Global OTT Market Outlook: USD 236B Today, 16.7% CAGR, and the Regions Defining Streaming Growth

Ken Research

December 19, 2025 - 5 min read

December 19, 2025

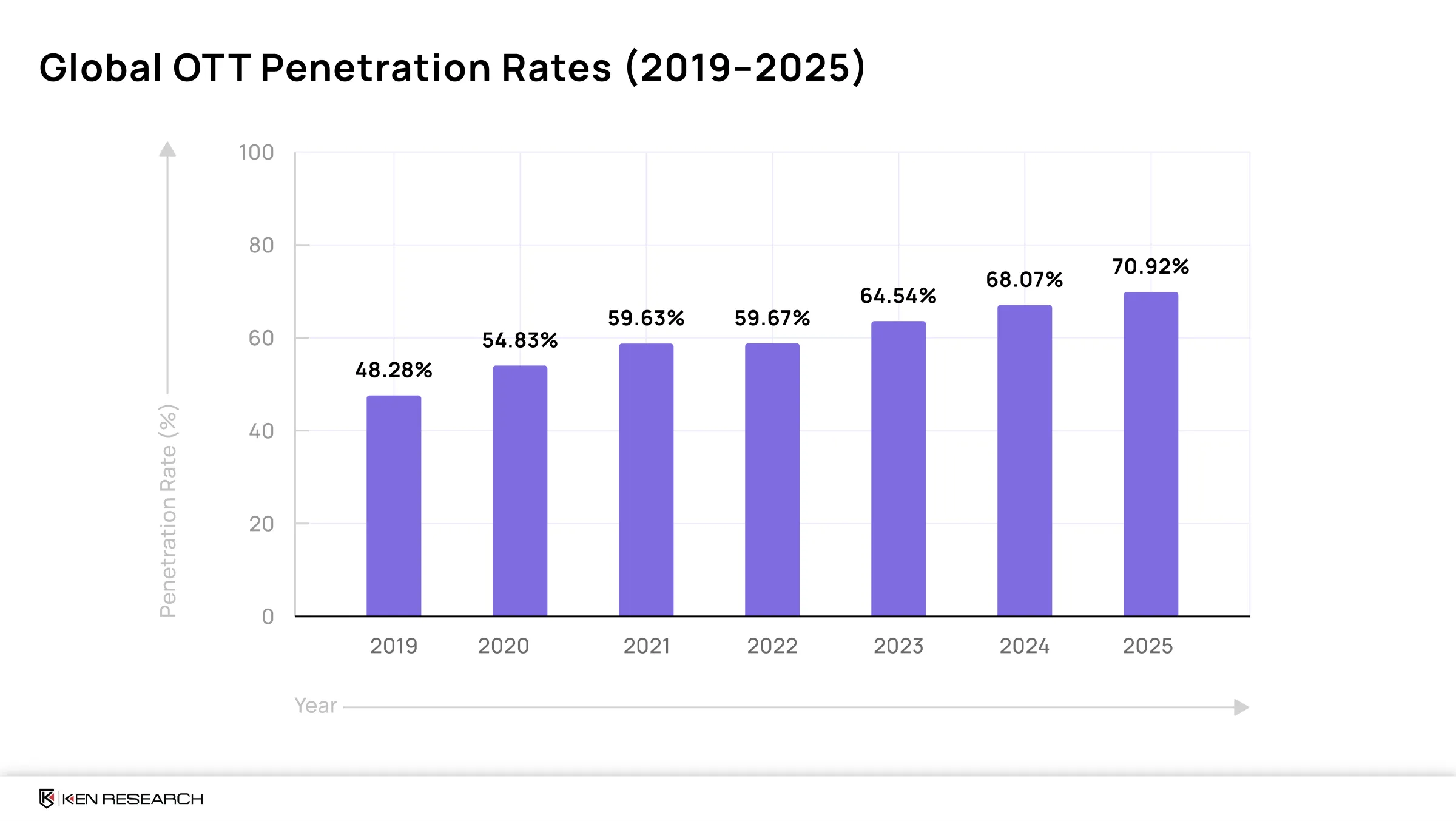

by Ken ResearchThe global Over-The-Top (OTT) video market continues to expand steadily, supported by digital access, rising broadband penetration, and diversified monetisation models. Global OTT penetration has strengthened consistently, rising from 48.28% in 2019 to 64.54% in 2023, and is projected to reach approx. 80% by 2030, reflecting a decisive shift in global video consumption behaviour.

Moreover, Global OTT Platform Market, valued at USD 236 billion in 2024, is projected to reach USD 596 billion by 2030, growing at a robust CAGR of 16.7% during 2025–2030.

India — Strong User Base Supported by Accelerating Digital Infrastructure

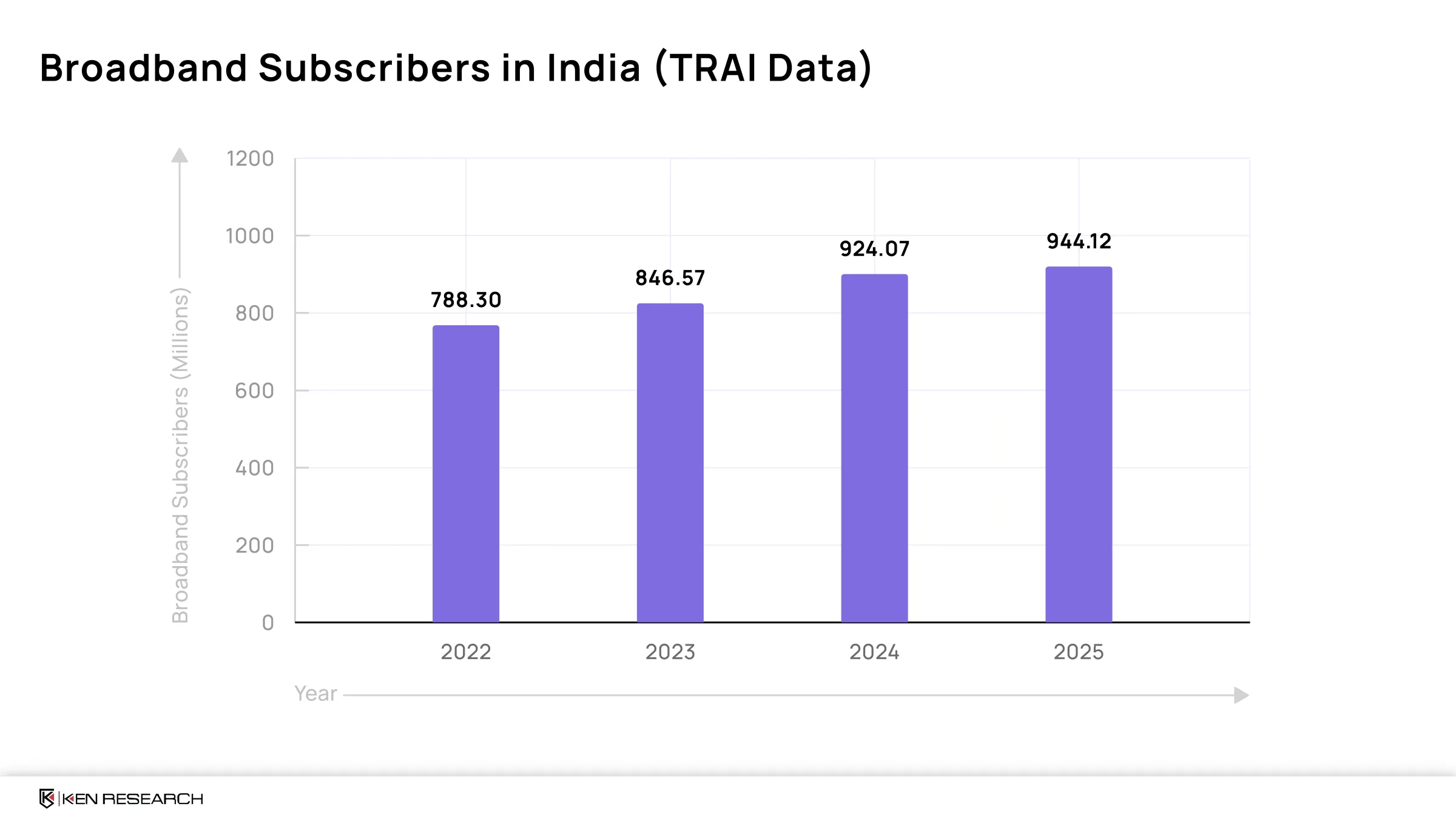

India remains one of the largest video-consuming markets globally. The Indian OTT market was valued at approx. USD 3.5 billion in 2024, supported by widespread smartphone access and rapidly improving data affordability. The Telecom Regulatory Authority of India in 2023 recorded over 850 million broadband users, providing a strong foundation for streaming penetration. The data shows that the total number of internet subscribers increased from 954.40 million at the end of Mar-24 to 969.10 million at the end of Mar-25 with a yearly rate of growth of 1.54 %.

India’s user base is large and diverse, but publicly verified ARPU data is limited. Industry consensus from multiple reports places India’s OTT Average Revenue Per User (ARPU) at approx. USD 9–12 per year, significantly below Western benchmarks. This low ARPU environment influences content investment models. While exact production budgets are proprietary, industry discussions indicate that Indian originals are typically produced at substantially lower per-hour costs than Western markets, enabling high-volume content pipelines.

India’s long-term trajectory is further supported by next-generation network expansion. The GSMA in 2024 projects Fifth-Generation (5G) mobile connections in India to surpass approx. 900 million by 2030, enabling higher-quality video consumption and premium-tier adoption.

Southeast Asia — Revenue Growth Strengthened by Rising Digital Payments and Premium Adoption

Southeast Asia continues to benefit from fast-growing digital adoption across Indonesia, Thailand, Vietnam, Malaysia, and the Philippines. According to Ken Research, Southeast Asia’s OTT video market generated over USD 3 billion in 2023, with strong momentum in subscription and advertising-supported formats.

While regional ARPU datasets suggest ARPU uplift of approx. 10–15% between 2021 and 2024, driven by premium tier upgrades, improved broadband access, and deeper payment-wallet adoption. Subscription growth remains healthy, supported by expanding mobile-first viewing and the increasing distribution of local-language originals.

Content production budgets in Southeast Asia vary widely and are not publicly disclosed. Multi-market content distribution remains a competitive strength, allowing platforms to amortise production costs across multiple ASEAN markets, enhancing return on investment.

Middle East & North Africa (MENA) - Premium Pricing Supported by High 5G Penetration

The MENA region presents a structurally unique OTT environment. KEN Research (2024) estimates that the MENA video-on-demand market will reach USD 1.07 billion in 2024, driven by rising broadband adoption and a strong.

Projections covering multiple countries indicate that the OTT sector across key markets such as Saudi Arabia, the United Arab Emirates (UAE), Egypt, and Morocco are expected to surpass USD 1.5 billion by 2027.

Connectivity quality remains a major differentiator. The International Telecommunication Union in 2023 ranks Saudi Arabia and the UAE among the top 10 countries globally for average 5G speeds, enabling smoother premium-tier adoption.

While consolidated ARPU data is limited publicly, paid OTT ARPU in Gulf Cooperation Council (GCC) markets at approx. USD 5–10 per month, supported by a stronger willingness to pay for premium Arabic and international content.

United States: High Monetisation Levels Countered by Rising Cost Pressures

The United States (U.S.) remains the world’s most mature OTT economy as the U.S. home and mobile entertainment market—including streaming video—generated USD 43.1 billion in 2023. The U.S. also maintains the highest revenue density, supported by high ARPU levels, diversified pricing tiers, and robust advertising markets.

Content budgets in the U.S. are substantially higher than Asian or MENA markets. Public disclosures show that premium episodic productions can exceed USD 15–20 million per episode for flagship titles on leading platforms. This contributes to rising margin pressure across the sector, intensifying the shift toward ad-supported tiers, licensing rationalisation, and cost-disciplined content strategies.

Europe — Sustained Growth Supported by Local-Language Investment

The European OTT market remains strong, supported by multilingual content ecosystems and rising connectivity. According to the European Audiovisual Observatory (2023), Europe counted over 140 million subscription video-on-demand (SVOD) subscriber. The European OTT video market to reach Euro (EUR) 30.6 billion in 2024, with continued expansion across Western and Northern Europe through 2030.

Europe’s structural costs remain elevated due to localisation, rights fragmentation, and regulatory compliance. However, increased investment into local-language originals continues to strengthen regional engagement and retention.

Comparative Insight — Regional OTT Dynamics Are Diverging Sharply

India’s OTT sector delivers 500 million video users but generates only USD 9 per user annually, creating the world’s widest scale-to-ARPU gap. Southeast Asia achieved USD 3.9 billion in 2024, supported by premium-tier upgrades that increased ARPU by approx. 10–15%. MENA is set to exceed 27 million subscriptions by 2025 and benefits from world-leading 5G availability in Saudi Arabia and the UAE. The U.S. leads monetisation with USD 231 in annual household streaming spend, enabling blockbuster budgets above USD 20 million per episode. Europe, projected to reach Euro (EUR) 38.4 billion in OTT revenue by 2029, is increasingly shaped by rising investment in local-language productions. These contrasts indicate that emerging regions hold the greatest expansion headroom, while mature markets prioritise sustainability over scale.

Ken Research Insight — Where Global Streaming Momentum Is Heading Next

India, Southeast Asia, and MENA are positioned to drive the next decade of OTT expansion. Their momentum stems from rising connectivity, deepening local-language ecosystems, and monetisation structures tailored to diverse user bases. Meanwhile, the U.S. and Europe are entering a margin-discipline era defined by ad-tier adoption, selective content spending, and tighter operational controls. Across all regions, the defining determinant will be how effectively platforms balance content cost with ARPU, shaping sustainable streaming trajectories through 2030 and beyond.

Related tags

Media and Entertainment

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.