Vietnam Mobile Payments Market at USD 50B Crossroads as Scale Grows but Profits Lag

Ken Research

January 14, 2026 - 10 min read

January 14, 2026

by Khushi RastogiVietnam’s mobile payments market has achieved remarkable scale, with QR codes now common in areas like the Old Quarter and Ho Chi Minh City's District. Transaction volumes reached 9.56 billion in 2024, marking an approximately 30% increase in transaction volume and a 14.4% rise in transaction value compared to 2023. In value terms, NAPAS reported a total transaction value of about USD 2.4 trillion (VND 61.05 quadrillion) in 2024, a scale that underscores how ‘payments work’ even as monetisation lags.

Adoption curves flatten at respectable heights, 77% of urban Vietnamese aged 18-45 use mobile payments monthly, yet profitability remains elusive as per Ken's analysis. MoMo, Vietnam's largest e-wallet with 33 million users, reported USD 130 Mn in revenue in 2024 with a transaction value of 1.4 Mn in 2024. The market sits on unrealised potential locked in transactional loops that generate 2.4 petabytes of behavioural data annually but capture little value from it.

Despite rapid growth, Vietnam's market still lags in monetisation compared to global leaders like India’s PhonePe and China’s Alipay. Both have integrated financial services, such as credit and insurance, into their payment systems. For example, in 2024, PhonePe achieved USD 1.1 billion in revenue, while Alipay processed USD 55 trillion in transactions, with only 8% of their revenue coming from transaction fees. Vietnam's e-wallets, like MoMo, need to shift from a focus on transaction volume to high-margin financial services to unlock greater profitability, following the successful models of India and China.

Payment Infrastructure Was Built for Speed Rather Than Value Creation

Vietnam has established a digital payments system that operates reliably and at scale, with non-cash transactions now firmly integrated into everyday economic activity. In 2024, data released by the State Bank of Vietnam showed that non-cash payment transactions increased 43.32% in volume and 24.23% in value year-on-year, confirming that electronic payments have moved from the margins to the core of Vietnam’s financial system.

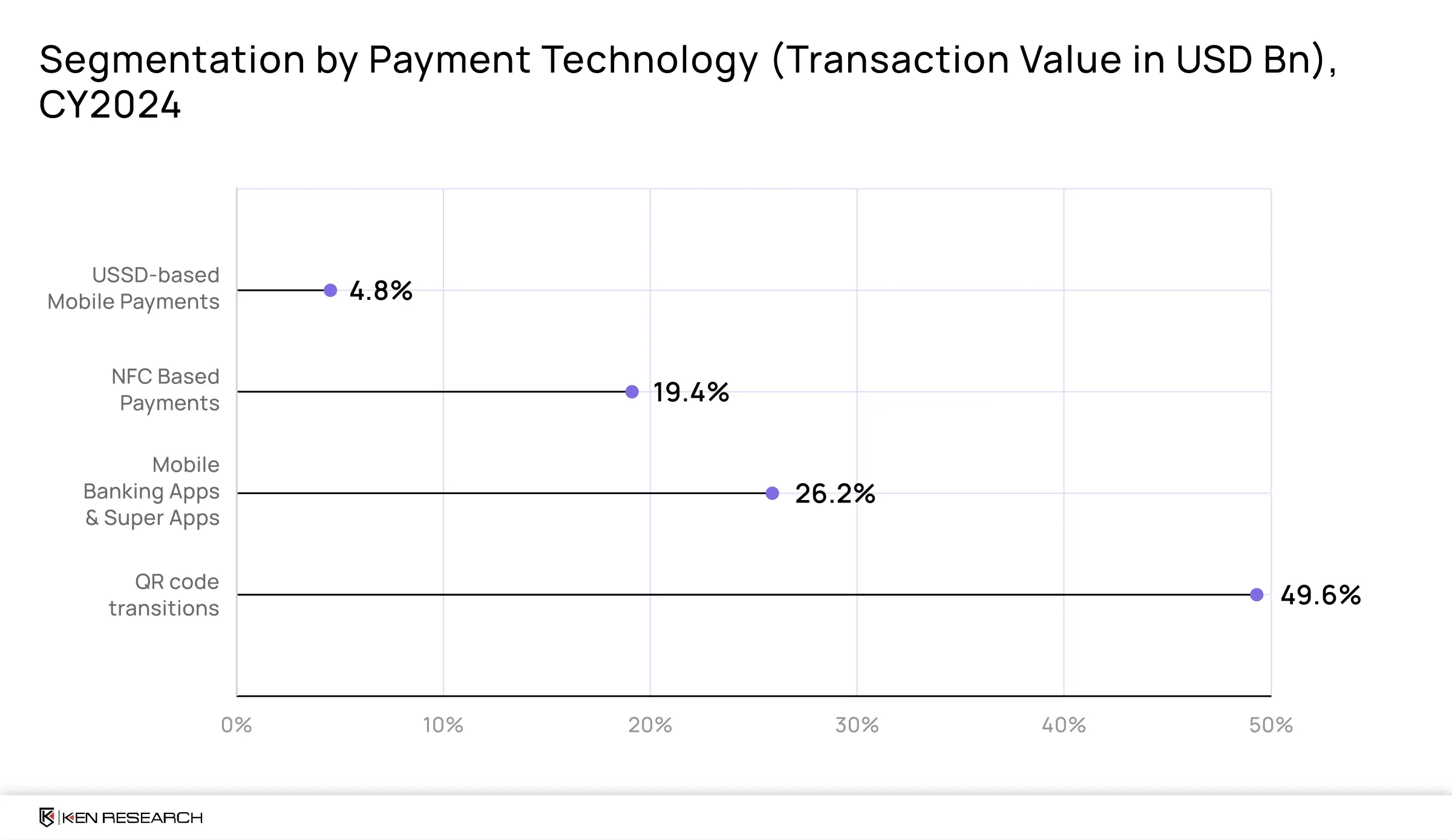

The strongest acceleration in 2024 came from QR-based payments. According to the same SBV data set, QR transaction volumes increased by 61.63%, while transaction value surged by 150.67%, making QR the fastest-growing payment method in the country during the year. This growth extended across channels, with internet-based payments expanding 51.2% in volume and 37.17% in value, and mobile payments increasing 37.37% in volume and 21.79% in value. Over the same period, cash usage continued to decline, as ATM withdrawals fell 16.77% in volume and 5.74% in value, reinforcing that the shift toward digital payments is structural rather than cyclical.

Despite these gains, the underlying limitation of the system has become clearer as scale has increased. Vietnam’s payments architecture has been optimised primarily for transaction throughput rather than post-payment value creation, meaning that efficiency at the rails has not translated into proportional economic returns beyond the point of settlement.

Most Merchants Use Digital Payments Only as a Settlement Tool

Merchant acceptance has expanded rapidly, largely because QR-based payments are inexpensive and easy to deploy. For many small businesses, enabling digital payments required minimal setup, allowing acceptance to scale quickly across retail and services.

By mid-2024, SBV reporting confirmed more than 34 million active e-wallets, out of approx 58 million activated wallets, operating across a highly competitive ecosystem. However, while acceptance has improved checkout convenience, it has not consistently changed how merchants manage cash flow, access credit, or make operational decisions. In most cases, digital payments remain a settlement tool rather than a foundation for deeper financial engagement.

The economic relationship between payment providers and merchants typically ends once the transaction clears, limiting the ability of payments to function as a gateway to broader financial services.

Market Fragmentation, Split Transactions, Data, and Monetisation Potential

Vietnam payments market is structurally fragmented. As of 2024, the country supported 53 licensed payment intermediaries, including 49 e-wallet providers, according to disclosures from the State Bank of Vietnam. This density has accelerated adoption but has also distributed transaction activity across dozens of parallel platforms.

The cost of fragmentation does not appear in transaction failures, which remain rare. Instead, it emerges over time through diluted data quality, weaker customer lifetime value, and limited ability for any single provider to compound insights across the full scope of user activity.

Vast Transaction Data Remains Underused for Credit and Personalisation

Vietnam’s digital payments system now generates vast volumes of transactional data across QR, mobile, and internet channels. The 150.67% increase in QR transaction value in 2024 alone points to a rapidly expanding pool of behavioural information, yet much of this data remains underutilised. Fragmentation across platforms constrains its use for underwriting, personalisation, and financial product development, while downstream services such as merchant credit and working-capital support continue to rely heavily on traditional documentation and collateral. As a result, the ecosystem produces data at scale but lacks the integration required to consistently convert that data into insights or monetisable financial relationships.

The India Divergence: When Public Infrastructure Beats Private Competition

India didn't build a payments market, but it built payments as a public utility and then let the market build on top. UPI processed 172 billion transactions worth USD 2.88 trillion in 2024, with 0 merchant discount rates on person-to-merchant transactions

The UPI Architecture Advantage

Unified Payments Interface transformed interoperability from an ambition into a foundational infrastructure. A single QR code works across banks and apps, enabling merchant adoption to scale to 50 million acceptance points, 18 times Vietnam’s density, while transaction success rates rose from 87% in 2019 to 98.3% by 2024.

PhonePe, with 550 million users, achieved profitability by 2024 with USD 1.1 billion in revenue, not from transaction fees (which are zero on UPI) but from adjacent services. Their credit book reached USD 2.1 billion by offering instant merchant loans using cross-platform payment data. Insurance penetration among PhonePe users hit 23% versus the 3.7% national average, while Google Pay India reports USD 0.8 million in FY24 profit through convenience fees and ads.

Competing payment rails mean competing for merchant acceptance, as VNPay, ZaloPay, and MoMo collectively spent an estimated USD 180 million on merchant acquisition in 2023. Energy spent on distribution doesn't flow to product innovation. The market remains stuck optimising the transaction layer, while India moved to monetising the relationship layer, where operating margins reach approximately. 28-42% versus Vietnam's payment providers at 4-8%.

Standardisation Allowed India to Monetise Relationships Instead of Transactions

When payment infrastructure commoditises, value creation shifts. India's lending to digital merchants grew from USD 800 million in 2021 to USD 8.4 billion by 2024, a 10.5 times expansion enabled by interoperable payment data. Credit models built on UPI transaction history show 34% lower default rates than traditional SME loans.

Vietnam's fragmented rails make each of these harder, as a merchant processing payment through three different wallets generates three incomplete data trails. Credit models stay siloed within each provider's universe. Merchant finance requires proprietary scale, MoMo would need to reach 60%+ market share to build statistically increase credit models, versus India, where any fintech can tap into UPI's universal data layer.

China's mobile payments market doesn't exist as a standalone category. It dissolved into super-apps where payments are embedded in an infrastructure that is invisible, instant, and assumed. Alipay and WeChat Pay processed USD 55 trillion in 2024, but transaction fees contributed only 8% of Ant Group's USD 28 billion revenue. The remaining 92% came from ecosystem monetisation credit (38% of revenue), wealth management (31%), and merchant services (23%).

The average Alipay user generates USD 187 annually in platform revenue, not from paying, but from borrowing (USD 47 per user from Huabei credit), investing (USD 82 per user in the Yu'ebao money market fund), and insurance (USD 31 per user). Payment frequency (43 transactions monthly) drives credit eligibility. Payment amounts inform investment recommendations. Payment merchant mix shapes insurance offerings.

Vietnam's payment apps remain exactly that, payment apps, as MoMo's ARPU sits at USD 5.20 annually, with 94% from transaction fees and cashback partnerships. ZaloPay, integrated within Zalo's messaging app with 75 million users, generates USD 4.80 ARPU, still primarily transaction driven and only 8% of Vietnamese mobile payment users have accessed credit through their payment app, versus 67% in China's mature ecosystem.

The infrastructure dividend

Ant Group's operating margin reached 42% in 2024 because payments became the zero-marginal-cost data layer feeding high-margin financial services. Customer acquisition cost for credit products dropped to USD 0.80 customers were already using payments. Underwriting costs fell 73% using payment behaviour versus traditional credit bureaus.

Vietnam’s Standalone Payment Apps Face Structural ARPU Limitations

Vietnam processes 27 million daily payment transactions, generating 47 million data points, but only 3.2 million credit decisions annually leverage this data, a 14:1 ratio of data generated to data monetised. E-commerce platforms like Shopee and Lazada integrate payments but don't share the financial relationship with the underlying payment providers. Food delivery apps Grab and Shopee Food facilitate 8.3 million weekly payment transactions but control the customer data, leaving payment processors as invisible infrastructure.

The result: Payments remain a utility layer that others leverage while payment providers capture thin transaction margins. Grab's fintech ARPU reached USD 12.40 in Vietnam by 2024, nearly 2.4 times higher than standalone payment providers, because they monetise the transportation and delivery context around payments, not just the payment itself.

Five Structural Gaps Continue to Constrain Vietnam’s Payments Market

Interoperability Fragmentation Limits Total Addressable Usage

Fragmentation caps total addressable usage, as State Bank research found that 31% of potential digital payment transactions still occur in cash because the customer's preferred app isn't accepted. Each additional QR code at merchant checkout adds 2.3 seconds to transaction time and increases abandonment probability by 4.7%.

Lack of Monetisation Keeps Revenue Growth Below Profit Thresholds

Transaction volume without margin expansion is revenue without profit. Vietnam's payment providers collectively generated USD 940 million in revenue in 2023 against an estimated USD 820 million in operating costs, a collective 12.8% operating margin. By comparison, India's mature players operate at 28-31% margins, and China's ecosystem leaders at 38-42%. The gap represents USD 260-280 million in foregone annual profits—the cost of efficiency without a monetisation strategy.

Limited Merchant Value Creation Drives High Churn and Low Stickiness

Despite 2.8 million merchants accepting digital payments, only 340,000 (12%) report that payment acceptance improved business operations beyond customer convenience. Working capital access remains unchanged for 89% of digitally active merchants. Payment providers run expensive merchant acquisition programmes Merchant churn rates average 23% annually and stop displaying QR codes when promotional periods end, suggesting acceptance was incentive-driven, not value-driven.

Urban-Centric Growth Creates a Hard Ceiling on Market Expansion

Mobile payments optimised for urban density and digital literacy. Urban Vietnam generates 86% of the transaction volume. Semi-urban markets show 34% mobile payment penetration versus 67% in cities. Rural areas sit at 18% penetration. Market saturation in core segments, while 62% of the population remains underserved, means Vietnam's addressable market is artificially constrained. If semi-urban and rural adoption matched urban levels, transaction volume would reach 28 billion annually, a USD 330 billion GMV opportunity currently untapped.

Trust Constraints Limit High-Value Transactions and Cross-Sell of Financial Products

Average mobile payment transaction value hovers at USD 12, well below the USD 31 average in India and USD 43 in China. Transaction value distribution reveals the constraint: 73% of transactions fall below USD 10, and only 4% exceed USD 50. User surveys cite fraud concerns (41% of respondents), data security worries (38%), and unclear dispute resolution (33%) as barriers to higher-value transactions. This trust ceiling limits payment providers' ability to move upmarket into financial services credit products, see 67% application abandonment rates, and wealth features attract only 2.1% of payment app users, versus 31% in China's trust-established ecosystem.

Future Winners Will Convert Transactions into Financial Relationships

Vietnam has successfully developed a mobile payments system with 99.2% uptime, processing 27 million transactions daily. While these figures highlight the infrastructure's strength, the market has yet to fully capitalise on its potential. With 9.8 billion transactions annually and 47 million data points daily, the key question remains: Can these transactions be converted into profitable financial relationships?

Looking at India and China offers valuable lessons as India’s UPI, in 2024, processed USD 2.4 trillion in payments, supporting USD 8.4 billion in merchant lending and USD 3.2 billion in consumer credit. This success is driven by interoperable infrastructure, which allows for specialised monetisation beyond just payment processing. Similarly, China’s Alipay generates USD 187 in average revenue per user (ARPU) through an integrated ecosystem of financial services, such as credit, investments, and insurance, with profit margins on these services reaching 38-42%.

In contrast, Vietnam’s mobile payment platforms, like MoMo, generate just USD 5.20 in ARPU, largely from transaction fees. While processing billions of transactions, these platforms have not yet integrated broader financial services to create high-margin value.

As competition intensifies, Vietnam’s market faces shrinking margins, with operating margins compressing from 15% in 2021 to 12.8% in 2023. The market’s future will reward those who can transform transactions into financial relationships, driving long-term profitability rather than relying on transaction volume alone.

Related tags

Payments

Banking

Banking Financial Services and Insurance

Get started

We've helped companies around the world future-proof

their businesses - and we can do the same for you.