Decoding Digital Spend of India’s 75 million SMBs: Where Adoption Ends and Monetisation Begins

Download the Full Consulting POV NowExecutive Summary

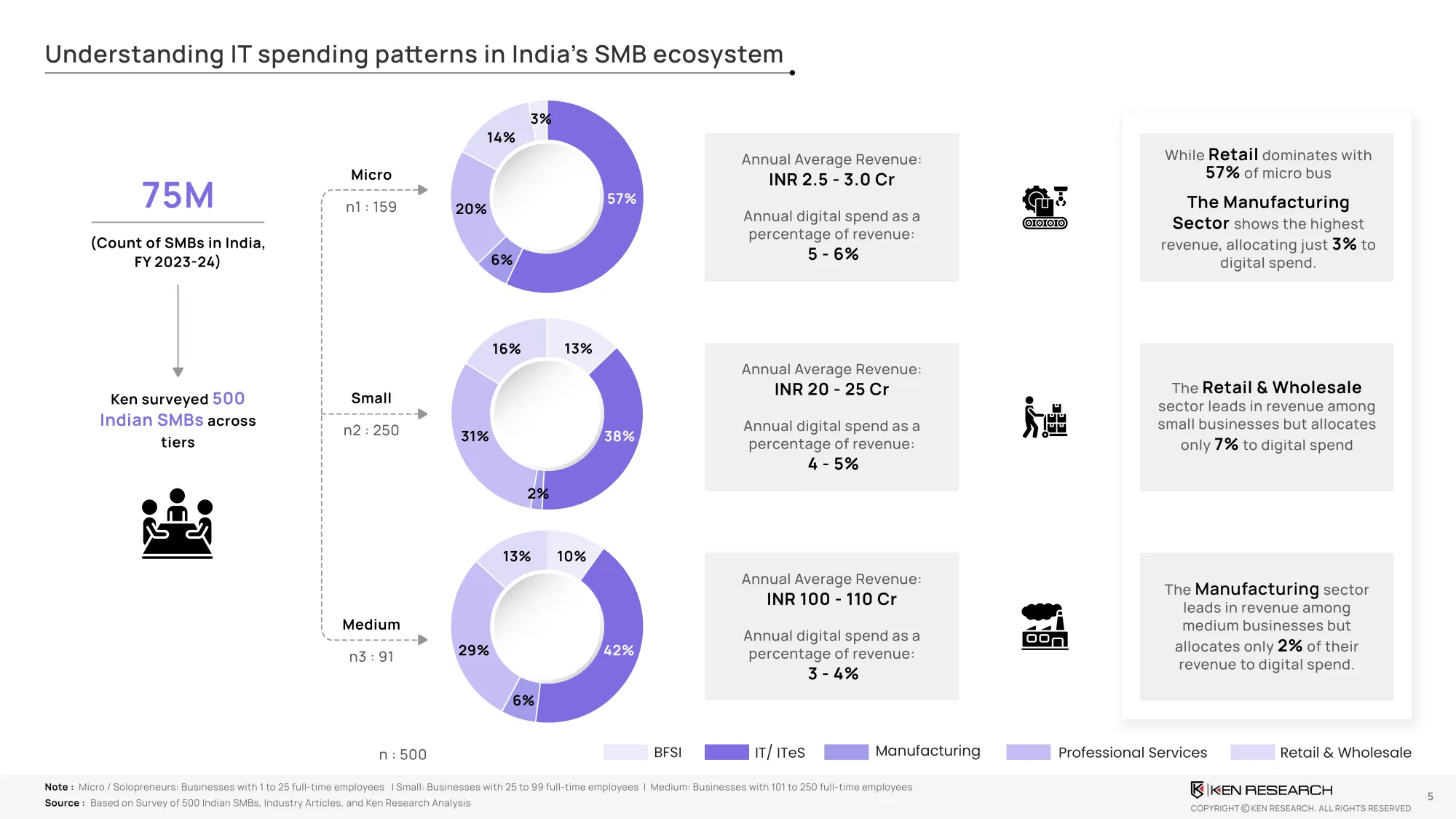

India is home to nearly75 million small and medium businesses, yet their digital spending behaviour remains widely misunderstood. While digital adoption is often described as widespread, the underlying spend data tells a more selective story. Indian SMBs are digitally connected, butnot uniformly digitised, with technology investments tightly aligned to immediate operational value.

Based on a survey of500 SMBs across micro, small, and medium segments, this POV decodes how much SMBs spend on digital tools, how spending evolves with scale, and where monetisable opportunities realistically exist. The data shows that whileabsolute digital spend rises sharply with scale,digital spend as a percentage of revenue declines, signalling disciplined, ROI-driven purchasing behaviour.

How Much Do Indian SMBs Actually Spend on Digital?

Digital spending varies materially by enterprise size.Micro SMBs (1–25 employees)generate revenues ofINR 2.5–3.0 croreand allocate5–6% of revenueto digital tools, largely restricted to essential connectivity and productivity solutions.Small SMBs (25–99 employees), with revenues ofINR 20–25 crore, spend4–5%, reflecting a transition phase where digital investments begin to expand selectively.Medium SMBs (101–250 employees)generateINR 100–110 crorein revenue but restrict digital spend to3–4%, despite significantly higher absolute budgets.

This pattern highlights a critical insight:digital maturity increases with scale, but spending discipline strengthens even faster.

Revenue Leadership Does Not Equal Digital Intensity

Sector-wise analysis reveals thathigh revenue does not automatically translate into high digital intensity.Manufacturing SMBs, despite strong topline performance, allocate just2–3% of revenueto digital tools. Meanwhile,retail and wholesale businesses, which dominate the micro and small SMB universe, demonstrate higher relative digital adoption despite lower absolute revenues.

This divergence underscores thatdigital spend is driven by visibility and immediacy of impact, not revenue scale alone.

The Tech Iceberg: How SMBs Digitise in Layers

SMB digital adoption follows a layered structure best described as aTech Iceberg. At the visible top are technologies such as connectivity, productivity software, and payments—solutions that are easy to deploy and deliver immediate benefits. Beneath the surface lieCRM, marketing tools, hosting, and basic security, where adoption increases meaningfully only among small and medium enterprises. At the deepest layer areERP systems, cloud infrastructure, project management, and advanced HR tools, largely restricted to medium-scale SMBs.

The key implication is thatmost SMBs are digitally enabled but not digitally integrated.

What SMBs Actually Pay For: Spend Reality by Solution Type

Spending behaviour across solution categories reflects pragmatic decision-making.ERP systemsare largely adopted by medium SMBs, with annual spends ofINR 3.0–3.5 lakh.CRM and marketing toolssee limited adoption among micro enterprises, with spend rising from~INR 1.0–1.1 lakhfor small businesses to~INR 3.5–3.6 lakhfor medium firms.

Connectivity remains foundational, with micro SMBs spendingINR 5,000–7,000 annually, while medium enterprises spendINR 3–4 lakh.Cloud hosting, atINR 8–10 lakh annually, is almost exclusively a medium-enterprise investment.Cybersecurity spendincreases fromINR 30,000–35,000for small SMBs toINR 65,000–70,000for medium firms.

Across categories, SMBs consistently investonly where value is immediate and operationally visible.

The Spend Curve: Selective Acceleration, Not Uniform Growth

The spend curve analysis dismantles the assumption of uniform digital growth.Micro SMB spending remains largely flat, constrained by affordability and limited complexity.Small SMBs show selective acceleration, particularly in CRM, marketing, and connectivity.Medium SMBs demonstrate sharp spend escalation, especially in cloud, project management, security, and productivity tools.

This confirms that SMBs arenot under-digitised due to lack of awareness, but rathersequencing adoption based on readiness and ROI.

Where the Monetizable Opportunity Actually Lies

The real opportunity is not in pushing enterprise-grade technology across all 75 million SMBs. Instead, value lies insegment-specific monetisation strategies. Micro SMBs respond to affordable, bundled, subscription-led tools. Small SMBs represent the inflection segment, where modular upgrades unlock incremental spend. Medium SMBs—with enterprise-like complexity—represent the largest monetisation pool for cloud, ERP, security, and AI-enabled platforms.

The data makes one point clear:the next phase of SMB digital growth in India is about monetisation discipline, not adoption evangelism.

Strategic Implication

India SMB technology marketis not a volume play—it is aprecision play. Vendors and investors that align product depth, pricing, and packaging to SMB scale will capture disproportionate value. Those that assume uniform readiness across the SMB universe will face low conversion and high churn.

Download the Full POV:Decoding Digital Spend of India’s 75 million SMBs