Australia Logistics Market 2025: From Regional Hubs to National Advantage in a AUD 39 Billion Freight Economy

Ken Research

October 28, 2025 - 4 min read

October 28, 2025

by Khushi RastogiAustralia’s freight backbone is vast, integrated, and increasingly data driven. In 2023–24, the network moved approximately 249 billion tonne-km by road, 448 billion tonne-km by rail, 88 billion tonne-km by coastal shipping, and 0.2 billion tonne-km by air. Government road investments reached AUD 39 billion in 2022–23, reflecting the sector’s scale and national importance.

At the policy level, the National Freight and Supply Chain Strategy is guiding this expansion, focusing on safety, resilience, and multi-modal efficiency as freight demand climbs toward 2050. As freight demand is projected to grow by 35–40 % by 2050, current investments signal long-term recalibration.

However, capacity growth is uneven across states. Industrial vacancy remains tight around 2.5 % nationally, which keeps rents high and accelerates brownfield optimisation near major cities.In this context, Australia’s logistics system is evolving from a national network into a constellation of regional strengths, each with distinct roles and advantages.

Against this backdrop, Australia’s logistics map divides into regional power corridors, each optimising a distinct role.

East Coast Consumer Corridor (NSW, Victoria, Queensland)

The Eastern Seaboard forms the country’s primary consumption and import zone, handling roughly 70 % of domestic freight. It connects dense urban markets with coastal ports and inland intermodals, underpinning both consumer and e-commerce supply chains.

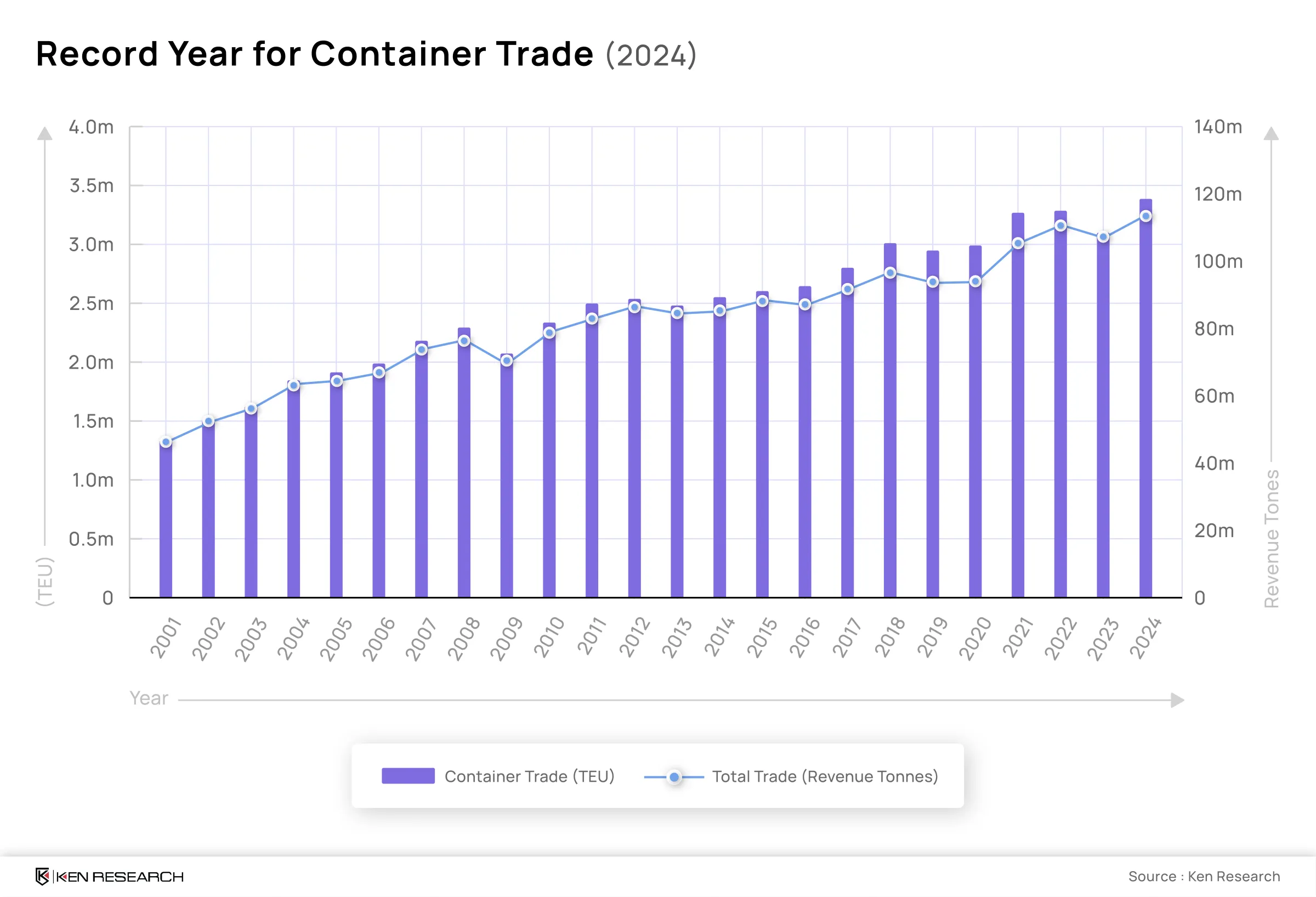

At the core, Port of Melbourne handled a record 3.396 million TEU in 2024—a 2.4 % year-on-year increase supported by stronger agri-export volumes. Melbourne’s western corridor continues to expand, offering new distribution capacity for retail and FMCG players.

Further north, Port Botany processes nearly 2.8 million TEU annually, representing 99.6 % of NSW container throughput. With design capacity beyond 7 million TEU, it anchors metropolitan logistics growth. Road freight activity increased to 86 billion tonne-km in 2023–24, reinforcing the dominance of road in metro distribution.

Crucially, infrastructure such as the Inland Rail Project is reshaping this corridor—creating 7,600 jobs and AUD 570 million in regional contracts. Once complete, it will connect ports, warehouses, and inland hubs faster and more sustainably.

Together, these developments show that East Coast logistics are moving from capacity-driven growth to productivity-led performance a shift mirrored across the country.

West: Resources Super-Corridor (Pilbara & WA Export Chain)

Moving westward, Western Australia remains the backbone of Australia’s export economy. Its logistics infrastructure is built around iron ore, LNG, and critical minerals, carried predominantly by heavy-haul rail and serviced through deepwater ports.

The Pilbara Ports Authority achieved record throughput of 775.7 million tonnes in FY 2024–25, a milestone that underscores operational efficiency and export resilience.

Moreover, WA’s logistics providers are prioritising digital fleet management and low-carbon transport, as the sector shifts toward sustainability and automation. Rail’s share of the national freight task, 448 billion tonne-km, owes much to these Western export corridors.

In parallel, new container capacity proposals in Queensland highlight the push to diversify export gateways and reduce east-coast congestion, demonstrating how regional innovation supports national resilience.

Hence, Western Australia’s logistics network is not just resource-focused — it’s setting the benchmark for digitalisation and decarbonisation in bulk logistics.

North & Centre: Gateways, Defence, and Agrifood

Transitioning north, Darwin and the Northern Corridor are evolving into Australia’s strategic Indo-Pacific gateway. The area blends defence logistics, LNG export operations, and agri-food cold chains, creating an intermodal platform for regional trade.

Investment in multimodal terminals and temperature-controlled storage supports perishable exports while enhancing resilience against climate and supply disruptions. These assets also strengthen links with northern Asia’s growing food demand.

Meanwhile, central nodes such as Alice Springs and South Australian intermodals connect inland resource and farming zones to ports. The rise of cross-dock microhubs and hybrid line-haul/final-mile models reflects an adaptive response to Australia’s geographic dispersion.

The Northern and Central regions, therefore, represent the logistics frontier — smaller in scale but pivotal in resilience, connectivity, and trade diversification.

Technology & Sustainability: Efficiency Is the Margin

Across all regions, the next efficiency wave is digital as Operators are investing in AI route optimisation, IoT fleet telemetry, and automated warehouse systems to streamline operations and reduce idle time.

Sustainability is gaining commercial traction as Trials of electric and hydrogen-powered trucks in Victoria and NSW, along with solar-integrated logistics parks, are lowering costs and aligning with Australia’s 2030 decarbonisation goals.

As land scarcity limits new builds, brownfield retrofits, mezzanines, rooftop solar, and automated yard flows offer faster ROI than greenfield expansion. This trend keeps logistics competitive despite high construction and fuel costs. Technology and sustainability now serve as the twin levers of margin protection, improving reliability while reducing environmental and operational risk.

Risks and Outlook: Resilience Remains Regional

Despite progress, systemic challenges remain. Driver shortages, fuel-price volatility, east-coast congestion, and extreme weather continue to test logistics continuity.

The ongoing rollout of the National Freight and Supply Chain Strategy and the staged delivery of Inland Rail will be key to relieving these pressures. Their success will determine whether logistics performance keeps pace with economic and population growth.

Ultimately, the next phase of competitiveness will rely on how seamlessly Australia’s regional networks interconnect enabling national efficiency through local strength.

Conclusion: From Regional Strength to National Advantage

Australia logistics market is no longer defined by a single network but by a series of specialised regional systems working in concert. The east coast powers imports and consumption, the west anchors exports, the north expands trade reach, and the centre ensures continuity across distances.

The industry’s evolution is shifting from expansion to optimisation focusing on visibility, automation, and carbon reduction rather than sheer volume. Each region contributes uniquely to this transformation, reinforcing the system’s collective resilience. Ken Research estimates Australia’s logistics market exceeded AUD 125 billion in 2024, growing approx 5.2 % CAGR through 2030.

In 2025 and beyond, Australia’s logistics advantage will be built region by region — where digital infrastructure, regional investment, and sustainable freight form the foundation of national competitiveness.

Related tags

Logistics and Shipping

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.