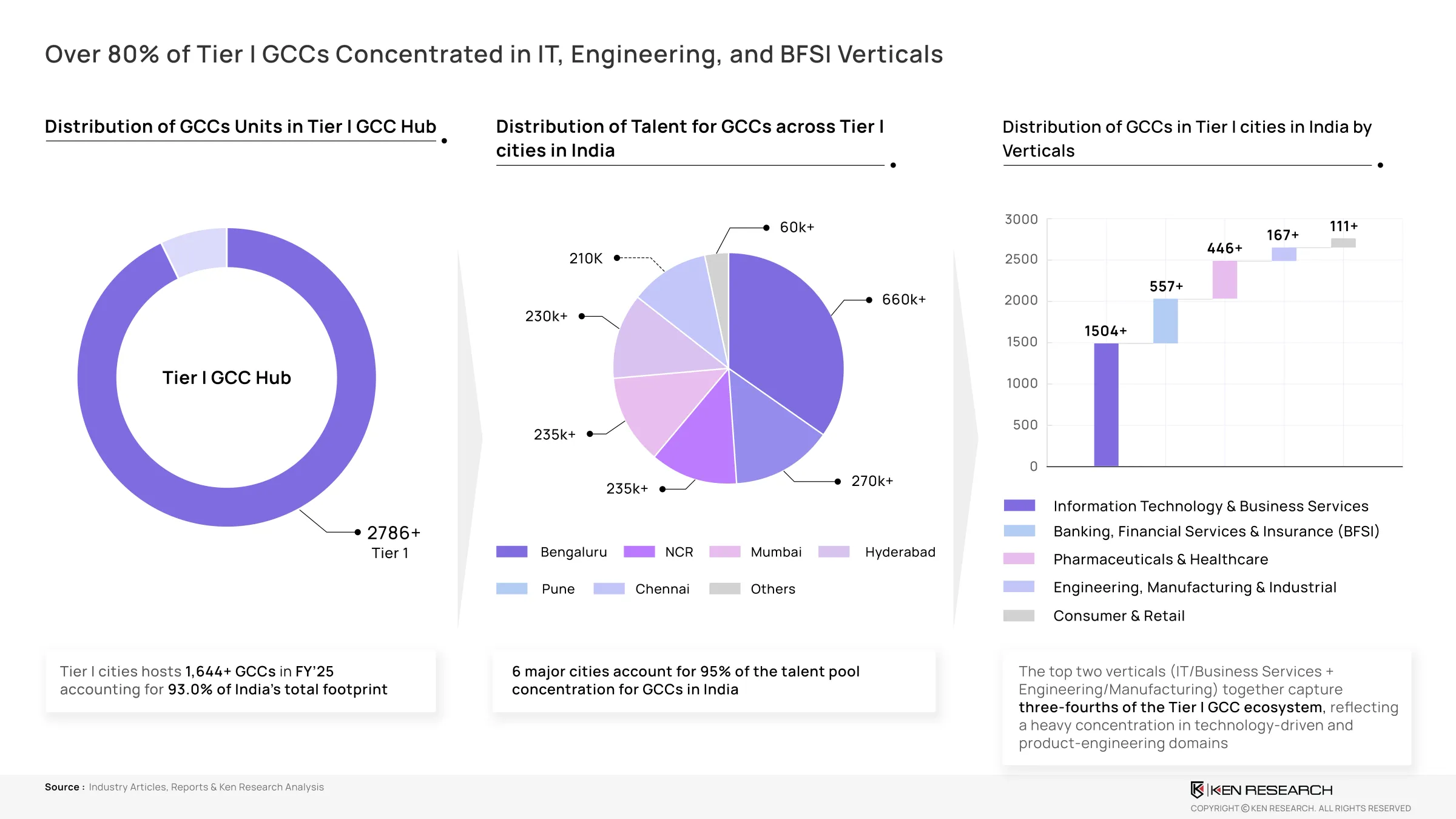

Location Strategy: Why Tier-I Cities Still Dominate

Despite cost pressures, Tier-I cities remain central to India’s GCC ecosystem:

- 92% of India’s GCC unitsare located in Tier-I hubs

- Bengaluru alone hosts ~30% of all GCCs in India

InCY’24:

- Bengaluru accounted for~46% of India’s total notable GCC leasing

- 11.9 million sq. ft.was leased—more than the combined total ofHyderabad, Chennai, and Pune

- IT-BPMdrove the largest share of leasing activity at9.1 million sq. ft.

Nearly47% of India’s GCC IT workforceis concentrated inBengaluru and NCR, underscoring the continued importance of talent density, leadership availability, and ecosystem maturity over pure cost arbitrage.

Sector Focus: Where India’s Capability Advantage Is Deepest

India’s GCC ecosystem is concentrated in high-value verticals:

- Over 80% of Tier-I GCCsoperate across:

City-level specialization is also evident:

- Hyderabad and NCRhave emerged as ER&D hotspots, jointly hosting a significant share of India’s ER&D GCC talent

- Chennaihas become a preferred hub for automotive and industrial GCCs, with~13% of India’s automotive-focused GCC talentbased there

This concentration reinforces India’s position as aglobal capability specialist, rather than a generalized services destination.

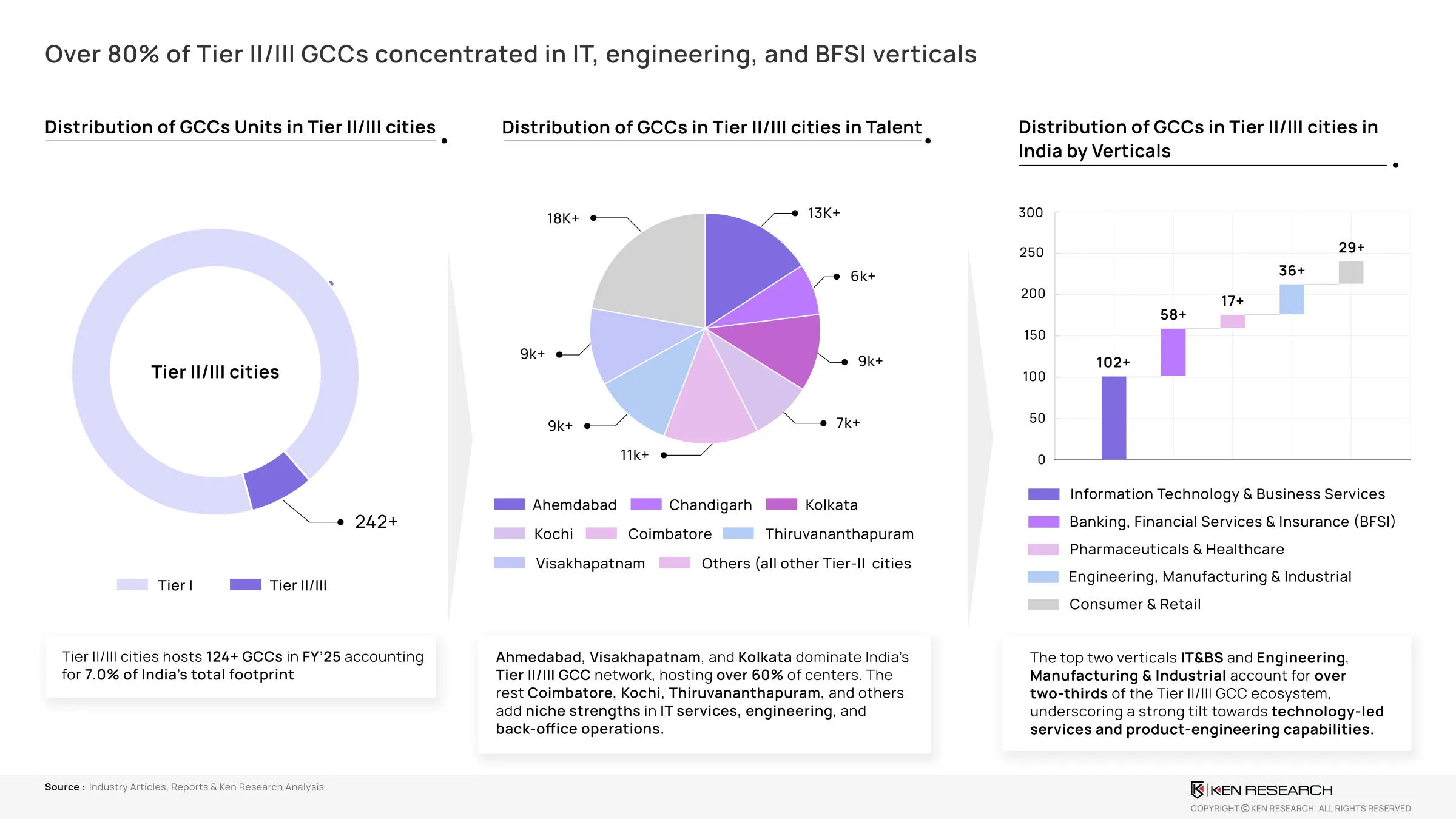

Tier-II and Tier-III Cities: The Next Layer of Expansion

Tier-II and Tier-III cities currently account for~7–8% of India’s GCC footprint:

- 124+ GCCsoperate in these cities as of FY’25

- Over 60%of Tier-II/III GCCs are concentrated in:

Key insights from the PPT:

- Ahmedabadleads in talent availability (4.3–5.0 million professionals)

- Trivandrumcommands the highest rents among Tier-II/III hubs (INR 55–65 per sq. ft. per month)

- GCC activity in these cities remains concentrated inIT, engineering, and BFSI, accounting for over two-thirds of the Tier-II/III ecosystem

Tier-II/III locations are best positioned ascomplementary extensions, supporting specific functions rather than replacing Tier-I hubs.

Policy Is Now a Competitive Differentiator

State governments are actively shaping GCC location decisions :

- Karnataka

- Gujarat

- Tamil Nadu, Andhra Pradesh, Madhya Pradesh

Policy support has moved from facilitative tostrategically competitive, accelerating India’s GCC expansion.

Strategic Imperatives for Global Enterprises

To succeed in India’s evolving GCC landscape, enterprises must:

- Design GCCs asglobal mandate owners, not support units

- Balance scale with specialization and leadership depth

- Align location strategy with talent density, ecosystem maturity, and policy incentives

- Invest in transformation capabilities acrossAI, cloud, cybersecurity, and ER&D

- Build long-term operating models, not transactional centers.

Execution quality, not just scale, will define the next generation of GCC leaders.

India Is Becoming the Global Control Tower for Enterprise Capability

India’s GCC ecosystem has crossed a strategic threshold. With unmatched scale, rising leadership ownership, deep talent pools, and proactive policy backing, India is no longer just the preferred offshore destination, it is theglobal command centre for enterprise capability and innovation.

The next phase of GCC growth will be defined bywho uses India to execute strategy, and who uses India to shape it.