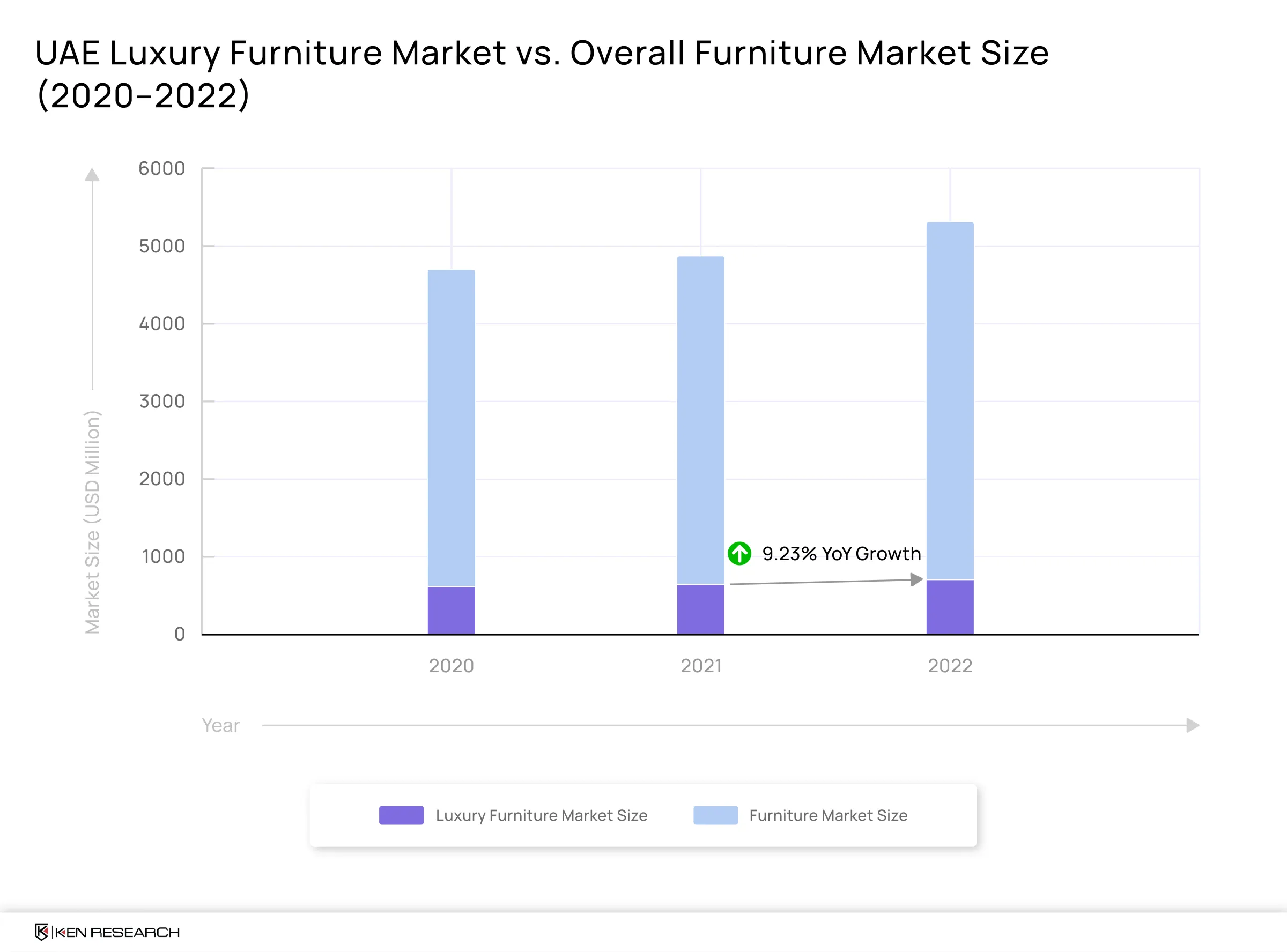

UAE’s $ 802 Million Luxury Furniture Market Set for Demand Surge Amid 30% Rise in UHNWIs

Ken Research

February 27, 2026 - 13 min read

February 27, 2026

by Unnati MiglaniThe UAE luxury furniture market, valued at approximately USD 802 million, is entering a new growth phase driven by a rising high-net-worth resident base and ongoing premium real estate development. Increased affluence, continued migration of millionaires, and the expansion of ultra-prime villas, branded residences, and luxury hotels are fueling demand for bespoke, design-led furniture. Consumer preferences are shifting toward customisation, exclusivity, and curated craftsmanship.

Simultaneously, the UAE’s e-commerce sector, projected to surpass USD 13.27 billion by 2028, is redefining how premium brands reach high-end consumers. Future growth will hinge less on standalone showrooms and more on integrated omnichannel strategies, tailored offerings, and strategic brand positioning within high-income corridors. Companies that align closely with real estate pipelines, develop phygital engagement models, and deliver differentiated craftsmanship are best positioned to capture long-term demand in this evolving market.

Why is the demand for luxury furniture flourishing in the UAE?

Rising Millionaire Base and Wealth Inflows Strengthening the Demand

As incomes and private wealth expand in the UAE, demand for luxury furniture is structurally strengthening. The resident base of USD millionaires crossed 240,000, up roughly 13,000 from 2024. Alongside domestic wealth creation, inbound wealth migration remains a major tailwind - the UAE welcomed about 7,200 relocating millionaires in 2024 and is projected to attract around 9,800 net incoming millionaires in 2025. The UHNWI population is set to increase by 30% by 2028. With unemployment hovering near 2%, the market’s high-income demand base remains resilient—supporting sustained spend on luxury housing, bespoke interiors, and premium furniture. Reports also suggest that only 9% of the UAE’s population lived below 50% of medium income as of 2018, and the number has reportedly decreased since.

Get in-depth market insights on the UAE’s luxury furniture market –Download Ken Research’s free Sample Report

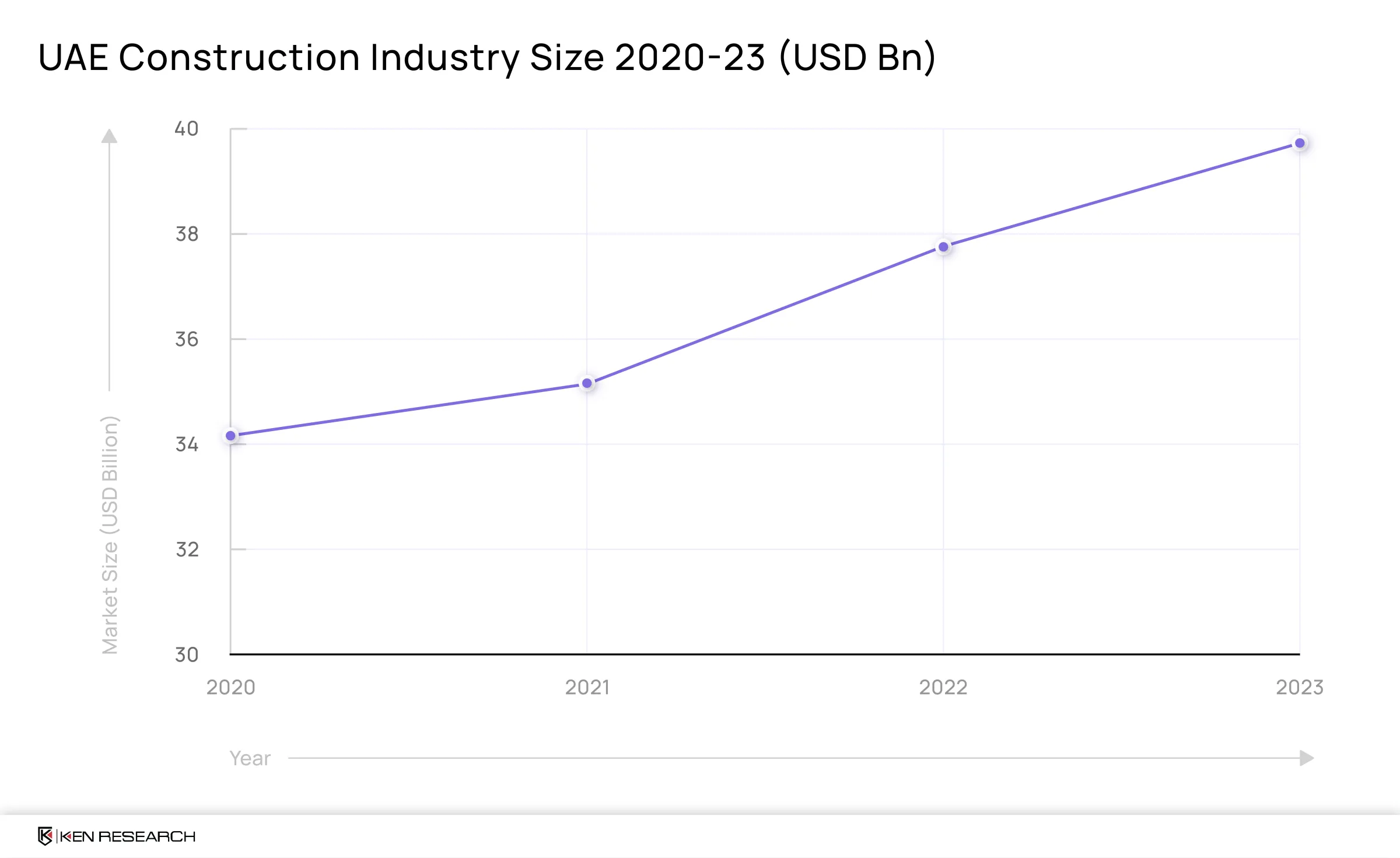

Construction Momentum and Premium Infrastructure Expansions

UAE’s construction market has shown promising growth in recent years. Based on Ken Research’s analysis, Residential projects drove almost 60% of the construction market, while 58% of the total residential construction remained concentrated in Dubai as of 2023.

The UAE’s expanding pipeline of branded luxury residences and ultra-premium hospitality assets is reinforcing demand for high-end furniture and bespoke interiors. A new cycle of luxury master developments across Dubai, Abu Dhabi, and Ras Al Khaimah is approaching phased completion between 2025 and 2028, setting the stage for a coordinated surge in premium villas, branded residences, and penthouses that will underpin sustained demand for high-end furniture and interior solutions.

The Dubai Creek Harbour, with nearly 40,000 planned residential units, and the Mohammed Bin Rashid City, offering over 26,000 units alongside a substantial hospitality component, are being delivered in phases, expanding high-end urban supply. At the same time, ultra-prime hubs such as Palm Jumeirah and City Walk remain highly sought after, with new luxury launches and phased expansions continuing into 2027–2028. Sustained absorption across these corridors is reinforcing demand for penthouses, luxury apartments, and expansive villas—driving momentum in premium interior fit-outs and luxury furniture procurement.

On Saadiyat Island, led by Aldar Properties, the 27 sq km masterplan integrates thousands of beachfront villas and apartments with luxury hospitality and cultural assets, with additional branded residences scheduled for delivery through 2026–2028.

In Sharjah, Al Zahia, developed by Majid Al Futtaim, spans approximately 1 million sq m and is designed for around 12,000 residential units, combining villas, townhouses, and apartments alongside City Centre Al Zahia, with phased completion targeted for 2025–2027.

Complementing these, Mercedes-Benz Places by Binghatti represents a landmark branded residence project valued at roughly USD 8 billion, spanning over 10 million sq ft with more than 13,000 residential units, targeted for delivery around 2027–2028.

Growing Penetration of Global Brands

Global luxury brands operate under inherently high CAPEX and OPEX structures, particularly in premium urban markets such as Dubai, where flagship retail rents, fit-out costs, and operating expenses are elevated. Their continued entry and expansion under these cost conditions reflects confidence in the depth of affluent demand, premium absorption capacity, and long-term commercial viability of the market, reinforcing the structural growth potential of the UAE’s luxury furniture segment.

Italian luxury design houses are expanding their physical footprint in the UAE – Poltrona Frau operates dedicated showrooms in upmarket locations like the Mall of the Emirates and Jumeirah Road in Dubai through its partnership with Majid Al Futtaim, anchoring its premium Italian furniture offering within prime retail environments. Further elevating the European design presence, Paola Lenti inaugurated its first Middle East flagship showroom in Dubai last year, formally extending its global retail network into the region.

At the same time, ultra-luxury automotive lifestyle labels are entering the interiors segment via landmark retail destinations. Bentley Home opened its first dedicated UAE showroom at The Dubai Mall Zabeel in November 2024, marking its standalone retail debut in the Emirates. Shortly after, Bugatti Home launched its first global boutique at the same location, selecting Dubai as the brand’s inaugural retail showcase for its furniture line.

Beyond individual brand launches, Majid Al Futtaim continues to play a catalytic role in strengthening the UAE’s luxury retail ecosystem. The group has expanded its premium portfolio to include brands like Poltrona Frau and has facilitated the regional presence of European labels such as Corneliani and Eleventy across high-footfall luxury destinations, including Mall of the Emirates and Dubai Mall. While Corneliani and Eleventy operate in the fashion segment, their expansion reflects the broader clustering of global luxury categories within concentrated premium retail hubs.

The sustained rollout of international design-led and lifestyle-driven brands backed by institutional retail operators signals continued confidence in the UAE’s affluent consumer base and the long-term trajectory of luxury demand across categories, including furniture and interiors.

Capturing Demand in the UAE’s Luxury Furniture Market – Actionable Insights from Ken Research

The growth in the UAE’s luxury furniture market has been structural. To strengthen their position in this market, brands will need to capitalise on evolving consumer preferences while eyeing major developments in the market to leverage opportunities and long-term relationships that will lock in sustainable growth for both established players and new entrants.

Discover the latest global luxury furniture trends – Download Ken Research’s free Sample Report

A Premium Value Ecosystem Anchored in Customisation and Exclusivity

Ken Research’s Survey insights indicate a structurally strong demand for customisation within the premium furniture segment. Bespoke designs and one-of-a-kind furniture pieces are increasingly preferred by affluent buyers who continue to seek products that reflect individual identity, align with their personal values, and fit in the overall aesthetic of their living spaces. The rising demand for curated living environments creates an opportunity for luxury furniture brands to go beyond standardised offerings, focusing on personalised experiences, bespoke customisation, and community engagement.

Simultaneously, buyers also remain cautious about the after-sales service reliability, indicating a critical gap in the current value proposition. Strengthening after-sales service, warranty management, and responsiveness can boost trust, brand loyalty, and word-of-mouth referrals.

Beyond furniture quality and craftsmanship, competitive pricing and reduced delivery timelines attract hospitality buyers who are often pushed to continuously adapt to evolving design trends. Players that effectively combine design differentiation with operational agility are well poised to capture the majority of the demand for luxury furniture as residential and hospitality segments continue to dominate this market.

Deepening Demand for Italian Aesthetics Across the Premium Market

Ken Research’s studies indicate a structural inclination among consumers towards high-quality Italian furniture. The growing Italian footprint in the UAE’s furniture retail space also continues to validate this growing demand. Majid Al Futtaim is driving Italian expansion by strengthening its offline retail network for Italian brands.

Other Italian brands like Natuzzi Italia have captured a significant share in the UAE’s luxury furniture market, dictated by its premium craftsmanship, rich Italian heritage and designs that align well with the UAE’s luxury-oriented consumer base. In 2024, Natuzzi Italia generated approximately USD 142 million in invoiced sales, reflecting steady demand for high-end Italian furniture globally. The brand has anchored its positioning around comfort-driven design, with a strong focus on modular configurations that align with contemporary luxury living. Its mono-brand showrooms in prime retail corridors, including Sheikh Zayed Road in Dubai and The Galleria, Al Maryah Island in Abu Dhabi, reinforce a controlled and premium brand environment within high-footfall luxury destinations. This direct retail presence in flagship locations supports consistent brand storytelling, strengthening Natuzzi Italia’s positioning within the UAE’s luxury furniture market.

A Strong Phygital Presence to sustain Demand

While the majority of the luxury furniture transactions are closed offline, the UAE’s expatriate-driven population continues to exhibit strong online-first behaviour, strengthening the position of digital channels as central to brand and product discovery.

An integrated online and offline presence is increasingly becoming a strategic imperative for premium furniture brands – a strong digital footprint can help enhance customer discovery, shortlisting and early-stage engagement, combined with a robust offline presence that boosts brand equity, experiential validation and conversion. Since customisation continues to remain popular, integration of 3D virtual visualisation and AR/VR, allowing consumers to experience bespoke outcomes without physically interacting with the product, can help narrow the gap between expectation and delivery, thereby reducing customisation-related friction while enhancing purchase confidence.

Flagship stores in upmarket locations are critical for experiential reinforcement and brand positioning. Leading players such as 2XL Home are pairing digital enablement with experiential retail expansion. The brand’s strong offline footprint in upmarket destinations such as The Galleria, Al Maryah Island in Abu Dhabi and premium retail corridors across Dubai and Sharjah reflects sustained confidence in immersive physical retail. Complementing this, 2XL operates a fully transactional bilingual e-commerce platform offering Buy Now Pay Later and nationwide delivery, reinforcing convenience-led purchasing. Active engagement across social media platforms, including Instagram, Facebook, and LinkedIn, further strengthens customer interaction and brand visibility, demonstrating a structured omni-channel strategy within the UAE’s luxury furniture market.

Targeting High-Growth Corridors

DIFC in Dubai and ADGM in Abu Dhabi are well-established financial districts that bring together offices, residences, hotels, and retail within clearly defined business zones. DIFC hosts over 8,000 registered companies, while ADGM has issued over 11,900 active licences, with more than 3,200 operational entities across financial and non-financial sectors, creating a dense concentration of corporates and high-income professionals where demand for luxury offerings is flourishing. For furniture brands, expanding into these districts is a strategic geographic move to tap steady demand for office fit-outs, corporate housing, and hospitality furniture rather than mass retail sales. Higher entry and operating standards limit low-quality competition in these areas, allowing design-led, contract players to compete on quality, reliability, and long-term relationships, building a defensible presence in the UAE’s premium furniture market.

While demand remains concentrated in Dubai and Abu Dhabi, emerging markets such as Sharjah, Ras Al Khaimah, and Al Ain are poised to gain momentum amid ongoing urbanisation and infrastructure expansion. In Sharjah, the Sharjah Waterfront City is expected to deliver more than 1,500 villas, while Aljada is planned to contribute over 25,000 residential units, reflecting growing developer confidence and strengthening long-term residential demand across these evolving geographies.

Ras Al Khaimah is entering a high-growth development cycle underpinned by large-scale hospitality and mixed-use investments aligned with its Tourism Vision 2030, which targets over 3.5 million annual visitors by 2030. The emirate welcomed approximately 1.35 million overnight visitors in 2025, reflecting steady momentum toward this strategic goal. Anchoring this expansion is the Wynn Al Marjan Island integrated resort, scheduled to open in early 2027, which will significantly enhance the emirate’s luxury hospitality offering. In parallel, the planned Radisson Blu Hotel and Radisson Blu Residences at RAK Central, targeted for 2029 completion, will add further hotel and branded residential inventory to the market.

Sustainability-Led Positioning to Strengthen Brand Appeal

Sustainability is becoming a marker of sophistication among affluent consumers, who now prefer responsible luxury over excess. The UAE’s expat-driven population remains highly influenced by global sustainability trends, creating opportunities for luxury brands to incorporate sustainable practices into their products, operations, and brand communication. Government policies and mandates are also accelerating the integration of sustainability into business operations – the Emirates Green Building Council’s technical guidelines support environmentally responsible standards aligned with the UAE’s broader sustainability agenda, while the Emirates Authority for Standardisation and Metrology (ESMA) has set regulations governing material safety, chemical treatments, and formaldehyde emissions – areas closely linked to furniture manufacturing.

Brands are leveraging sustainability positioning to differentiate themselves and attract consumers. Pottery Barn, a global home furnishing brand operating through its robust online platform in the UAE, aligns with its parent company’s global ESG commitments, including responsible sourcing initiatives across wood and cotton within its brand portfolio. In fiscal 2024, Pottery Barn generated approximately USD 3.04 billion in net revenue, making it one of the largest contributors within the Williams-Sonoma group. As international brands expand in the UAE, sustainability-led positioning and ethically sourced materials are emerging as increasingly important competitive differentiators for players targeting affluent, globally aware consumers.

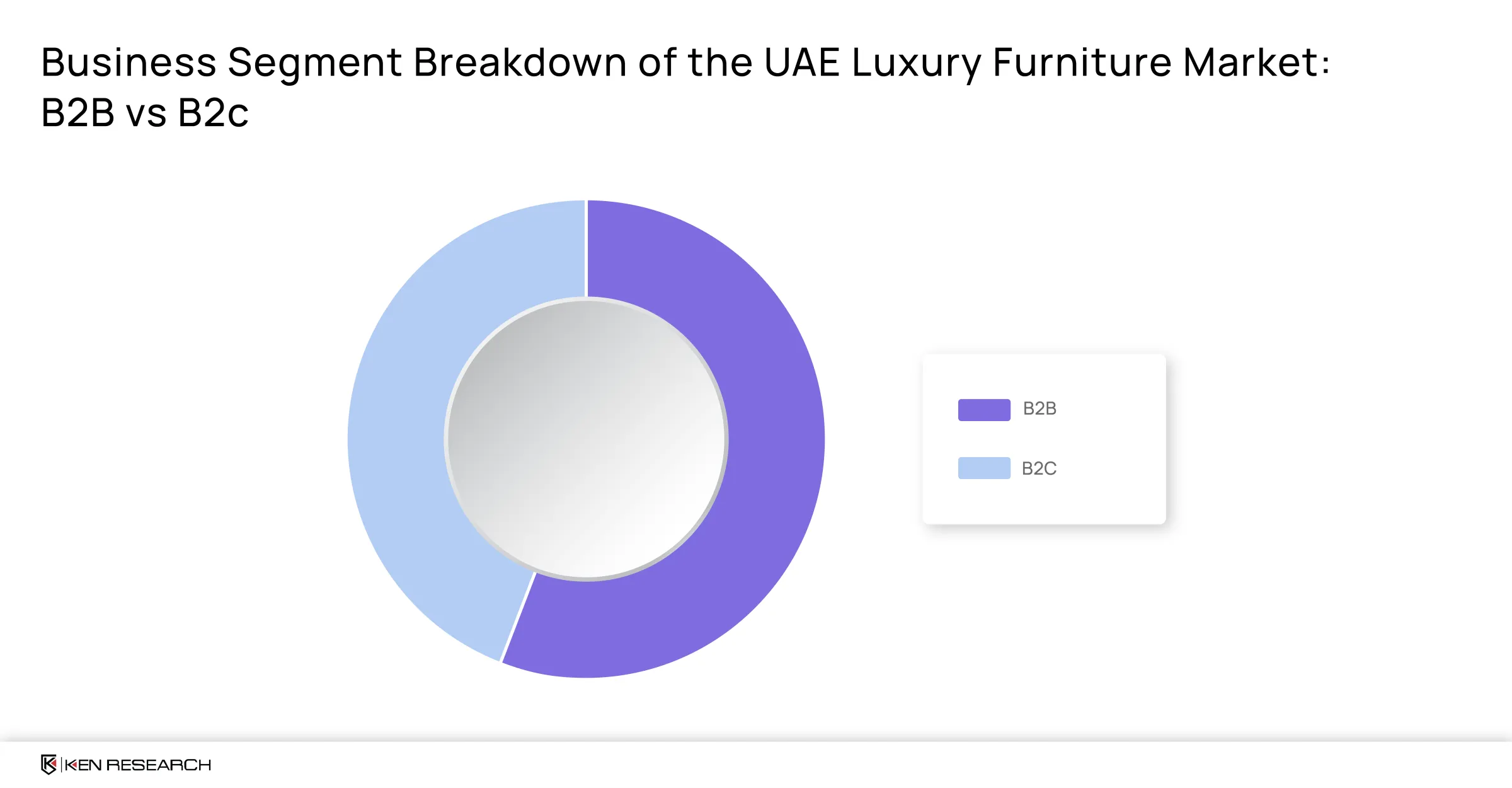

Landing strong B2B Partnerships

With over 60% of total furniture sales in the UAE generated through B2B channels, luxury players pivoting from showroom-led retail toward a structured, upstream demand-capture model embedded within the luxury real estate and hospitality value chain are well-positioned to lock in long-term growth. Securing positioning at the specification stage as a preferred FF&E and turnkey interiors partner, through collaborations with branded residence developers, master-planned communities, and ultra-luxury hospitality operators, can enable brands to embed demand within project pipelines rather than depending on post-handover discretionary purchases.

Market precedents have reinforced the commercial viability of this approach - Natuzzi Italia’s partnership with Peace Homes Development for building the Natuzzi Harmony Residences integrates branded Italian interiors directly into the residential offering, structurally anchoring furniture procurement to property sales. Similarly, Marina Home’s collaboration with internationally renowned designer Kelly Hoppen resulted in one of the brand’s best-selling collections, demonstrating how design-led partnerships can materially enhance brand positioning while driving measurable commercial performance.

Leveraging Local Manufacturing and Cultural Craftsmanship as Competitive Differentiators

High import duties and tariff volatility are increasingly pressuring profit margins for furniture players reliant on overseas sourcing. Currently, more than 70% of furniture sold in the UAE is imported from markets such as China, Italy, Germany, and the United States, exposing brands to currency risk, logistics costs, and policy shifts. As the UAE government continues to encourage and support local manufacturing through industrial diversification initiatives, leveraging domestically produced furniture offers a strategic advantage in both cost control and supply chain resilience.

Beyond operational benefits, local production aligns with evolving consumer preferences. The demand for traditional and artisanal Arabic design is strong, with affluent consumers placing high value on craftsmanship, cultural authenticity, and premium quality. Brands such as KAD Designs are tapping into this segment by blending modular functionality with traditional design craftsmanship. At the same time, as international brands deepen their presence in the UAE, national brands that deliver top-tier quality with globally inspired aesthetics are well-positioned to compete effectively and capture long-term market share.

Conclusion

The UAE luxury furniture market is entering a robust growth phase, supported by rising affluence, an expanding high-net-worth population, and the proliferation of ultra-prime residential and hospitality projects. Demand is increasingly oriented toward bespoke, design-led, and Italian-inspired offerings, with consumers valuing personalisation, exclusivity, and curated living experiences. Brands that strategically align with real estate pipelines, offer integrated omnichannel experiences, and deliver differentiated craftsmanship will be well-positioned to capture sustained demand. Get in touch with our consultants for actionable strategies that promise long-term growth – book a call now!

Related tags

Furniture

Home and Office Furnishings

Consumer Products and Retail

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.